REG - 5 REITs For The 'Old Geezer'

2023-05-27 07:00:00 ET

Summary

- Time horizon constitutes one of the most influential variables in structuring portfolios.

- I encourage readers of all ages to spread capital across multiple asset classes.

- We hand-picked all 5 of these REITs because we believe they will provide investors with predictable and durable dividends in any environment.

This article was published at iREIT on Alpha on Friday May 26, 2023.

Last week, I wrote an article titled, "If I Were Starting Over In My 20's I Would Buy These REITs." It was dedicated to our interns at iREIT on Alpha, who are all in their early 20's.

As you know, there are different risk profiles for investors and time horizon constitutes one of the most influential variables in structuring portfolios .

Regardless of age, however, I always stress the importance of diversification, because one of the lessons that I learned at an early age is that overconfidence can contribute to a series of investors issues.

I encourage readers of all ages to spread capital across multiple asset classes , and as much as I love real estate investment trusts, or REITs, I would not put all of your eggs in one basket.

After publishing the above-referenced article, several retired readers asked me to pen an article with a few REITs for them. One reader even called himself an "old geezer," which I suppose puts me in the same age category since I'm now the proud grandfather of a one-year-old ("Asher").

Old Geezer : a cranky old man and can carry the connotation of either age or eccentricity. Wikipedia.

As I'll remind you, when researching a company, we look for earnings growth, profitability, dividend growth, dividend consistency, dividend yield, and the strength of the company's balance sheet.

For people that are retired or close to being retired, I think the most important metric to look at is safety, or the strength of the company's balance sheet, followed by earnings consistency, dividend consistency, and lastly the dividend yield.

This is not to say that profitability and growth don't matter, because they do, but the aspects that I think are the most important for retirees is the long-term solvency of the company, the amount the company pays you, and the track record of those payments.

What we are not looking for a REIT with a large amount of debt relative to its assets or earnings, or a REIT that has a history of suspending or cutting the dividend.

We also don't want to pick a REIT that has a low dividend yield even if it has a strong dividend growth rate. For someone in their 20's I would encourage them to investigate REITs that have moderate yields but high growth rates. But for retirees I think dependable current income trumps growth.

Now to be perfectly honest, several of the REITs we listed in the article referenced above could be on this list as well since. These include Mid-America Apartment Communities, Inc. ( MAA ) or Alexandria Real Estate Equities, Inc. ( ARE ), since they both have excellent balance sheet metrics and both yield around 4%.

Some REITs are just good to own regardless of your age, and as a matter of fact there is one REIT in last week's article that is also included here (can you guess who?)

Realty Income Corporation (O): Yielding 5.2%

Realty Income Corporation is maybe the best example of the perfect REIT at any age level, but especially for a retiree. They check all the boxes with a strong balance sheet , very consistent earnings and distributions, and a high dividend yield . Realty Income has been around since 1969, when they started out with a single Taco Bell.

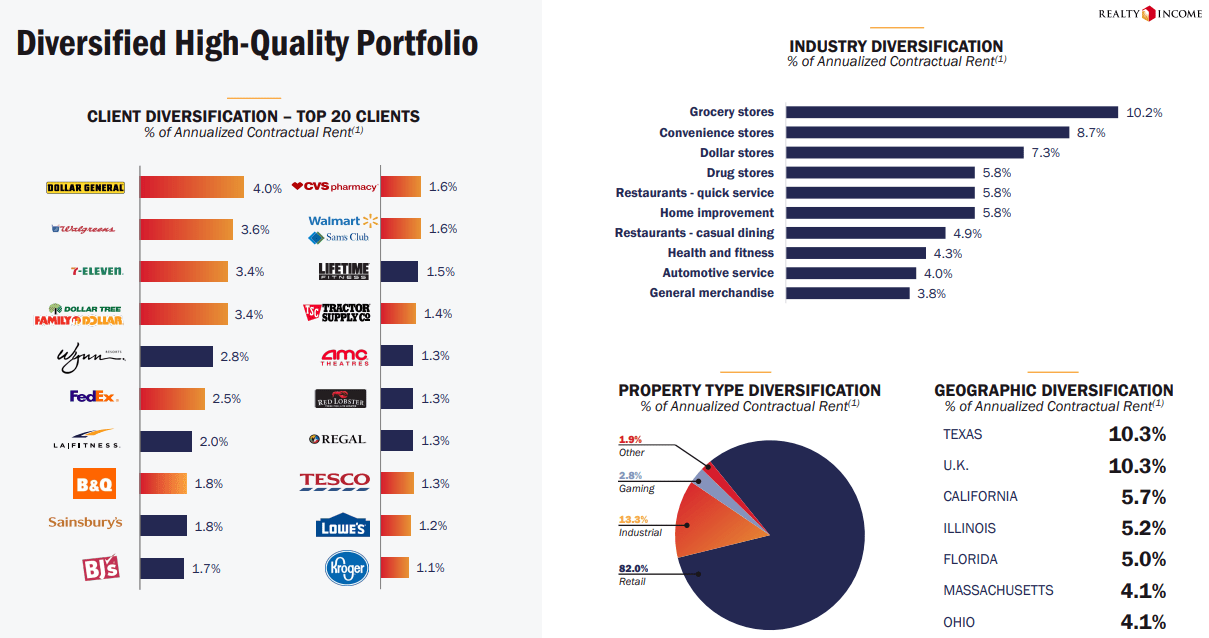

They went public in 1994 and have been one of the most reliable companies ever since. Realty Income is a triple-net-lease REIT that mainly owns retail properties, but also holds non-retail properties in their portfolio such as industrial and gaming.

Their earnings are nothing if not consistent, which is in large part due to the number of properties they own and the diversity and number of tenants they serve. As shown below, 82% of Realty Income's portfolio is made up of retail properties, 13% are industrial, and 2.8% are gaming properties.

{kind=link}

Realty Income has a diverse set of tenants that operate in industries that are e-commerce resistant like dollar stores, convenience stores, grocery stores and pharmacies. In total their portfolio contains 12,492 properties that encompass approximately 246.7 million square feet of leasable space.

Their properties are leased to 1,259 tenants, spread across 84 industries, have an occupancy rate of 99.0%, a weighted average remaining lease term of around 9.4 years, and are located in all 50 U.S. States, the U.K., Spain, Puerto Rico, and Spain.

You want to talk about earnings consistently? Based on their adjusted funds from operations ("AFFO"), Realty Income has had positive earnings per share growth in 26 out of the last 27 years.

They have delivered a 14.6% compound annual total return with half the volatility of the market since their public listing. They don't have the fastest earnings growth rate, but they have a solid 5% median AFFO growth rate per share since 1996.

{kind=link}

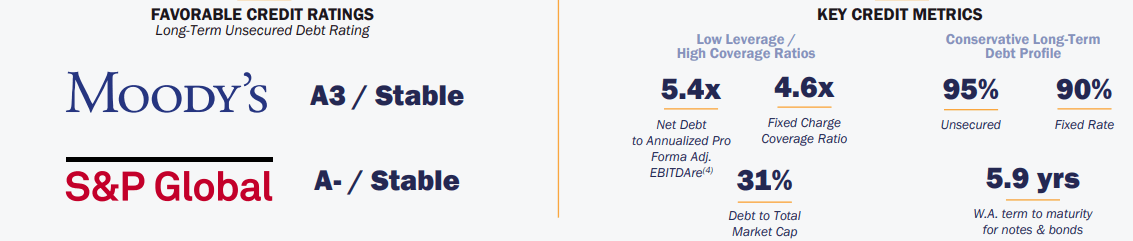

Realty Income is investment-grade with an A3 credit rating from Moody's. They have excellent debt metrics, including a net debt to pro forma adjusted EBITDAre of 5.4x, a fixed charge coverage ratio of 4.6x, a long-term debt to capital ratio of 41.21%, and a debt to total market capitalization of 31%.

Their debt is 95% unsecured, 90% fixed rate, and they have a weighted average term to maturity of 5.9 years. Realty Income has minimal maturities due in 2023 and as of March 31, they had $3.1 billion of liquidity that excludes unsettled forward equity of roughly $1.5 billion and $1.0 billion from their bond offering that closed in April.

{kind=link}

One of the things Realty Income is best known for is their dividend which is paid monthly. Realty Income is one of the few REITs that are a Dividend Aristocrat - it has a superb dividend track record.

They have increased their dividend for 29 consecutive years, declared 634 monthly dividends, and have increased their dividend for 102 consecutive quarters.

Since 1994 they have delivered a 4.4% compound annual dividend growth rate. On top of that they pay a 5.18% dividend yield that is well covered with an AFFO payout ratio of 75.69%.

Realty Income - Investor Relations

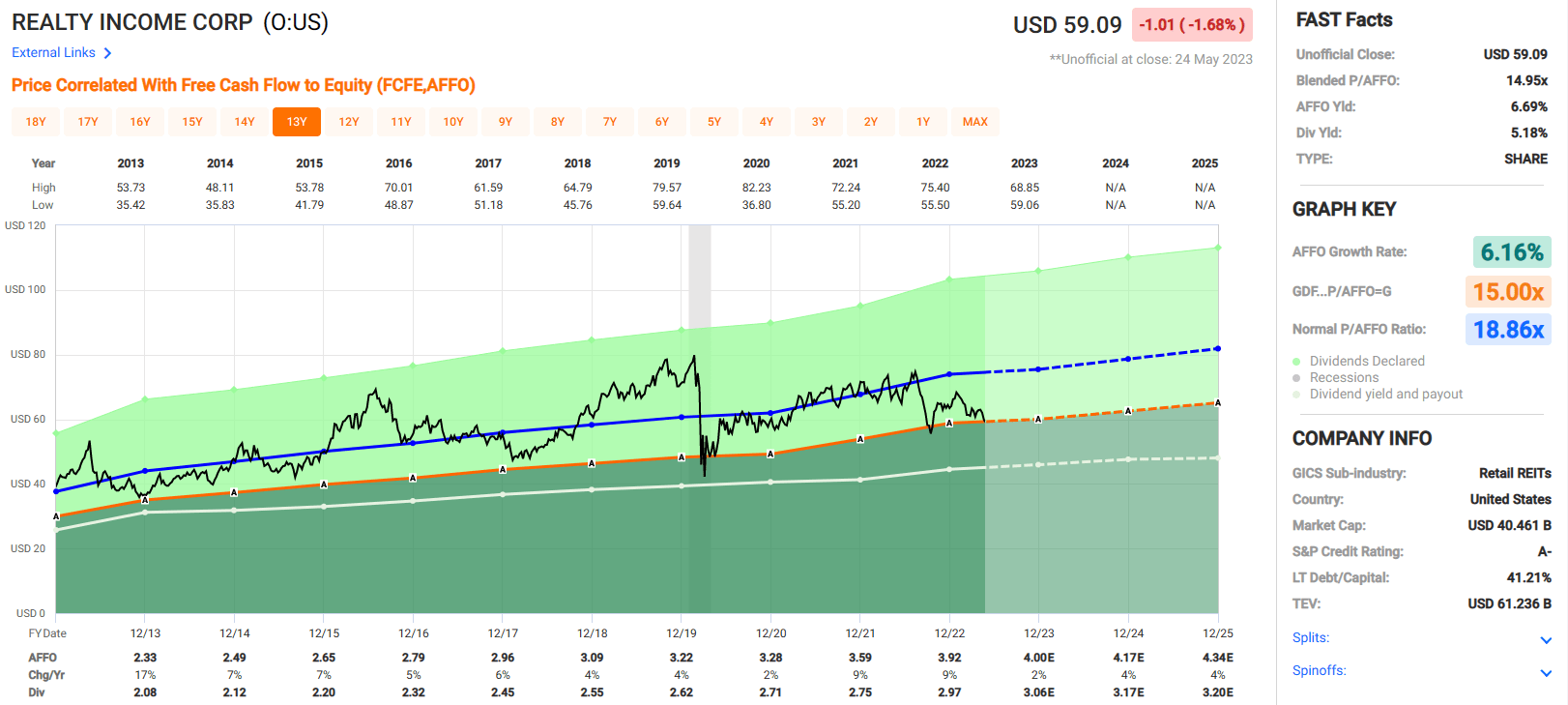

As I mentioned before, Realty Income is a good holding no matter what your age, but for retirees it is especially suitable since it is one of the most reliable REITs and has one of the best track records in the industry. They are currently trading at a P/AFFO of 14.95x, which is significantly below their normal P/AFFO multiple of 18.86x.

At iREIT, we rate Realty Income a BUY.

{kind=link}

Camden Property Trust (CPT): Yielding 3.9%

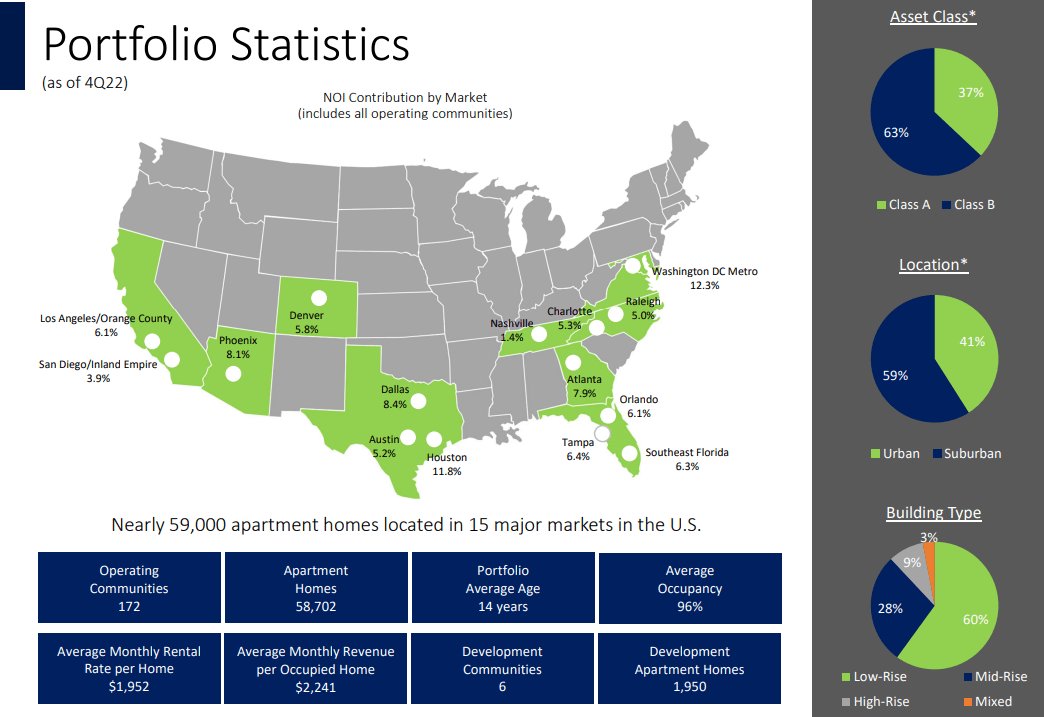

Another company to consider is Camden Property Trust , which is an apartment REIT. Tenant diversity is a given with apartment REITs but they can vary in terms of their core markets, property types (class A / class B) and occupancy rates. To make sure we have consistent earnings, we want to look at the number properties and units, occupancy rate, and the location of their properties.

As shown below, most of CPT's properties are located in the sun belt, which should be an advantage for them given the ongoing migration trend. Their largest market is in Washington D.C. which makes up 12.3% of their net operating income ("NOI"), followed by Houston and Dallas which makes up 11.8% and 8.4% of their NOI respectively. CPT's portfolio consists of 172 multifamily properties that contain 58,702 apartment homes with an average occupancy rate of 96.0%.

{kind=link}

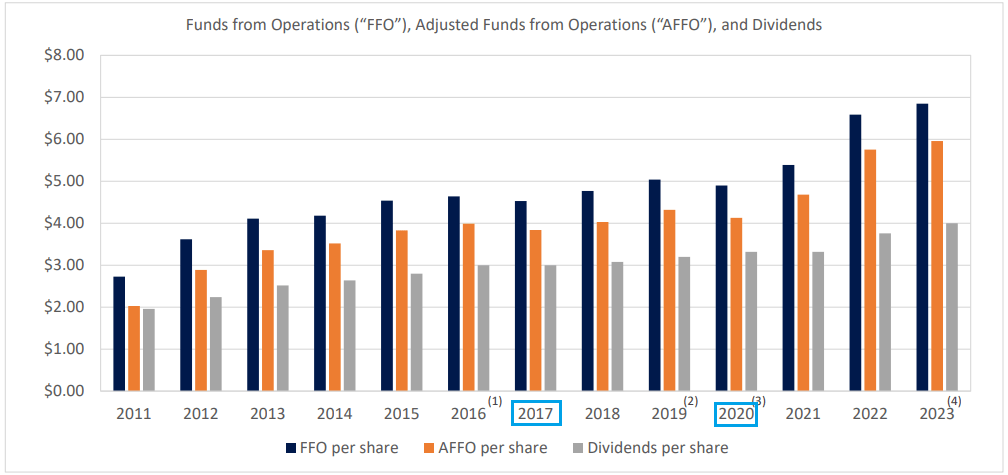

Camden Property Trust has had consistent AFFO growth since 2011, with the exception of 2017 and 2020 when AFFO declined by 4% each year. While CPT's earnings are not as consistent as Realty Income, they have grown AFFO per share in 10 out of the last 12 years.

Overall, they have an average AFFO growth rate of 5.76% and have either increased or maintained the dividend in each year since 2011. They increased the dividend in each year except for 2017 and 2021 (when the dividend was maintained but not raised). The chart below excludes a special dividend of $4.25 that was paid in 2016.

{kind=link}

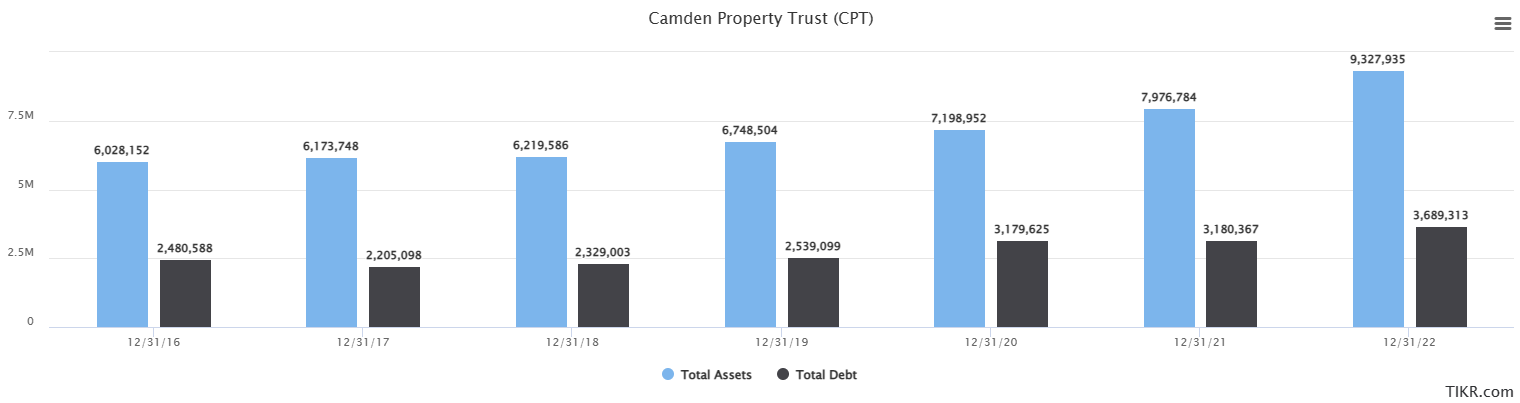

CPT is investment-grade with a credit rating of A- by S&P Global and has excellent debt metrics. Their total debt-to-total assets ratio comes in at 39.55%, they have a net debt to adjusted EBITDA of 4.1x, an interest expense coverage ratio of approximately 6.7x, and a long-term debt to capital of 40.32%.

CPT's debt is 86.3% unsecured, 82.6% fixed rate and has a weighted average interest rate of 4.1% and a weighted average term to maturity of 6.2 years. Additionally, they have $1.1 billion available to them under their credit facility.

{kind=link}

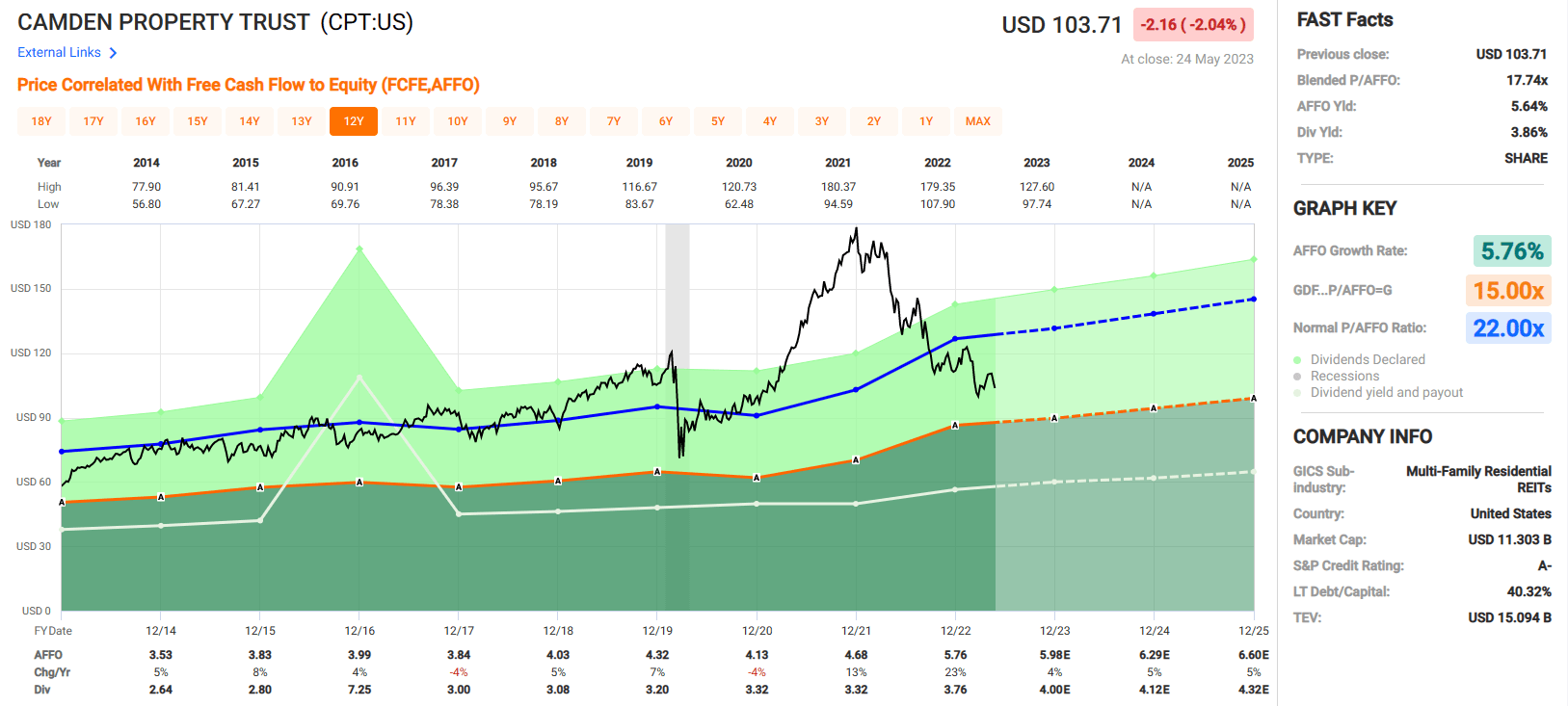

Camden Property Trust pays a 3.86% dividend yield that is very secure with an AFFO payout ratio of 65.28%. CPT has a fortress balance sheet and with just a few exceptions they have consistently delivered earnings and dividend growth. Apartments are one of my favorite REIT sectors in today's environment given the elevated level of interest rates.

One of the largest threats to apartment demand is oversupply and tenants that leave to purchase a house. While higher interest rates hurt CPT's cost of capital, it also reduces construction and makes mortgaging a house prohibitively expensive for many residents. Currently, CPT is priced at a P/AFFO multiple of 17.74x which is well under their normal AFFO multiple of 22.00x.

At iREIT, we rate Camden Property Trust a BUY.

{kind=link}

STAG Industrial, Inc. (STAG): Yielding 4.3%

The next selection for retirees is Stag Industrial, Inc. , which is in the industrial sector. STAG has a different investment approach when compared to many other industrial REITs, in that they don't target primary markets with a high barrier to entry that many other REITs and institutional investors focus on. Instead, they focus more on middle market industrial properties that don't get the same amount of attention from larger REITs or institutional investors.

STAG implements this strategy so that they can compete with local investors in fragmented markets where they believe they have competitive advantage due to their access to the capital markets. STAG's portfolio consists of 561 industrial properties that cover 111.6 million square feet and are located in 41 States.

{kind=link}

STAG is well diversified by tenant, with their top tenant (Amazon) only contributing 2.8% of their annualized base rent ("ABR"). No other tenant contributes over 1%, and their top 10 tenants combined only contribute 9.9% of their annualized rental revenue.

STAG - Investor Relations

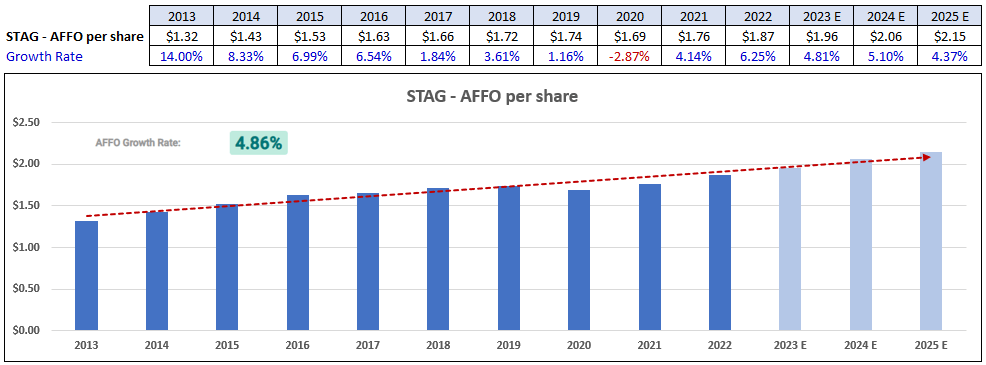

STAG has consistently delivered AFFO per share growth with AFFO growth in 9 of the last 10 years. Overall they have an average AFFO growth rate of 4.86%, which is not the fastest growth rate but it is solid. Analysts expect AFFO growth of approximately 5% in both 2023 and 2024.

{kind=link}

STAG is investment-grade with a Baa3 credit rating from Moody's and a BBB credit rating from Fitch. They have strong debt metrics with a net debt to adjusted EBITDAre of 5.0x, a fixed charge coverage ratio of 5.6x, and a long-term debt to capital of 39.49%.

{kind=link}

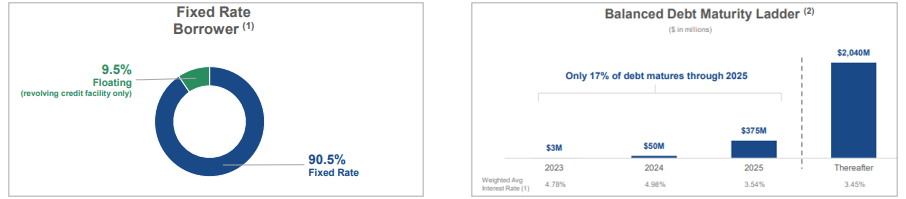

STAG's debt is 90.5% fixed rate and has a weighted average interest rate of 3.49%. They have $778.9 million in liquidity with minimal maturities in 2023 and only 17% of their debt matures through 2025.

{kind=link}

STAG pays a dividend yield of 4.36% that is well covered with an AFFO payout ratio of 78.08%. There are a lot of attractive industrial REITs, but I picked STAG for retirees due to the high current yield, which is one of the highest in the industrial sector, and because it pays monthly dividends.

While a REITs dividend schedule should never be the primary driver in making an investment decision, it does add an extra element for retirees, as the monthly income can match monthly expenses which may make it easier to plan around.

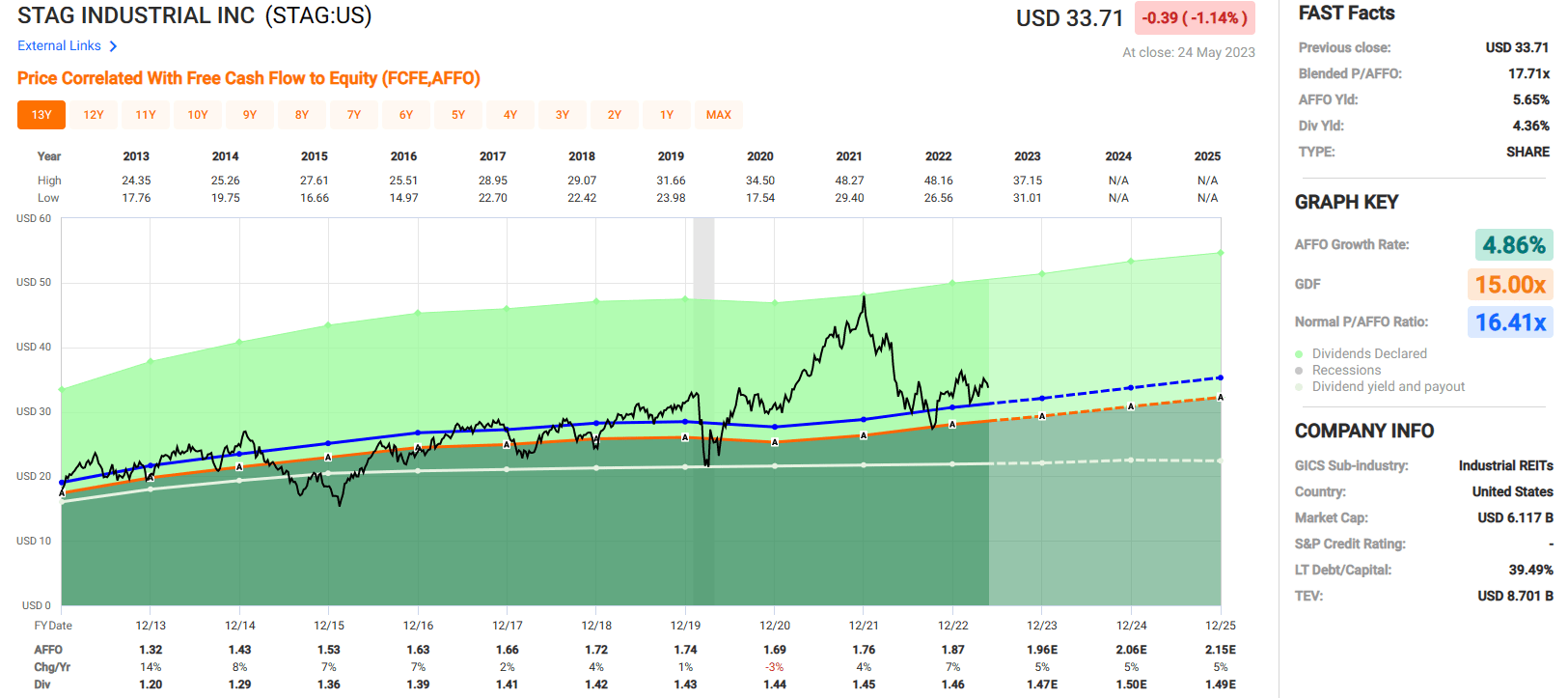

Currently STAG trades at a P/AFFO of 17.71x, which is a bit higher than their normal AFFO multiple of 16.41x, but is much lower than the average industrial REIT.

At iREIT, we rate STAG a BUY.

{kind=link}

Regency Centers Corporation (REG): Yielding 4.7%

While I've been focusing on bottom-up analysis to select today's picks, I also wanted to pick REITs in different sectors in order to add diversify. Like Realty Income, Regency Centers Corporation primarily owns retail properties, but unlike Realty Income, they specialize in in shopping centers anchored by a grocery store rather than single-tenant, freestanding properties.

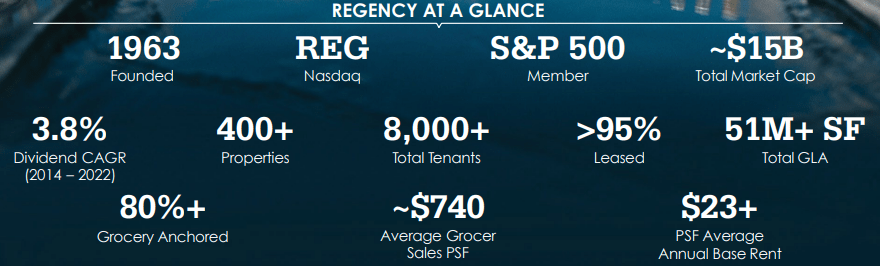

Regency Centers is a shopping center REIT that has over 400 properties, of which over 80% are anchored by a grocery store. Their properties cover 51 million square feet of gross leasable area ("GLA"), serve over 8,000 tenants, and are approximately 95% leased.

{kind=link}

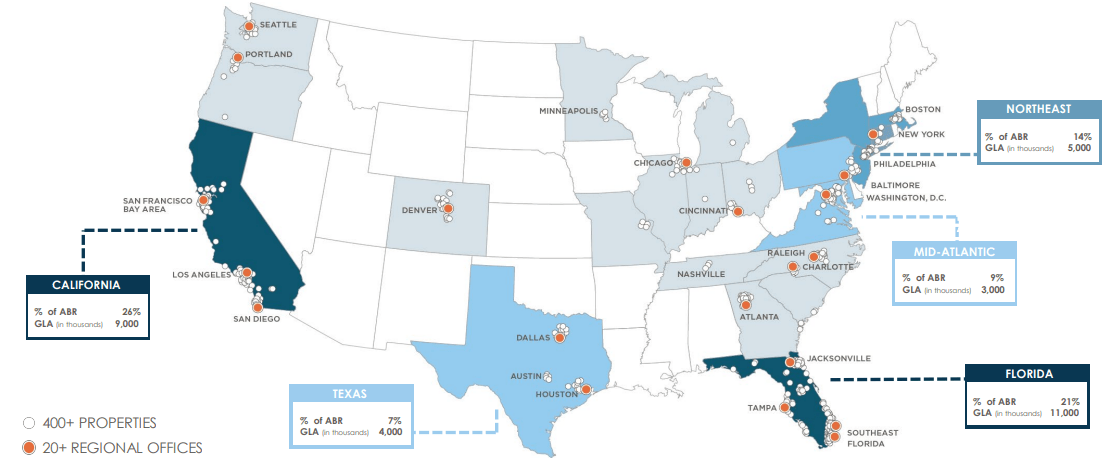

Regency Centers has properties spread across the U.S. with the majority of their properties located in the Northeast and the Mid-Atlantic regions of the country as well as Florida, Texas, and California. Measured by ABR, California contributes the most at 26%, followed by Florida at 21% of their ABR.

{kind=link}

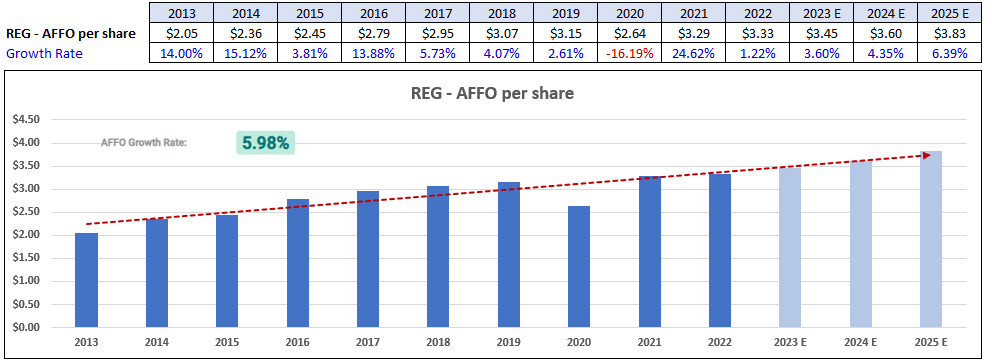

REG has consistently delivered AFFO growth over the past decade except for in 2020 during the pandemic. On the whole, REG has had an average AFFO growth rate of 5.98% since 2013. Analysts expect continued growth with projected AFFO growth rates at 3.6%, 4.35%, and 6.39% in the years 2023, 2024, and 2025 respectively.

{kind=link}

Regency Centers is investment-grade with a BBB+ credit rating from S&P Global. REG has strong debt metrics with a net debt to operating EBITDAre of 4.9x, a fixed charge coverage ratio of 4.7x, and a long-term debt to capital of 41.15%.

Their consolidated debt is approximately 95.66% fixed rate and has a weighted average interest rate of 3.9% and a weighted average term to maturity of 8.1 years. REG has minimal maturities in 2023 and total liquidity of $1.2 billion.

{kind=link}

Regency recently announced an all-stock merger with Urstadt Biddle Properties Inc. (UBP) valued at ~$1.4B, implying an attractive 7.2% cap rate. UBP owns high-quality, grocery-anchored centers in the supply-constrained NY tri-state area with similar demographics to REG.

The deal is expected to be immediately accretive driven by G&A synergies with further leasing upside and increased geographic diversification. REG leverage remains low (5.2x).

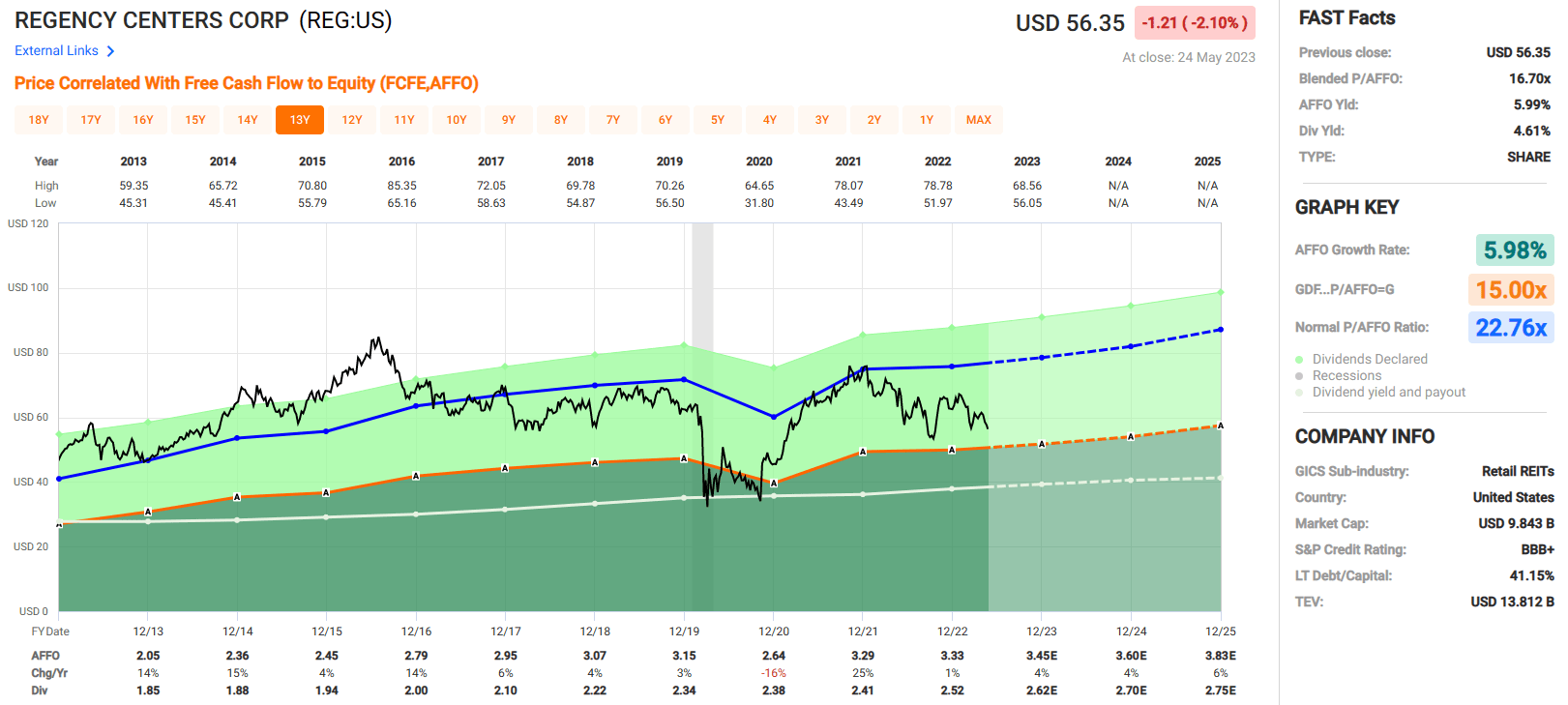

Regency Centers pays a 4.61% dividend yield that is well covered with an AFFO payout ratio of 75.87%. REG has increased their dividend each year since 2013 and has an average dividend growth rate of 3.18% over that time period. Currently REG is trading at a P/AFFO multiple of 16.7x, which is a significant discount to their normal AFFO multiple of 22.76x.

At iREIT, we rate Regency Centers a BUY.

{kind=link}

Public Storage (PSA): Yielding 4.2%

For our final "old geezers" selection, we picked Public Storage , which is a self-storage REIT that owns, develops, and operates self-storage properties. Additionally, they manage self-storage properties for third parties and offer tenant reinsurance programs to cover certain losses of stored items.

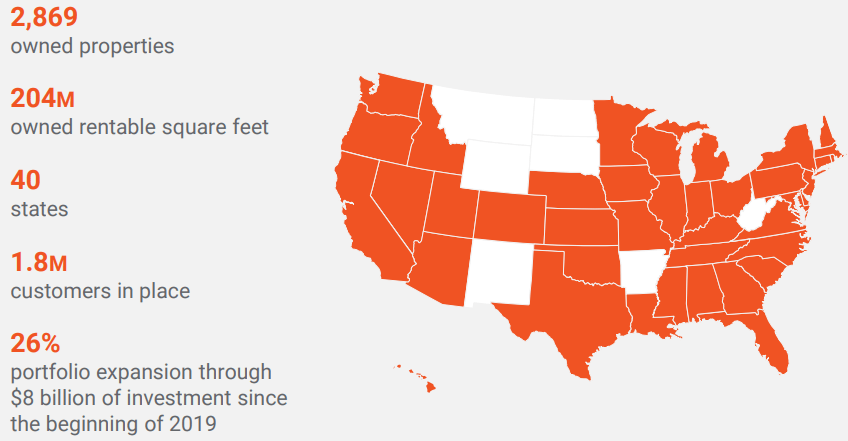

Their portfolio consists of 2,869 properties that cover 204 million rentable square feet and serve 1.8 million customers in 40 States. In addition to self-storage, PSA also offers business storage, Car and RV storage, boat storage, and climate-controlled storage. Additionally, PSA had a weighted average square foot occupancy rate of 93.2% as of March 31, 2023.

{kind=link}

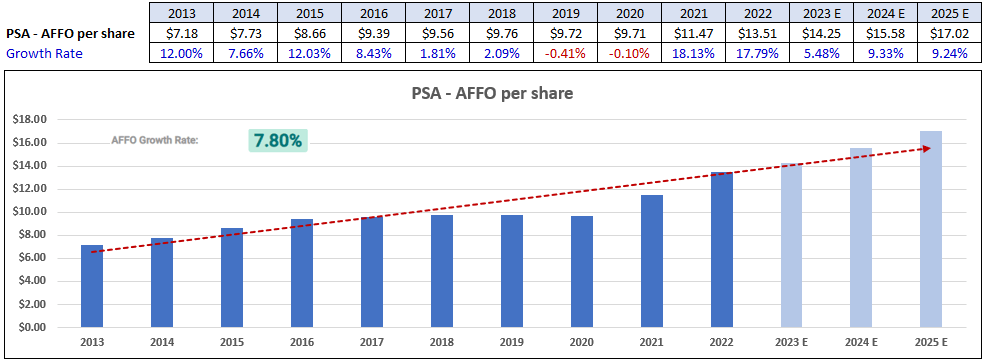

Public Storage has delivered AFFO growth in 8 of the last 10 years. AFFO fell by -0.41% in 2019 and -0.10% in 2020, but in on average PSA has an annual AFFO growth rate of 7.80% over the last decade. Analysts expect AFFO growth of 5.48% in the current year and over 9% AFFO growth in years 2024 and 2025.

{kind=link}

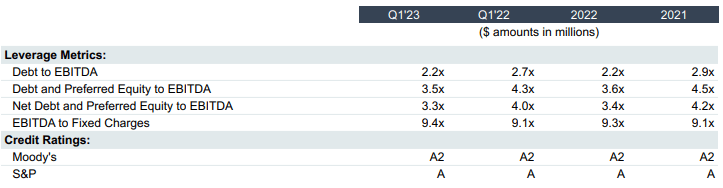

PSA has an A credit rating from S&P and an A2 rating from Moody's. They have excellent debt metrics with a debt to EBITDA of 2.2x, a debt and preferred equity to EBITDA of 3.6x, a long-term debt to capital ratio of 40.67%, and a fixed charge coverage ratio of 9.3x. As of the end of the first quarter, PSA had approximately $6.9 billion in debt with a weighted average interest rate of roughly 2.2%.

{kind=link}

Public Storage pays a 4.23% dividend yield that is very secure with an AFFO payout ratio of only 59.22%. This excludes the $13.15 special dividend that was paid in 2022. PSA has either increased or maintained its dividend since 2013.

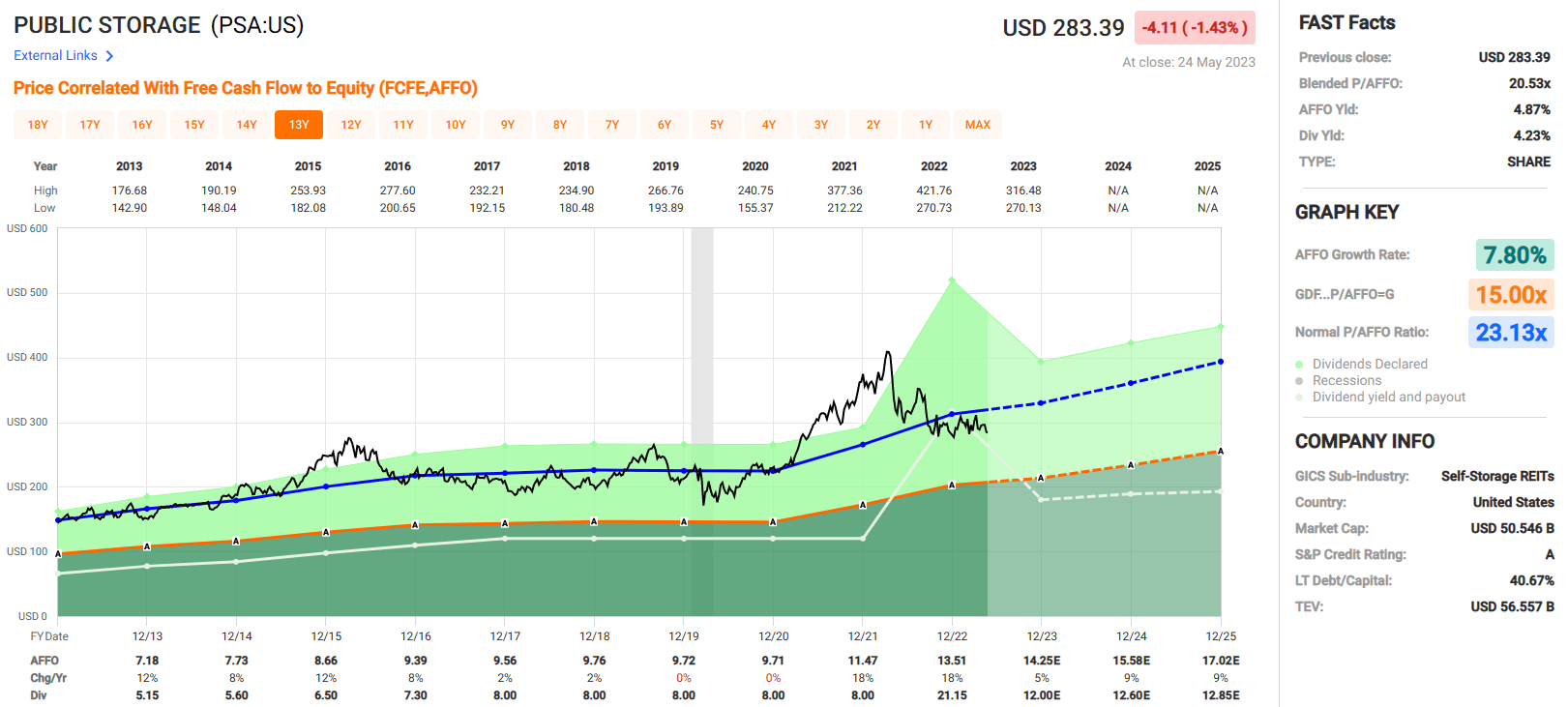

From 2017 to 2022 the regular dividend was maintained at $8.00 per share annually, but in early 2023 PSA increased their dividend by 50%, increasing the quarterly dividend from $2.00 to $3.00 per share or a total of $12.00 per share annually. Currently, PSA is trading at a P/AFFO multiple of 20.53x, which compares favorably to its normal AFFO multiple of 23.13x.

At iREIT, we rate Public Storage a BUY.

{kind=link}

In Closing

One of the most important REIT metrics that we look for is sustained levels of high cash flow, because we know that it leads to stability in valuation, as a substantial portion of asset value stems from relatively predictable cash flows.

We hand-picked all 5 of these REITs because we believe they will provide investors with predictable and durable dividends in any environment. They are also attractive because of their discounted valuation, which should lead to above average total return prospects.

As I pointed out to a reader this morning, you should be extremely happy you own these REITs a year from now. By adopting asset-allocation targets (we recommend 15% to 30% in REITs) that dovetail with personal risk tolerances (time horizon), you will greatly increase the odds of investment success and sleep well at night!

Happy SWAN Investing!

For further details see:

5 REITs For The 'Old Geezer'