VNQ - 5 REITs That Will Likely Cut Their Dividends

2023-08-14 08:05:00 ET

Summary

- Not all REIT dividends are sustainable.

- Quite a few will have to cut their dividend in the coming quarters.

- We highlight 5 of them.

I am very bullish on REITs ( VNQ ) because their valuations have gotten very low in many cases, but I am still objective enough to realize that not all glitter is gold.

In a recent article, I explained that quite a few REITs will likely need to cut their dividend in the coming quarters.

That's simply because some REITs are overleveraged. Others are poorly managed and simply pay too much. And then there are others that own cyclical assets that will struggle as the economy dips into a recession.

Below I highlight 5 REITs that are likely to cut their dividend:

Easterly Government Properties ( DEA )

Let me start by saying that I don't think that DEA is in a rush to cut its dividend.

The REIT is generally well-managed, its properties enjoy long-term leases, and they have limited debt maturities in the near term.

So they could keep paying the current dividend for a while if they decided to.

But eventually, I think that a cut is likely because they own a lot of single-tenant office buildings that are leased to government agencies and according to a recent survey (US Government Accountability Office), 17 of 24 agency headquarters were utilizing 25% or less of their office capacity and every other agency used less than 50% of the space in the first quarter of 2023.

Easterly Government Properties

This shows you that government agencies are working even more remotely than private companies and this makes sense to me given that the government probably doesn't care as much about the productivity of their employees. This report appears to have prompted a major REIT activist investor, Land & Buildings, to short DEA. They issued the following statement on Twitter ( TWTR ):

"Downsizing of the office footprint by the government agencies is likely, in our view. 98% of Easterly Government Properties rents are from U.S. government agencies. L&B has a position in DEA."

Making matters worse is that they have quite a lot of leverage with a Debt-to-EBITDA ratio of 7.2x and they are paying out nearly all of their cash flow with a 93% payout ratio, leaving little room for error.

Their interest expense will inevitably go up in the coming years even as their capex requirements go up, and unfortunately for them, most of their leases have limited rent hikes to make up for that.

The government holds particularly strong bargaining power and they have been able to negotiate flat shell rents across most leases and only provide compensation for the growing expenses of the building.

That's a big issue in today's rising interest expense environment and it could eventually likely lead to a sizable dividend cut.

I don't see the value here.

OUTFRONT Media ( OUT )

While I don't see the value in DEA, I actually see it in OUT and I am bullish on the company.

This is one of a few REITs that specializes in billboards and it has sold off heavily over the past year because its business is somewhat cyclical and it has quite a bit of leverage.

The sell-off is somewhat understandable in that sense, but I think that it has gotten overblown. Yes, a recession would cause some pain and would likely even force the REIT to cut its dividend, but that's not the end of the world.

OUTFRONT Media

A cut would likely only be temporary, just as how the REIT temporarily suspended its dividend during the pandemic, but then rapidly reinstated it.

It is a cyclical business and when you operate with more leverage than average, you just have to be flexible with your dividend policy.

My point here is that I think that OUT is undervalued and offers good value for long-term-oriented investors, but I wouldn't buy it solely for the dividend. It is more of an upside play.

Medical Properties Trust ( MPW )

Another REIT that I think is undervalued, but likely to cut its dividend is MPW.

We own a position in it, but we still recognize that this is a high risk / higher (potential) reward type investment and the dividend is at high risk because their cash flow does not fully cover it and some of their tenants are facing difficulties.

So far, the management has said that they expect these difficulties to ease over the coming years, which would then improve the dividend coverage, but in the last conference call, the management hinted at a possible cut to increase liquidity:

Jonathan Hughes (analyst)

"Okay. And I guess then just sticking with the updated guidance from this morning and the midpoint of kind of the third quarter and fourth quarter FFO implied by the updated guidance is about $0.35 and then if you take out the non-cash income, you’d get to just call it, $0.28 or so of FFO, which would be below the quarterly dividend, but I know that’s expected to improve in the next year. And I asked about sustainability of that dividend last quarter and you are comfortable with -- and you said you were comfortable with it, but the market today is still giving you a little credit with the stock yielding 13% and leverage is up from last quarter to nearly 7 times. So I just have to ask again, has the Board seriously considered a cut to retain more funds to more quickly improve the balance sheet and pay down debt?"

Steven Hamner ((CFO))

"So, look, I would just reiterate what both, Ed and I have already said, and that is we’re not satisfied with our cost of capital as implied by the share price. We’re not getting the credit that we think we should.

And so going all the way back to, I think, our fourth quarter call back in February, I think, we actually said everything is on the table and that’s at the Board level. And then, again, just a few minutes ago, I said the Board is constantly evaluating, considering that. And we’ve talked already on this call about liquidity opportunities and I’ll just repeat it, if everything is on the table."

Once more, don't buy this one for the dividend. MPW is a total return play with significant long-term upside potential, but it has a speculative nature and the dividend is today at high risk.

Global Net Lease ( GNL )

This one is easy.

A conflicted management team that has time and time again diluted shareholders with equity issuances at the wrong time.

A lot of single-tenant office properties that will face significant issues in the coming years and require a lot of capex.

A dividend payout that's not covered.

Too much leverage.

And finally, an expensive merger and management internalization that will likely be the catalyst to a right-sizing of the dividend.

{kind=link}

Here's what a big shareholder of GNL said about the merger:

“The proposed merger is another deceptive effort by AR Global, in complicity with GNL and RTL, to skirt ongoing proxy fights against them, and the ultimate accountability that will face them," Jason Aintabi, Founder and Chief Investment Officer of Blackwells said in a statement. " Shareholders should be on high alert that the compromised boards of GNL and RTL approved a deal that would arrogate a $375 million ransom payment to AR Global, Michael Weil and Nick Schorsch in return for all the value they’ve destroyed. Blackwells strongly opposes the cockamamie merger, and expects most other shareholders to do the same.”

I am staying far away from this one.

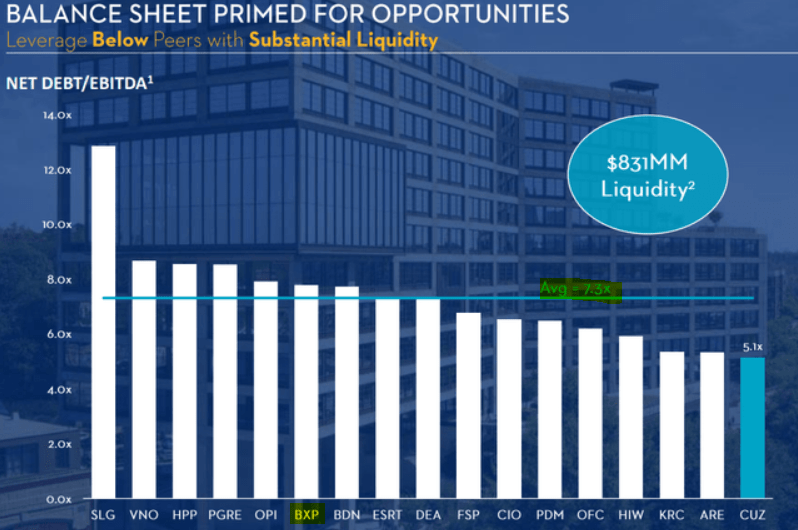

Boston Properties ( BXP )

Finally, some of you will likely be surprised that I bring up BXP, which is commonly perceived to be the "blue-chip" of office REITs.

It has a good balance sheet, a strong management team, and it owns mostly class-A properties.

But even that won't save you in today's office apocalypse.

BXP is heavily invested in coastal markets, which are suffering more than the average, it also owns some older properties that will require a lot of capex, and it has slightly more leverage than the office peer group - and its interest expense will skyrocket in the coming years:

{kind=link}

{kind=link}

Piedmont Office ( PDM ) has less leverage and owns better-performing sunbelt office buildings and it just recently refinanced some of its debt with a near 10% interest rate.

As BXP's interest expense ticks up and it needs to reinvest in its office buildings, I expect it to cut its dividend sometime in the coming years.

The payout ratio may seem low today, but that was also the case for mall REITs back in 2017. If you recall, back then, many of us including myself made the mistake of thinking that the mall REITs could sustain their dividend payments because their payout ratios were low based on their FFO.

But we made the mistake of underestimating the capex that was coming their way. I fear that the same applies here.

Bottom Line

Every sector has some good, some average, and some bad companies.

REITs are no different.

Some REITs are exceptionally opportunistic today and offer a path to significant returns in the coming years.

But at the same, some other REITs are on shaky legs and could lead to painful losses in the years ahead.

Select carefully.

For further details see:

5 REITs That Will Likely Cut Their Dividends