DB - 5 Reasons Deutsche Bank Should Be In Your Portfolio Of Bank Stocks

2023-06-04 02:21:05 ET

Summary

- Deutsche Bank is considered a strong buy based on its undervalued P/B ratio, healthy capital position, competitive dividend yield, diversified revenue stream, and bearish price trend.

- The bank's risks, such as exposure to commercial real estate loans and deposit outflows, are mitigated by its conservative risk management approach.

- DB could be a great addition to a financial-sector stock portfolio, providing exposure to European banks.

Summary.

My stock pick today is Deutsche Bank ( DB ), a global financial powerhouse with company roots in Germany and a strong US presence. In fact, its stock is listed on the NYSE, unlike many other large banks based in Europe, who often trade in the US markets through an ADR or through the OTC markets.

Much like the precision engineering of certain European import cars, I am using a systematic approach to analyzing this stock, based on a 5-step process I already wrote about in recent articles.

To rate this stock, I ask the following key questions, and each "yes" answer scores one point. A total score of 5 would make this stock a strong buy, for example, while a score of 0 or 1 would make it a sell. A score of 3 would be a "hold."

- Does the stock seem undervalued based on its P/B ratio?

- Do they have a healthy capital position?

- Is this stock's dividend yield competitive among firms in the same sector?

- Does the firm have a diversified revenue stream across several business segments?

- Does the price chart indicate a buying opportunity right now?

With evidence below, I will show that this stock is currently a Strong Buy opportunity.

Although not an owner at the moment, I have personally traded this stock in the past during the dip buying opportunity this past March, as part of a larger portfolio strategy to own some exposure in banks headquartered in Europe.

So, here are 5 reasons an investor could consider adding Deutsche Bank to their portfolio of financial-sector stocks.

A P/B Ratio that Shows this Stock as Undervalued.

This stock is showing as undervalued, based on the P/B Ratio found on Seeking Alpha:

Deutsche Bank - P/B Ratio (Seeking Alpha)

In fact, its trailing twelve-month Price to Book ratio scored an impressive A+ rating from Seeking Alpha!

Not only that but this stock's P/B Ratio is 72% lower than its sector median ratio of 0.98. In comparison to peers, UBS ( UBS ) has a P/B Ratio of 1.05 , while Goldman Sachs ( GS ) is around 1.04.

The answer to whether it is undervalued is therefore a Yes .

My sentiment was echoed as early as February by another Seeking Alpha analyst, Labutes IR , whose analysis reiterated that "Deutsche Bank is one of the cheapest banks within the European banking sector."

A Global Firm Anchored by a Strong Capital Position.

When it comes to systematically critical banks on a global scale like Deutsche Bank, I will next take a look at their capital ratios, to see if it is adequately prepared to weather financial shocks without facing solvency issues.

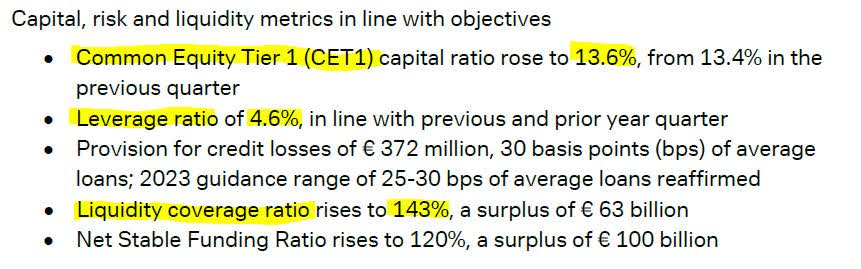

The following is from their Q1 release:

Deutsche Bank - Q1 2023 results - capital ratios (Deutsche Bank)

{kind=link}

This tells me that they are a Yes when it comes to being in a healthy capital position.

With a CET1 of 13.6%, LCR of 143%, and leverage ratio of 4.6%, it is not in any trouble when it comes to both regulatory requirements and its own capital goals and being well above the Basel III requirement of 4.5% for CET1.

A Competitive Dividend Yield among its Sector.

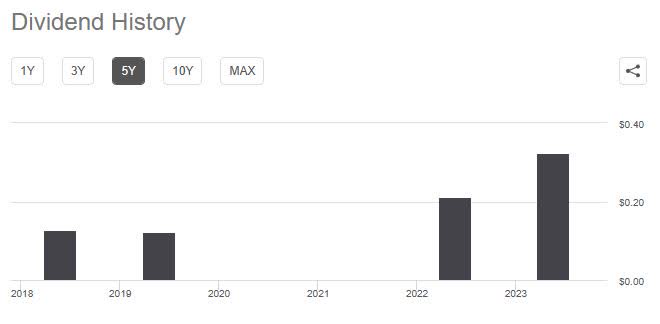

Based on dividend info from Seeking Alpha , this stock does not pay a regular quarterly dividend, although it recently declared an annual dividend payable last month, at $0.32 a share. So, if you did not own the stock by the ex-date, you missed out on this dividend. However, there is always next year.

As the chart below shows, no annual dividends were paid in 2020 or 2021, however the firm came back to paying dividends in 2022 and grew them coming into 2023.

{kind=link}

Based on the June 6 closing price of $10.60 a share, the dividend yield comes out to just over 3%. I think this is competitive amongst its peers since it beats the current yield for UBS ( UBS ) of 1.41%, comes close to the 3.59% yield at Bank of New York Mellon ( BK ), and close to Goldman Sachs ( GS ) yield of 3.16% . I picked those three stocks for comparison purposes due to their size, status as global systemically critical banks, and having some similar business segments to Deutsche.

Second, from a forward looking perspective I see a renewed commitment by management to return capital back to shareholders, which is important to me as an investor.

This was reiterated in their March news release , with the firm focusing on a longer-term plan of returning capital back to stockholders, commenting on their recent dividend hike:

This corresponds to an increase of 50 percent and is in line with the ambition to distribute around 8 billion euros of capital to shareholders for the financial years 2021 to 2025. From 2025 onwards, the Management Board aims to distribute a total of 50 percent of the net profit attributable to shareholders.

Based on the evidence, the answer to whether their dividend is competitive among firms in the same sector, is an obvious Yes .

However, for investors in financial-sector stocks, it also shows that adding so-called European banks to a portfolio going forward could provide diversification to a dividend-income investor who already trades bank stocks. As I have written in the past, I like stocks that pay a regular dividend if I have to hold them longer during market dips, and it appears the large banks have the adequate cash needed to distribute some back to stockholders.

My point of view was also supported in an April 2023 article in the Financial Times by the founder & CEO of Algebris Investments :

Capital return has become a hugely attractive component of the investment case for European banks. After years of building up capital ratios from extremely low levels, banks sit on mountains of excess capital and regulators are waving through significant returns of capital to shareholders.

A Diversified Portfolio of Revenue Streams.

The next thing that interests me is how diversified is this firm's revenue streams, so they are not overly dependent on one segment.

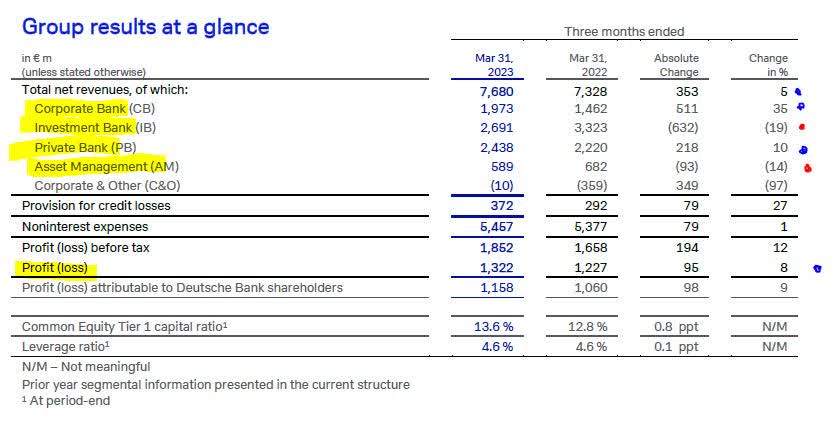

From the most recent Q1 2023 quarterly results , as reported back on April 27, besides mentioning that their profitability saw its best quarter since 2013, we can also see how they performed by business segment.

Briefly, the corporate bank segment saw top-line growth of 35% YoY, the investment bank was down 19%, the private bank up 10%, while asset management was lower 14% YoY.

One cannot ignore the effect of rising interest rates in this case either, as the bank's release mentions growth of 71% NII in the corporate bank while the private bank was also "driven by strong net interest income."

Here is a breakdown by segment:

Deutsche Bank - Q1 2023 results - by segment (Deutsche Bank)

{kind=link}

Based on this, the answer to whether the firm is diversified enough in its revenue across multiple business segments is a Yes .

But how does this factor into a forward-looking strategy for the rest of 2023?

For that, I think the fact that the May 2023 interest rate hikes by both the Fed and the European Central Bank will continue to benefit this bank for the next few quarters, in those segments that benefit from NII.

But also, their management's own forward-looking positivity tells me of their confidence in the coming year.

In the Q1 results commentary, CEO Christian Sewing set the kind of tone I am looking for from the leadership team:

We aim to accelerate execution of our strategy through a number of measures announced today: raising our ambitions for operational efficiency, boosting capital efficiency to drive returns and support shareholder distributions, and seizing opportunities to outperform on our revenue growth targets. Strong organic capital generation enables us to re-affirm our commitment to distributions and we are preparing to conduct further share buybacks later this year.

A Price Chart showing a Buying Opportunity.

When looking at this stock's closing price chart on Friday June 2, I see a potential buying opportunity echoed by the death cross signal in the chart below, circled in red, indicating a bearish trend:

Deutsche Bank - price chart on June 2 (StreetSmart Edge trading platform)

{kind=link}

The above is a 2-year chart showing the 50 day simple moving average (dark blue line) overlaid with the 200-day simple moving average (dark red line).

If using this trading strategy of buying during a death cross and selling during a golden cross, one can take advantage of bearish and bullish trends.

However, this alone should not be part of a long-term strategy, but one component of it. This is because, as the chart shows, it is not certain how long a bearish period will last after a death cross occurs. The last one went from April 2022 all the way to December 2022, for example.

If an investor had bought at the April 2022 price drop, and held until February 2023, they would have achieved a capital gain, as the chart shows.

The answer to whether it is currently approaching buying range again, is a Yes , as the chart trend shows an investor may be able to snatch up some shares at the low to mid-$10 range if it remains there in the coming week, and holding those shares until they get past $12 again at least, perhaps after another golden cross formation.

In an article for Nasdaq and StockMarket.com , author Brandon Michael supported my viewpoint as well when it comes to use of golden crosses:

When used correctly, it can provide valuable insight into potential market movements. As well as help you make better trading decisions by providing accurate information about where stocks might be moving next.

However, it’s important to remember that you should never rely on one single indicator exclusively. Instead, use multiple tools together.

Risks to my Outlook.

The risks to my bullish outlook for this firm could come from two areas that usually affect the banking segment: a bank's risk exposure to loans going bad as well as exposure to deposits that clients suddenly decide to pull out.

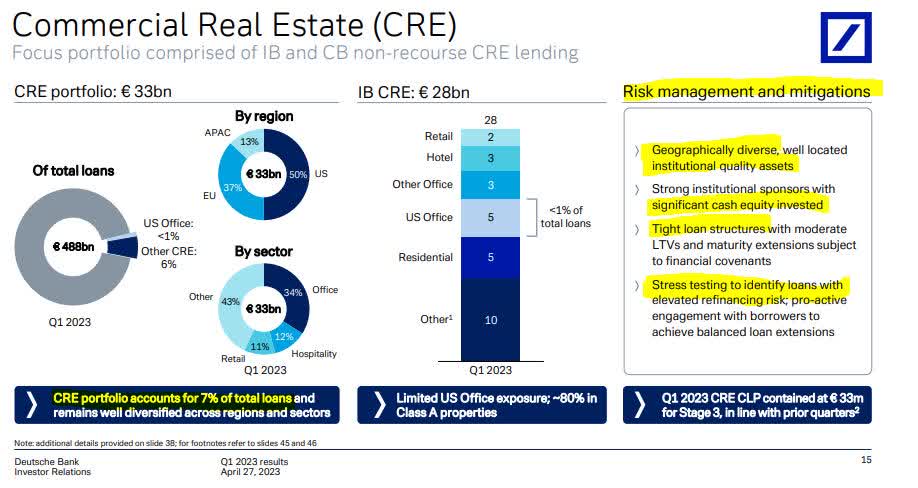

First, let's look at this firm's exposure to commercial real estate:

Deutsche Bank - Q1 2023 results - Commercial Real Estate Exposure (Deutsche Bank)

{kind=link}

It appears this bank has taken steps to diversify its exposure to commercial real estate risk across several global regions, and property categories, along with use of stress testing.

I am keeping an eye on this type of risk because the issue was highlighted in a recent May 10 article by Investopedia, discussing the Fed's recent Financial Stability Report:

Commercial real estate poses a risk to U.S. banks, particularly smaller, regional lenders that are most exposed to the sector, according to the Federal Reserve in its latest Financial Stability Report.

Loans on office properties are disproportionately issued by the smallest lenders, which have greater exposure to the sector than big banks and mid-sized regional lenders.

The other side of the balance sheet is the deposit side. Now, here is what their deposit base looks like:

Deutsche Bank - Q1 2023 results - Deposit Base (Deutsche Bank)

As you can see, their client funds are across a diversified portfolio but also a large amount of deposits are in their base country of Germany with the majority being insured.

Deutsche Bank is not anywhere near the same situation as Silicon Valley Bank so it would be an apples to oranges comparison. Deutsche is not exposed to that level of uninsured deposits who could potentially cause a bank run. But rather, as its Q1 presentation shows, it has a well-diversified deposit base.

The culprit of uninsured deposits was echoed by a March 17 article in the Harvard Business Review :

At the heart of Silicon Valley Bank’s failure are uninsured depositors — specifically startup companies who held far more than the insured limit of $250,000 and who couldn’t make payroll without access to their accounts.

Therefore, my view is that the two key risks of commercial real estate exposure and exposure to uninsured deposits are offset by this bank's own risk mitigation strategy and diversification.

Conclusion.

In conclusion, this stock scores a 5 on my analysis and is therefore a strong buy.

This is based on the evidence provided showing a good score for dividend yield, capital ratios, revenue diversification, current price trend, and P/B ratio.

This rating is offset by the risk of the firm's exposure to commercial real estate loans as well as risk of deposit outflows, two risks being mitigated by the firm's conservative risk management approach, as highlighted in their own quarterly presentation and commentary.

For someone new to financial stocks, or wanting to add to your existing portfolio, Deutsche Bank at its current price point could be a great addition to the portfolio and a way to own the European banks.

For further details see:

5 Reasons Deutsche Bank Should Be In Your Portfolio Of Bank Stocks