VTI - 4 Reasons The Market Rally Will Not Endure

2023-07-03 12:37:10 ET

Summary

- Stocks closed the first half of the year on Friday with the Nasdaq having its best six-month start to a year in four decades.

- However, there are myriad reasons this market is becoming more overbought by the day, and a reckoning is on the horizon for equities in the second half of 2023.

- A partial list of some things that make no rational sense in what has become a 'Hopium' market follows in the paragraphs below.

If there must be madness, something may be said for having it on a heroic scale " ? John Kenneth Galbraith, "The Great Crash 1929."

Equities surged on Friday to close out the trading week, the quarter, and the first half of 2023 on a high note. The Nasdaq (COMP.IND) rose nearly 1.5%, while the S&P 500 (SP500) was up one and a quarter percent. It was the best first of a year for the Nasdaq in four decades. However, most of this rally has been confined to a large part to mega-cap technology stocks such as NVIDIA Corporation ( NVDA ) .

{kind=link}

For June, the S&P 500 gained 6.5%. This was its best monthly performance since October. The Nasdaq advanced 6.6%. For the quarter, the Nasdaq was up 12.8% and now is up an impressive 31.7% year to date after falling by a third in 2022. The S&P 500 was up 8.3% for the quarter and is up 15.9% for the year. It is important to keep firmly in perspective that this has not been a broad-based rally. The Dow Jones Industrial Average (DJI) is up only 3.4% for 2023 and the Russell 2000 (RTY) has risen approximately eight percent.

Other than the lack of market breadth, there are myriad reasons this market is overbought and likely to face a significant correction at some point in the sector half of 2023. Here are four key concerns investors should have around equities at current trading levels.

Inverted Yield Curve:

The Treasury yield curve is deeply inverted at the moment. Currently, the 3-month treasury bill (US3M) is yielding right at 5.2%, the Two-Year (US2Y) is going for 4.95%, and the 10-Year (US10Y) is going for 3.85%. An inverted yield curve has been historically a sign a recession is on the horizon. And the current degree of yield inversion is as high as it has been since the early 80s when the country was treated to a brutal double-dip recession.

One of the main pillars of the banking system is the ability to borrow short and lend longer-term at higher rates. When the yield curve inverts it upends that system in a negative way. The rapid rise of interest rates caused huge unrealized losses in the bond portfolios at Silicon Valley, Signature and First Republic Banks which triggered a series of events that led to three of the three biggest bank failures in American history earlier this year.

Bank of America ( BAC ) ended the first quarter with approximately $100 billion in unrealized losses in its bond portfolio. While Bank of America is obviously " too big to fail" and will withstand these headwinds, it will crimp the bank's profitability and lending capacity. Similar challenges at other banks are likely to lead to a " credit crunch" which will negatively affect many industries, especially small and medium-cap companies restricting economic activity.

The Coming Commercial Real Estate Debacle

As I detailed in last week's piece " The Canary In The Coal Mine ," the CRE sector is facing a ton of hurt that will only get worse in the coming quarters. This is especially true in the office and retail real estate areas of the market. The corresponding rise in delinquency rates and write offs for the financial system will only get worse as CRE has some $1.5 trillion that needs to be refinanced over the next three years. This debt will have to be rolled over not only at higher rates but in many cases on assets that have much lesser values than they did the last time debt was issued. Many owners will just " hand over the keys" to lenders, which is what the operators of the two largest hotels and biggest mall property in San Francisco have done recently.

We are seeing examples of the extreme losses of value in these types of properties on a weekly, if not, daily basis now. Last week the historic Trust Building located in downtown Los Angeles was sold for just under $40 million. This building was last purchased for $80.7 million in 2016 by owners that put some $40 million into renovating this 11-story, 334,000 square foot building which was financed via a $91.7 million loan from JPMorgan Chase & Co. ( JPM ) . Look for these sorts of losses to cascade through the financial system going forward. This will add a huge layer of stress to already struggling regional banks that hold approximately of these sorts of commercial real estate loans.

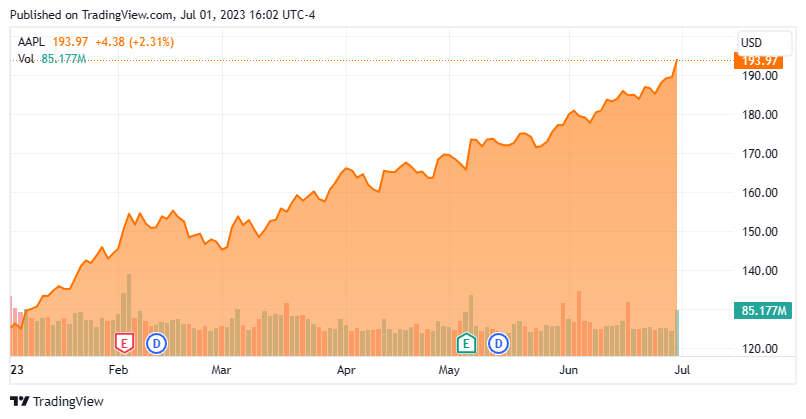

Apple Has A $3 Trillion Market Cap

Apple Inc. ( AAPL ) crossed over the $3 trillion market capitalization threshold last week for the first time. Let me repeat that again for effect. Apple now is worth over $3 trillion according to Mr. Market. The stock has gained 55% so far in 2023 and it and other mega caps are responsible for most of the gains in the NASDAQ year-to-date.

{kind=link}

Let's put that in perspective, Apple has a higher market cap that every country's annual GDP in the world sans a half dozen.

GDP By Country (2023 Est.) (Wikipedia)

What really is amazing is the stock has had this massive rally in 2023 even as both revenues and earnings are projected to be slightly down from FY2022's levels. Despite this, AAPL has reached a valuation of approximately 32 times forward earnings and nearly eight times forward revenues.

These sorts of extreme valuations are what one usually encounters towards the end of bubbles. I still remember Credit Suisse touting Cisco Systems ( CSCO ) as potentially the first trillion-dollar market cap concern back in February 2000. A month later, the Internet Bust started and Mr. Market took tech investors out behind the woodshed and treated them like rented mules.

The Economy Is Weaker Than Being Reported

Last week the final revision for first quarter GDP raised growth to 2% for the quarter from just 1.3% previously. Stronger exports and weaker imports were responsible for most of the revision. While two percent growth is historically not something to write home about, it was significantly higher than expectations.

However, there are myriad reasons to believe actual economic growth is weaker than being reported. Among these are:

1. Corporate profits fell nearly six percent on a year-over-year basis in the first quarter.

2. The consumer (responsible for roughly 70% of economic activity) is challenged on many fronts. The average consumer has lost over three percent of buying power to inflation since the beginning of 2021. Personal Savings rates have fallen to levels not seen since the Financial Crisis of 2008 and layoffs are accelerating.

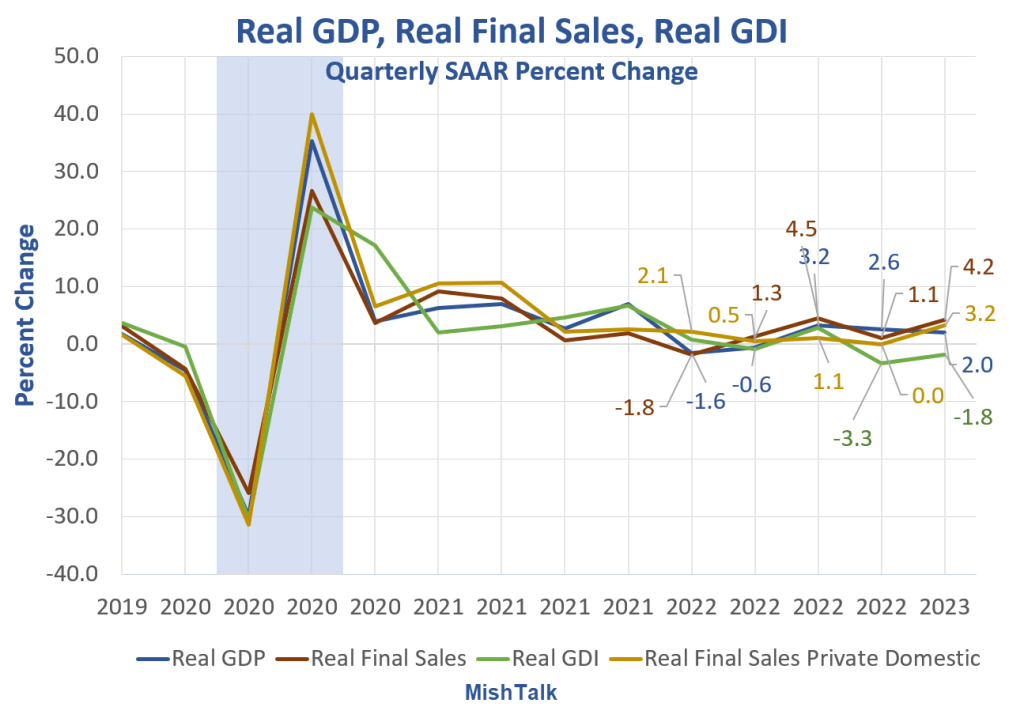

3. Part of the GDP report contains figures for both Gross Domestic Product [GDP] and Gross Domestic Income [GDI], which in theory should be equal over time. However, as noted by President Obama's Chief Economist Jason Furman in a tweet this week.

Over the last two quarters GDP has grown at a 2.3% annual rate while GDI has fallen at a 2.6% annual rate. This is the largest discrepancy in at least 20 years .

{kind=link}

Expect some " reversion to the mean" in coming quarters, which should be a drag on GDP projections as weaker real growth is reflected.

4. Finally, a good portion of the tepid growth the economy is seeing is coming from government spending. Unfortunately, and obviously, the Federal government spending $1.5 trillion to $2 trillion more annually more than it takes in is simply not sustainable.

For these reasons, it is hard to be in any way optimistic about the prospects for equities in the second half of the year. Frankly, I will be surprised if we don't get at least a 15% pullback in the NASDAQ at some point by year end. I also believe a recession is the most likely scenario for late 2023/early 2024.

Therefore, my portfolio is positioned very cautiously as we open the second half of the year with by far my biggest holding being short-term treasuries that yield more than five percent. Discretion is simply the better part of valor for investors with stocks currently trading at overbought levels.

It's better to face madness with a plan than to sit still and let it take you in pieces ."? Josh Malerman.

For further details see:

4 Reasons The Market Rally Will Not Endure