REXR - 5 REITs I Felt Like Writing About

2023-04-03 17:36:19 ET

Summary

- Strong demand from consumers pushes tenants to continue leasing space.

- The need for space drives revenues, which drives AFFO per share. Growth rates are lower in some cases for 2023 because of variable rate debt.

- Average short-term rates for 2024 will probably be lower than 2023, so that shouldn't be a headwind to growth rates for long.

- I'll toss in one bonus pick to reach six REITs. Underpromise and overdeliver.

I want to start by talking about SBA Communications ( SBAC ), American Tower ( AMT ) and Crown Castle International ( CCI ).

I own shares in all three of these REITs. Tower REITs are a large allocation within my portfolio. For all the articles I write on mortgage REITs and BDCs, I have more invested in these three tower REITs combined than I do in common shares of mortgage REITs and BDCs combined .

I believe the tower REITs are going to be excellent long-term investments. However, we should address some of the headwinds and the tailwinds. This won't be every factor that impacts the tower REITs. It is one article. Not a dissertation.

After the tower REITs, I will highlight two other current bargains.

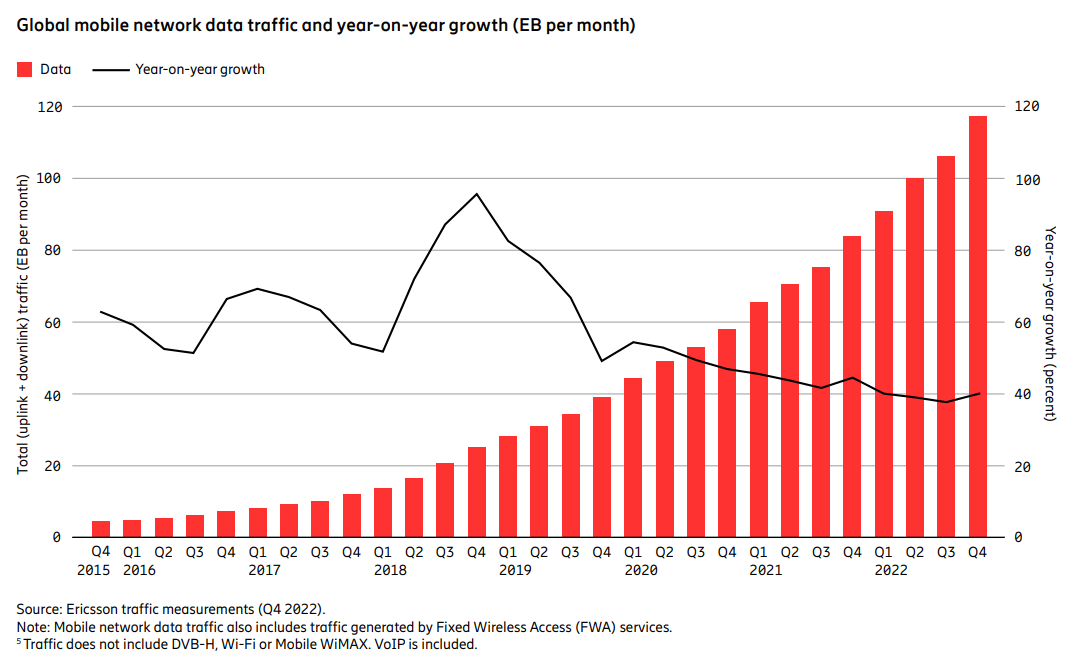

Data Consumption

Globally, data consumption is growing at 40% year-over-year and the growth shows up every quarter. The numbers were demonstrated in the Ericsson Mobility Report :

{kind=link}

Ericsson Mobility Report

Mobile data demand is only going to increase. The trend is clear in the chart. Fundamentally, it makes sense. Improving video quality takes more data. Loading a page with even more bloated code for features you don't want still takes more data.

What if Our Carriers Are the Best in The World?

I’ve criticized Verizon ( VZ ), AT&T ( T ) and T-Mobile ( TMUS ) for their weak investment in bringing 5G to customers. Is that fair? Probably. Using the 5G index from speedcheck.org, the median 5G speed test for the United States came in at a pathetic 57Mbps. A national disgrace. That’s ranked 28th in the world. Mexico landed at 72Mbps, good for 21st. In the areas that are actually getting sufficient 5G coverage, speeds are vastly better. If we replace the median for the United States with the 10th percentile, the speed jumps to 362Mbps. That’s a decent 5G connection, but it isn’t offered to most consumers.

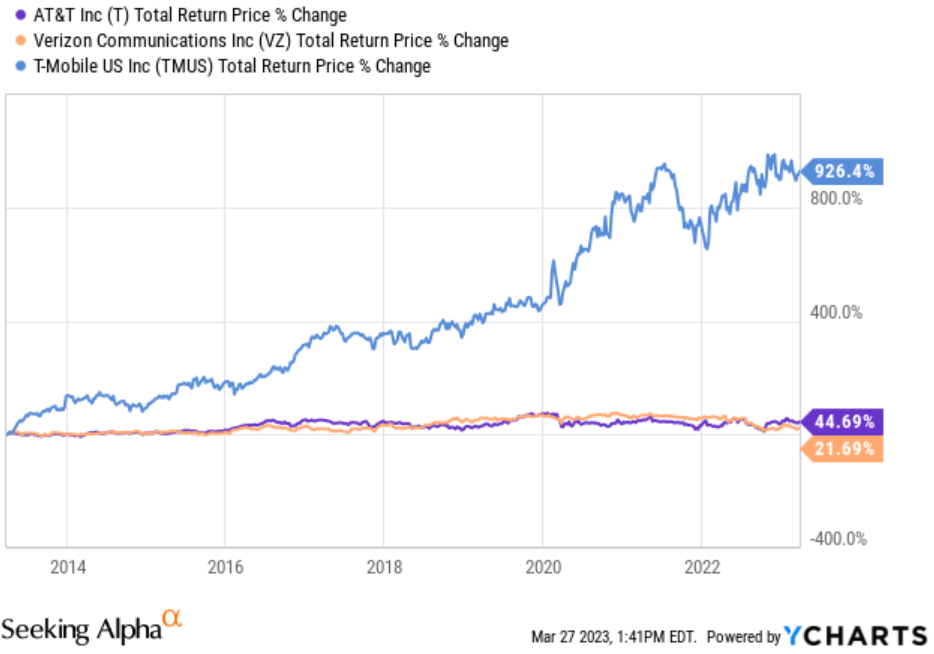

Why don’t carriers invest more in building out a First World 5G network? There are a few reasons. One is that the carriers have way too much debt. They borrowed stupidly, spent recklessly (sometimes on junk customers didn’t want), then saw interest rates rising rapidly. That makes building a better network a hard sell. Unfortunately, in the oligopoly, consumers don’t have many alternatives to supporting these debt-laden monuments to incompetent management (AT&T and Verizon):

The REIT Forum

Disclosure: I didn't make this chart the same day as uploading the article, so VZ (down to $158 billion) and T (down to $133 billion) have seen their market caps fall slightly further. Not enough to be material to our analysis, but I like to be accurate. TMUS market capitalization is still the same within a $1 billion rounding error.

To put those numbers in percentage terms:

The REIT Forum

While AT&T and Verizon ramped up leverage, they delivered a pathetic return to shareholders. T-Mobile, on the other hand, created enormous amounts of value as they were able to grow by simply not being T or VZ:

{kind=link}

YCharts

Good job, T-mobile. Not being T or VZ paid off.

That chart includes the value of dividends. It would appear that the key to industry success is simply not having the board of directors from AT&T and Verizon. Someone has to hold executives accountable when they spend lavishly on something that is not building a better network.

Prices Whacked in February

As rates ripped higher, the tower REITs took a big hit. Higher rates pressure earnings a bit, but they also pressure the over-leveraged carriers to reduce capital expenditures. Since tower REITs are long-term investments, some investors will also emphasize higher discount rates. Sure, those are all headwinds. Yet the demand for better connections remains.

The headwinds are primarily short term, while demand only continues to grow. That’s a nice environment for building long-term positions. The actual impact to cash flows over the next decade from the headwinds is minimal compared to the damage already seen in the share prices. All three of these REITs are down between 30% and 35% from their 52-week highs.

Biggest Risk

The biggest risk to the tower REITs is not satellite . Satellite is generally not cost-effective for high data speeds or when the customer is moving quickly.

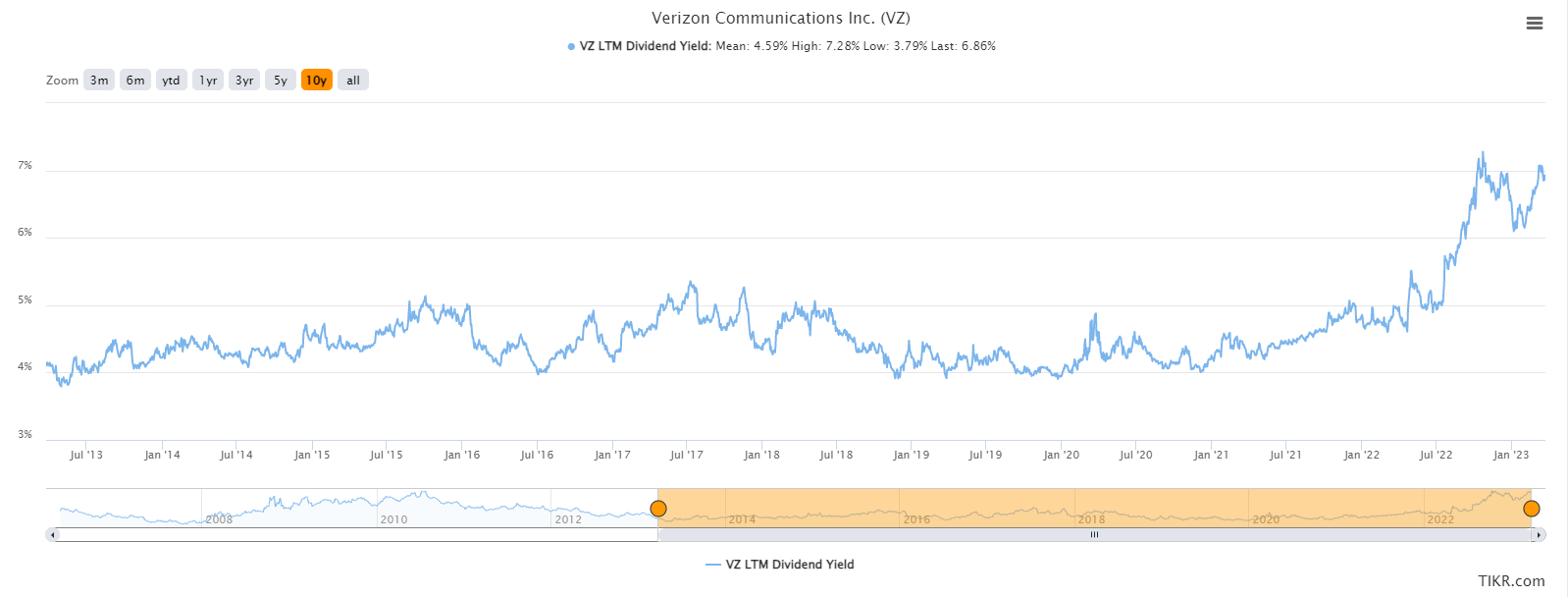

The biggest risk is the leverage at Verizon and AT&T. Leverage is creating a significant risk for these companies, which is reflected in the valuation.

Verizon now carries a 6.93% dividend yield. That's very high compared to their prior history:

{kind=link}

TIKR.com

AT&T on the other hand, slashed its quarterly dividend from $.39 per share to $.28 per share.

Other Bargains

There's a trend in our picks. Regarding equity REITs, we strongly prefer REITs that generate high growth in AFFO per share and have favorable demand from the end consumer. That doesn't mean that every tenant is strong. It means that consumers want the product that is delivered through the REIT's facilities.

For tower REITs, it comes down to the demand for mobile data from the end consumers.

For industrial REITs, it comes down to the consumer's desire to buy junk online and have it delivered quickly.

Prologis

Prologis ( PLD ) is the biggest industrial REIT. It's also a great choice for long-term wealth builders.

Occupancy remains high:

{kind=link}

PLD

Most of the expiring leases are renewed:

{kind=link}

PLD

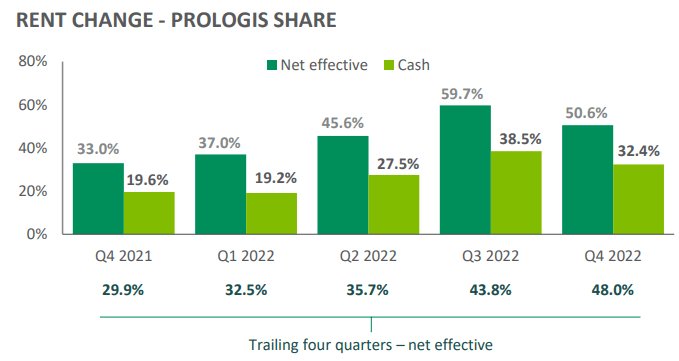

Prologis can significantly increase rents:

{kind=link}

PLD

That combination leads to massive growth in same-store net operating income:

{kind=link}

PLD

Those factors all combine to push substantial growth in normalized FFO per share. However, sometimes investors misread the growth rates because PLD also includes some profits from their development activity. That can make the year-over-year growth rates look more volatile than they would otherwise be.

Rexford Industrial

Rexford Industrial ( REXR ) is another one of my favorite REITs. The portfolio is entirely located in southern California. Even if you're one of the many Seeking Alpha readers who simply hates everything about California (hello, about 80% of you), you may still love the math.

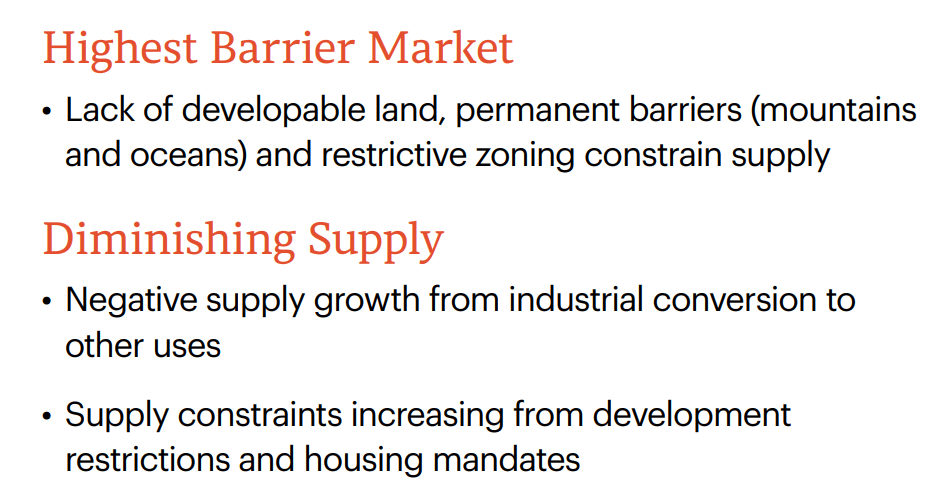

Southern California is an ideal place for industrial real estate:

{kind=link}

REXR

I want to emphasize the point about negative supply growth. While Rexford is achieving huge leasing spreads, the supply in southern California is falling. Rexford is operating in the "infill" markets.

They're in locations where it's extremely hard to build any new supply.

Even if a developer could get approval to build there, the land underneath the warehouse is so valuable that it usually goes to other uses. Probably not office anymore. Office real estate is terrible, as The Real Deal highlighted:

{kind=link}

The Real Deal

That's awful, but I suspect it will go even higher. Much like terrible malls with repetitive tenants and excessive markups, office space is simply overbuilt.

We don't want to own offices, but we do want to own industrial real estate. Quick sanity check! Southern California industrial real estate is still occupied, right?

REXR

That looks good.

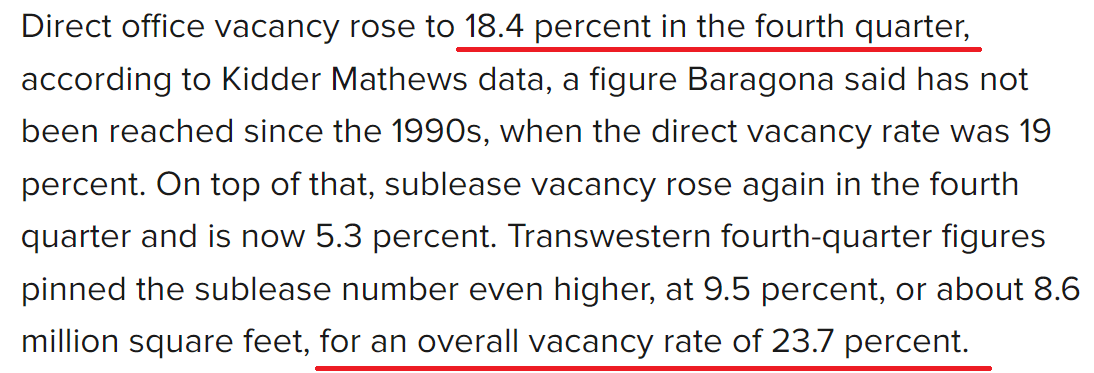

How's office space doing in California? Does anyone have the vacancy rate for a big important market like Los Angeles?

{kind=link}

Avison Young

Thanks, Avison Young , for those figures.

Conclusion

We like REITs that have a strong history of providing growth in AFFO per share and strong demand trends that should enable them to perform well in the future. That does not require significant growth in every year. The tower REITs generally had exposure to floating-rate debt that significantly impacted their year-over-year growth metrics.

Their growth rates shouldn't be hammered that way by higher floating rates in 2024. There's a strong chance that the average fed funds rate for 2023 will be higher than the average for 2024. That can annihilate the interest rate story for pressure on AFFO per share.

Industrial REITs should see strong leasing spreads throughout the rest of the decade with a good chance to go beyond that. Brick-and-mortar is facing a serious decline as ordering online only becomes more convenient.

There's one other tailwind I'd love to see. I'd like to see Amazon ( AMZN ) improve its filtering mechanics when searching the site. The sheer volume of key data points customers cannot use to filter results is insane. That would be another step in further cementing the absolute domination of ordering our junk online.

Bonus Pick

You get one more for free! I also like Alexandria Real Estate ( ARE ). I wrote a huge subscriber article on Alexandria (paywalled link) for members of The REIT Forum. I also provided a public article with a portion of it. I'll share another bit here:

Guidance for 2023 calls for spending $200 to $400 million on acquisitions (though with the current share price, I think they should be cautious), and $2,400 to $3,550 million on construction. That’s why Alexandria keeps growing. They do expect to see debt increase by $550 to $850 million (net of repayments) to fund construction. However, they also expect to see significant proceeds from dispositions or sales of partial interests. That is their primary source of cash for development.

Dispositions have been another important part of their playbook. ARE doesn’t keep all of the assets they develop. They sell a substantial amount of real estate because they want to leverage their expertise in development. During 2022 they had $2.2 billion in dispositions.

My Expectations

I think on average we should expect normalized FFO per share growth to run at least 3% annualized (big bear scenario) up to about 8% annualized (big bull scenario). That’s an average growth rate and there should be years outside that range. It excludes any non-recurring items. That’s a good range for a REIT with a 4.13% dividend yield (at $117.08). I would guess that the actual forward growth rate probably runs around the 5% to 6% range over the next decade, but that’s a long time and other factors certainly could creep up.

I’m expecting the dividend growth rate would be comparable to FFO growth rates.

I own shares in all 6 REITs. Using today's closing prices, each position is worth 1.63% to 8.6% of my total portfolio.

Ratings: Bullish on AMT, CCI, SBAC, PLD, REXR, ARE

For further details see:

5 REITs I Felt Like Writing About