ILCB - 4 Reasons A Long Recession Is Likely To Start Soon

2023-07-15 00:36:23 ET

Summary

- The article suggests that a recession is likely to start within the next year, based on economic theory and history.

- I discuss the Austrian Business Cycle Theory, which states that monetary expansion can lead to a misallocation of resources, causing a boom and bust cycle.

- The article also points to four indicators of an impending recession: rising short-term interest rates, slowing money supply growth, slowing bank deposit growth, and an inverted yield curve.

After investor fears of high inflation and rising interest rates leading to a recession caused a significant fall in stock prices last year, this year has been characterized by growing investor optimism for a “soft landing” and no recession, which has contributed to rising stock prices.

But is this growing optimism and rise in stock prices justified? Are we out of the woods with regard to recession risk?

Based on my understanding of economic theory and history, I think the answer to these questions is no. In fact, I think a recession is highly likely to start within the next year, if it hasn’t done so already.

In this article, I first discuss the primary cause of the “boom and bust” business cycle. Then I detail four key economic factors that have led to recessions in the past and are pointing to another recession now.

Cause Of The Boom & Bust Business Cycle

The boom and bust business cycle of economic expansions and recessions has been a recurring feature of our economy since the Industrial Revolution. The primary cause of the business cycle has been a source of debate for over a century. Over the years, the business cycle has been blamed on everything from random fluctuations in “overproduction” and “overoptimism” to “underconsumption” and “overpessimism”. But these theories do not explain what causes the fluctuations in the first place.

I believe the best explanation — and the one most useful for investors — is the business cycle theory developed by Austrian economist Ludwig von Mises over a century ago. His student, F.A. Hayek, won the 1974 Nobel Prize in economics for developing this theory in the 1930s. In honor of these two Austrian economists, this theory is called “Austrian Business Cycle Theory” or “ABCT” for short.

In the words of the Nobel Prize committee :

von Hayek’s contributions in the field of economic theory are both profound and original. His scientific books and articles in the twenties and thirties aroused widespread and lively debate. Particularly, his theory of business cycles and his conception of the effects of monetary and credit policies attracted attention and evoked animated discussion. He tried to penetrate more deeply into the business cycle mechanism than was usual at that time. Perhaps, partly due to this more profound analysis, he was one of the few economists who gave warning of the possibility of a major economic crisis before the great crash came in the autumn of 1929.

von Hayek showed how monetary expansion, accompanied by lending which exceeded the rate of voluntary saving, could lead to a misallocation of resources, particularly affecting the structure of capital. This type of business cycle theory with links to monetary expansion has fundamental features in common with the postwar monetary discussion."

In a nutshell, ABCT states that when money is created out of thin air by commercial banks in the form of new loans (aided by Federal Reserve monetary policy in the US for the past 110 years), it leads to an artificial lowering of interest rates. This new money available at lower interest rates encourages people to borrow the money to fund investment projects that were previously unprofitable at higher interest rates. This is the “boom” phase of the business cycle…the phase we all like!

But at some point, typically due to rising price inflation from the new money creation, interest rates begin to rise and money supply growth begins to slow. Then these new marginal projects are shown to be unprofitable and not able to be completed, since the new money did not create new scarce resources to complete the projects. This leads to the “bust” phase of the business cycle…the phase none of us like!

Based on this business cycle theory and historical data, below I discuss four reasons why I believe a long recession is likely to start soon.

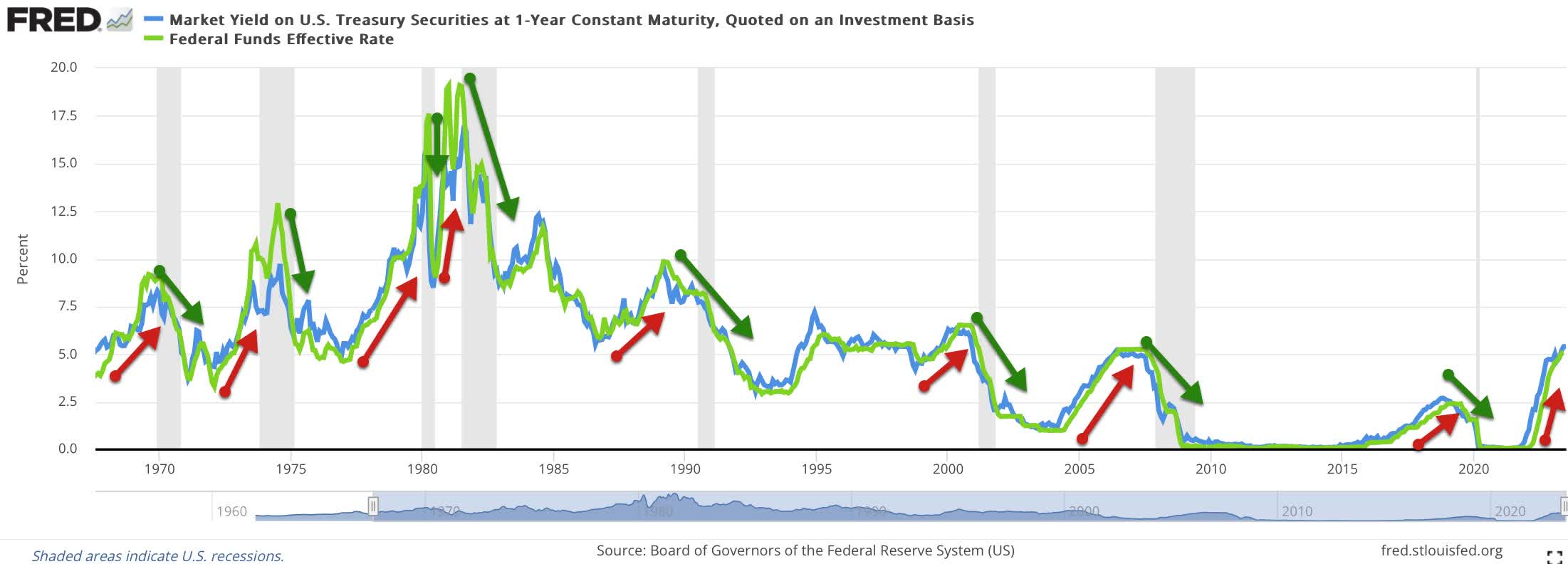

Rising Short-Term Interest Rates Lead To Recessions…

Consistent with ABCT, every recession in modern times has been preceded by a significant rise in short-term interest rates.

As shown in the chart below, all eight of the recessions since the late 1960s (shaded gray) have occurred after a significant rise in short-term interest rates, such as the 1-Year Treasury rate in blue and the Federal Funds rate in green. Since interest rates lead the economy with long and variable lags, historically there has been a wide range of one to three years before rising interest rates lead to a recession.

{kind=link}

Short-term rates have been rising for the past 16 months, which suggests a recession may have already started or is likely to start anytime in the next year or two.

As the chart also shows, the Fed typically raises the Federal Funds rate above short-term market-driven interest rates, such as the 1-Year Treasury rate, before cutting rates. With the current 3-Month Treasury rate at 5.47% and the 1-Year Treasury rate at 5.27%, the Fed is likely to raise the Federal Funds rate by at least another 0.25% to 0.50% from the current effective rate of 5.08%.

Another fact the chart shows is that short-term rates typically fall during, or even before, recessions start. For example, short-term rates started falling before the recessions of the early 1990s, early 2000s and 2008-2009, but that did not prevent those recessions from occurring. Again, interest rates work with a lag. The damage done by the prior rise in short-term rates led to the recessions, while the subsequent fall in rates helped lead to the recovery after the recessions.

Importantly, short-term interest rates are still rising and have not yet begun to fall.

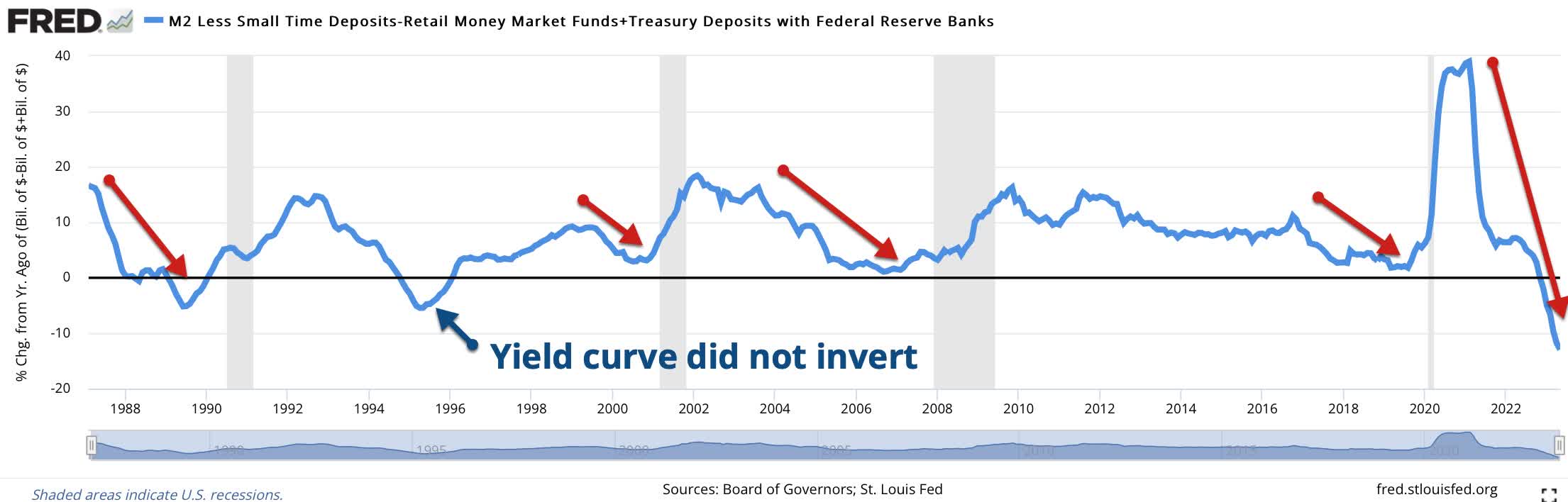

…As Does Slowing Money Supply Growth…

As interest rates rise, that causes loans to be more expensive, which lowers loan demand. Less bank lending leads to less new money creation, which leads to slowing money supply growth. Less money supply put pressure on marginal borrowers and marginal investment projects, which eventually leads to a recession with bankruptcies, layoffs, etc.

Based on the work of Austrian School economists such as Murray Rothbard and Joseph Salerno, we define money as the most liquid monetary assets that can be immediately used to buy goods and services. This includes M2 less small time deposits and retail money market funds, plus Treasury deposits at the Fed.

As shown below, money supply growth slowed before every recent recession. Money supply growth contracted in the mid-1990s, but that did not lead to a recession, likely because the yield curve did not invert, which I discuss below. Note that money supply has currently fallen 13% year-over-year, the largest decline since the Great Depression of the 1930s. Based on prior history, this does not bode well for future economic activity.

{kind=link}

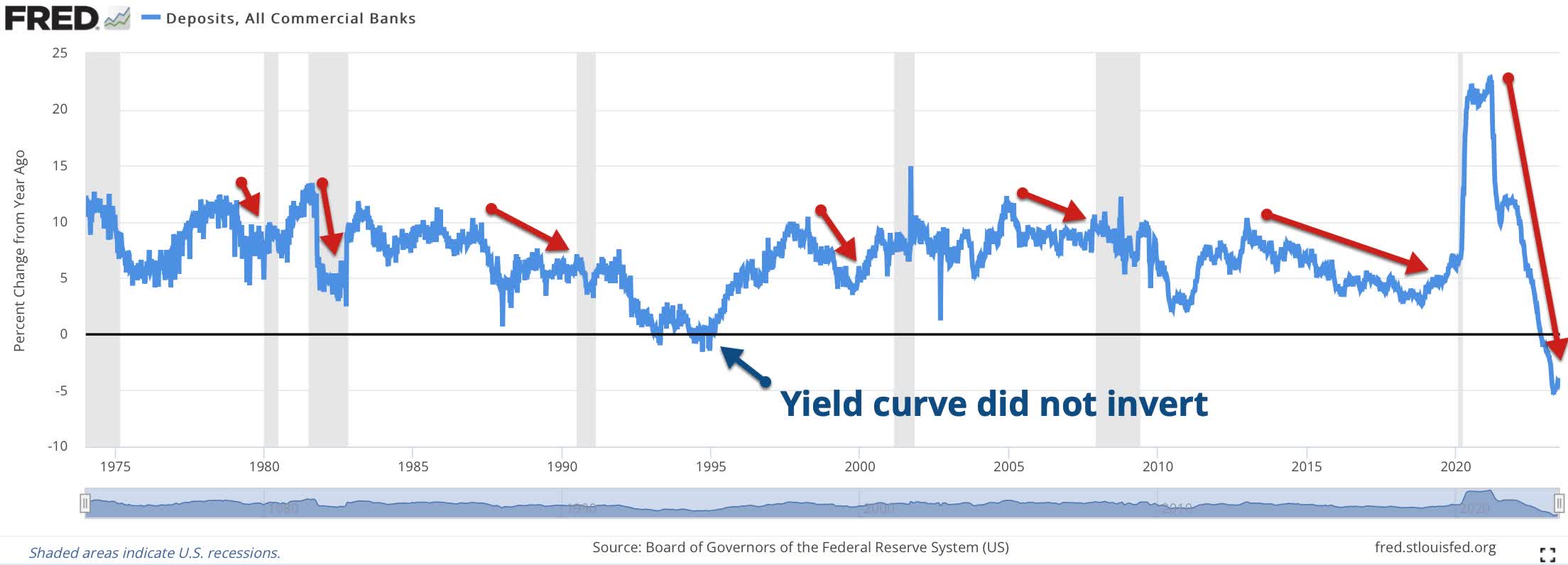

…And Slowing Bank Deposit Growth…

Bank deposits are a component of the money supply. Like the money supply, bank deposit growth typically slows heading into a recession. Also like the money supply, it is very unusual for bank deposits to actually decline. But due to the rapid rise in short-term rates recently, bank deposits are declining 4% year-over-year, as shown below. This decline is unprecedented in recent decades. It is being driven by people seeking out higher-yielding ways to store their money, such as in Treasury bills and money market funds.

{kind=link}

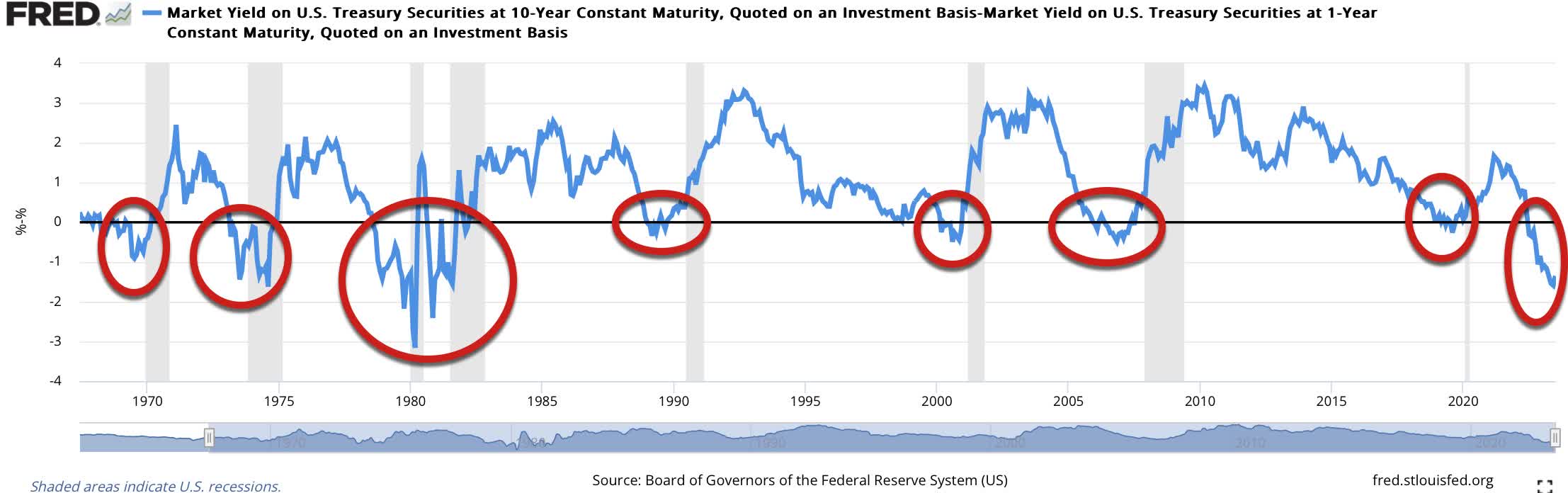

…And An Inverted Yield Curve

The chart below shows the yield curve spread between the 10-Year Treasury rate and the 1-Year Treasury rate. When the 1-Year Treasury rate has risen to a level above the 10-Year Treasury rate, which is unusual, that is called an “inverted yield curve”. Recessions typically follow an inverted yield curve, particularly because inverted yield curves discourage bank lending and new money creation, since banks lose money borrowing at short-term rates that are higher than the long-term rates they lend at.

{kind=link}

These recessions lagged yield curve inversions by an average of 12 months, with lags ranging from 6 to 22 months.

The 10-Year/1-Year yield spread first inverted 12 months ago, so a recession is on schedule to start soon, if it hasn’t done so already. But it could also start many months from now. For example, the yield curve inverted about 12 months before the early 2000s recession, 16 months before the early 1980s recession, 17 months before the early 1990s recession and 22 months before the 2008-2009 recession.

As shown below, this yield curve inversion is the deepest in over 40 years. While the depth of the inversion is not predictive, the longer the inversion lasts, the longer the recession typically lasts.

For example, the 22 months of inversion preceding the Great Recession of 2008-2009 caused that to be one of the longest recessions of the post-war era at 18 months. Based on the length of this yield curve inversion so far, the recession I expect is likely to last at least 10 months, which would make it one of the longest-lasting recessions since the Great Depression.

Note that due to the unusual length of the inversion before the Great Recession, many investors thought it was a faulty signal that no longer worked, particularly since the Fed was already slashing interest rates by late 2007. As we know, it was an excellent signal of a coming recession.

While it is always possible this time could be different and there may be no recession, based on the perfect historical track record of the yield curve, I believe the odds are heavily against it.

Conclusion

Based on the rapid rise in short-term interest rates, the decline in money supply and bank deposits and the deep and long-lasting inversion of the yield curve, I believe it is highly likely that the US will enter into a major recession soon, if it hasn’t done so already. Since stocks and other risk assets typically fall significantly during recessions, I believe investors should prepare for this high-probability risk.

For further details see:

4 Reasons A Long Recession Is Likely To Start Soon