O - 5 REITs/REs For 4.5%+ Yield With High Upside And BBB+ Ratings

Summary

- I'm a fan of investing in "baskets", and structuring my portfolio and my investments so that they generate impressive returns at conservative valuations.

- I also focus on fundamentals - and below BBB usually isn't for me.

- In this article, I show you how you can buy $10,000 of 5 companies, generating 4.5%+ yield at BBB+ with a conservative, average upside in the double digits.

Author's Notice: This article was published to iREIT on Alpha about 3 weeks ago back in January of 2023.

Dear readers/followers,

We've seen a fairly good start for the year - most things seem to be up, at least somewhat at this time, even though I fully expect them to decline back down again fairly soon as earnings and more worries for the year start coming in and materializing across the board.

I've been pushing capital to work in a variety of companies across multiple sectors - but I keep coming back to real estate as a focal point given the low valuations that are available here.

I wrote about Vonovia ( OTCPK:VONOY ) not that long ago, but I figured I could show subscribers how we can take some of the most undervalued businesses available today in the space, and construct a small purchase basket or portfolio with excellent fundamentals.

Let's say $10,000 - and we use $2,000 in each of the companies that we pick here.

We also want those companies to be conservative and "safe" - as safe as we can make them.

And we want them to have an upside, as well as a well-covered dividend.

So, to recap here, we want:

- BBB or above.

- 4.5% average yield for the invested $10,000

- A justifiable double-digit upside based on conservative multiples. I don't want any overvalued equity here, only cheap.

- No Office REITs.

- No Speculative Sector/Cannabis REITs.

- International Profiling

Can we do this?

Yes, we can - and I just did this.

So let me show you.

What I did was put money to work in 5 of the most attractively valued, higher-yielding, and safe Real Estate/REIT-based stocks I currently follow.

Here they are, in no particular order.

1. Vonovia (BBB+, 6.3%+ native yield)

While Vonovia has seen a decline for the past year, as the company dropped below €30/share, I've really been pushing on the gas in terms of buying the company, to where it now is above 1.5% both in my private and corporate account.

As with many of these stocks, you'll note the common denominator that the drop isn't accompanied by a fundamental worsening of the operating results. While the environment has changed - with zero interest rates being done, and the companies having to borrow at far higher rates - companies that have prepared for this possibility, like Vonovia, are still seeing very strong trends.

The company owns close to half a million units across Europe, with its obvious focus on Germany. Vonovia has one of the best capital structures on the market, and consequently still borrows/manages loans at less than 2% (or thereabout) interest on average, with a 50%+ rate of unencumbered assets in FY2022E. LTV is conservative as well.

I argue that Vonovia's main issues are political, not financial. Like other European geographies, Germany suffers from decades of underbuilding, especially in high-demand areas, which will drive demand for Vonovia's properties for years to come.

The current valuation trends would suggest that there are substantial or fundamental threats/risks to the company. While I do see some political uncertainties, the larger part of the company's operations remain completely unaffected and profitable. This is expressed in the company's operating results and the forecasted dividend growth.

With operating performance in line, rent growing, vacancy rates low, high rent collections, growth in FFO, and a solid 2023E guidance, Vonovia remains a "BUY" for me, and my first pick in this list.

I expect the company to do well enough over the past few years - and even if there's barely any growth here, the current price does not accurately reflect the underlying quality. If anyone has a concern or a realistic view as to why this company should be worth the price its trading at today at around €26 per share, I'd be happy to field this. Remember though, S&P Global analysts are some of the most split I've ever seen. 17 analysts give the company a range from €14 on the low to €70 on the high, with 12 out of 17 analysts either at a "BUY" or "Outperform" rating for the company with an average PT of €35, noting an upside of 33%+ here.

For that reason, I'm a "BUY" here, and the first $2,000 of this buying basket.

I own more than 1.5% of my portfolio in Vonovia, and I'm buying more.

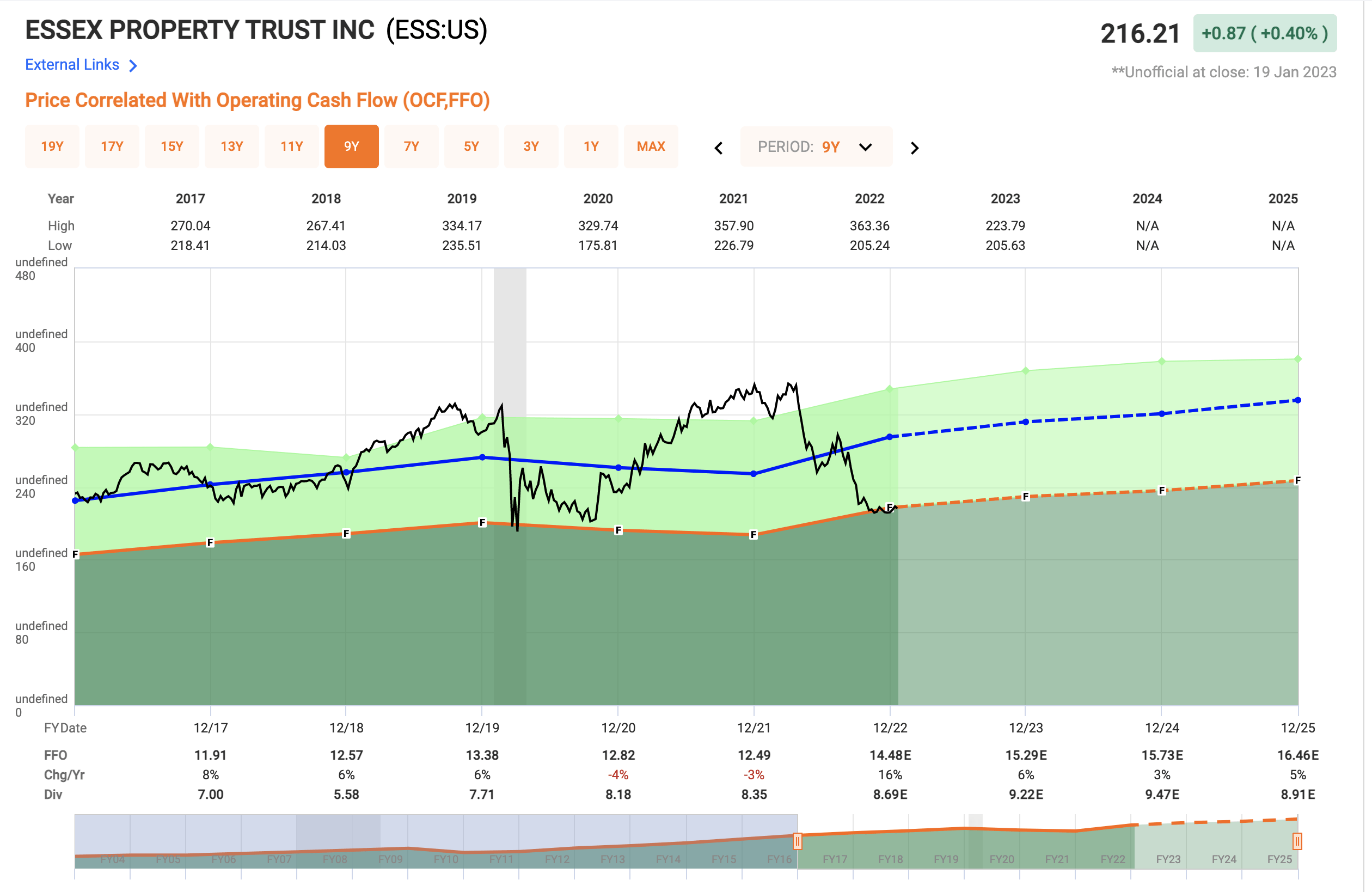

2. Essex Property Trust ( ESS ) (BBB+, 3.75% Yield)

Essex is another one I've written about before. Apartment REITs are some of the safer investments to be made in the sector, and a business like Essex isn't undervalued often - in fact, almost never.

On a high level, Essex seems really like the perfect sort of Resi REIT. You have a BBB+ credit rating, a yield of 3.75%+ that's more than covered by a superb FFO, and stable underlying operations. Essex has a market cap, following the decline, of just south of $14B.

The company's driving characteristic is that it's primarily a west-coast exposed residential REIT. This, of course, comes with its share of issues in the current macro and geopolitical climate as well as market trends. However, the way that the market is treating the company because of this is excessive, to say the least.

This was my stance a few months back as well - and fundamentals in terms of valuation haven't really changed since then. Take a look at this and you'll see that Essex is at COVID-19 valuation levels - and this is even with the company expected to grow FFO over the next few years.

{kind=link}

ESS valuation (F.A.S.T graphs)

You'll never hear me say that you should invest in this company above 20x P/FFO. I'm all about valuation - I might not be "Mr. Valuation", that's the esteemed Chuck Carnevale, who owns F.A.S.T graphs, but I try to work along the same lines. It's all about above-average quality at below-average valuation, with above-sector dividends. The wider we can get those spreads to go, coupled with those superb fundamentals, the better and the more interested I get.

For Vonovia, I believe 20-30% annualized RoR isn't out of the cards. For Essex, I'd go a bit more conservative. I'd forecast at 17-18x, which gives us around 14-17% RoR including dividends, to a 55% RoR for the 2025E period at year-end. Note, however, that this is below a relatively well-established premium, right?

Not something to scoff at, for sure.

Essex is my second pick - I'm at 1.1% here, and I'm buying more.

3. Realty Income ( O ) (A-, 4.57% Yield)

Realty Income again? Yes - Realty income again. I won't stop highlighting this company's current valuation until it either moves north of $68/share or until everyone tells me they're at capacity.

Realty Income is the largest REIT investment I hold. Including my corporate investment account, I'm at 7% of my total here, with a YoC of over 5.5%. The current yield is 4.57%, which is still respectable.

Yes, I believe the company is worth over 20x P/FFO premium, and yes, this means that there is a 50%+ potential RoR on an A- safety with a 4.4%+ yield portion here. Yes, we could go lower again, but I don't believe this to be a long-term reality if we do go that low. Realty Income has proven over and over again that not only can it survive in downturns, but it can also thrive.

My picks in this list do not necessarily focus on the companies that have the most upside out there. Only focusing on this quality means including companies that come at elevated risk ratios.

That's why most of the office picks I otherwise make aren't necessarily part of this list. Even if I view them as safe, I fully admit that they come with risk profiles that aren't compatible with what most conservative investors want.

So, here, it's all of:

- Quality

- Yield

- Valuation

If a REIT/RE company does not have all three, it doesn't get a spot on this list.

Realty Income has it - in spades. That's why it is the largest current holding in my entire portfolio, bar none.

I believe you should consider making it yours as well.

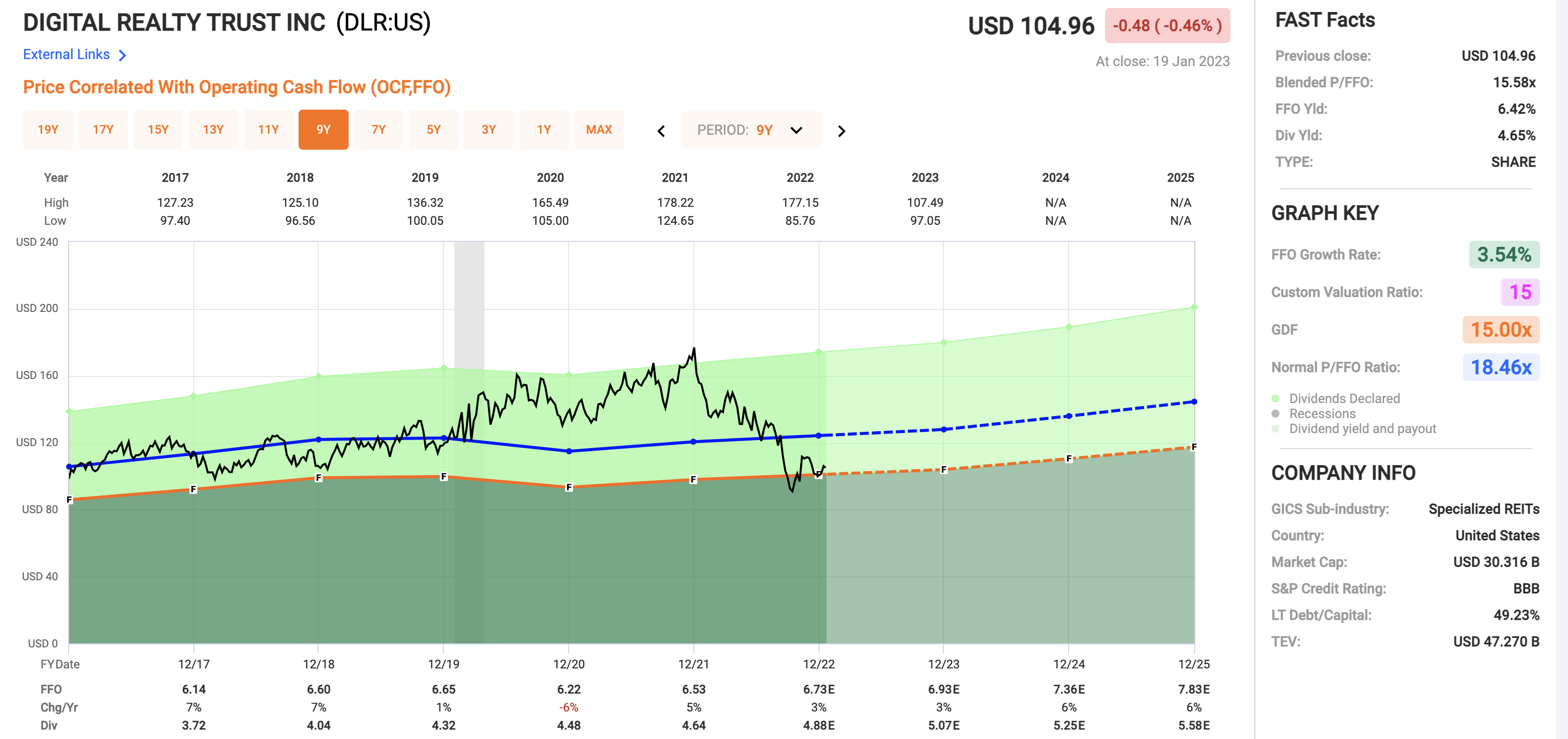

4. Digital Realty Trust ( DLR ) (BBB, 4.15% Yield)

I consider it a mark of quality that the lowest credit rating I'm willing to go down to here is BBB. Not BBB-, but a straight IG rating, and DLR is the only one on this list that has "that low" of a rating.

I wouldn't touch DLR at a high multiple - so I consider much of the premium to not be valid at this time. In fact, I would prefer forecasting DLR at no more than 17-17.5x P/FFO at the highest, making only a small allowance for its scale moat and the way the company has built an impressive cash flow generator.

Remember how this company traded during "froth"?

{kind=link}

DLR Valuation (F.A.S.T graphs)

DLR also has a strong international profile for its earnings, given where its data centers are located.

Above all, remember that the market loves to overvalue things and undervalue them. Going too high and too low in reaction to external factors or internal news is sort of the standard M.O. for how the market operates. It's up to us to take advantage of this, by buying low and selling high - not the other way around.

DLR may face some of the challenges that bear ascribe to it. I'm talking about things like increased competition, margin pressure, and increased costs. But I don't think it will fail to meet its cited growth objectives, even if those growth objectives are now at the single-digit and low-single-digit level.

Even at a low single-digit growth with a 17.2x P/FFO on a forward 2025E basis, we get a double-digit annualized RoR of over 12% here. People that are too bearish on DLR at this point often make the mistake of forgetting the company's fundamental advantages - its scale and current existing operations.

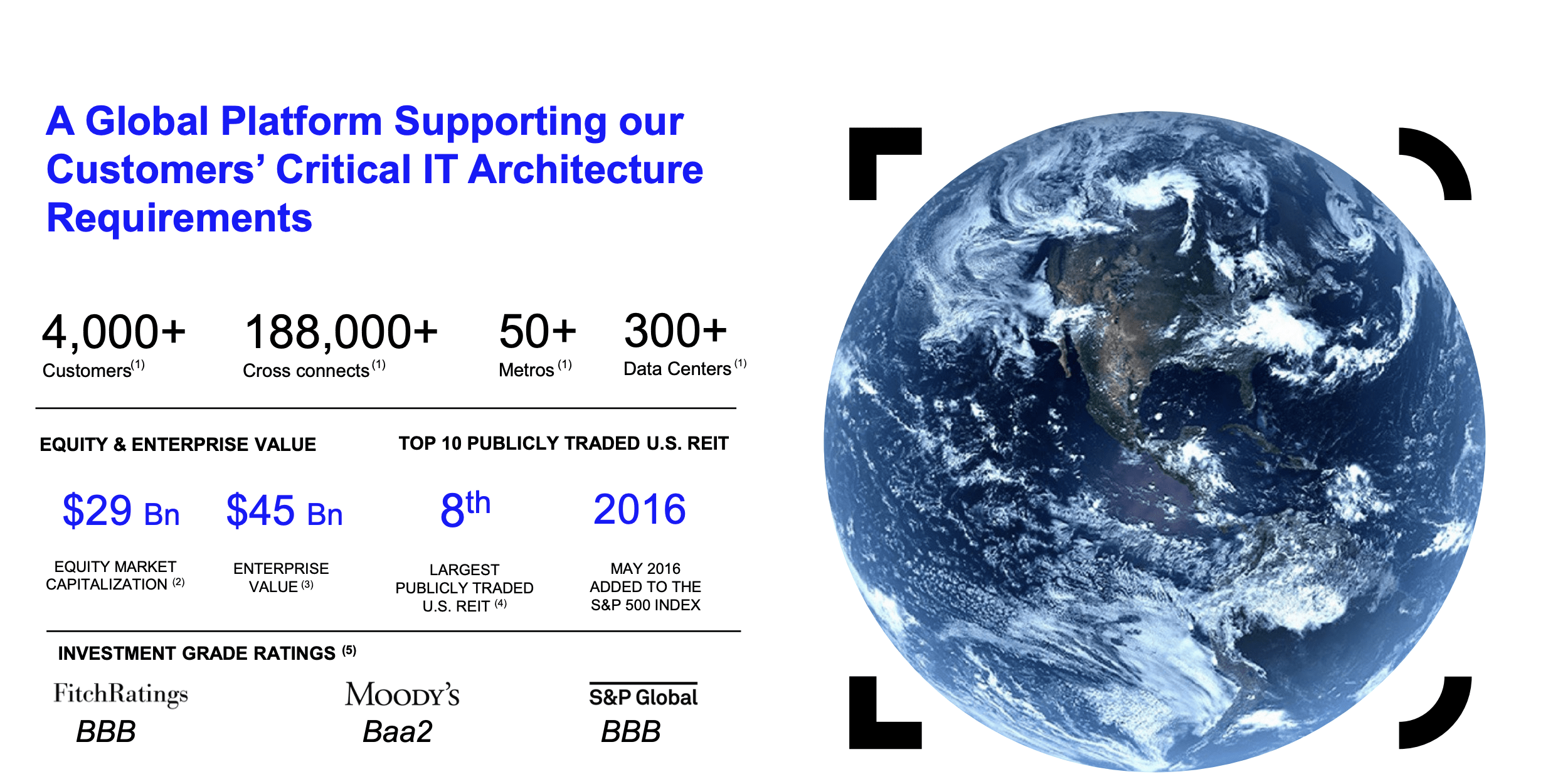

{kind=link}

DLR IR (DLR IR)

Switching isn't that easy, and while challenges will no doubt continue to present themselves, I firmly believe that the company will rise to face them. Many readers mistook my stance for a general bearishness against DLR. This is not the case. I was bearish about the valuation. I refuse to overpay for companies.

Digital Realty Trust is a global-spanning data center REIT "empire" that's bound to, at the very least, deliver stable results going forward - and this trend is confirmed by the recent quarterlies and current forecasts in the near term.

Bookings on a historical basis have shown good growth for at least 10 years, and the company's customer metrics are more than satisfactory. Companies of all sizes, and of all sectors, go through DLR. But DLR isn't an amazing grower. The fact is, it has never been that. Because of that, it should never have, as I see it, been trading above 20x P/FFO in the first place. This was a measure of the times we were in, where everything has to do with data, IT, software, crypto, and all the other related "buzzwords" gained some market premiums.

For too long, investors have acted as though the exuberant bullish thesis is based on "free money" and "infinite demand". It's essentially the same thesis/problem I saw for 99% of all tech investments a year ago - and why contrary to many investors, I was close to 0% invested in IT/Tech when the crash came.

But especially for existing quality infrastructure, there exists a very real bullish thesis that should be looked upon favorably at the right price.

Well, the right price is here now, and this is my #1 Data Center REIT.

I now have 0.5% in DLR, and I mean to buy more.

5. AvalonBay Communities ( AVB ) (A-, 3.5% Yield)

I went back and forth with myself several times before going for my last pick here. My "portfolio" could have gone above 5% on average in yield, with a much higher conservative upside, if I had elected to include either office or specialty REITs. In the end, I knew that this opened up valid concerns of risk due to how the market is looking for the office sector, or how things are going in terms of volatility in specialty areas, such as Cannabis.

So instead of going for one of my favorite office REITs, I went for AvalonBay instead.

AVB is a storied dividend payor with a 5% annualized DGR since its IPO and has averaged nearly 13% TSR since that IPO, making it a better bet than the broader market. Some very basic, and some very positive facts.

People like to often talk about risk today - and their talk about risk in AvalonBay is of course there as well. Well, AVB has an A-rating in credit, less than 5.4x net debt/core EBITDA, a 6x+ interest coverage, a 93%+ unencumbered NOI, and a payout in terms of FFO that goes below the 65% range for the 2022E period.

This company is a solid, 2%+ part of my overall portfolios, and I started buying again after the company hit below its 10-year premium FFO of 18.5x, which is when the double-digit upside to 18-20x P/FFO that I was looking for started to materialize. Thankfully, and as we're writing this article that's still an upside that we can see here.

AVB is very similar to Essex in many ways - and it also comes with a 9-13% annualized upside to premium valuations here, which I would argue to be one of the better ones in the space, combining safety as well as quality with a decent yield.

AvalonBay is my last choice in this list - the fifth spot, which turns this investment list or portfolio into a good basket of what I consider to be very undervalued, quality REITs with a good upside.

I have over 2% AVB in my portfolio, and I consider this quality apartment REIT a "BUY" here, for the conservative upside we're seeing.

Wrapping up

So - as mentioned - I could have gone with a much more Office-centric basket of REITs here, which I do consider quality and undervalued as well. I could also have gone with specialty REIT sectors, such as Cannabis, which is seeing some very compressed valuations due to the instability in the industry. There are also mall REITs I could have looked at as parts of this "basket" of REITs.

However, I realize that not everyone has the same sort of risk tolerance, or desire to expose oneself to these riskier (compared to what I'm presenting here) sectors.

For this reason, I elected to ignore most of what I view as solid investments in this article - exchanging safety but "paying" with the higher yield otherwise available if you went for these.

The basket I've picked for you here, if you invest $2,000 per company here, will yield a total of ~4.5%, generating ~$450 on a $10,000 investment over a period of 12 months.

I consider this a very solid sort of set of investments - because aside from the yield, it also comes with a conservative double-digit potential for capital appreciation.

This is pretty much what I look for when I do my monthly investment allocations - I look for "baskets" of companies that, combined, give me a solid return potential not only in the short term but the medium and long term as well.

So, that's my message in this article - and these are my five ideas. Questions? Let me know!

For further details see:

5 REITs/REs For 4.5%+ Yield With High Upside And BBB+ Ratings