UNIT - 4 Reasons To Buy Uniti Stock

2023-07-26 17:22:07 ET

Summary

- Uniti Group Inc., a REIT specializing in infrastructure for the communications industry, has seen its stock value decrease by 42% over the past year.

- We like the long-term prospects of fiber and how Uniti is positioned to improve in this space.

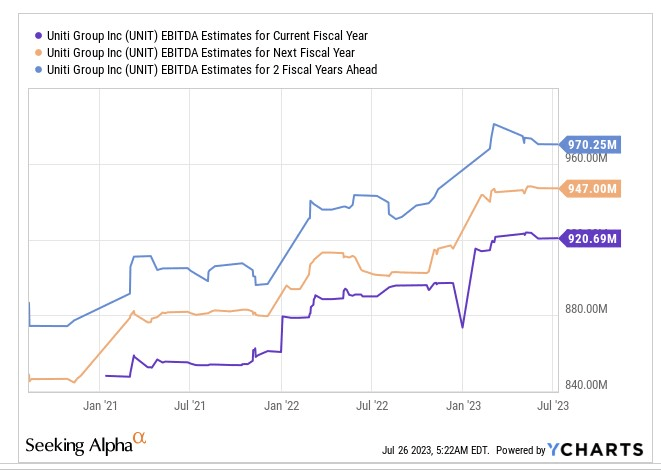

- Forward valuations look cheap, and the company offers decent EBITDA potential in the medium-term.

- Uniti could benefit from rotational interest within the real estate space.

- We like the developments on the charts and are enthused to note the recent positioning amongst key stakeholders.

Introduction

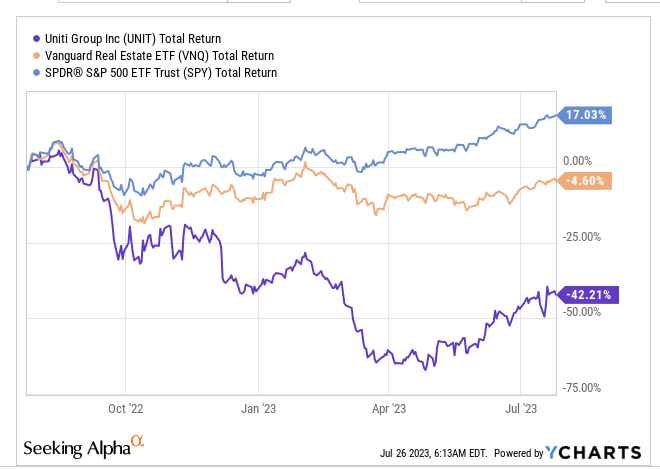

Uniti Group Inc. ( UNIT ), is a REIT that specializes in acquiring, constructing, and leasing critical infrastructure for the communications industry; this includes copper and coaxial broadband networks, fiber optic, and data centers. Over the past year, the stock of Uniti Group has proven to be a troublesome avenue for investors, shedding 42% of its value, and underperforming not just its peers from the real estate space, but the US benchmark index as well.

{kind=link}

Broad investor sentiment towards UNIT may not necessarily be too positive, particularly on account of UNIT’s heightened exposure to troubled entity Windstream (~65% of group sales). However, we still feel it wouldn’t be the worst thing in the world to consider a position in the UNIT stock at these levels. Here’s why we like this stock.

The Long-term Story Still Has Legs

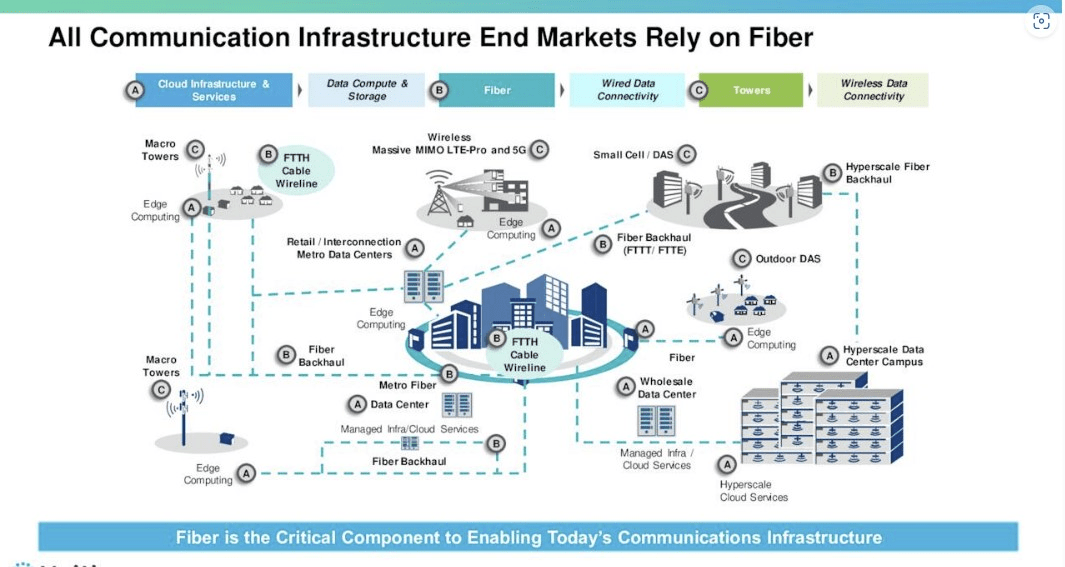

Amidst all the doom and gloom, it's important to not totally dismiss the long-term narrative here. Bandwidth-intensive avenues such as social media, streaming, 5G, smart devices, and cloud-based applications are all here to stay; rather their adoption will only snowball in the periods ahead. In a bandwidth-heavy world, the importance of fiber infrastructure should not be underestimated.

{kind=link}

With around 137K fiber network route miles, UNIT is currently the second largest independent fiber provider in America and this puts it in an enviable position to effectively lease-up, and generate high-margin recurring revenue (already this year, Uniti Fiber looks poised to deliver healthy monthly recurring revenue growth of 6-8% YoY). Customer stickiness too is quite evident with a monthly churn rate of just 0.2% which is best-in-class (churn as a function of MRR).

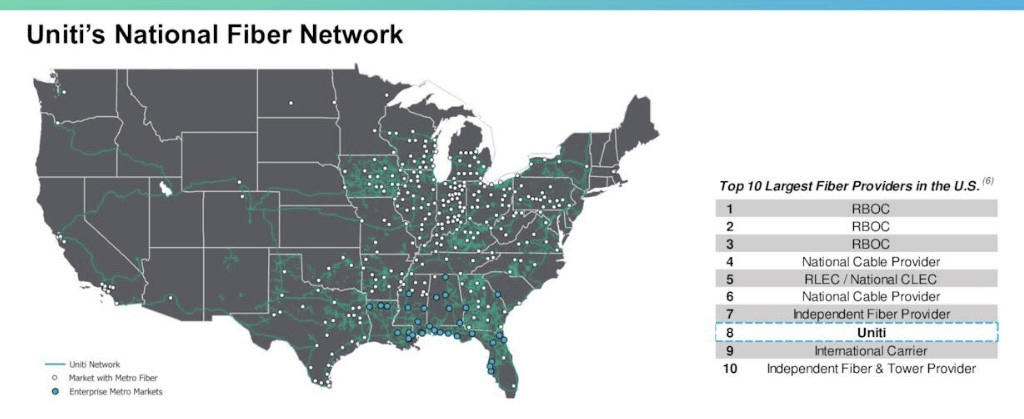

This is still inherently a very fragmented market, and UNIT, which was the first REIT to step into this space, is well-positioned to leverage its first-mover advantage, and build scale.

{kind=link}

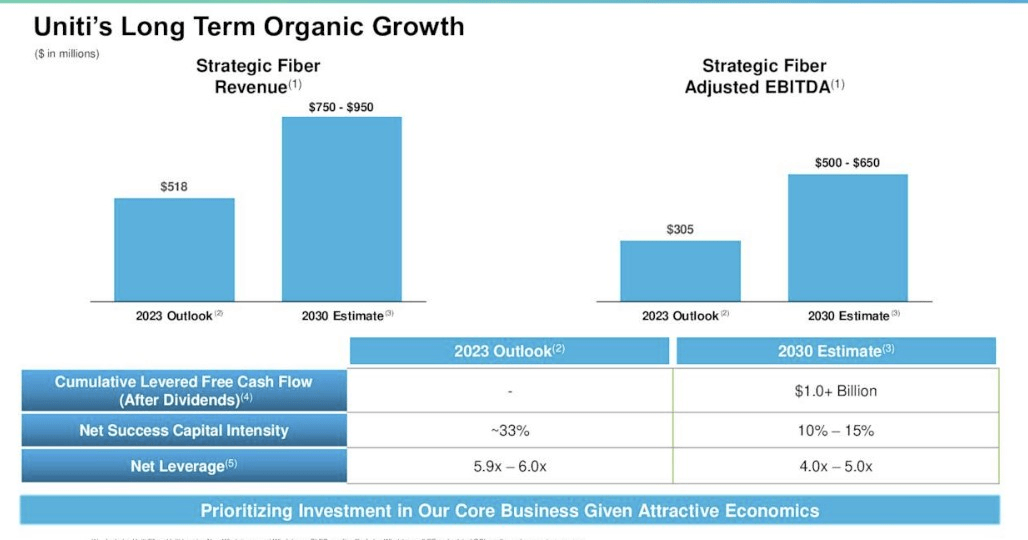

Building scale will also necessitate a leverage-heavy position, and Uniti’s critics have often used that as a stick to beat it, (the net leverage by the end of FY23 will likely hit levels of 5.9-6x ) but it’s not as though these debt funds are being channeled into building infrastructure that is going out of fashion. Besides, even though UNIT is highly financially geared, it’s also reassuring to note that the company recently refinanced its debt and won’t have any major debt maturities due until 2027 (only 3% of the outstanding debt matures before then).

In 2027, UNIT could likely be in a much healthier financial state. In a couple of years, the company should also turn FCF positive and will look to generate cumulative levered FCF of over $1bn over the next 7 years.

Besides, the heavy lifting on the investment side too should ebb. Previously capital intensity (CAPEX as a function of sales) for UNIT was over the 50% levels, but now it is already closer to the 30% mark, and by the end of this decade, it will drop to just 10-15%. By then, the Fiber business will also be a lot more lucrative with EBITDA margins poised to hit levels of 68% from 59% currently, even as revenue CAGRs of this business could be above mid-single-digits and closer to double-digit levels. Management believes by then, the non-Windstream component of their portfolio will also likely double from what it is now. Meanwhile leverage levels too could drop to 4x.

{kind=link}

Cheap Valuations

Within the broad real estate universe, we think UNIT could be a ripe candidate to catch the attention of bargain hunters. For context, the stock is currently priced at a forward P/AFFO of just 3.67x , a multiple that is not even a fourth of the sector median P/AFFO of over 15x.

Lest you forget, it’s not as though UNIT is operating a bog-standard pool of assets; in case investors need reminding, UNIT’s leasing segment EBITDA margins stand at a whopping 97% . Also, at such a drastic discount to the industry average, you’d think this business was priced for no growth at all, but conversely, UNIT is still poised to deliver healthy EBITDA growth every year, at an expected 3-year CAGR of 2.3% through FY25.

{kind=link}

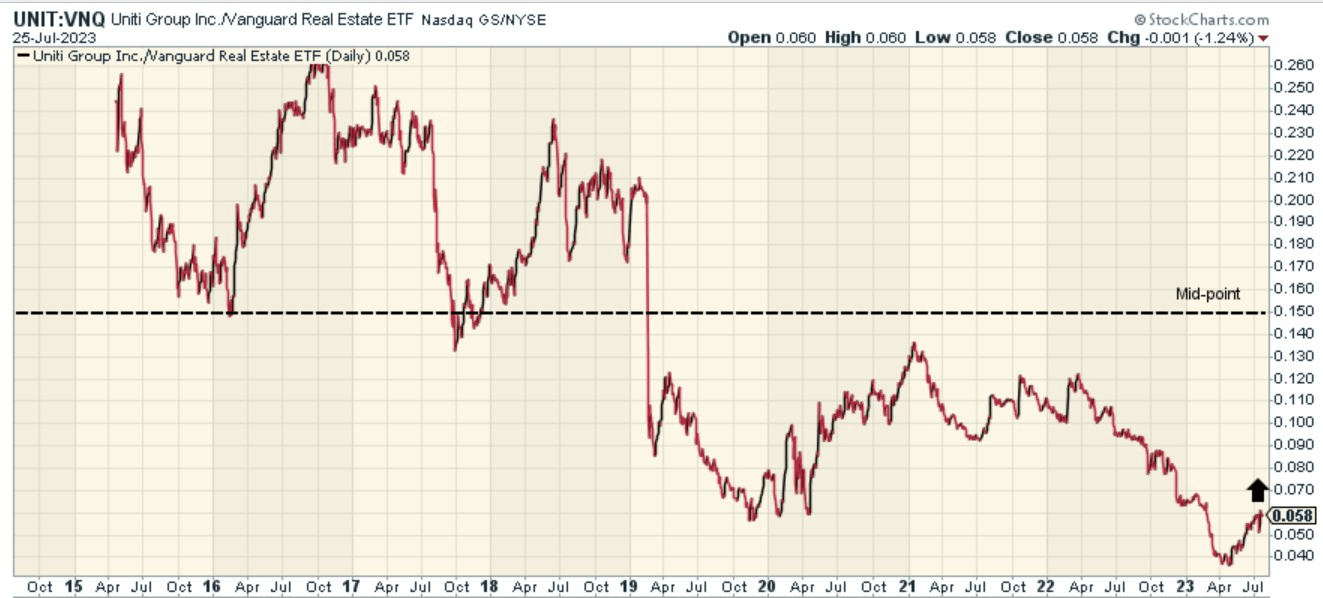

Rotational Potential Within Real Estate

Meanwhile, also consider how the UNIT stock is currently positioned relative to its peers from the broad real estate universe; the image below highlights how oversold the UNIT to Vanguard Real Estate ETF looks, trading around 60% off the mid-point of its trading range. Investors fishing for prospective rotational opportunities within the real estate segment could gravitate to UNIT on account of this.

{kind=link}

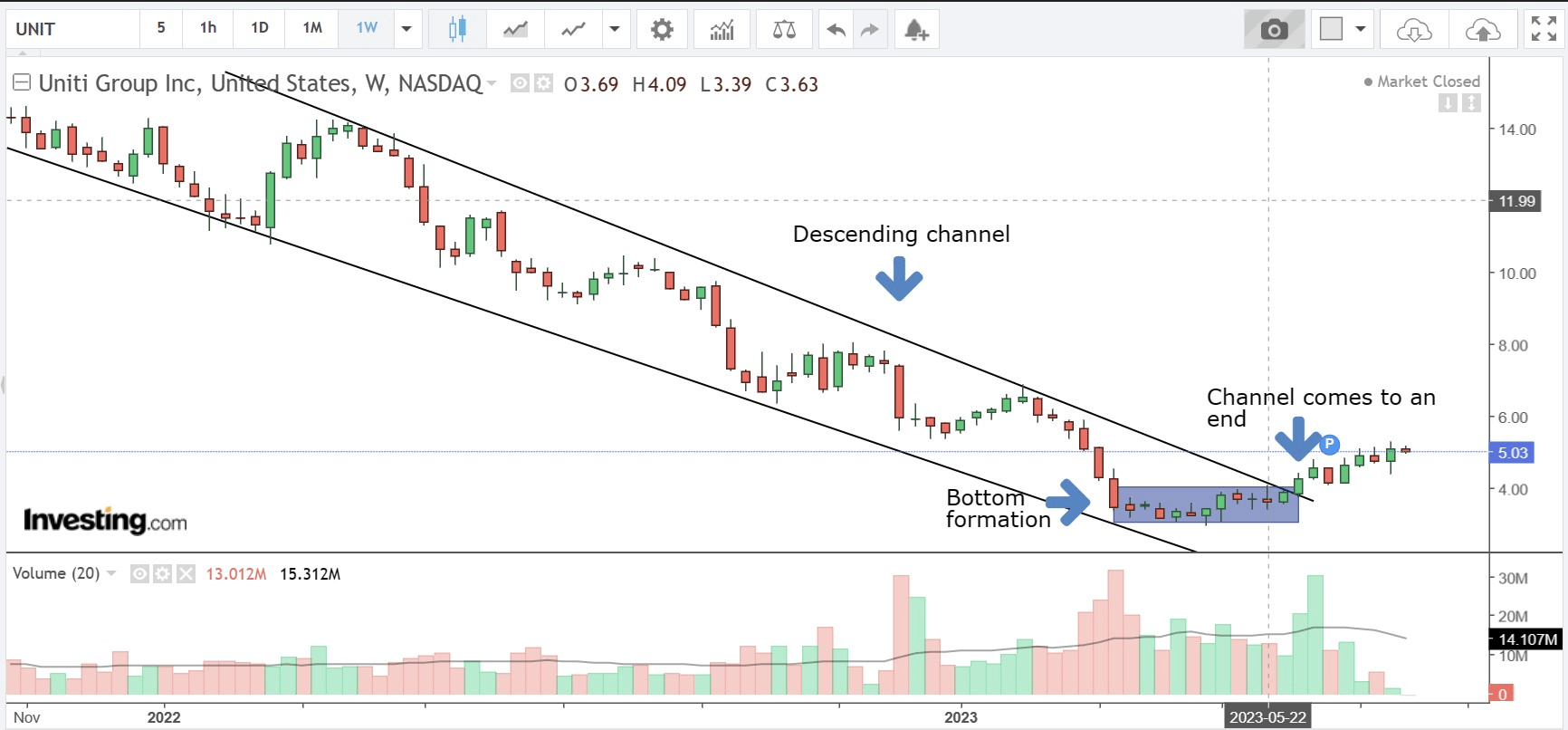

Closing Thoughts: Base Formation, Backed By Important Purchasing Interest

Besides the dirt-cheap valuations and the potential for rotation, we're also enthused to discover the recent price imprints on UNIT’s weekly chart which improves the bullish stance.

{kind=link}

Firstly, from the image above we can see that the price had been trending lower for many months, in the shape of a descending channel. However, from March 2023 onwards we began to see signs of a flattening out of the price action.

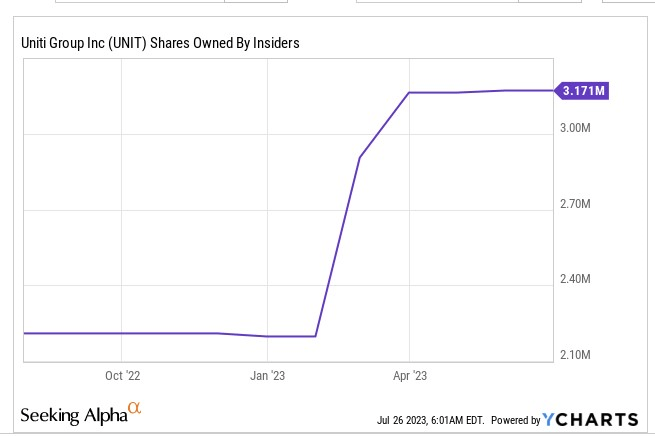

Interestingly enough, one of the catalysts for reduced selling then was insider buying by the UNIT management team. After over 5 years of not witnessing any insider activity, the CEO of UNIT ended up buying shares of the stock in early March .

{kind=link}

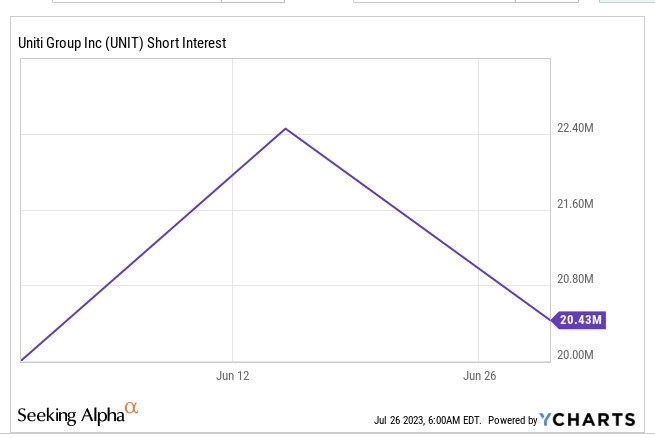

This emboldened the bulls, who then pushed the stock beyond the upper boundary of the descending channel, and since then the stock has been making steady progress. The recent resilience of the stock has also put off a fair few short-sellers, as their stake has come down recently.

{kind=link}

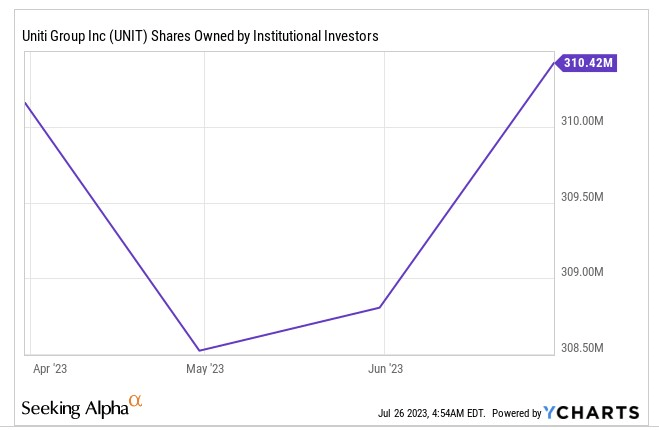

Crucially, it’s also been encouraging to note that the recent move hasn’t only been driven by the retail segment. In fact, since May, the institutional segment too has turned bullish on the UNIT stock, after months of selling, and provides an added degree of reassurance to the quality of the uptrend.

{kind=link}

For further details see:

4 Reasons To Buy Uniti Stock