SO - 4%-Yielding Southern Company Is A Utility Gem

2023-11-03 16:17:38 ET

Summary

- Southern Company's stock has performed well, up over 90% in the past five years, and its recent earnings report showed positive progress.

- The company is benefitting from warmer weather conditions, changes in rates and prices, and reduced expenses, offset by increased depreciation costs.

- Southern Company is focused on renewable energy and the expansion of Vogtle 3 & 4, and is expected to see significant changes in electricity sales growth in the future.

Introduction

I own Duke Energy ( DUK ). When I bought it, I was considering buying either DUK or Southern Company ( SO ) . While I wouldn't make the case that I bet on the wrong horse, I have to say that I underestimated Southern Company a few years ago.

A few years ago, Southern Company was struggling with delays in its Vogtle Unit 3 & 4 expansion, and the fact that cheap funding caused investors to rush into stocks that offer more renewable exposure. This includes companies like NextEra Energy ( NEE ). I own a small NEE position in my trading account that I may expand in the next few months.

Having said that, Southern Company has done tremendously well. Not only is the stock withstanding current headwinds pressuring utility stocks and related defensive investments, but it is up more than 90% over the past five years, including dividends.

My most recent article on the stock was published on August 7, when I highlighted its impressive business improvements.

The Southern Company has recently achieved a significant milestone with the successful launch of Vogtle Unit 3, making it a leader in America's return to nuclear energy.

With this expansion, the company is poised for growth, benefiting from rising income and declining capital expenditures.

Now, I get to reiterate that call, using the company's just-released earnings that gave us a lot of positive information, including positive progress at Vogtle Unit 4, solid guidance despite mild cyclical headwinds, and a strong long-term view, as it operates in one of the most favorable jurisdictions in the U.S.

So, let's get to it!

Southern Company Remains In A Great Spot

Let's start with the just-released third-quarter numbers.

In the third quarter of this year, the company's adjusted earnings per share were $1.42, surpassing both the company's estimate and the earnings from the previous year by $0.12 and $0.11, respectively.

Key factors contributing to this performance were warmer-than-normal weather conditions, changes in rates and prices, and reduced income taxes and operating and maintenance (O&M) expenses.

These gains were partially offset by increased depreciation and amortization costs.

For the first nine months of 2023, the adjusted earnings per share were $3.01, down from $3.35 in the same period in 2022.

This was primarily due to extremely mild weather conditions in the Southeast during the first half of the year.

Weather conditions still pose risks to fourth-quarter results, but the company projects achieving full-year adjusted earnings near the midpoint of its guidance range of $3.55 to $3.65 per share, which is everything investors needed to hear, as the stock is now trading back above $70 again, 19% above its 52-week low.

While year-to-date electricity sales are down 0.5% compared to the prior-year period, the company added approximately 35,000 electric customers and 19,000 gas customers during this period, with commercial usage performing well.

However, there are a few developments to keep in mind.

- Residential sales saw some fluctuations due to the transition of customers returning to offices.

- Industrial sales were affected by weaknesses in chemical, paper, and housing-related sectors.

- The service territories are undergoing an industrial transition, with a shift from traditional industries to the manufacturing of solar panels, batteries, airplanes, and electric automobiles.

We can ignore most weather-related fluctuations for two reasons.

- Utilities will always be subject to weather-related fluctuations.

- Southern Company is benefitting from some significant longer-term tailwinds.

During its earnings call, the company noted a strong level of economic development activity within its service territories.

They expect to provide formal updates during their fourth-quarter earnings call in February, but they highlighted the potential for significant changes in electricity sales growth.

Previous forecasts assumed annual electricity sales growth of 0% to 1%, but the power needs of data-centric businesses and manufacturing facilities are likely to lead to annual growth closer to a mid-to-high single-digit range over the next five years.

This may necessitate significant capital investments, but existing and new customers are expected to benefit economically from this growth.

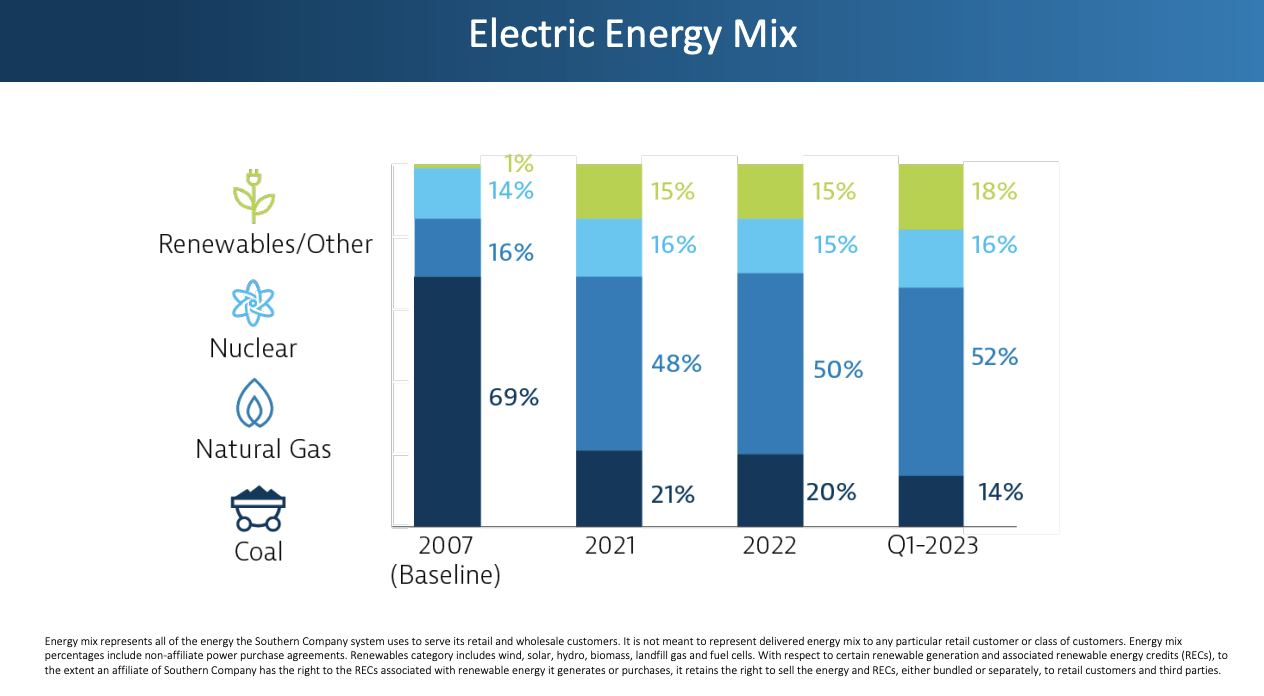

Speaking of capital investments, like all of its peers, the company is focusing on renewables and cutting coal.

In 2007, SO had 69% coal exposure. That number dropped to just 14% at the start of this year. By 2025, the company aims to reduce its 2007 coal capacity by 87%, growing renewable by more than 3x between 2015 and 2030 (to more than 17 thousand megawatts).

{kind=link}

A cornerstone of the company's strategy is the expansion of Vogtle 3 & 4.

Unit 3 of the Vogtle nuclear power plant successfully achieved commercial operations at the end of July and has performed well, according to the company.

Unfortunately, Unit 4 experienced a motor fault in one of the reactor coolant pumps during start-up and preoperational testing. This fault required a full replacement of the pump with one from the spare parts inventory. Preoperational activities continue in parallel with the pump replacement, including coatings and preparation for power ascension testing.

However, after the successful installation of the spare pump, Unit 4 is expected to commence start-up and preoperational testing, with a projected in-service date in the first quarter of 2024.

The company also filed an application with the Georgia Public Service Commission to adjust rates to include reasonable and prudent Vogtle Unit 3 and 4 costs.

Related to this application, the Georgia Public Service Commission public interest advocacy staff filed a stipulated agreement among Georgia Power and several other intervenors, which is intended to constructively resolve all issues regarding reasonableness, prudence and cost recovery for the remaining Vogtle 3 and 4 costs, not already in base rates. The Georgia Public Service Commission is expected to vote on this matter on December 19. - Southern Company

So far, I'm impressed. The company is sticking to its guidance, seeing ongoing secular growth tailwinds and solid progress in its Vogtle 4 endeavor despite minor setbacks.

Shareholder Distributions

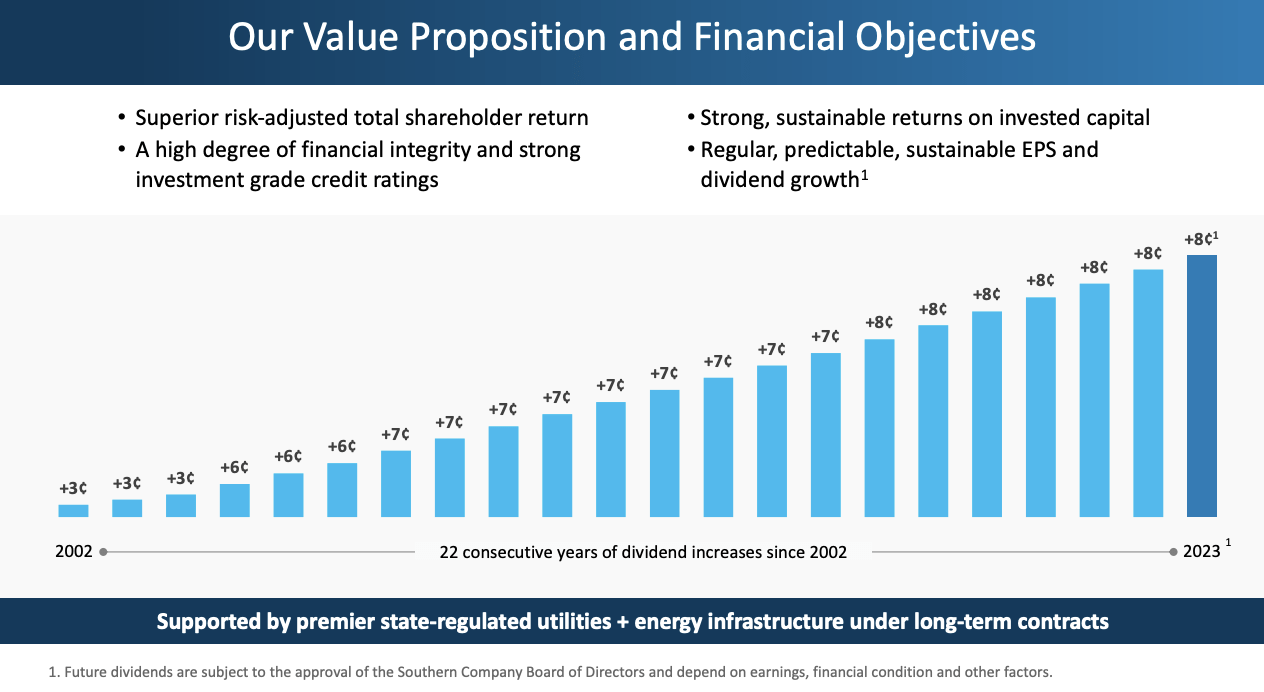

Southern Company is very proud of its dividend track record - and rightfully so.

The company, which has a BBB+ credit rating (just one step below the A-range), has hiked its dividend for 22 consecutive years, which obviously includes the dot-com bubble, the Great Financial Crisis, and the pandemic.

{kind=link}

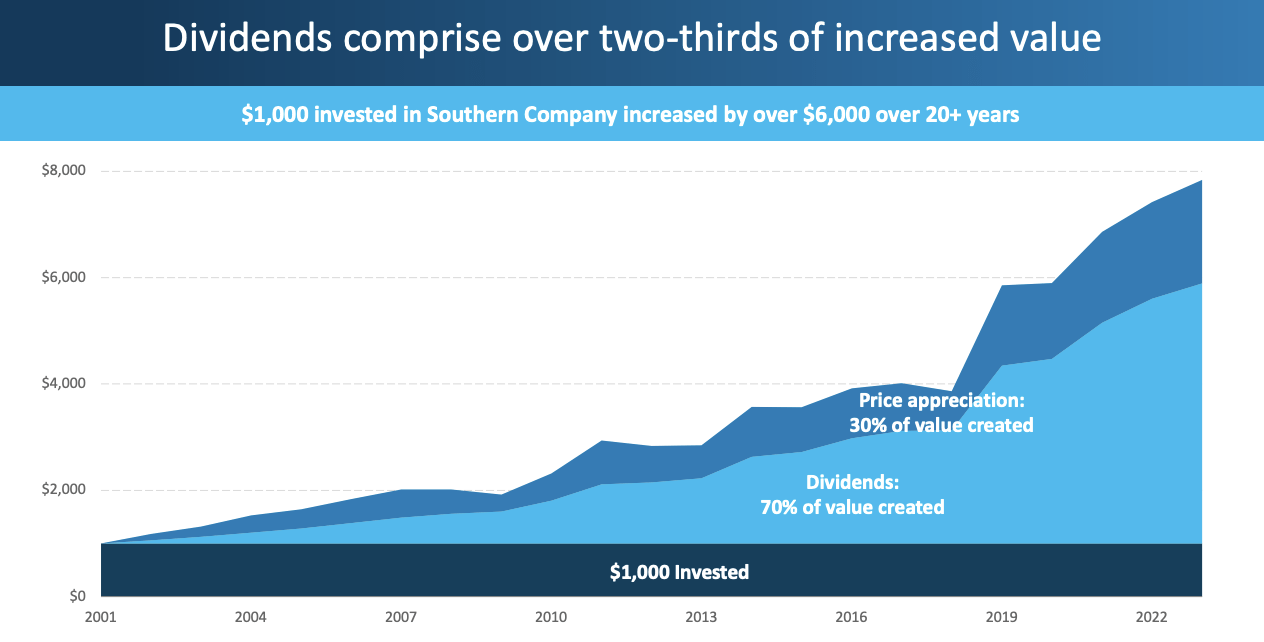

These dividends have contributed significantly to its total return. $1,000 invested in 2001 would have turned into almost $8,000. 70% of this return has come from dividends.

{kind=link}

The company currently yields 4.0%.

Over the past five years, this dividend has been hiked by 3.2% per year (on average). This year, the company is expected to generate $3.60 in earnings per share, which translates to a 79% payout ratio.

With that said, during the 3Q23 earnings call, the company was asked about boosting dividend growth. After all, over the past few years, it has hiked by $0.08 every year.

Travis Miller

Okay, makes sense and then a quick follow-up. The dividends, what do you think the Board is looking for to get off that $0.08 or lift growth rate to 4%, 5%, 6%? What are your thoughts around that?

Dan Tucker

Yes. I think it's primarily just working our way down to a sustainable payout ratio, right? So if you think about where our guidance sits here in 2023, our payout is going to be something like 77% for 2023. That's not a sustainable payout ratio for a growing company. Now that's largely a function of the ROEs we've been earning at Georgia Power during construction of Vogtle 3 and 4. As that rolls off, that payout ratio will begin to come down, but we just need to get it somewhere comfortably into something that probably starts with a six in order to start evaluating a higher growth rate. - SO 3Q23 Earnings Call

In other words, it will likely take a while until the company is able to boost dividend growth, which is fine, as financial stability and investments in future growth are more important.

And besides that, investors earn 4% while waiting for dividend growth to pick up. There are worse deals on the market, to put it mildly.

Furthermore:

- The company is free cash flow positive. It's one of the few utilities that is generating more cash than it is spending on capital investments.

- This year, the company is expected to generate $960 million in FCF. That number is expected to rise to $1.1 billion in 2025, allowing the company to lower its leverage ratio from 5.9x 2023E to 5.3x in 2025E.

The company can limit net debt growth and increasingly support higher dividend growth in the years ahead.

Valuation

Valuation-wise, we're dealing with an attractive opportunity despite the company's recent outperformance.

Using the data in the chart below, there are a few things that make the risk/reward attractive.

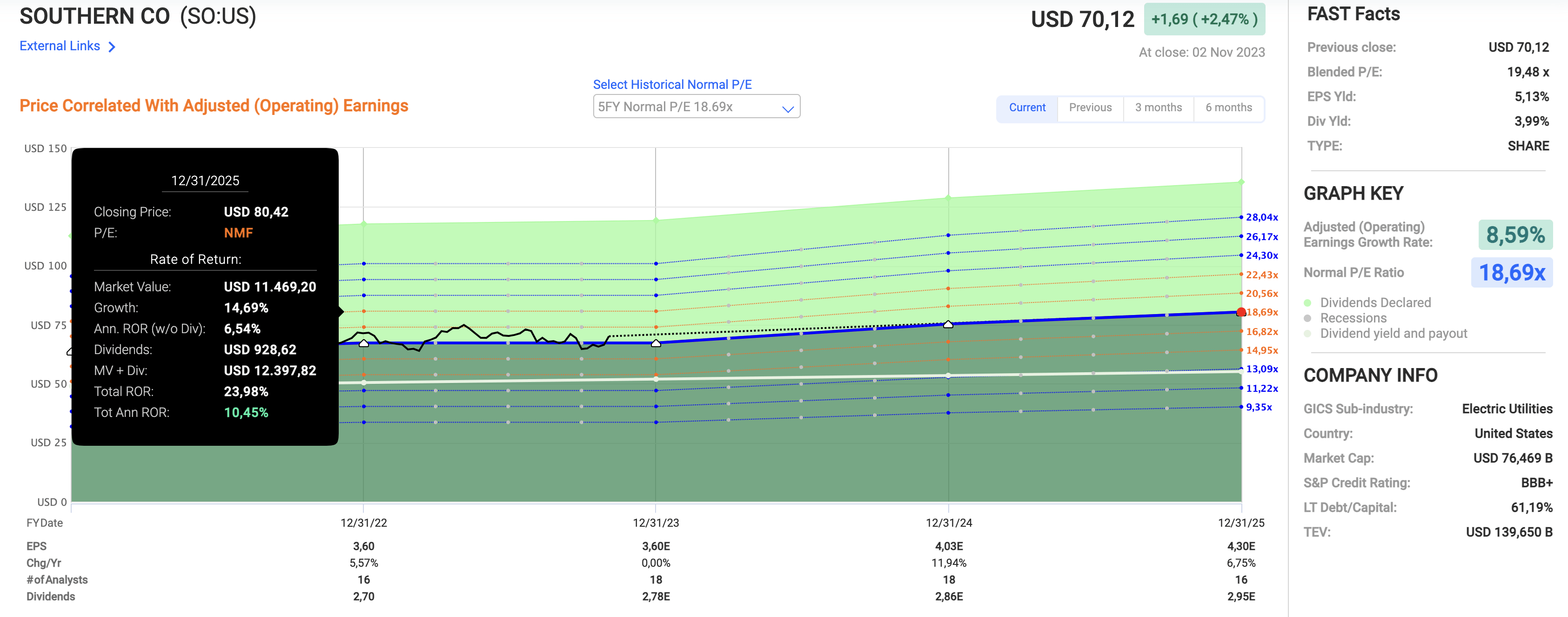

- Southern Company is trading at a blended P/E ratio of 19.5x earnings.

- The average normalized P/E ratio of the past 20 years is 16.8x earnings.

- However, over the past five years, the valuation has increased to 18.7x earnings.

- A higher valuation is warranted because Southern Company is growing rapidly.

- While EPS is expected to be flat this year, analysts expect 12% EPS growth in 2024, followed by 7% growth in 2025.

{kind=link}

If the company is able to maintain what I believe to be a reasonable valuation of 18.7x earnings, the company could return 10% per year through 2025. This includes its dividend.

I have to say that I am very tempted to sell my DUK stake and move it into SO. However, I have not yet made a final decision.

Takeaway

I've been impressed by Southern Company's recent performance in the utility sector. Despite past challenges, the company has demonstrated resilience and adaptability, making it an outperformer in a tough environment.

The latest third-quarter earnings report proved SO's strength. Its dividend track record, commitment to renewable energy, and financial stability make it an attractive investment.

Although a rebound in dividend growth may take time, the company's focus on future growth and its 4% yield for investors are enticing.

For further details see:

4%-Yielding Southern Company Is A Utility Gem