OKE - 5.4% Yield And Up To 10% Annual Return Potential - Buying Top-Tier Income With ONEOK

2023-12-29 12:37:05 ET

Summary

- ONEOK stands out with a 25-year dividend history, a 5.4% yield, and slow but secure dividend growth.

- OKE's diversified operations, acquisitions, and expansion into key regions position it for sustained growth.

- OKE's expected growth and over 5% dividend yield make it a compelling potential choice for my portfolio.

Introduction

I finally did it. I pulled the trigger on a high-yield stock I wanted to buy for a long time. Earlier this week, I bought Antero Midstream ( AM ), one of my favorite midstream players, with a yield of 7%.

In an article published on December 24, I explained why I wanted to buy this midstream player, as it is part of a bigger focus on value and income stocks.

While I am very far from becoming an income-focused investor, I believe in buying undervalued income companies in an environment where the market is trading at a lofty valuation with a high likelihood of a prolonged period of elevated inflation and interest rates.

Bank of America

I am convinced that this will become a stock-picking market, which will put investors who buy undervalued (high-quality) income plays in a great spot.

After buying Antero Midstream, I have to say that I want more.

Top-tier midstream plays go so well with my investments in upstream oil and gas producers, as they add lower-volatility income to my portfolio with less dependence on commodity prices (although I'm very bullish on the long-term future of oil and gas).

Moreover, as much as I like Master Limited Partnerships that often come with yields as high as 9% in the case of Energy Transfer ( ET ) and MPLX ( MPLX ), I am going for C-Corp midstream companies. They have the same tax situation as the "average" dividend stock and are a much easier way for a European like myself to buy midstream assets.

If the tax situation for a foreigner like me were a bit less complicated, I would also own ET and MPLX, as I have been very bullish on both as well.

That's where ONEOK ( OKE ) comes in, one of my favorites.

My most recent article on the stock was written on October 24, when I went with the title "Is 6%-Yielding ONEOK An Unbeatable S&P 500 Income Play?"

In this article, I am going to elaborate on that, using new findings and new business developments, including the company's presentation at this month's Wells Fargo Midstream and Utilities Symposium.

So, let's get to it, as we have a lot to discuss!

Buying High-Quality Income

I like a good high-yield stock. However, I am not a typical high-yield investor, as I am way too picky.

Truth be told, I dislike most high-yield stocks, as they tend to come with very slow growth and often poor long-term total returns.

While that may not be an issue for an income-focused investor living off his or her dividends, it's often a poor choice for younger investors.

Bear in mind that even Warren Buffett is still investing in growth. It's truly a personal decision.

That said, I believe it is time to focus on high-quality income plays.

This is what I wrote in my 2024 Outlook article :

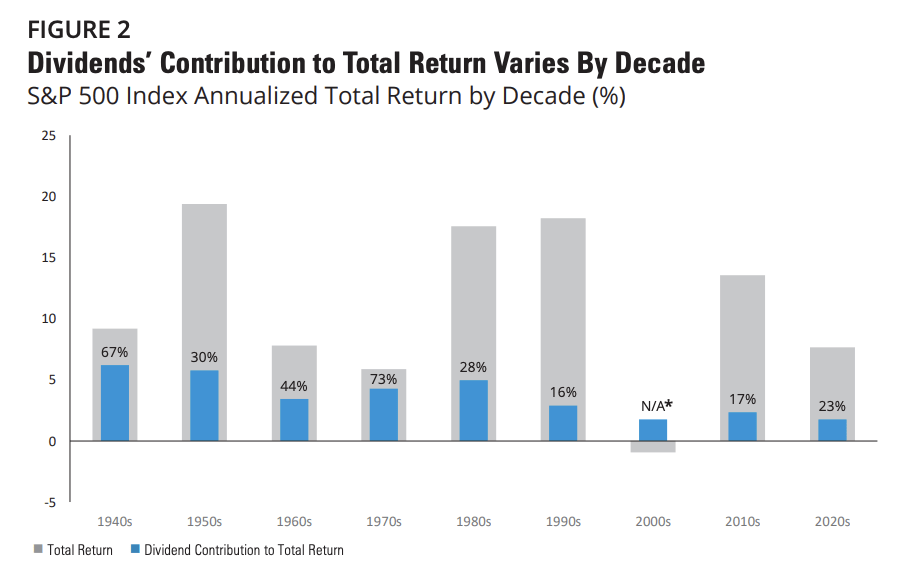

While I'm not a high-yield investor (I prefer dividend growth over dividend yield), I'm increasingly looking for income plays, as I believe that a much bigger part of the total return of the next 10 years will come from dividends. In times of sticky inflation and poor economic growth, the percentage of total return of dividends tends to be close to 30%.

Hartford Funds

{kind=link}

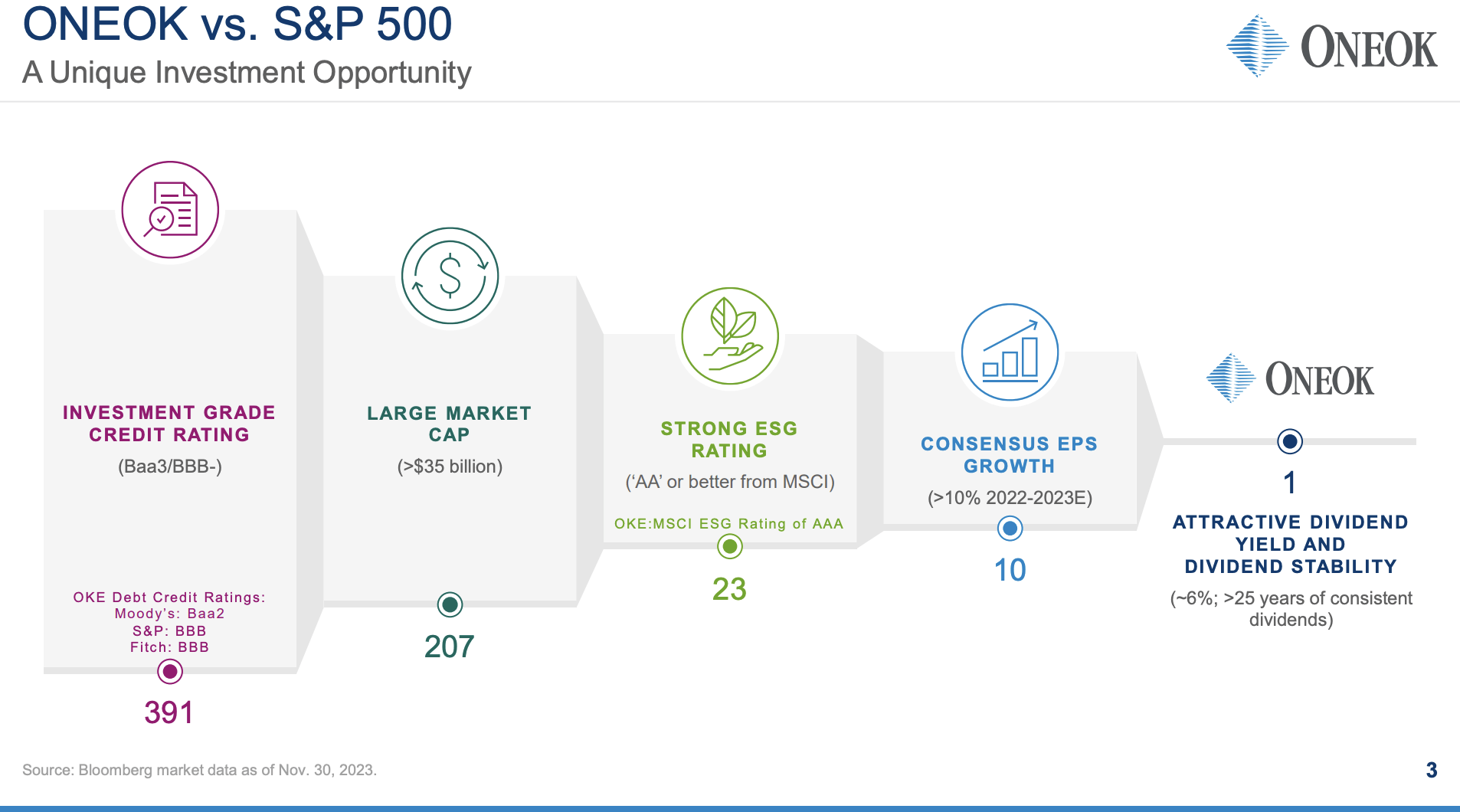

ONEOK is one of the companies that comes with both growth and income.

Using its own data below, it is the only S&P 500 stock that has a yield of close to 6% (it's currently lower due to its stock price performance) with more than 10% expected EPS growth in 2022-2023.

{kind=link}

ONEOK Inc.

While the company is obviously playing a bit with numbers to make it look like it's the only good income stock of the S&P 500 (like filtering out smaller companies and incorporating often vague ESG ratings), I cannot disagree with the company that it is a very attractive income stock.

For example, unlike most midstream companies (especially C-Corps), the company has refrained from cutting its dividend during the Great Financial Crisis, the 2015 commodity crash, and the pandemic, giving it a history of 25 years without cuts.

{kind=link}

ONEOK Inc.

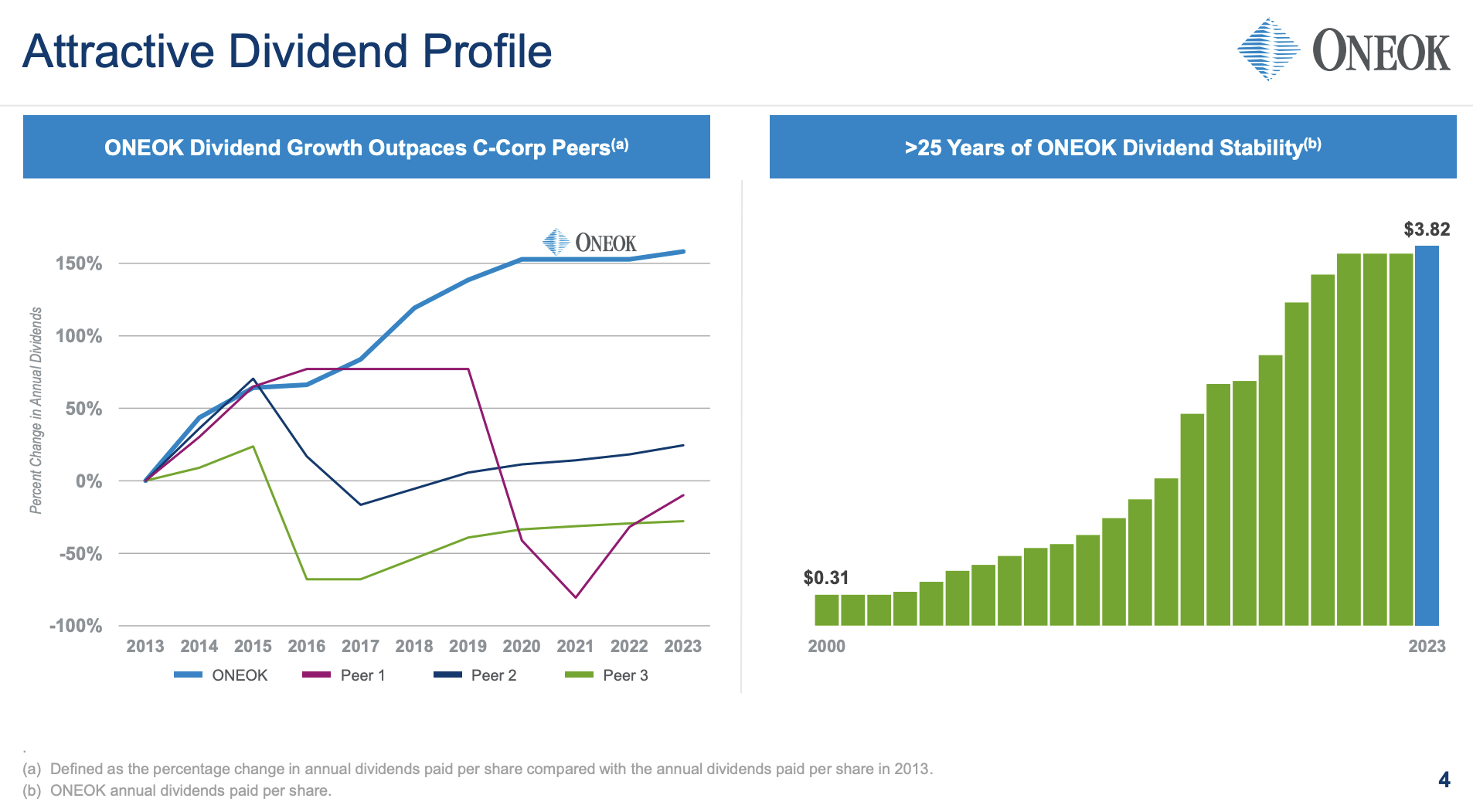

Currently, ONEOK yields 5.4%, which is based on a $0.955 dividend per share per quarter.

On January 18, the dividend was hiked by 2.1%. The five-year dividend CAGR is 3.3%.

Although dividend growth is slow, the dividend is safe.

- This year, OKE is expected to generate $2.6 billion in free cash flow. This translates to 6.3% of its market cap and an 85% cash payout ratio.

- Next year, OKE is expected to generate $3.5 billion in free cash flow (8.5% free cash flow yield, 63% cash payout ratio).

- The company is expected to lower net debt from $22.4 billion at the end of this year to $21.0 billion at the end of 2025, potentially lowering the net leverage ratio from 4.4x to 3.3x. It has an investment-grade BBB credit rating.

In 2022, net debt was below $14 billion. The surge was caused by the acquisition of Magellan Midstream Partners for $25 per share in cash and 0.6670 OKE shares per Magellan unit. It also included $5 billion of Magellan debt.

The good news is that this deal is one of the reasons why ONEOK is in a great spot to grow its business over time.

ONEOK Also Comes With Growth!

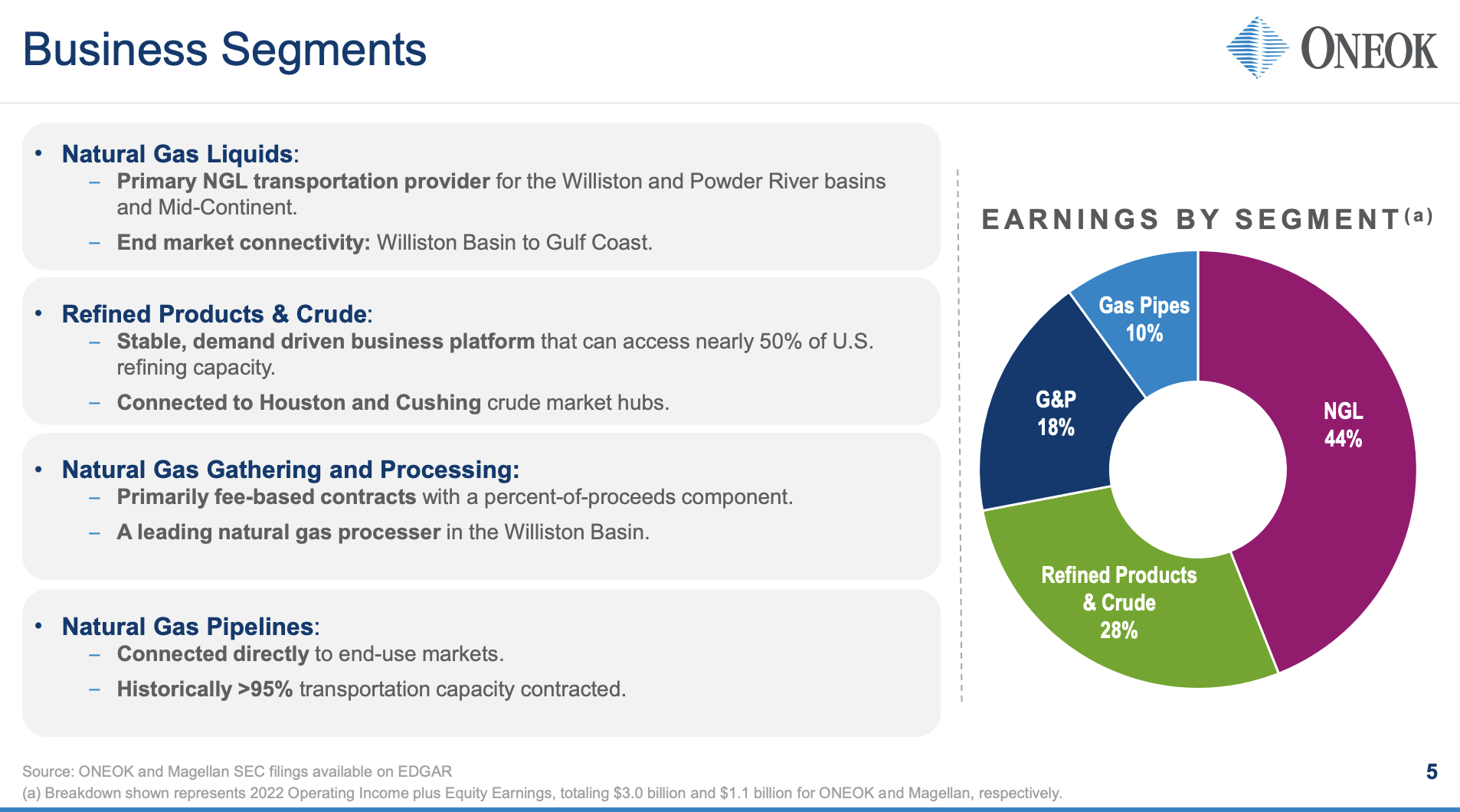

Since this deal closed, OKE has been one of the most well-diversified midstream operators in the U.S., generating earnings from natural gas liquids ("NGL"), refined products, gathering & processing, and gas.

{kind=link}

ONEOK Inc.

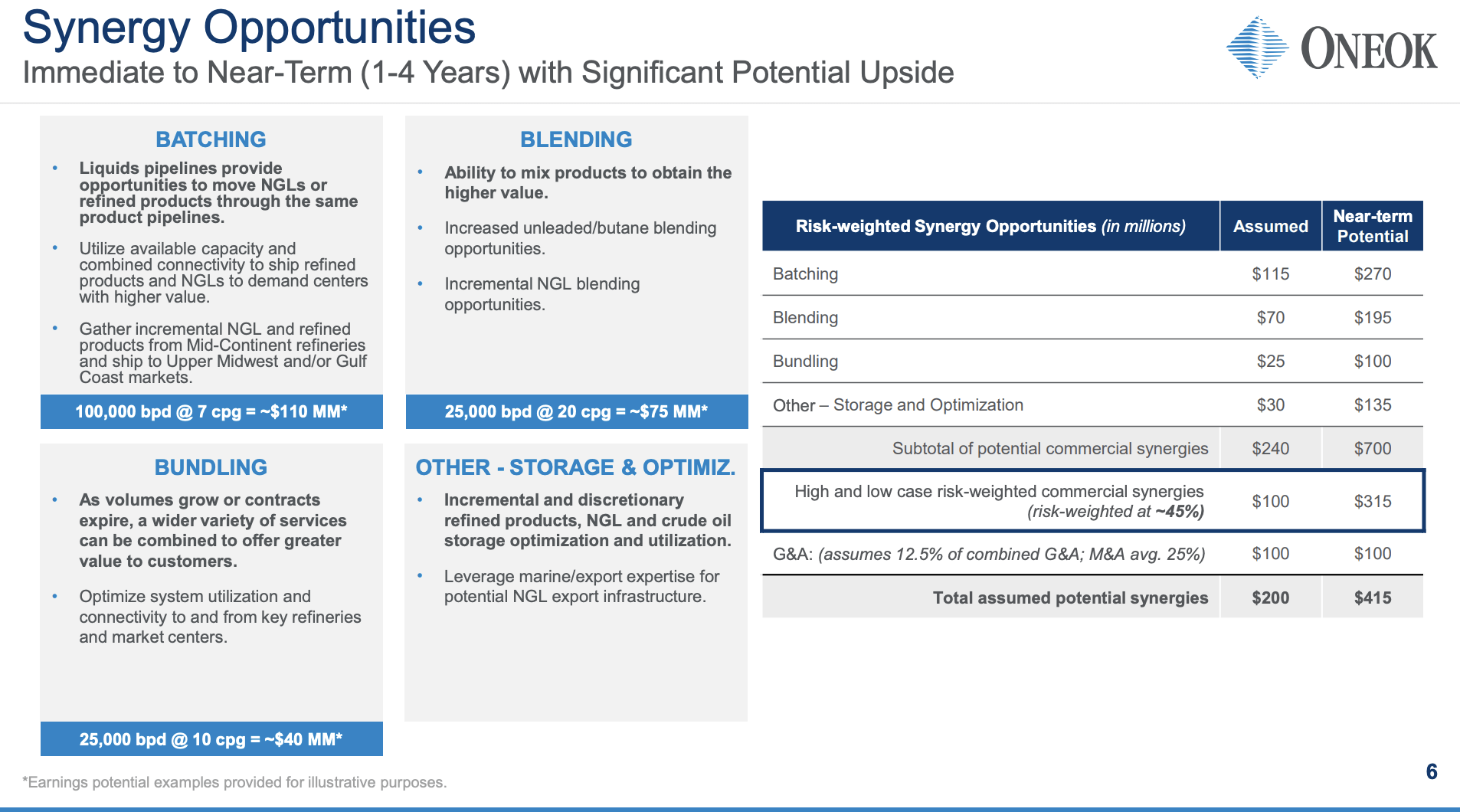

Even better, the integration of recent acquisitions has resulted in cost synergies that are contributing to the company's bottom line.

The company is actively identifying and pursuing synergies across its operations, both immediate and long-term. This includes optimizing condensate sales, leveraging NGL assets, and exploring various commercial synergies.

{kind=link}

ONEOK Inc.

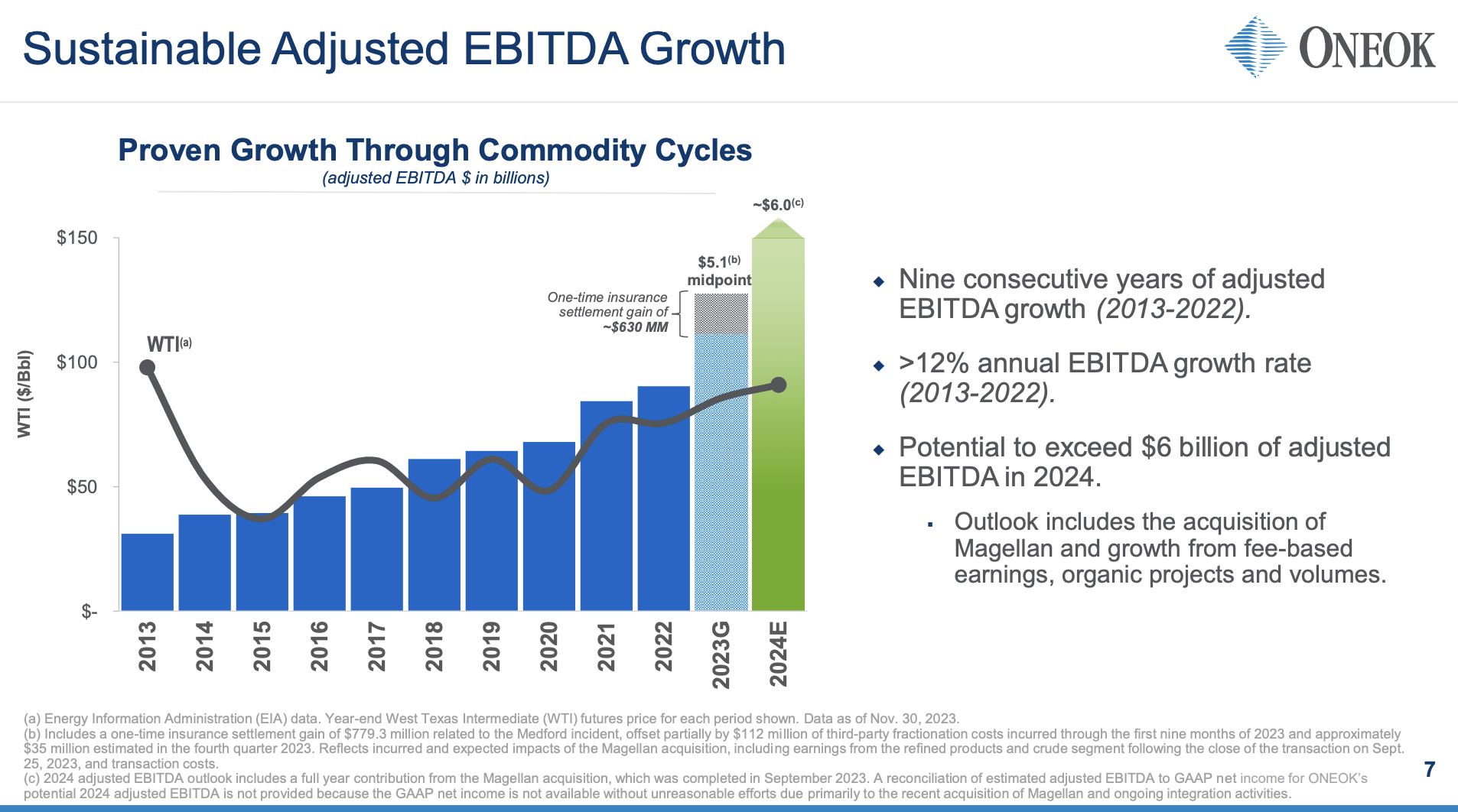

Looking at the chart below, we see that the company has grown its adjusted EBITDA for nine consecutive years, including the 2015 commodity crash and the pandemic.

Next year, the company is in a good spot to generate adjusted EBITDA north of $6 billion.

{kind=link}

ONEOK Inc.

On top of using M&A to fuel growth, the company is strategically investing in growth projects to expand its footprint and capitalize on emerging opportunities.

These initiatives encompass infrastructure projects like the Saguaro pipeline and LNG facility, demonstrating a forward-looking approach to meet evolving market demands in one of the most important energy segments.

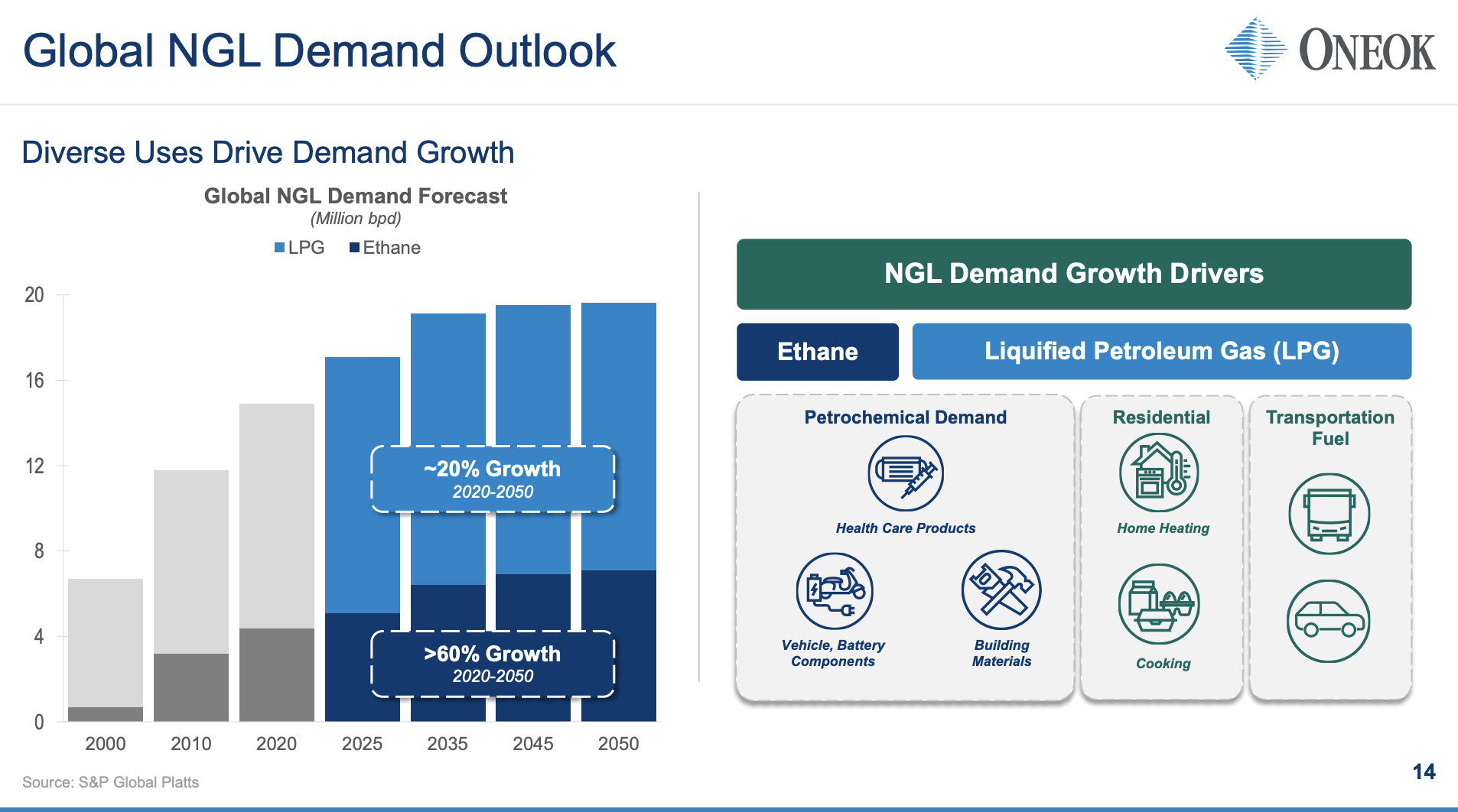

The progression of these projects, including the commencement of contracting for LNG facility trains, signifies tangible steps toward future growth with support from rapidly rising NGL demand.

Not only do I expect NGL supply to increase as the declining quality of U.S. shale oil will lead to a bigger share of production being natural gas liquids (higher-margin liquids that are not crude oil), but we also see that NGL demand is expected to rise rapidly in the decades ahead.

{kind=link}

ONEOK Inc.

In fact, ONEOK is benefiting from many growth areas that could fuel future earnings and dividends.

One prominent area of focus for the company is the robust demand for natural gas storage.

Following Winterstorm Elliott, there has been a notable resurgence in the need and desire for natural gas storage . Recognizing this trend, ONEOK has successfully re-contracted storage at favorable rates.

This strategic move has not only contributed to the company's growth but has also enabled them to revisit and expand on previous storage projects that were economically unviable at the time.

Moreover, ONEOK's expansion into the Bakken region has positioned the company for significant growth.

With long-term contracts in place and a comprehensive system that includes multiple plants and pipelines, ONEOK makes the case that it offers a compelling solution to producers.

The company's ability to provide a reliable and extensive system, especially in a region where gas drilling is primarily focused on oil extraction, highlights its strategic advantage and ability to align with customer needs.

{kind=link}

ONEOK Inc.

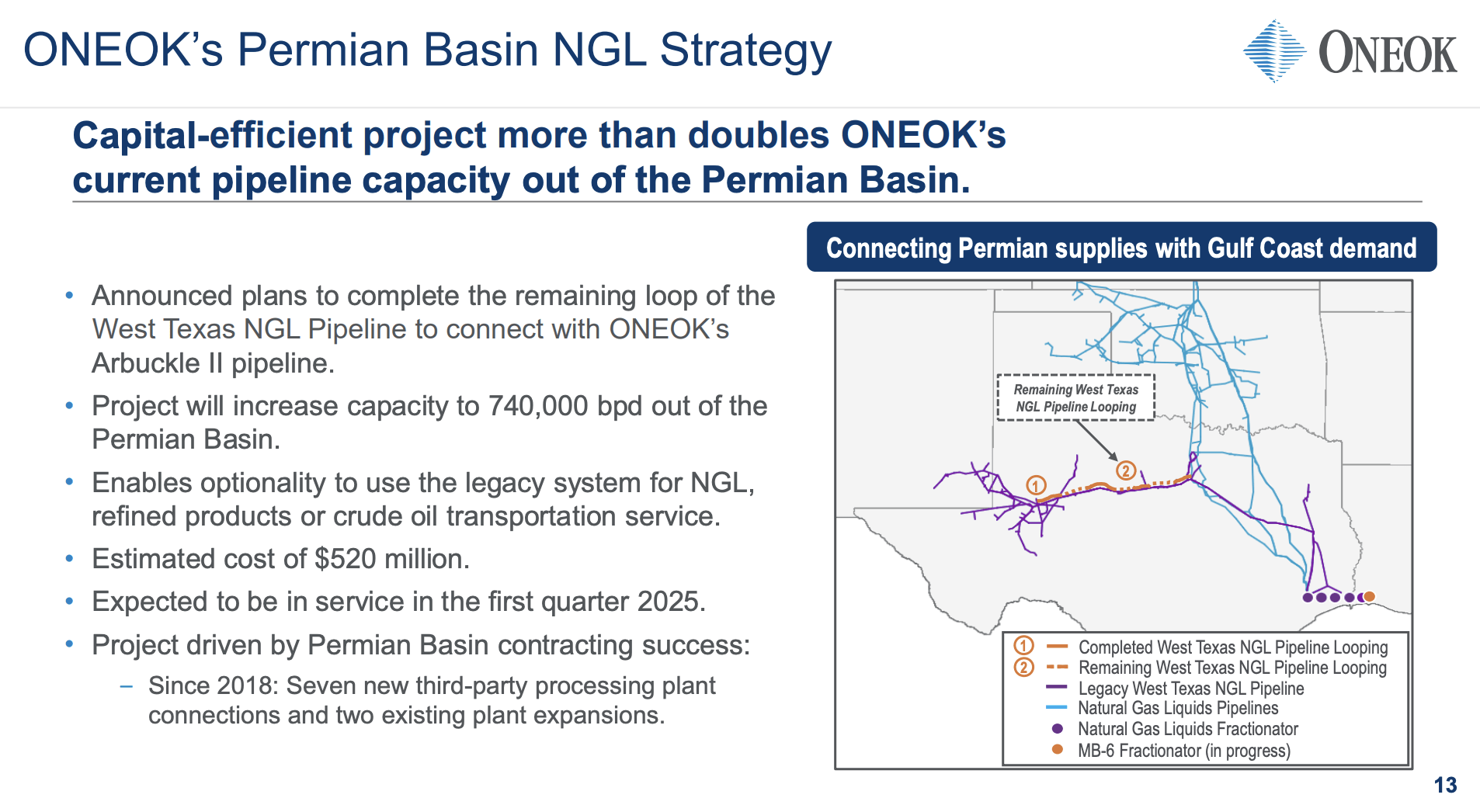

In terms of geographical expansion, ONEOK's presence in the Permian Basin signifies a strategic move to tap into the significant growth potential in the region.

Despite not having a gathering and processing footprint in that area, the company has demonstrated its competitiveness by strategically adding capacity and leveraging bundling opportunities.

This approach, coupled with a focus on connectivity and market competitiveness, positions ONEOK as a key player in the Permian NGL takeaway landscape.

{kind=link}

ONEOK Inc.

This brings me to the valuation part of this article.

Valuation

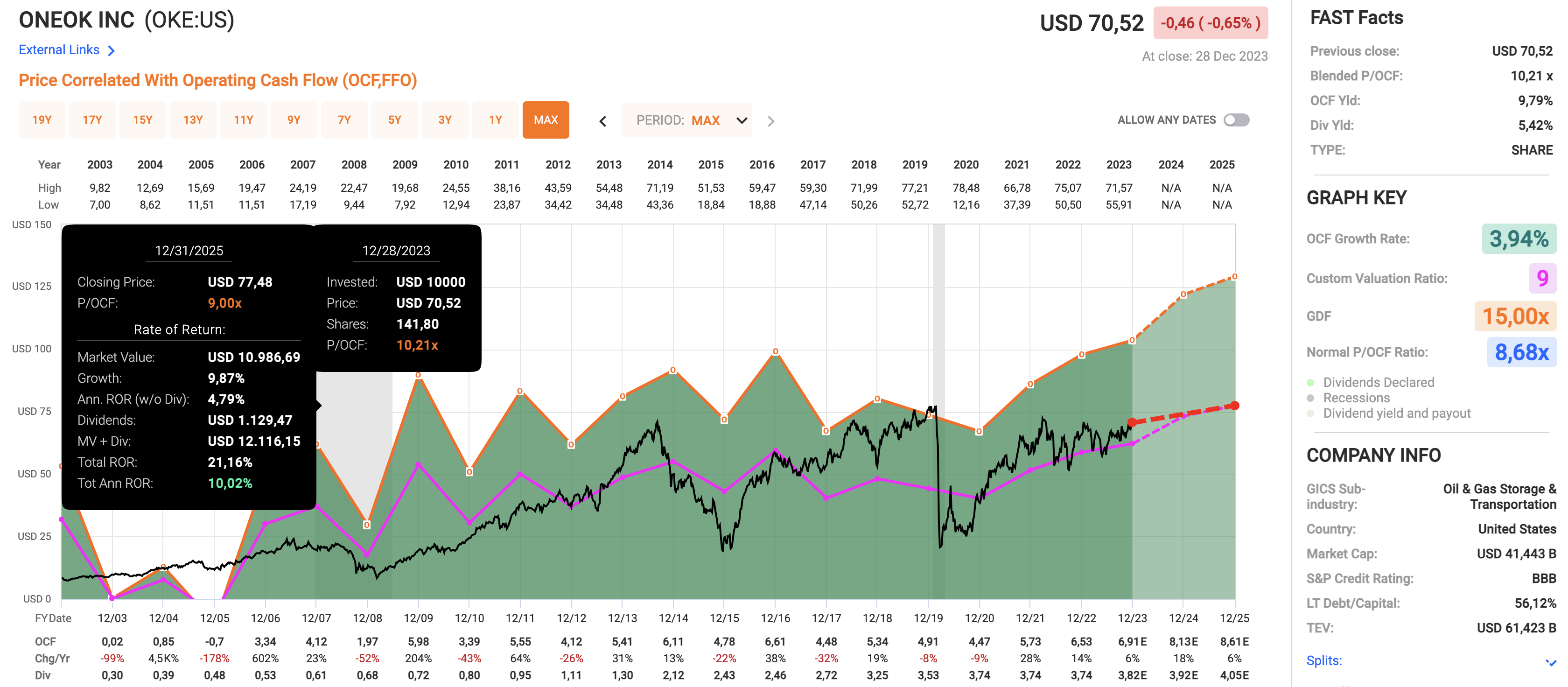

In light of the company's growth plans, analysts seem to agree. This year, operating cash flow ("OCF") is expected to grow by 6%, followed by 18% expected growth in 2024 and 6% growth in 2025.

Furthermore, using the data in the chart below.

- OKE is trading at a blended P/OCF multiple of 10.2x.

- Its long-term normalized valuation multiple is 8.7x. However, I believe a slightly higher number of at least 9.0x is warranted, as growth is likely to be more consistent.

- Hence, when combining a 9.0x valuation with expected OCF growth rates and its +5% dividend yield, we get a total return outlook of roughly 10% per year, which I believe is very fair.

- Since 2003, OKE shares have returned 13.9% per year!

{kind=link}

FAST Graphs

All things considered, I put OKE shares on my watchlist. I am likely to add more high-yield plays to my portfolio next year.

Given my high expectations for OKE, I believe it would make a great addition to my dividend (growth) portfolio, which focuses on strong companies with wide moats in future-proof industries.

Takeaway

Having recently added Antero Midstream to my portfolio, I'm now eyeing ONEOK as a standout high-quality income play.

With a remarkable 25-year history without dividend cuts, ONEOK distinguishes itself in the midstream sector.

Boasting a 5.4% yield, the company has slow but secure dividend growth, backed by a robust financial outlook.

Meanwhile, OKE's strategic acquisitions, cost synergies, and diversified operations, including a focus on natural gas liquids and expansion into key regions like the Permian Basin, position it as a top player in the industry.

Despite a slightly higher valuation, the combination of OKE's expected growth and over 5% dividend yield suggests a fair total return outlook of around 10% per year, making it a compelling addition to my dividend-focused portfolio.

For further details see:

5.4% Yield And Up To 10% Annual Return Potential - Buying Top-Tier Income With ONEOK