INTC - 5 Economic Themes And A Dividend Investor's Allocation Strategy For 2023

Summary

- There are five themes to watch for in 2023 that will have big impacts on the economy and markets.

- Pretty much everyone expects a recession in 2023. That makes the contrarian in me uncomfortable, but I agree with the consensus.

- How bad could a recession in 2023 be? It's hard for me to get too bearish or too bullish.

- Prepare for falling inflation and (eventually) falling interest rates.

- I offer three categories of dividend stocks to which I'm allocating more capital going into 2023.

Every year around the turning of the calendar, I try to sit down and think through our current position in the economic cycle and what's likely to come during the next year. That helps me decipher economic themes and ultimately an allocation strategy for what's ahead.

In what follows, I offer five themes to watch for in 2023, followed by a discussion of my personal allocation decisions in light of those themes.

1. Falling Inflation

The year-over-year rate of inflation appears to have peaked in the middle of summer this year and has been on the decline ever since.

Of course, one would naturally recoil at the idea that 7.1% inflation is good news. But this YoY metric communicates the combined price hikes that have taken place over the last 12 months, not necessarily the real-time movements of prices today.

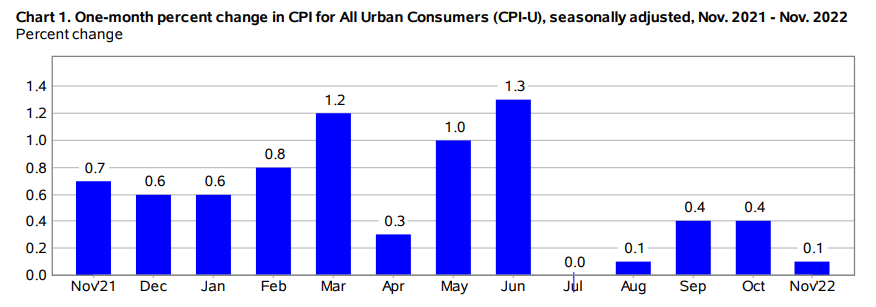

To get a better picture of up-to-date inflation, let's look at the month-over-month CPI from November 2022:

{kind=link}

Bureau of Labor Statistics

As you can see, the big MoM increases in consumer prices ended abruptly in June and have been in a historically normal range since then.

In fact, if not for the lagging "shelter" (housing) component of the CPI, the MoM CPI reading would have been negative over the past two months.

Consider this: Since the middle of summer, the price of crude oil dropped by about 40% through around December 12th. That's called deflation!

Let's back up and get a bigger picture here. The Fed distinguishes three main factors influencing the rate of inflation:

- Core Goods : During the pandemic, this was the central area of concern and the biggest contributor to inflation, as bottlenecks in the production and supply chain along with unprecedented government fiscal stimulus caused a massive mismatch between supply and demand. Today, this area is finally (mostly) under control, and little further inflation is expected for goods.

- Housing : A lagging indicator for home prices and new rent rates. This lags for a few reasons. First, not everyone buys a home every year, so home prices alone aren't that meaningful to most people from the perspective of their regular consumer spending. What matters more are property insurance, taxes, and home maintenance that do go up along with home prices. Second, rent rates being signed on new leases today don't reflect the rent rates being paid for all leases. Rent jumps up for individual renters over time as leases come due and roll over at those higher rates, and thus big increases in rent rates only gradually work their way into the data.

- Core Services : These are all the myriad other services besides shelter that Americans use, from air travel to hotels to pedicures to pool cleaning. Since they largely involved face-to-face contact with other humans, services suffered the worst during the pandemic and saw the least inflation. But now this is the biggest area of concern for any further inflationary pressure.

People are still traveling and catching up on all the human interaction-y things that they missed out on during the pandemic. So, services are still going strong.

But goods and housing are no longer contributing to upward inflationary pressure like they were 6 months to a year ago. In fact, since housing costs only influence the CPI with a lag, the upward pressure on the CPI we are getting right now from what housing prices were doing 6 months ago will eventually reverse and create a drag on the CPI because of the dropping home prices and rent rates we are experiencing today.

I wrote in much greater detail why inflation is likely to keep falling in " Why Inflation Has Likely Peaked ."

Ultimately, I think inflation will settle back into the 2-3% range a year or so from now, barring any more fiscal shocks such as another round of helicopter money from Uncle Sam.

2. The Fed as an Unreliable Narrator

In literature, there's a concept called the "unreliable narrator."

In books, we trust the narrator inherently. After all, why would they lie to us? They're the one with total control over the story. We only know what they tell us.

But in some stories, whether books or movies, the narrator does lie to the audience, and we only find that out later on. This is called an "unreliable narrator." Once the audience realizes the unreliable narrator has lied once, their credibility is permanently compromised. Everything they say is now questionable.

The Fed is an unreliable narrator of the US economy and their own future actions.

Sometimes the Fed deceives the public with planned and purposeful posturing that is intended to produce a certain outcome.

For instance, the market freaked out when it saw the Fed's recent dot plot projection for the Fed Funds rate to reach 5.125% by December 2023, but this strikes me as the Fed simply using their "forward guidance" as another policy tool to tame inflation.

What do I mean by that? Well, note that the Fed views "forward guidance" (what they say they are going to do in the future) as one of its monetary policy tools. The market and consumers react to what the Fed says they are going to do, and then the Fed has less work to do with, well, actual monetary policy like adjusting interest rates.

The funny thing is that the market usually falls for it. I'm reminded of an adult doing a silly, simple magic trick for a little kid over and over again. The kid is stunned by it every time, as if each iteration was the first time they'd seen it.

One thing that seems abundantly clear if you look at the Fed's history of forward guidance: Don't listen to what they say they are going to do. Just watch the data.

The Fed is an unreliable narrator.

3. Persistent Labor Shortage

At this point, you might object that the labor market is still red hot, with the unemployment rate at an ultra-low 3.7%. How can inflation persistently fall and the Fed change course in such an environment?

But employment is a lagging economic indicator, not a leading one.

It makes sense if you think about it. From the time a company identifies that they need more workers and posts a job opening online to the date that employees are actually hired can be weeks or months. And then time it takes to gather data about new hires and release the BLS report that ends up getting cited on CNBC takes another few weeks or so.

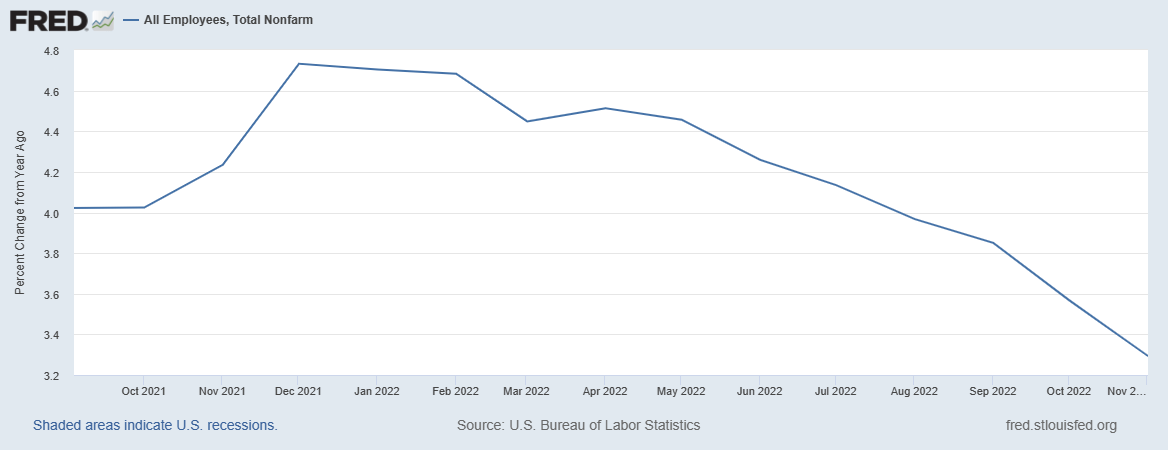

Rather than a snapshot in time, it's better to look at the trend in employment growth. When looking at the year-over-year growth in all nonfarm employees, we find that the trend has been downward since the beginning of 2022.

{kind=link}

St. Louis Federal Reserve

At the current pace of decline, growth in total employment should turn negative by around the middle of Spring 2023 - if the trend continues, of course.

Okay, that's the short-term outlook for employment, but what about the bigger picture?

Even before the pandemic began, there were signs of a labor shortage as younger workers were not replacing retiring baby boomers fast enough.

As I wrote about in an article on the labor shortage and robotics stocks for High Yield Investor, the pandemic greatly exacerbated this trend. Early retirements spiked up during the pandemic and continuing to today, and older workers who exited the workforce have not come back for the most part. Their experience cannot easily or quickly be replaced.

Amid aging demographics, this persistent labor shortage, driven by more retiring boomers than millennials and Gen Zers entering the workforce, appears set to continue.

What is the upshot for 2023?

My general take is that the employer mindset of "labor hoarding" may go dormant next year but won't disappear entirely. Some firms will be more proactive about hiring for their future needs when unemployment rises, while others will invest in machines/equipment/software that will reduce their total labor needs.

Put together, I think these factors should ensure that the unemployment rate does not spike as high as it typically does during downturns and/or won't stay high for very long.

I seriously doubt, though, that this labor shortage will cause wage growth to remain persistently and problematically high - high enough to cause inflation to remain higher than 3-4%.

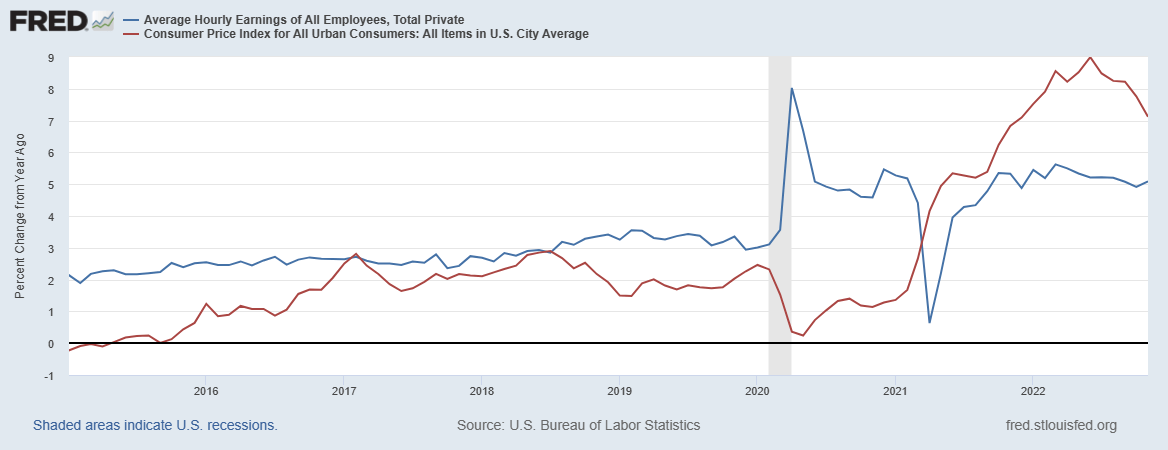

The spike in wage growth in 2020 was largely because employers had to compete with enhanced unemployment benefits and stimulus checks. In the last two years, though, wage growth has simply been trying to catch up to inflation.

Notice that since the early months of 2021, the YoY CPI (red line) has been higher than YoY wage growth (blue line):

{kind=link}

St. Louis Federal Reserve

Understandably, wage growth would lag inflation, because wages & salaries aren't adjusted as frequently as consumer prices. Moreover, workers tend to push for higher wages only after they've already begun to feel the pinch of inflation.

4. Widely Anticipated Recession

Almost everyone who pays attention to markets or the economy is expecting a 2023 recession at this point.

Consider, for example, an October survey showing that 98% of CEOs expect a recession in the next year or so.

Now combine this with perhaps the most reliable forward indicator of an oncoming recession known to man: the inverted 10-year minus 3-month Treasury yield spread, which is now flashing "Recession Alert!"

The yield curve hasn't been this inverted since the early 2000s, and before that, the early 1980s.

Contrarianism is in my nature. When everyone in the room believes one thing, I often reflexively defend the other side. I instinctively dislike the excesses and dangers that often come with groupthink. (I would point to the extreme polarization of American politics as Exhibit A.)

That said, I'm with the consensus on this one.

Barring another big round of fiscal stimulus, which would boost aggregate demand in the short run but would almost certainly result in another spike in inflation after the initial sugar rush, the most bullish I can get on the economy is that the economy slows considerably but just barely remains out of official recession territory.

On the other hand, the most bearish I can get isn't that bearish. The labor market is strong. There's plenty of pent-up demand for homes, just waiting for lower mortgage rates. The supply-demand equilibrium for oil appears to be settling in a favorable range for both consumers and oil companies.

So, how bad will this widely anticipated recession actually be? My guess is that it won't be that bad, with some overleveraged parts of the market that few pay attention to bearing the brunt of the pain.

But perhaps the most important point to note about a 2023 recession is that it, along with falling inflation, is likely to cause interest rates to drop as well. Recessions have an excellent track record of bringing down both inflation and interest rates.

5. The Rebound of Tech & Real Estate

In 2022, it's striking to note the massive disparity in performance between energy stocks ( VDE ) and REITs/real estate ( VNQ ) & technology stocks ( VGT ):

I don't necessarily envision this chart totally reversing in 2023, because I think oil is reaching an equilibrium where the price isn't likely to shoot up or collapse down again, barring some unforeseen shock.

I don't think the bull market for the energy sector is over, but will it have another year of 50%+ appreciation in 2023? I doubt it.

On the other hand, I expect the factors that severely beat down the technology and real estate sectors in 2022 to reverse in 2023. Rising inflation and interest rates in 2022 should give way to falling inflation and interest rates in 2023, setting the stage for a nice rebound in beleaguered tech stocks and REITs.

Now, do these sectors have further to fall before they bottom out? Maybe, maybe not. But I do think they will end 2023 higher than they start it.

Allocation Focus Going Into 2023

To be clear, I am not a short-term trader who tries to buy low and sell high on a regular basis. I am a long-term, buy-and-hold-until-the-thesis-breaks investor with a particular focus on dividend growth stocks.

So, when I talk about my allocation decisions going into 2023, I am not talking about selling stocks over here and reallocating that capital over there. I'm instead talking about where I'm going to focus new buying, using cash from saved income and dividends.

Below I highlight three areas of allocation focus going into 2023:

1. Renewable Energy

I am aware of the thoughtful arguments against overreliance on renewable energy as well as the paucity of available rare earth metals and resources required for production of renewable energy assets and batteries.

But just as it can be unwise to fight the Fed, it can also be unwise to fight the federal government. The Inflation Reduction Act creates a 10-year runway of guaranteed tax credits for the installation and production of renewable energy and battery storage facilities, and "REPowerEU" does something similar for Europe.

Renewable energy power producers should hugely benefit from this long growth runway, made even more profitable by Uncle Sam.

My favorite opportunities in this space are:

- Brookfield Renewable Partners ( BEP , BEPC )

- Clearway Energy, Inc. ( CWEN , CWEN.A )

- NextEra Energy Partners ( NEP )

These are dividend growth all-stars, offering both 4%+ yields and 5-13% annual dividend growth rates. And with the wind at their backs (literally and figuratively), they have many more years of growth to come.

2. Blue-Chip Growth REITs

REITs and growth stocks have been punished severely in 2022, which means that the REITs with high growth rates and high valuation multiples have been particularly beaten up. Three of my favorites are:

These three should be able to weather a recession with minimal damage to their fundamentals, while the lower interest rates brought on by a recession would massively benefit them and likely result in their valuation multiples expanding again.

3. Beaten Down Cyclicals

Finally, because the oncoming recession is widely anticipated, certain cyclical stocks have been absolutely pummeled in anticipation of future weakness. But, given their big selloffs this year, I would guess that these stocks will actually begin to rebound when that pain eventually comes. Stock prices anticipate the future, after all, and if the Fed gives them a reason for hope in the form of rate cuts, the future will begin to look brighter.

Four of my favorite beaten down cyclicals that I'm buying now are:

- Leggett & Platt ( LEG )

- Avient Corporation ( AVNT )

- Whirlpool Corporation ( WHR )

- Intel Corporation ( INTC )

Many of LEG's products end up in vehicles, furniture, and beds, all discretionary products that are often purchased with financing or loans.

Likewise, WHR's home appliances are often purchased as replacements when consumers are feeling flush with cash, and new units are put in newly constructed homes. But consumers currently aren't feeling flush with cash, nor are as many new homes being built.

AVNT's formulants are intermediate products found in countless goods across all sectors of the economy. As such, AVNT's fundamentals typically correlate with GDP growth pretty closely.

Lastly, INTC's struggles with its lagging technology are well-known, as is its significant cash burn rate right now as the company invests heavily in semiconductor fabrication plants in the US and Europe. However, between the CHIPS Act and a $15 billion investment from Brookfield Infrastructure ( BIP , BIPC ), it is looking like INTC will be able to fund its heavy investments over the next few years while keeping its dividend intact.

Benediction

I've made some mistakes in 2022, and I've also done some things right.

Perhaps the biggest investment success I've achieved is simply sticking with my dividend growth strategy as outlined in last year's end-of-year missive titled " Death Of A Capitalist - And Investing Principles For 2022 ."

Looking back on the last year, are there some things I could have and should have done differently? Yes.

But at the same time, I think many minor mistakes are covered up and forgotten in time if one just sticks to a well-thought-out investment strategy that fits their personality and financial goals.

Ultimately, my goal is to achieve financial independence by generating a sustainable dividend income stream large enough to afford a comfortable standard of living while also leaving room for some reinvestment and charitable giving.

Fortunately, nothing got in the way of my progress toward that goal in 2022, and I hope the same holds true for 2023.

As always, I am grateful for Seeking Alpha and the many readers who give insightful, encouraging, and sometimes challenging comments. The result is a level of intelligence and civility among online interlocutors that simply can't be found anywhere else on the Internet.

We are a community of investors who understand the concept of an expanding pie, and that the contest of ideas is not against each other but against falsehoods and poor returns. Investing is a game we can win together, even and especially if we have different philosophies and strategies.

Iron sharpens iron. You, dear reader, have sharpened my thinking in 2022, and I hope happens in 2023.

Merry Christmas, Happy New Year, and may 2023 be a healthy and prosperous year for us all!

For further details see:

5 Economic Themes And A Dividend Investor's Allocation Strategy For 2023