TTFNF - 5 Attractive Dividend Stocks From An Emerging Markets Country

Summary

- When looking for ways to diversify your investment portfolio outside of the United States, there are plenty of other possibilities.

- One option is considering companies from emerging markets: in today’s article, I will take a deep dive into the Brazilian stock market.

- I will show you 5 Dividend paying companies that I currently consider to be attractive in terms of risk and reward.

- However, due to macroeconomic and currency risks I would limit my investments in companies from the Brazilian Market to a maximum of 5% of your overall investment portfolio.

Investment Thesis

When aiming to diversify your investment portfolio among countries outside the United States, emerging markets often come into focus. In this article, I will present five companies from Brazil that I consider to be attractive in terms of risk and reward.

However, an investment in these companies comes with relatively high risk. This is particularly due to the macroeconomic and currency risks that come attached to such investments.

For this reason, I suggest not investing more than 5% of your overall portfolio into companies from Brazil. Implementing this strategy allows you to benefit from the advantages of an additional diversification of your investment portfolio, and, at the same time, you are limiting your risks.

The selected companies share the following characteristics:

- They have strong competitive advantages that contribute to building an economic moat over their competitors

- They are among the leading companies within their Industry / Sector

- They have a strong Profitability (underlying once again their strong competitive advantages over their competitors)

- They are attractive in terms of Valuation

- They pay shareholders a relatively attractive Dividend Yield

These are the five picks from Brazil that I consider to be attractive in terms of risk and reward:

- Itaú Unibanco (NYSE: ITUB )

- Petróleo Brasileiro S.A. – Petrobras (NYSE: PBR )

- Vale (NYSE: VALE )

- Banco do Brasil ( OTCPK:BDORY )

- Ambev (NYSE: ABEV )

Itaú Unibanco

Itaú Unibanco is among my top picks when thinking about investing in Brazil: this is based on the company’s strong competitive advantages (such as its strong brand image and broad distribution network) in combination with its attractive Valuation.

At this moment, Itaú Unibanco has a P/E [FWD] Ratio of 8.34, which is 19.28% below the Sector Median (10.33). Moreover, its current P/E [FWD] Ratio is 24.18% below the company’s Average P/E [FWD] Ratio from the past 5 years (11.00), thus reinforcing my belief that the leading Brazilian bank is currently undervalued.

When comparing Itaú Unibanco to leading U.S. banks such as JPMorgan (NYSE: JPM ) (P/E [FWD] Ratio of 10.91) or Bank of America (NYSE: BAC ) (P/E [FWD] Ratio of 10.25), we can see that Itaú Unibanco’s Valuation is significantly lower. However, in my opinion, these leading U.S. banks deserve to be rated with a significant premium when compared to Itaú Unibanco, due to their broad diversification and the significantly lower risks that come attached to an investment in them.

I also consider Itaú Unibanco to be an attractive pick, because of its enormous Profitability: the banks Return on Equity [TTM] is 61.25%, which is 445.25% above the Sector Median (11.23%). Itaú Unibanco’s Return on Equity is significantly higher than the one of Brazilian competitors such as Banco Bradesco (NYSE: BBD ) (ROE of 17.02%) or Banco Santander (Brasil) (NYSE: BSBR ) (15.60%). In addition, Itaú Unibanco’s ROE is also significantly higher than that of U.S. bank Citigroup (NYSE: C ) (ROE of 7.50%).

Furthermore, Itaú Unibanco’s Net Income Margin [TTM] of 57.17%, which is 108.20% above the Sector Median (27.46%), once again, indicates that the bank is an excellent pick in terms of Profitability.

The Brazilian bank pays a Dividend Yield [TTM] of 2.12%.

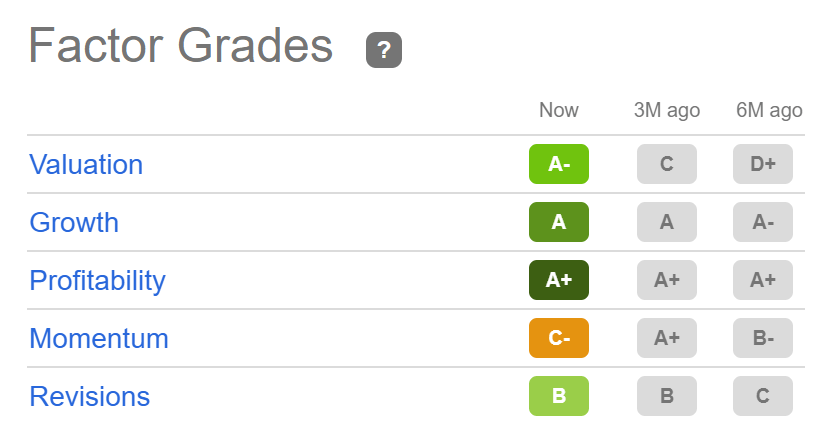

The Seeking Alpha Factor Grades support my theory that Itaú Unibanco is currently a buy: the banks receives an A+ rating in terms of Profitability and an A rating for Growth. For Valuation, the banks gets an A- rating. For Revisions, it gets a B and for Momentum, a C-.

{kind=link}

Source: Seeking Alpha

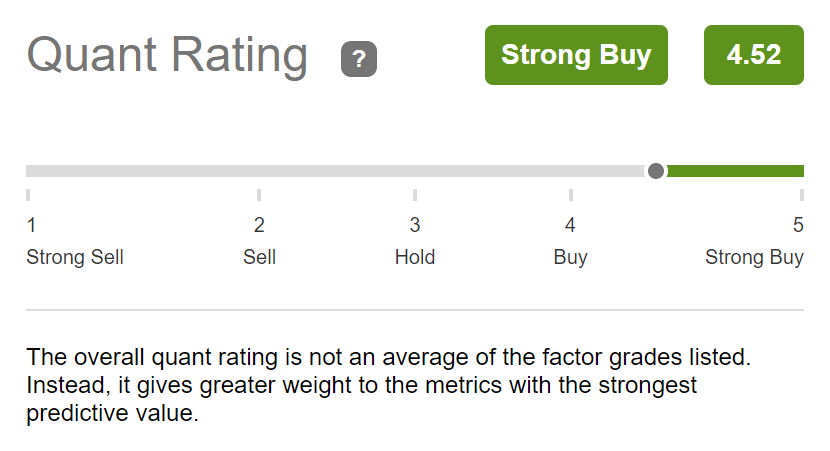

The Seeking Alpha Quant Rating, once again, supports the theory that Itaú Unibanco is currently highly attractive. According to the rating, the bank receives a strong buy rating, strengthening my belief to include it as part of this selection.

{kind=link}

Source: Seeking Alpha

Petróleo Brasileiro S.A. – Petrobras

Several metrics show us that Petrobras is an attractive pick for investors considering an investment in a company from an emerging market.

The company has a high EBIT Margin [TTM] of 47.54%, which lies 146.37% above the Sector Median (19.30%), indicating that it has an excellent competitive position and providing evidence of it being an excellent pick in terms of Profitability. The same is confirmed when looking at the company’s Return on Equity: its Return on Equity of 47.60% is 126.75% above the Sector Median (20.99%).

Petrobras is also attractive when it comes to Valuation: its current P/E [FWD] Ratio of 2.21 is 72.87% below the Sector Median (8.15). This Valuation is significantly lower when compared to U.S. competitors such as Exxon Mobil (NYSE: XOM ) (P/E [FWD] Ratio of 10.77), Chevron (NYSE: CVX ) (10.88) or Occidental Petroleum (NYSE: OXY ) (5.15). It is also significantly lower when compared to European rivals like TotalEnergies (NYSE: TTE ) (5.38), Shell (NYSE: SHEL ) (6.50) or BP (NYSE: BP ) (6.51). However, I also consider the risk of investing in Petrobras to be higher when compared to its U.S. and European competitors. Therefore, I would suggest not to invest more than 1.5% of your overall investment portfolio into the company if you decide on buying a position in Petrobras.

Petrobras Price / Book [FWD] Ratio of 0.97 is another indicator that the company is attractive in terms of Valuation: its Price / Book Ratio is 45.68% below the Sector Median (1.78).

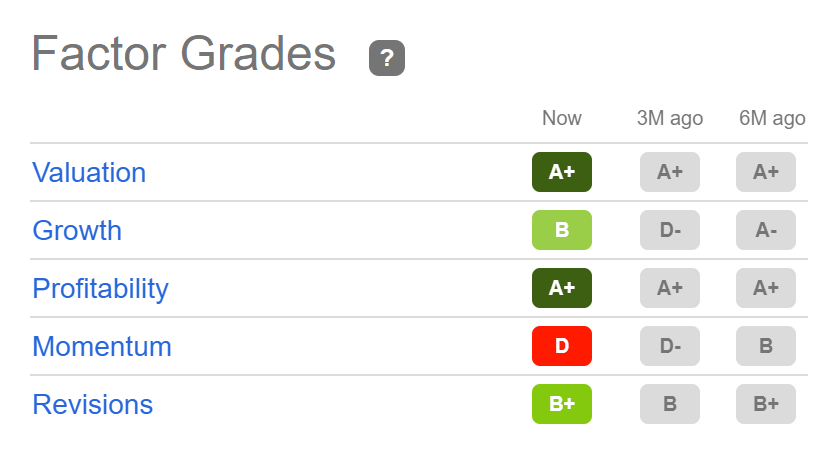

Petrobras attractiveness in terms of Valuation and Profitability is confirmed by the Seeking Alpha Factor Grades: for both Valuation and Profitability, the company receives an A+ rating. For Revisions, it gets a B+ rating and for Growth, a B rating. Only for Momentum, does the company get a less attractive D rating.

{kind=link}

Source: Seeking Alpha

Vale

Vale is a Brazilian company out of the Steel Industry that produces iron ore. Vale currently pays its shareholders an attractive Dividend Yield [TTM] of 8.86%. The company is an appealing choice to be part of this selection, particularly due to its current Valuation: the company has a P/E [FWD] Ratio of 4.63, being 68.29% below the Sector Median (14.61). At the same time, the company’s current P/E [FWD] Ratio sits 36.34% below its Average P/E [FWD] Ratio over the past 5 years (7.28).

In addition to that, Vale’s Price / Sales [FWD] Ratio is 1.75, which lies 65.50% below its Average Price / Sales [FWD] Ratio over the past 5 years, indicating once again that the company is an excellent fit in terms of Valuation.

Moreover, Vale is an attractive choice when it comes to Profitability: the company’s EBITDA Margin [TTM] of 51.79% is 164.74% above the Sector Median (19.56%), serving as a strong indicator that it is highly profitable with a strong competitive position.

The same is confirmed when taking a closer look at the company’s Return on Total Assets [TTM] of 24.49%, which is 355.75% higher than the Sector Median (5.37%).

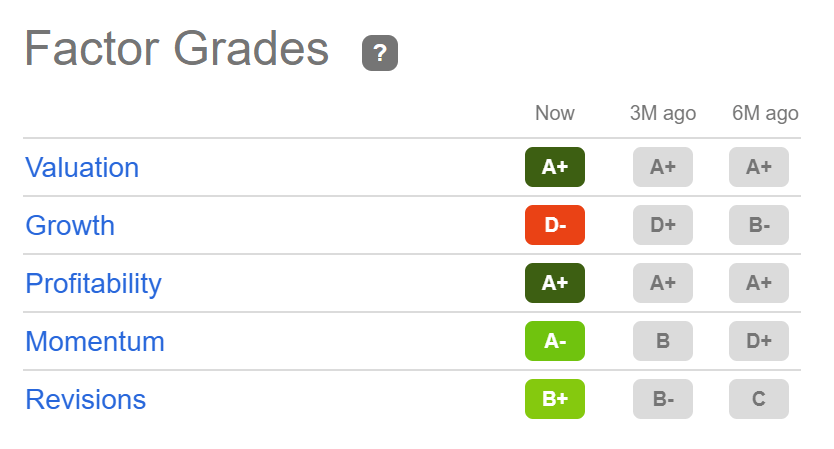

Vale’s strong Profitability and its attractive Valuation are underlined by the Seeking Alpha Factor Grades: for both the company receives an A+ rating. For Momentum, it has an A- rating and for Revisions, a B+. For Growth, the company gets a D-.

{kind=link}

Source: Seeking Alpha

Banco do Brasil

Banco do Brasil shows excellent results in terms of Profitability: its Return on Equity is 18.44%, which is 64.11% above the Sector Median (11.23%). Its Net Income Margin [TTM] of 33.00% lies 20.17% above the Sector Median (27.46%). Both are important metrics that confirm the bank's enormous Profitability and serve as indicators of its strong competitive position within its industry.

Banco do Brasil currently pays its shareholders a Dividend Yield [TTM] of 9.05%.

The bank has a P/E [FWD] Ratio of 3.77, which is significantly below the one of competitors such as Banco Bradesco (P/E [FWD] Ratio of 5.92) or Banco Santander (Brasil) (9.63). The company’s Price to Book [TTM] Ratio of 0.75 is significantly lower than that of the following competitors: Banco Bradesco (0.93), Banco Santander (Brasil) (1.38).

The Seeking Alpha Factor Grades also underline that Banco do Brasil is an excellent choice in terms of Valuation and Profitability: for both, the bank is rated with an A+ rating. For both Growth and Revisions, it receives an A rating, while it gets a B- for Momentum.

{kind=link}

Source: Seeking Alpha

The Seeking Alpha Quant Ranking further underlines that Banco do Brasil is an excellent choice when compared to its peer group. The bank is ranked 5 th out of 60 within the Diversified Banks Sector and 13 th out of 666 within the Financials Sector. It is ranked 49 th out of 4764 in the overall ranking.

Source: Seeking Alpha

In addition to that, Banco do Brasil is currently a strong buy according to the Seeking Alpha Quant Rating, which once again underlines my own buy rating for the Brazilian bank.

{kind=link}

Source: Seeking Alpha

Ambev

Ambev currently pays an attractive Dividend Yield [TTM] of 5.89%. Its Payout Ratio of 67.41% indicates that there is enough room for future Dividend enhancements. The company's current Dividend Yield is 188.23% above its Average Dividend Yield [TTM] from over the past five years (2.04%), serving as a first indicator that Ambev is currently undervalued.

At this moment in time, the company has an attractive Free Cash Flow Yield [TTM] of 6.28%, which is 38.39% above the Sector Median (4.54%). At the same time, its current Free Cash Flow Yield [TTM] is 100.39% above its Average over the past 5 years.

Furthermore, it can be highlighted that Ambev’s P/E [FWD] Ratio of 15.49 is 23.73% below the Sector Median (20.32) and 30.40% below its Average P/E [FWD] Ratio from the past 5 years (22.26). Both metrics offer further reason to believe that Ambev is currently undervalued.

In addition to that, it can be highlighted that its Price / Cash Flow [TTM] Ratio of 10.14 is 34.93% below the Sector Median (15.59), indicating that the price you pay for the stock is relatively attractive in comparison to the Free Cash Flow generated by the company.

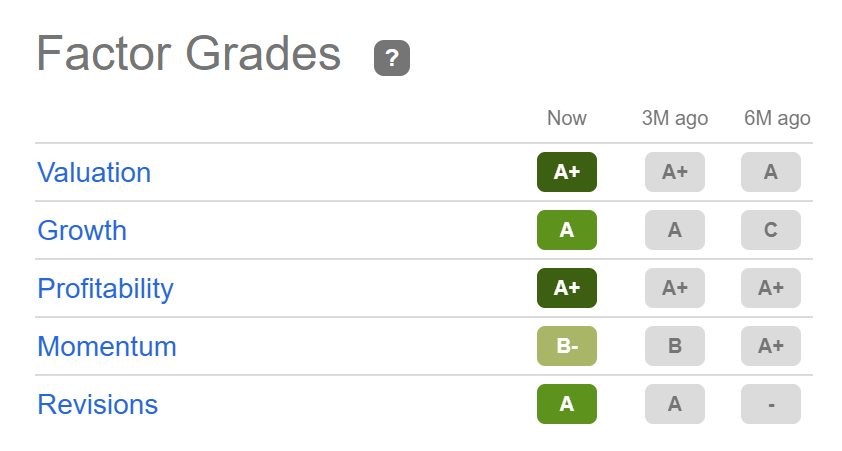

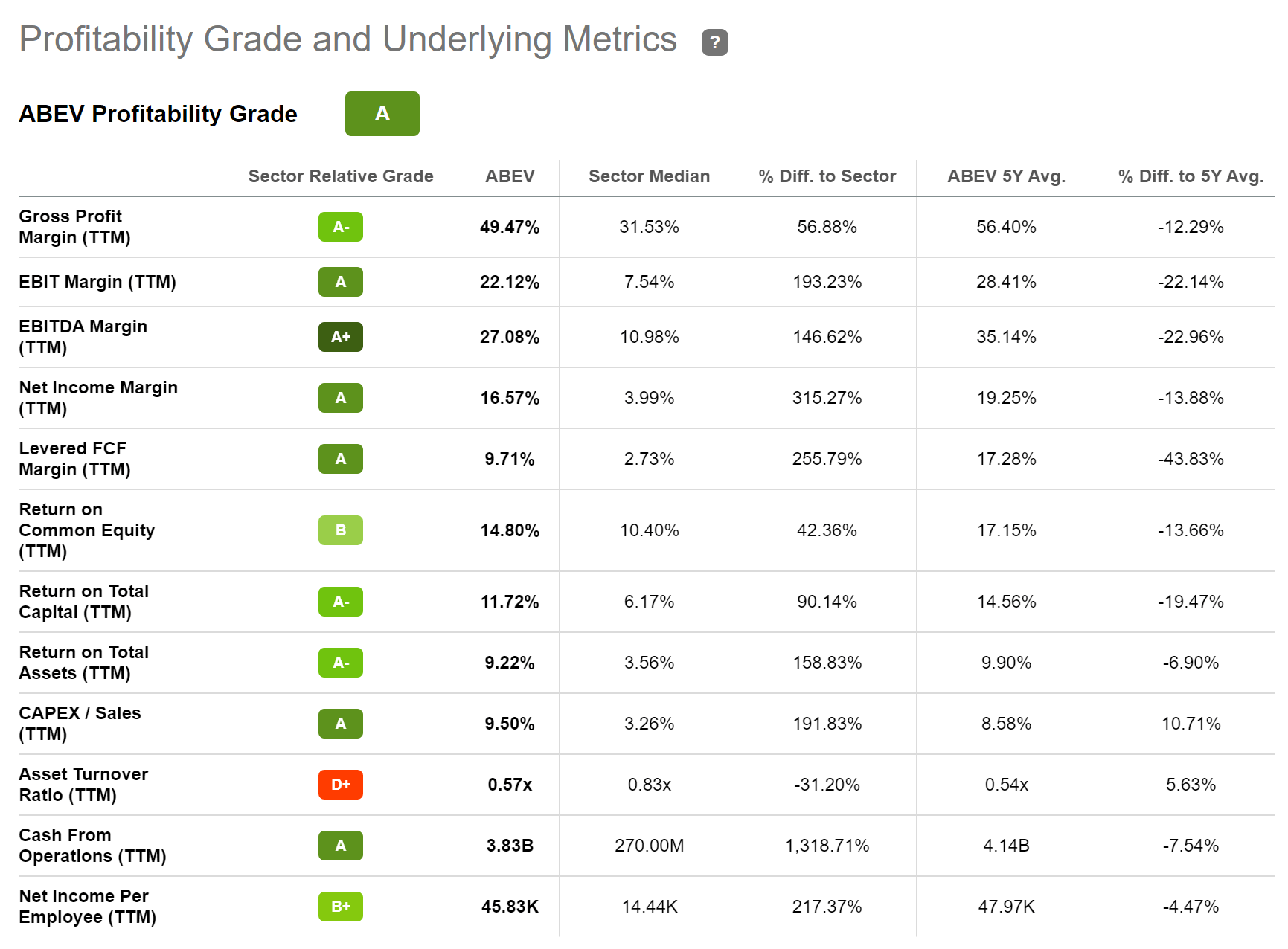

Having a closer look at the Seeking Alpha Profitability Grades for Ambev, we can further see that it’s highly profitable: Ambev has an EBIT Margin [TTM] of 22.12%, which is 193.23% above the Sector Median (7.54%). Moreover, its Return on Equity of 14.80% is 42.36% above the Sector Median (10.40%). Ambev’s Profitability metrics underline its strong competitive position within the Brewers Industry and further strengthens my belief to make the company part of this selection.

Below you can find the Seeking Alpha Profitability Grades for Ambev.

{kind=link}

Source: Seeking Alpha

There are additional companies from Brazil that I consider to be attractive when it comes to risk and reward: among these picks are growth companies such as Nu Holdings (NYSE: NU ), StoneCo (NASDAQ: STNE ) and XP (NASDAQ: XP ). Through his holding company Berkshire Hathaway (NYSE: BRK.B ), star investor Warren Buffett is invested in the first two companies, which we can interpret as an additional quality indicator for both.

Since all of these picks have performed relatively poorly within the past 12 month period (Nu Holding’s has shown a performance of -48.92%, StoneCo of -26.79% and XP -52.59%), they are currently available for an attractive Valuation. However, none of them currently pay a dividend. For this reason, they are not part of this list that focuses on dividend paying companies from Brazil.

Conclusion

When selecting these five Brazilian dividend paying companies, I have paid particular attention to them all having strong competitive advantages over their competitors and being among the leading companies within their respective industry. All of these picks have at least an A rating in terms of Profitability as according to the Seeking Alpha Factor Grades, thus underlying the excellent competitive positions they hold within their Industries. Moreover, they have at least a B+ rating in terms of Valuation.

Investing in companies with strong competitive advantages, and that are highly profitable, contributes to the fact that you don’t need to worry so much about losing your money when the price of their stock decreases. This is because you know that the company you have invested in will survive in the long term.

However, when considering an investment in companies from outside the U.S. you have to be aware of the additional risk factors that come attached to such an investment. When investing in companies from Brazil, I see the relatively high macroeconomic and currency risks as being the main factors to consider. In the event that the Brazilian Real depreciates against the dollar in the future, the dividend payments you receive from companies may also become worth significantly less.

Particularly due to the high currency risks that come attached to an investment in companies from Brazil, I suggest that you don't invest more than 5% of your overall investment portfolio in such companies (the sum of all your investments in Brazil should not exceed 5% of your total investment portfolio). By doing so, you can benefit from having an additional diversification for your investment portfolio and, at the same time, you limit the risks that come along with an investment.

Author’s Note: Thank you for reading! I would love to hear your opinion on this article and to know which are your favorite emerging markets stocks!

For further details see:

5 Attractive Dividend Stocks From An Emerging Markets Country