UBP - 5 Quality REITs Yielding Over 5%

2023-04-25 08:30:00 ET

Summary

- In the 2010s, 5%+ dividend yields from moderately high-quality stocks were hard to come by. Today, not so much.

- REITs have been hit particularly hard in the current market by higher interest rates and negative sentiment.

- I highlight 5 moderately high-quality REITs with 5%+ dividend yields, paying special attention to their balance sheets and dividend safety.

I began investing in the 2010s during a drought. It wasn't a water drought. It was a yield drought.

The Federal Reserve held their key interest rate at basically zero. As inflation remained muted, the Fed's low interest rate caused Treasury bond yields to compress. (In Europe, trillions of euros of government debt even reached into negative yield territory.)

Lower Treasury yields pushed down municipal and corporate bond yields as well. In turn, this caused bond proxies like preferred stocks to trade at or above their par/redemption values. And finally, even common stock dividend yields compressed to some of their lowest average levels in history.

Savers couldn't generate any yield whatsoever from bank savings accounts, so they moved up the risk ladder. Everyone did. To find high yields, investors had to accept more risk.

Today, the situation is dramatically different.

Relatively high yields from strong companies with quality assets and solid balance sheets are possible to obtain now.

How long will these relatively high yields remain available? Will values get even better soon? Or could the window of opportunity to buy quality high yields close soon as stock prices rebound?

I don't know. I readily admit that I am no market-timing wizard. My strategy, and the strategy I believe most investors should follow, is to:

- buy quality companies at reasonable prices (and, for me, attractive dividend yields),

- enjoy the high returns (and dividends!) generated by those quality companies indefinitely , and

- only sell if the investment thesis breaks.

Investors are often too smart for their own good and overcomplicate the investing process. But take a look at most of the greatest long-term investors of all time, including Warren Buffett, Charlie Munger, Terry Smith, and others, and you'll find the simple formulation presented above to be disproportionately represented among them.

So, since the market has given us the opportunity to buy quality companies at higher-than-average yields, I suggest we not look this gift horse in the mouth.

Many real estate investment trusts ("REITs") in particular are a strikingly good value right now, in my estimation, partially because of the strong (but fallacious) correlation between "commercial real estate" and office buildings in the broader media. I discussed this in " Blue Chip Real Estate Is A Bargain - Top Picks Across 5 Sectors ."

Let's look at five more quality REITs. These five may not be quite the same level of quality as the five presented in the article above, but they offset this small step-down in quality with dividend yields over 5%.

Armada Hoffler Properties ( AHH )

- Dividend Yield: 6.5%

AHH primarily owns and develops mixed-use centers on the East Coast, although the REIT also owns some single-use multifamily, retail, and office properties.

{kind=link}

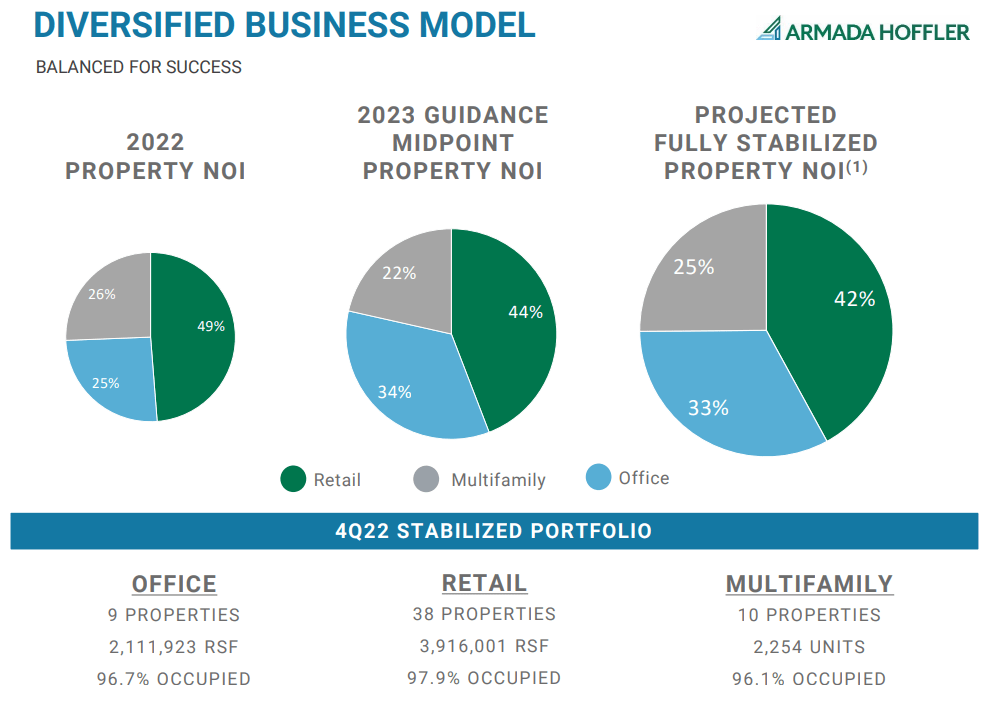

The market seems to be fretting over AHH's office exposure (about 1/3rd of total NOI this year), but it's important to remember that these are Class A, trophy office buildings that have actually been benefiting from the flight to quality among office tenants. Hence the strong 96.7% occupancy rate.

One example of the quality of AHH's office buildings is Thames Street Wharf in downtown Baltimore, completed in 2010 and leased to Morgan Stanley.

{kind=link}

It's a state-of-the-art building in an unbeatable location (adjacent to the Inner Harbor and walking distance to the National Aquarium) with high barriers to entry, and it is leased to a strong tenant with high name recognition. The mixed-use center in which Thames Street Wharf is located also boasts financial giants like Transamerica and T. Rowe Price ( TROW ) as tenants.

While this is admittedly one of AHH's "crown jewel" office properties, it does exemplify the characteristic quality of its office exposure.

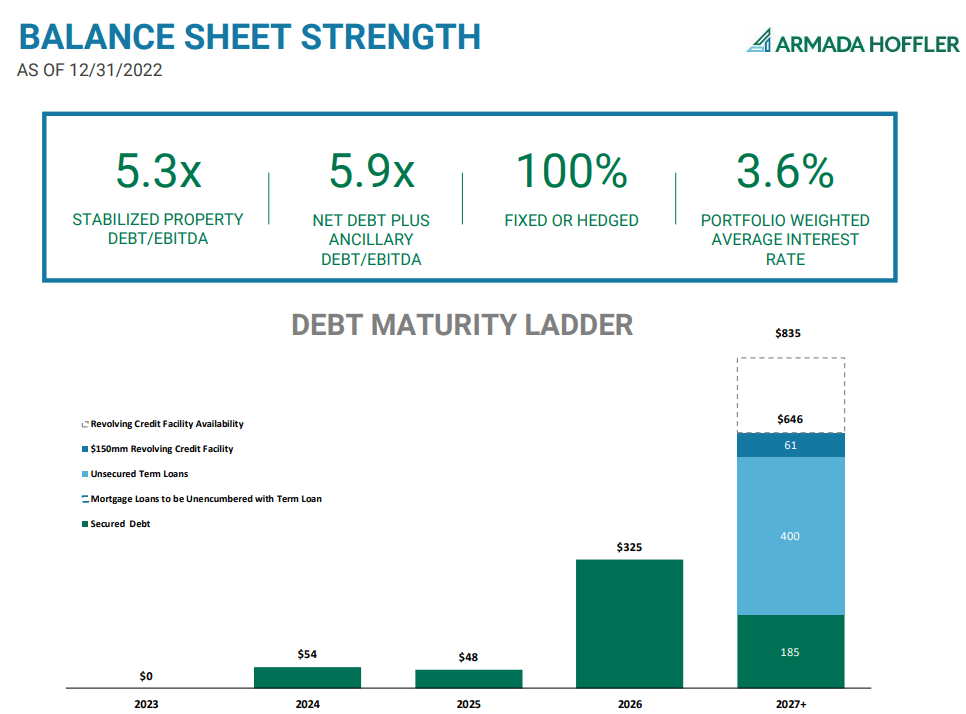

Moreover, unlike some of the troubled office REITs with high debt and lots of upcoming debt maturities, AHH's balance sheet (recently rated "BBB" by DBRS Morningstar) has relatively low debt at net debt to EBITDA of 5.3x for the stabilized portfolio and 5.9x including debt associated with development projects.

{kind=link}

Notably, 100% of AHH's debt at this point is fixed-rate or hedged to make it effectively fixed-rate for some period of time. About 60% of debt is truly fixed-rate, while 40% is variable rate with some sort of hedge in place (caps or swaps) to keep the rate flat.

What's more, AHH has no debt maturing for the rest of this year and very little maturing in 2024 and 2025. As such, refinancing risk is very low at this point.

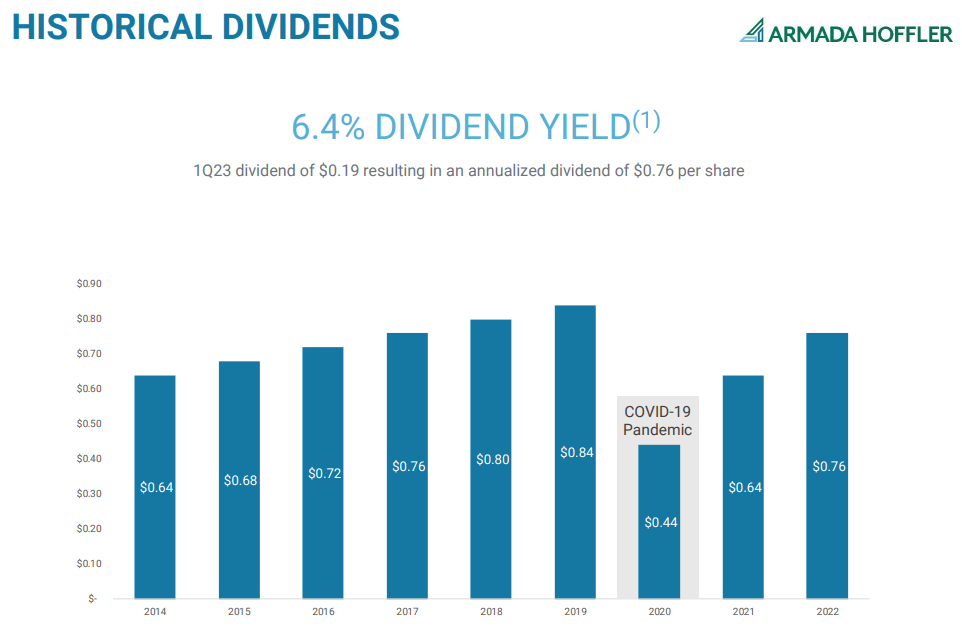

During COVID-19, AHH understandably took a big hit when the REIT cut its dividend nearly in half. But given social distancing measures (especially on the East Coast), that cut appears to have been necessary. Since then, AHH has been bumping up its dividend back towards pre-COVID levels at a rapid pace.

{kind=link}

The current annualized dividend of $0.76 represents a payout ratio of only 61% of 2023 NFFO (closer to 80% of AFFO), making the dividend safe and likely to continue growing.

And at a 6.5% dividend yield, the dividend does not need to grow that fast in order for AHH to be a solid performer for dividend growth investors and income investors alike.

Hannon Armstrong Sustainable Infrastructure ( HASI )

- Dividend Yield: 5.5%

HASI invests in renewable energy and other sustainable infrastructure assets primarily through secured debt and preferred equity. Although structured as a REIT, HASI is perhaps most similar to a business development company ("BDC").

{kind=link}

HASI's portfolio has three broad categories:

- Behind-the-meter , such as residential rooftop solar panels

- Grid-connected , including solar and wind farms that feed into the electrical grid

- Sustainable infrastructure , including green building modifications

The average investment is around $12 million, generates an average yield of 7.5%, and has a remaining contract term averaging 17 years. Most of HASI's customers are utilities, large corporations, or government entities. The company has an excellent history of credit underwriting, having taken less than 20 basis points of credit losses since 2012.

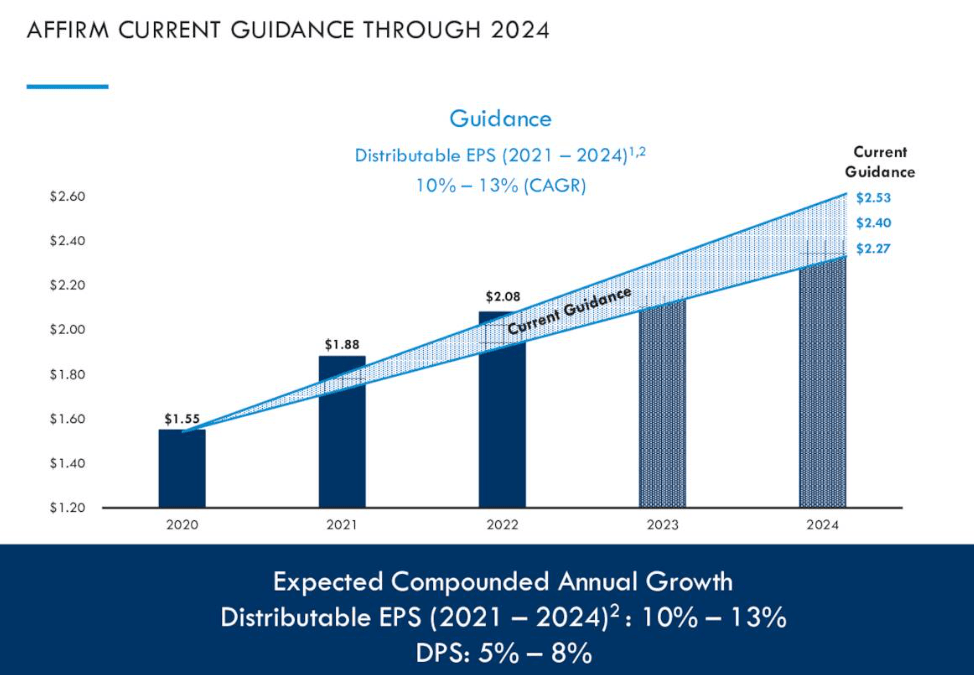

From 2014 through 2022, HASI has grown its distributable EPS at an average annual rate of 11%. Perhaps not coincidentally, HASI also has also established a track record of generated a distributable EPS return on equity of around 11%. Management projects another 10-13% distributable EPS growth in 2023 and 2024 as well.

{kind=link}

As for the balance sheet, HASI hovers right on the edge of investment grade and sub-IG with its Baa3 rating from Moody's and BB+ rating from Fitch. The company ended 2022 with about $870 million in liquidity, mostly in the form of undrawn capacity on its revolver.

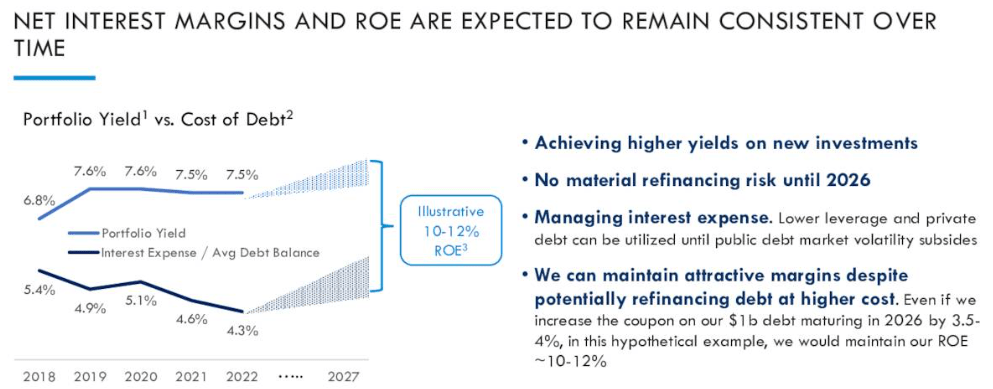

And though 14% of HASI's debt is floating rate, management believes that higher investment yields going forward should offset higher interest expenses such that its ROE can be maintained at 10-12%.

{kind=link}

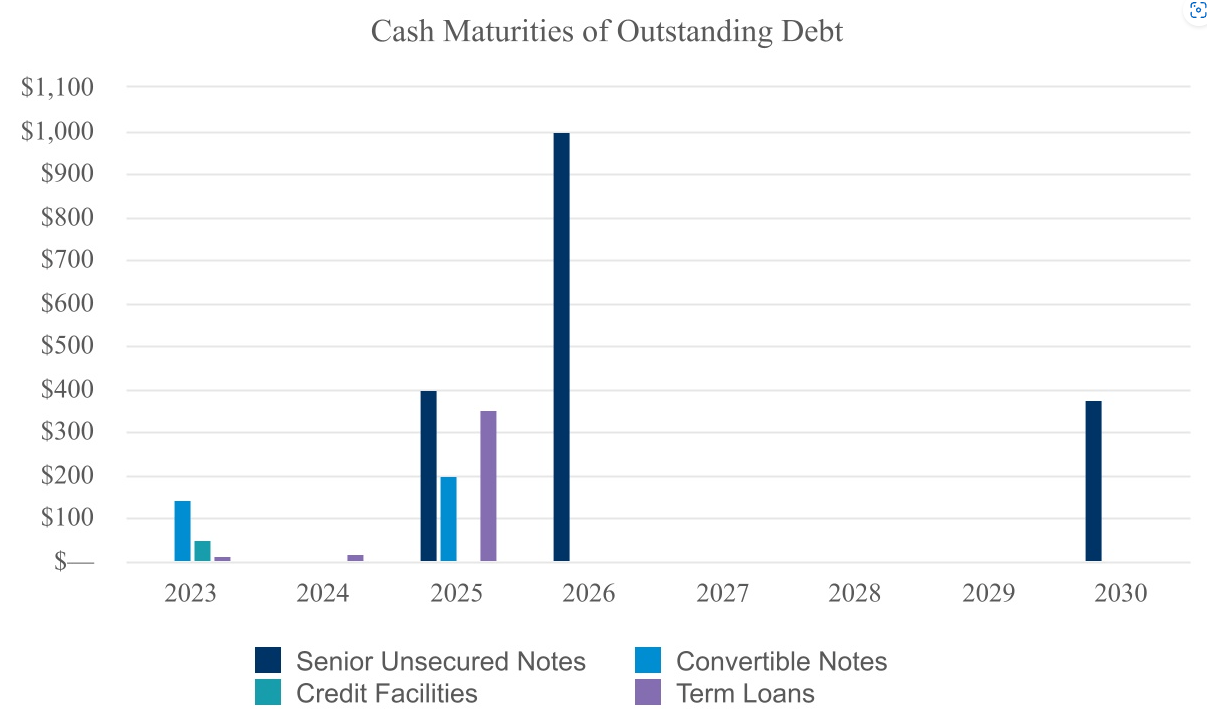

As of the end of 2022, about 17% of HASI's debt were project-level, non-recourse loans. Meanwhile, 13% of debt was in the form of convertible notes, and 70% of total debt was in the form of senior unsecured notes.

Aside from some convertible notes that will mature and become convertible into cash or common stock this year, HASI has very little debt maturing until 2025. This chart shows the maturity schedule for all debt except non-recourse loans):

{kind=link}

Meanwhile, the non-recourse loans have varying maturities going all the way out to 2047, but these are also amortizing loans, which means that the principal is steadily paid down over time in addition to interest.

Assuming distributable EPS of $2.28 this year, HASI's payout ratio currently sits at around 70%. That leaves plenty of room for further dividend growth in the coming years. Management's stated goal is for dividend growth of 5-8% annually.

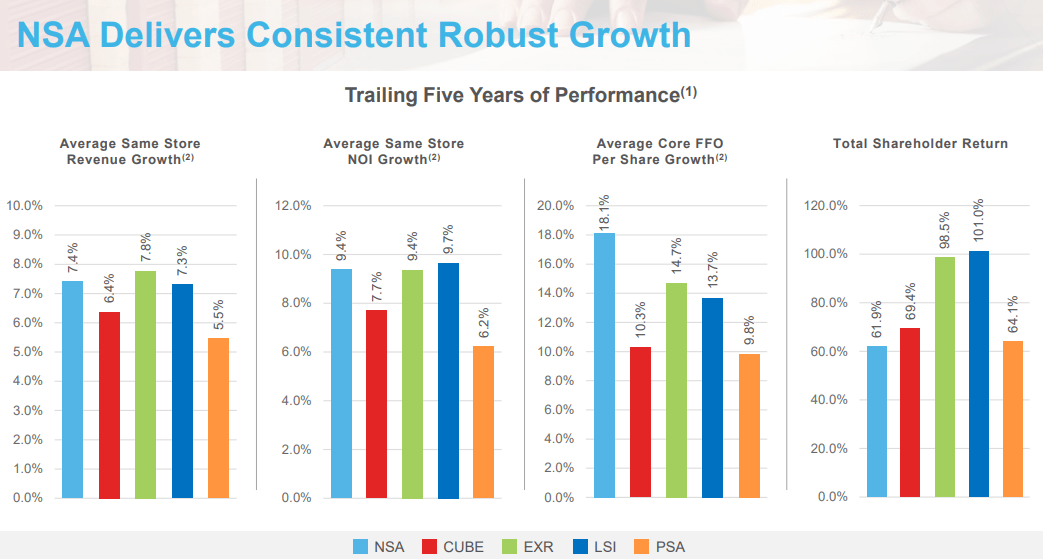

National Storage Affiliates ( NSA )

- Dividend Yield: 5.7%

Unlike other storage REITs like Public Storage ( PSA ) and Extra Space ( EXR ), NSA's model is to aggregate multiple storage brands under its holding company. In a fragmented industry with lots of private operators, NSA has plenty of acquisition opportunities, and it targets the highest quality privately owned storage properties among them.

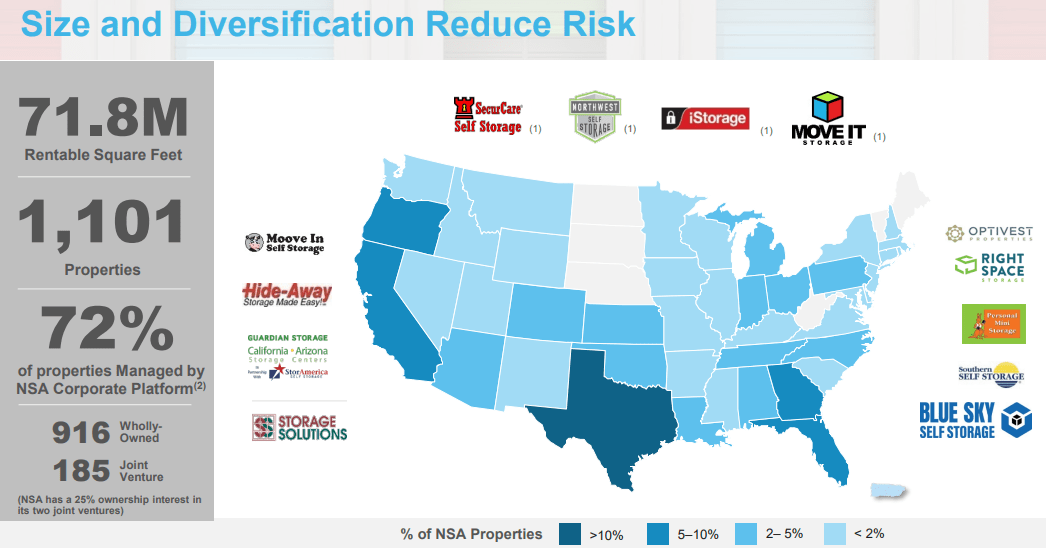

Sometimes these properties are sold on an individual or portfolio basis, and sometimes NSA acquires them with a Participating Regional Operator ("PRO") that basically act as joint venture partners. Of NSA's 1,101 properties, it wholly owns 916 of them and holds 185 in JVs, while 72% of its portfolio is managed internally with the rest managed by PROs.

{kind=link}

Around 2/3rds of the portfolio is located in the Sunbelt, with Texas being by far its largest state. And rather than compete with the likes of PSA and EXR in the top 20 markets of the US, the majority of NSA's properties are located in suburbs and secondary markets.

This storage facility aggregation strategy has worked well for NSA over time. Since inception in 2012, NSA has grown its portfolio more than 10 times over, going from 100 properties to ~1,100. And in the last five years, the REIT has posted some of the best fundamental performance in its peer group, and yet it has also had the worst stock price performance.

{kind=link}

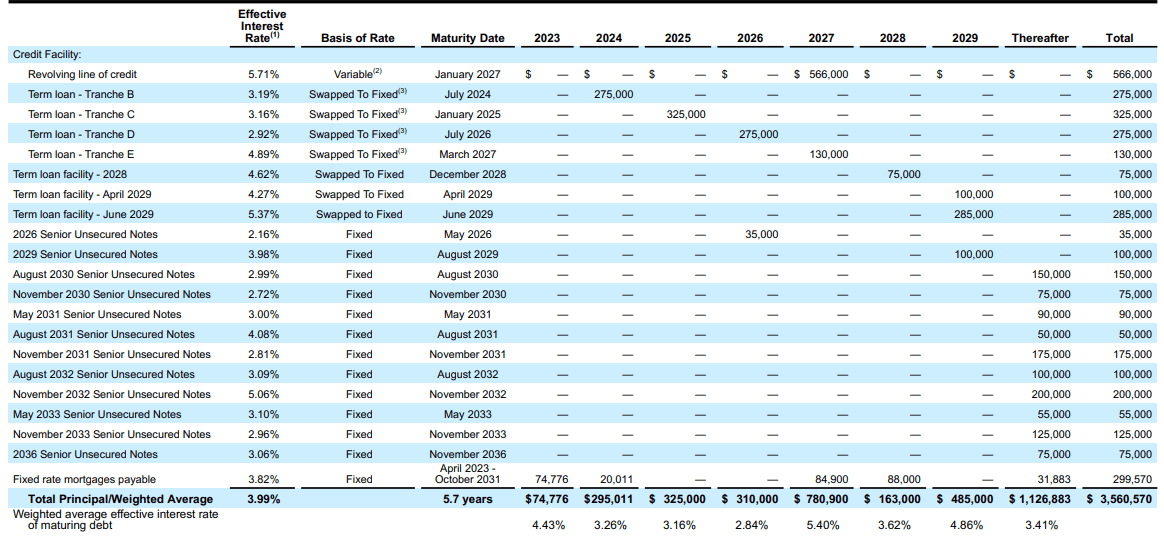

The market appears to worry about NSA's 17% of total debt with floating interest rates. But note that NSA's investment grade-rated balance sheet is reasonably well structured with net debt to EBITDA of 6.0x, interest coverage of 4.3x, a weighted average remaining maturity of 5.7 years, and (after a recent refinancing) very minimal debt maturing until mid-2024.

{kind=link}

Also, for what it's worth, NSA insiders purchased about $6 million of stock on the open market during Q4 2022 at prices ranging from about $37 to $39.

With a payout ratio edging toward the high side at 78% of core FFO, I wouldn't expect big dividend growth this year, but the prospects for mid-single-digit growth in 2024 and beyond look promising.

Urstadt Biddle Properties ( UBA , UBP )

- Dividend Yield: 5.8%

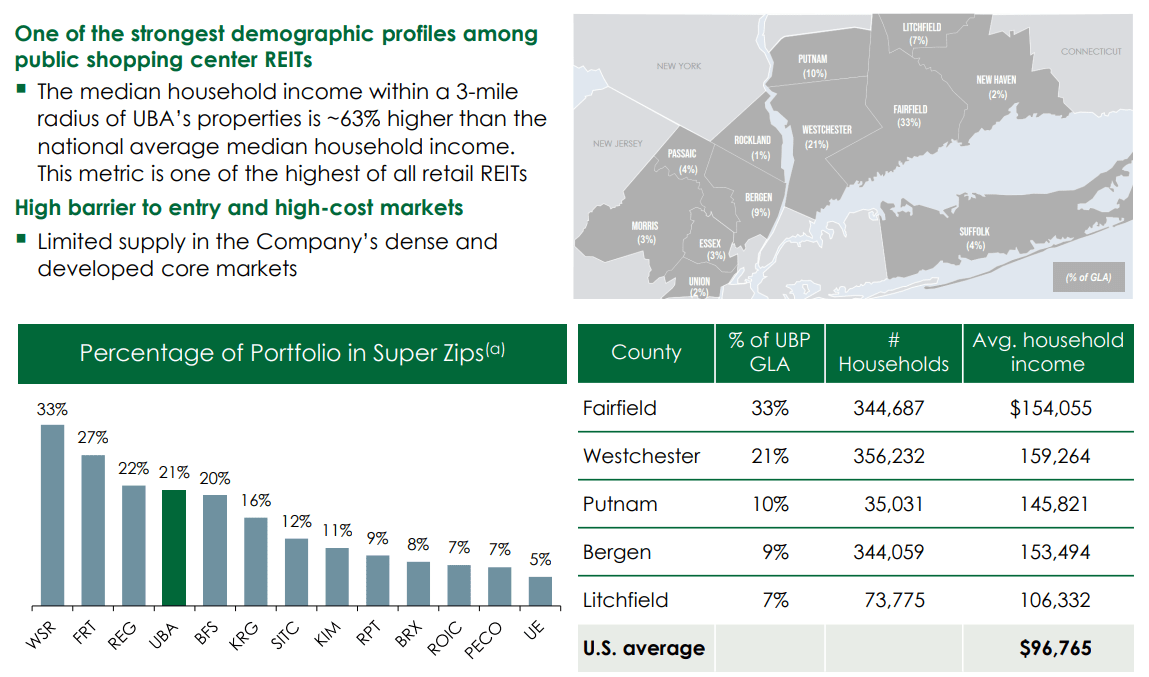

UBA owns a portfolio of 77 shopping centers in the New York tri-state area suburbs surrounding NYC, the vast majority of which are anchored by a grocery store, pharmacy, or wholesale club.

{kind=link}

These counties surrounding NYC enjoy some of the best demographic profiles in the nation, with high rates of education, income, and population density. Moreover, for a variety of reasons, almost no new retail space is being built in these markets.

The REIT may not have an investment grade credit rating (or any rating at all), but the balance sheet is actually in good shape. No debt is maturing in 2023 or 2024, and only 25% of total capitalization is in the form of debt. The rest of the capital structure is perpetual, either from preferred stocks with no required redemption date or common stock.

UBA 2022 Presentation

Recently, management has been using excess cash to buy back stock, which should steadily generate incremental FFO per share growth.

Finally, note that the company remains controlled by the founding family, who run it very conservatively. UBA may never be a fast-grower, but its dividend is safe and important to the Urstadt and Biddle families, who own about 20% of common equity.

W.P. Carey ( WPC )

- Dividend Yield: 5.9%

WPC is a globally diversified net lease REIT with a particular emphasis on industrial & warehouse real estate in the US and Europe as well as essential retail in Europe specifically. About 32% of the tenant base (by base rent) are investment grade-rated, although WPC typically invests heavily in tenants just below IG ratings or with implied IG profiles.

Slightly over half of the portfolio is in industrial or warehouse/distribution properties, but WPC also has exposure to office, retail, and self-storage.

WPC Q4 2022 Presentation

WPC's single-tenant net lease office properties are largely leased to critical government tenants or are corporate headquarters buildings. For example, for a 10-year period after the Great Recession, WPC owned the New York Times headquarters in NYC. The NYT did a sale-leaseback during the 2008-2009 recession when they needed cash, and they bought back the building as soon as they were contractually able to do so.

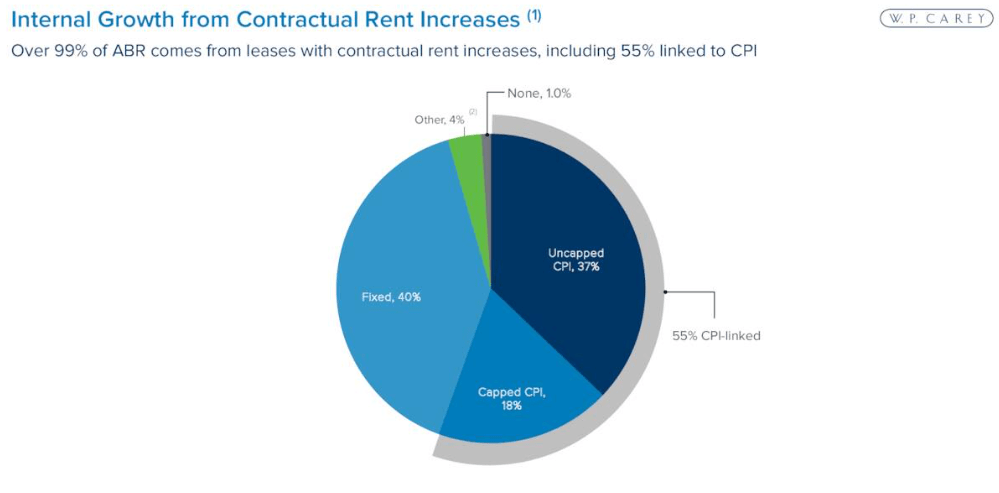

One of the most distinctive aspects of WPC's portfolio is its heavy emphasis on CPI-based rent escalations. At the end of 2022, 55% of rent enjoyed CPI-based rent bumps, split between 37% uncapped and 18% capped.

{kind=link}

Due to these attractive lease features, WPC's same-store rent growth reached as high as 3.4% year-over-year in the second half of 2022.

Finally, note that WPC took considerable measures to strengthen its balance sheet over the last several years, including earning a credit rating upgrade to BBB+, lowering its net debt to EBITDA ratio to 5.7x and its weighted average interest rate to 3.0%.

{kind=link}

WPC does have some debt maturing this year (5.4% of total debt) and next year (16.2%), but note that the REIT just issued a ~$550 million term loan denominated in euros at an effective interest rate of 4.34%. This should at least allow the REIT to pay off the remaining debt owed this year, and it does so without dramatically increasing WPC's interest costs.

The REIT has increased its dividend for 24 consecutive years, and later this year that record should extend to 25 years.

Bottom Line

Each of these five quality REITs traded at dividend yields significantly lower during the last bull market periods. And though higher interest rates are somewhat of a headwind for them, they are not in nearly as bad of shape as their stock prices would suggest.

Some REITs are in trouble during the current high interest rate environment, but these five are not among them, in my estimation.

Their dividend yields are attractive, and their real estate assets should generate a moderate amount of growth as well. I rate them each as "buy-and-hold-and-enjoy-the-dividends."

For further details see:

5 Quality REITs Yielding Over 5%