VICI - 5 REITs To Add To Your Christmas Shopping List

2023-12-21 08:05:00 ET

Summary

- REITs are today offering a historic opportunity.

- Rents keep on rising, balance sheets are stronger than ever, but valuations are heavily discounted.

- Here are 5 REITs to add to your Christmas shopping list.

Co-produced by David Ksir.

Real estate investment trust, or REIT, share prices have declined meaningfully over the past two years, and we think now is a great time to invest in REITs, because:

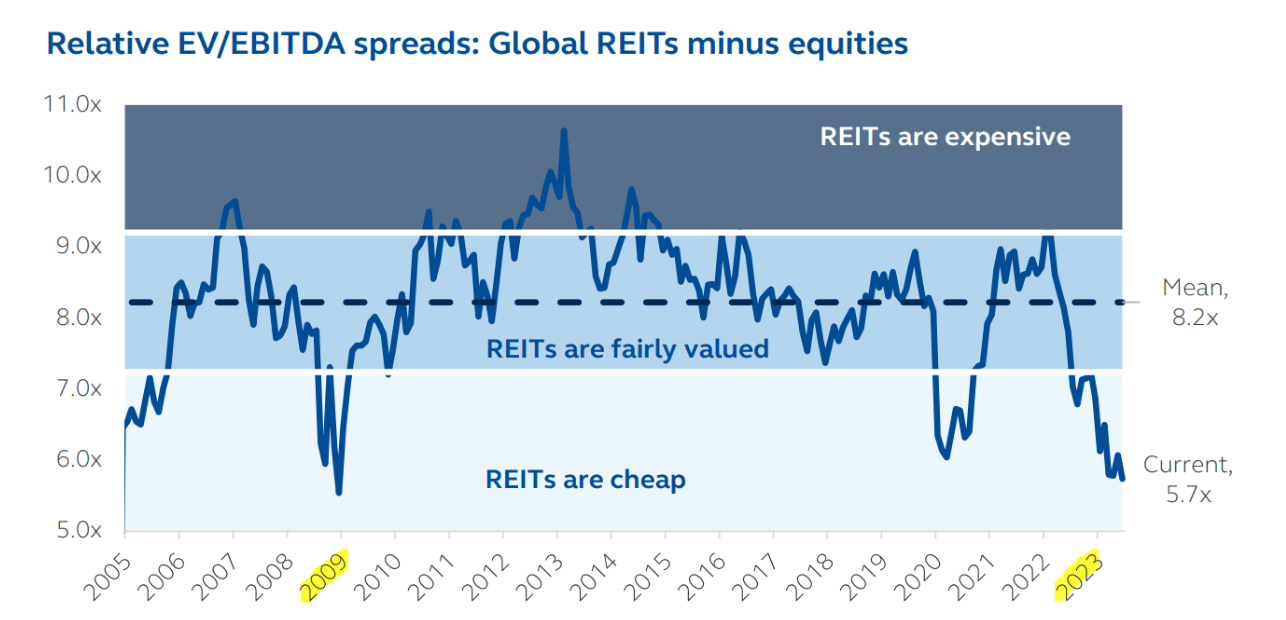

1) Valuations are now at the very low levels last seen during the Great Financial Crisis:

{kind=link}

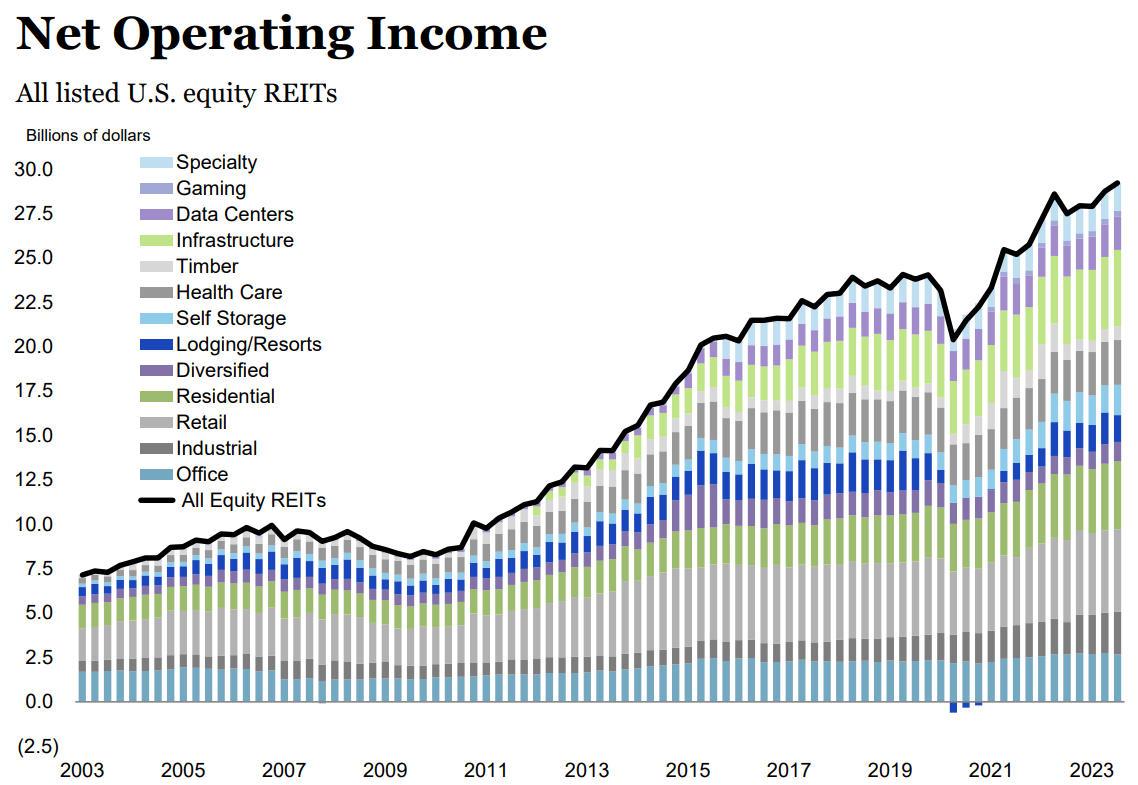

2) Most REITs are positioned to grow their cash flows despite high interest rates. This is because leverage is low, maturities are long, and rents are still growing at near the fastest pace in a decade:

{kind=link}

3) And we see a significant chance of rate cuts in the second half of next year. Most major banks, including Bank of America ( BAC ), JPMorgan ( JPM ), and Deutsche Bank ( DB ), are predicting just that, and this is starting to become the consensus expectation of the market:

Refinitiv via CNBC

If they are right and interest rates indeed decline from here, then the share prices of many REITs could rise significantly already in the near term. If they are wrong and rate cuts take longer to materialize, then we'll get to collect and reinvest high dividends while we wait for the (eventual) decline in rates, which based on our research is very likely.

Today, we highlight 5 REITs that make great BUYs and should be on everyone's Christmas shopping list.

Agree Realty Corporation ( ADC )

The best word to describe ADC is safety.

The REIT focuses on high-quality big box properties leased to very reputable investment-grade rated tenants such as Walmart ( WMT ) or The Home Depot ( HD ), and it also invests heavily in ground leases, which are the safest properties across all sectors of commercial real estate. For these reasons, ADC has historically enjoyed near-perfect rent collections and very stable revenues.

Agree Realty

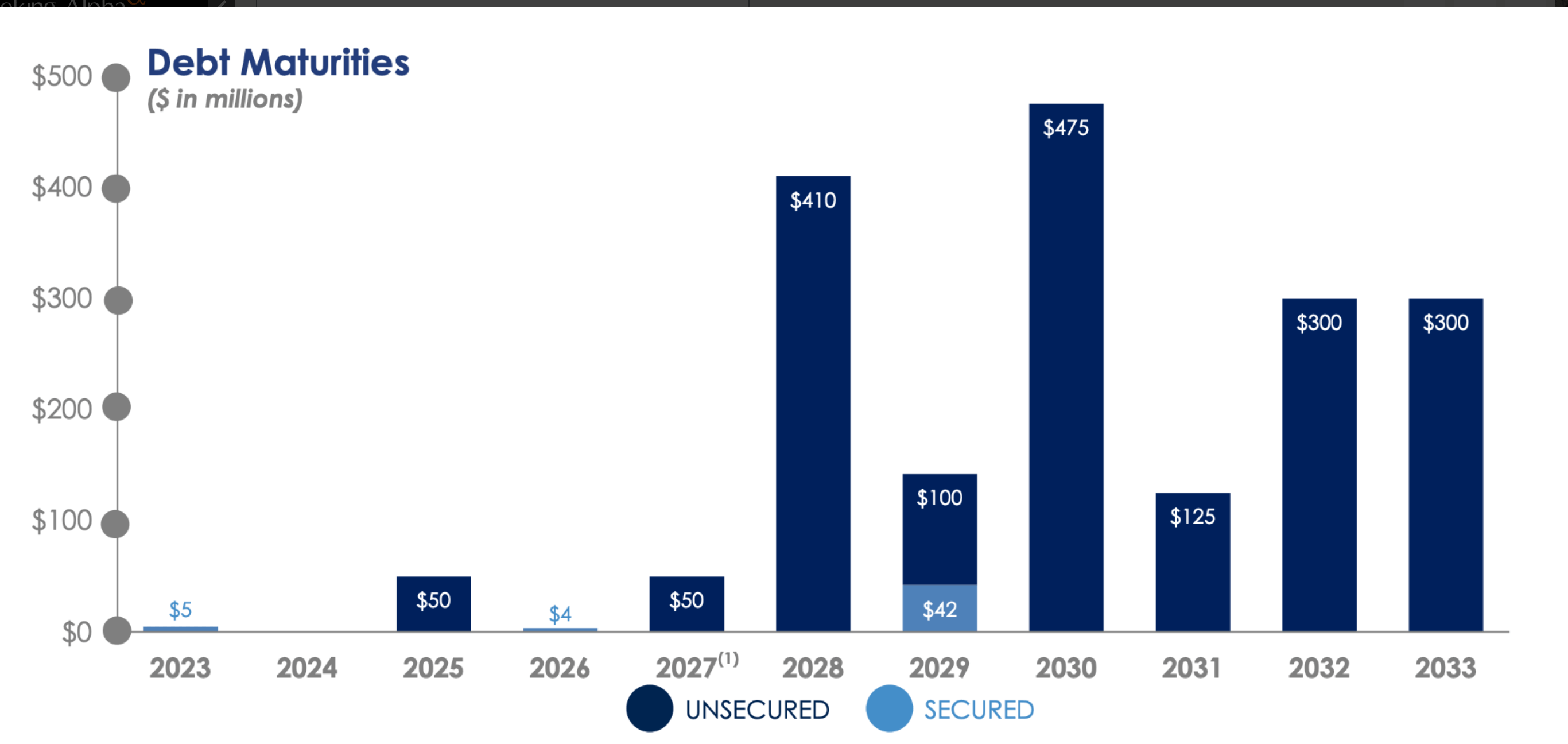

On the balance sheet side, ADC is barely impacted by the surge in rates because it has minimal debt maturities before 2028.

{kind=link}

Therefore, the future growth is highly visible. It can grow by ~3% annually thanks to its lease escalators, and it also retains a significant portion of its cash flow, allowing it to buy additional properties.

The REIT pays a 5% dividend yield, and I expect it to grow by about 5% in the next years as the current payout ratio of 73% is below the low end of management's target of 75-85%.

So without any repricing upside, we can expect roughly 10% annual total returns.

But at $60 per share, ADC trades at an implied cap rate of ~6%, which is a healthy 180 bps spread to the current 10-year treasury yield (US10Y) of 4.2%.

Assuming a 50-100 drop in long-term rates, we would expect ADC's share price to rise by about 25% from here.

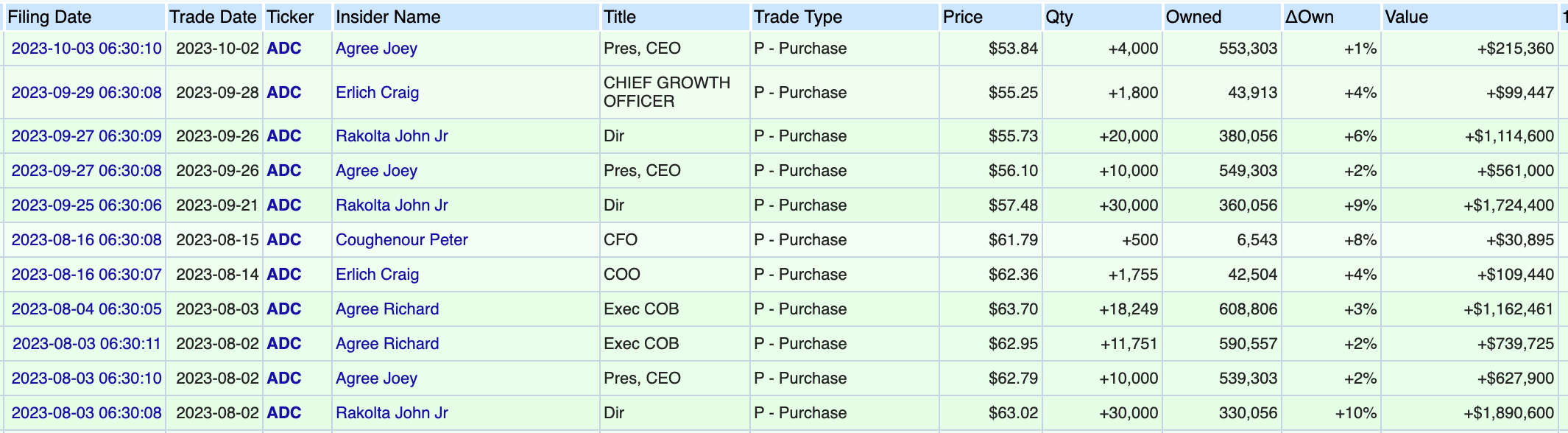

Finally, you should note that insiders have bought over $8 million worth of shares since August of this year:

{kind=link}

VICI Properties Inc. ( VICI )

VICI specializes in casino net lease properties and it is unique in that most of its leases enjoy CPI adjustments. In particular, all of its Caesars Entertainment, Inc. ( CZR ) leases, as well as some Hard Rock and Century leases, have CPI-linked indexation with no caps . These account for over 40% of VICI's total rent.

This is a major advantage in today's uncertain world.

Inflation is now cooling down, but it could again accelerate in the future, and VICI is particularly well protected.

VICI Properties

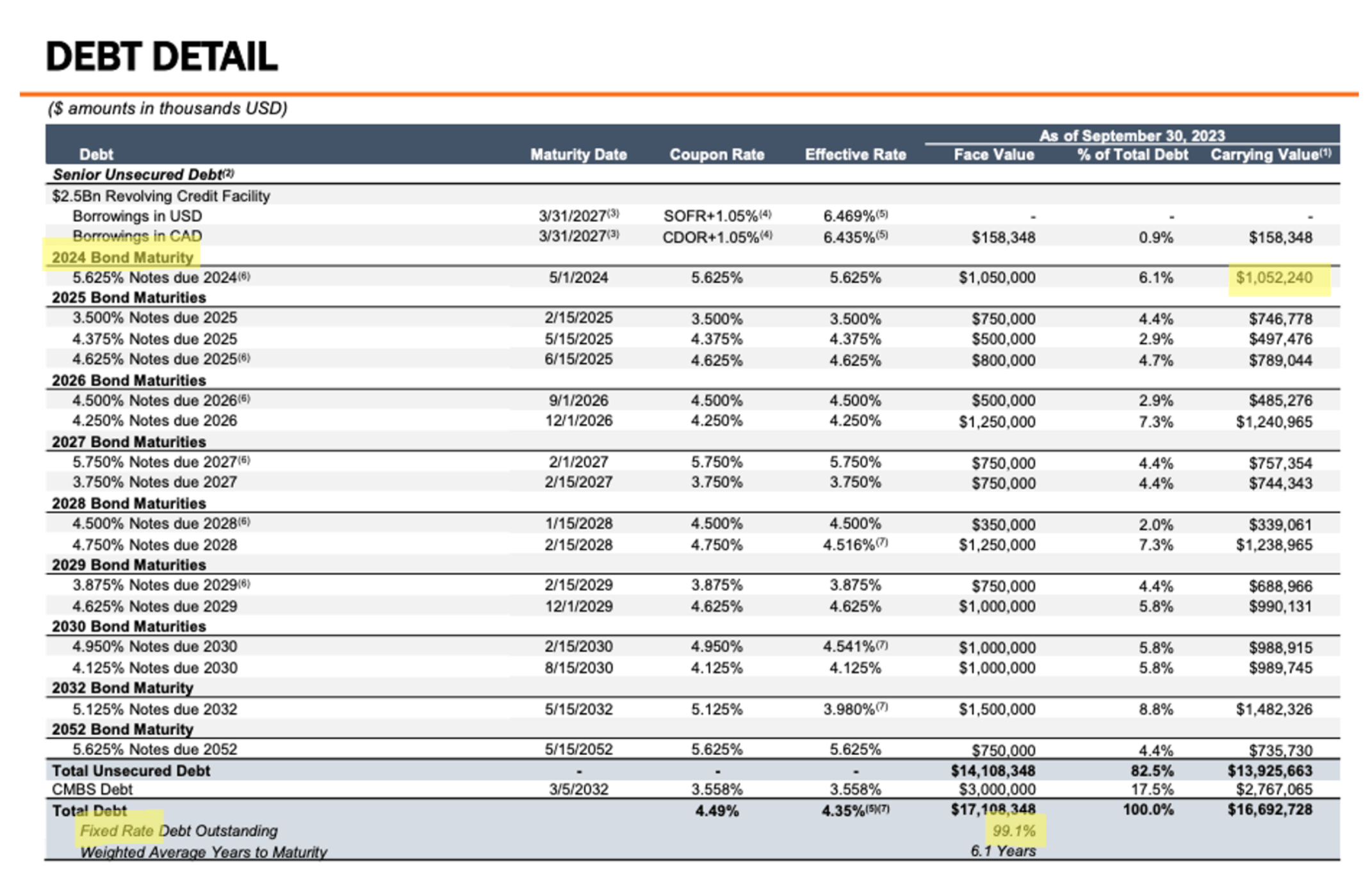

VICI's balance sheet , although more leveraged than ADC's, is also strong and well positioned for a period of high-interest rates. VICI has hedged 99% of its interest rate risk, and near-term debt maturities are very manageable. Next year's refinancing risk has already been partly eased, and even if interest rates stay high until 2025, I estimate that the refinancing of all 2025 maturities at a rate of 6.5% would only have a negative impact of 2% on its adjusted funds from operations, or AFFO.

{kind=link}

Keep in mind that rates will only stay as high as they are today, if inflation stays high. And in that case, VICI will benefit from their CPI-linked indexation, which will more than offset the (potential) interest expense increase. And the same would be true in 2026, 2027, and beyond. In short, high interest rates as a result of high inflation don't appear to be a risk to VICI's cash flow. At all.

But while cash flow is largely unaffected by rates, the same is not true of valuation. VICI currently trades at an implied cap rate of 6.5%, which is 230 bps above 10-year yields. Given VICI's BBB- rating, I'd argue that's a fair spread.

If and when interest rates return to lower levels, we would also expect about 25% upside, but VICI enjoys better protection against inflation.

EPR Properties ( EPR )

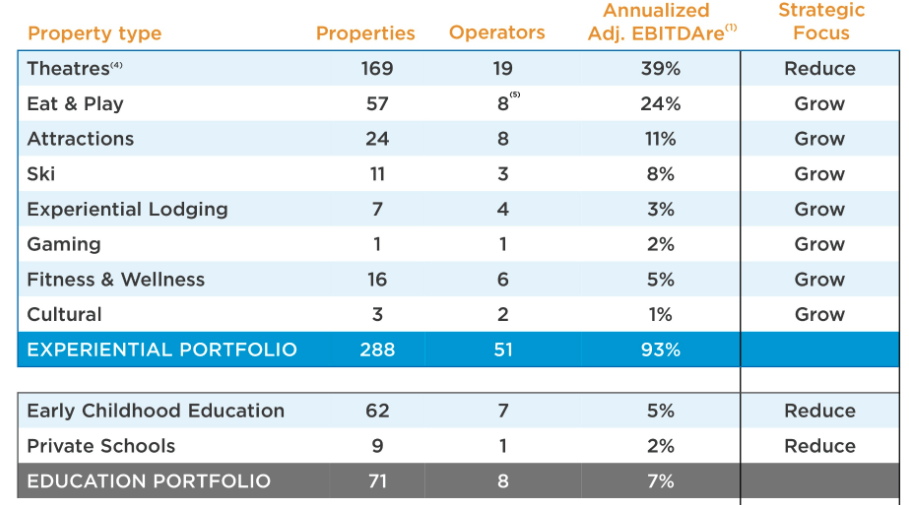

EPR Properties is an experiential REIT with 40% of its portfolio invested in movie theatres, 24% in "eat-and-play" concepts such as Topgolf or go-karting, and the rest is invested in other attractions such as water parks and ski resorts.

EPR Properties

{kind=link}

EPR has sold off significantly due to fears concerning its movie theaters, which suffered significantly during the pandemic.

But I believe the market has overreacted.

Movie theatres have largely recovered from the pandemic, driven by the successful releases of the Barbie and Oppenheimer movies, and their box office is expected to grow by another 24% (to $9 Billion) next year.

Moreover, EPR has recently closed a restructuring agreement with Regal that proved that the cash flows of these properties are durable.

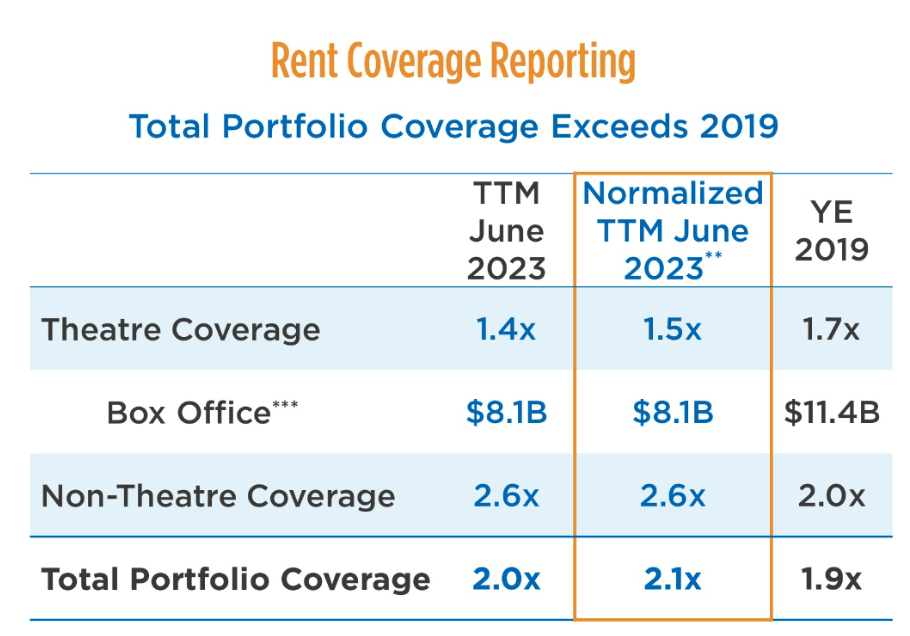

Regal will keep 41 out of 57 properties, which will be placed under a new master lease, and the remaining 16 properties will be sold or released to another tenant by EPR. Under the agreement, the lease term will be extended from 9 to 13 years, and the 41 properties will generate 96% of rent previously paid for the 57 properties. The deal is very positive for EPR.

Adjusting rent coverage for the restructuring agreement, trailing 12-month coverage for movie theatres would be 1.5x, and with box office revenues expected to grow, management expects next year's coverage to return to the pre-pandemic average of 1.6-1.8x.

{kind=link}

That's a very positive development, but the stock price has not reacted to it.

The stock pays a 7.4% dividend yield, which is comfortably covered with a payout ratio of 66%, and trades at a high implied cap rate of 8.4%. That's over a 4% spread to long-term yields.

I believe that as the market realizes that movie theatres are here to stay, the spread will decrease to 2.5-3%. As a result, the stock has 30% upside potential, and that's on top of further upside from a decrease in interest rates.

NewLake Capital Partners, Inc. ( NLCP )

NewLake is a cannabis REIT with a portfolio of cultivation facilities and dispensaries, located primarily in license-limited states.

I think the stock is interesting because:

- It pays a high 12% dividend yield which is well-covered despite some tenant delinquencies,

- the valuation is very cheap with an implied cap rate of 17%,

- the REIT has no debt ,

- the management is shareholder-friendly and heavily buys back stock,

- and there are several potential bullish catalysts for next year.

NewLake Capital Partners

Amongst the biggest potential catalysts is legislation.

There are currently three things worth noting. Firstly, it now seems likely that cannabis will eventually be rescheduled to a Schedule 3 substance. This will significantly lower taxes for operators and consequently benefit NewLake with improved rent coverage for its tenants.

Secondly, the Senate has passed a modified version of the SAFE Banking bill, which should relax banking standards in the cannabis industry. In turn, operators should have easier access to capital, which has been one of the main headwinds for them.

Finally, the cannabis industry has filed a lawsuit to challenge the government's ability to regulate cannabis across state borders. While it's unclear if the lawsuit will be successful or how long it will take to resolve, it could be a major positive step in closing the federal-state legislation gap.

NLCP is riskier than most other REITs, but the stock has over 50% upside potential even without any change to interest rates.

Alexandria Real Estate Equities, Inc. ( ARE )

Finally, ARE is a REIT I've written extensively about.

It focuses exclusively on life science properties, which significantly reduces the threat of work-from-home since this kind of work cannot be done remotely.

Alexandria Real Estate

More importantly, it is very well positioned for a potential higher for longer scenario because of its ability to increase rents and its fortress balance sheet , which ensure stable and growing cash flows.

ARE can grow rents much faster than most REITs, thanks to:

- above average rent escalators of 3%,

- significant 15-20% cash spread on new leases because its rents are deeply below market.

- and a sizeable mostly pre-leased development pipeline.

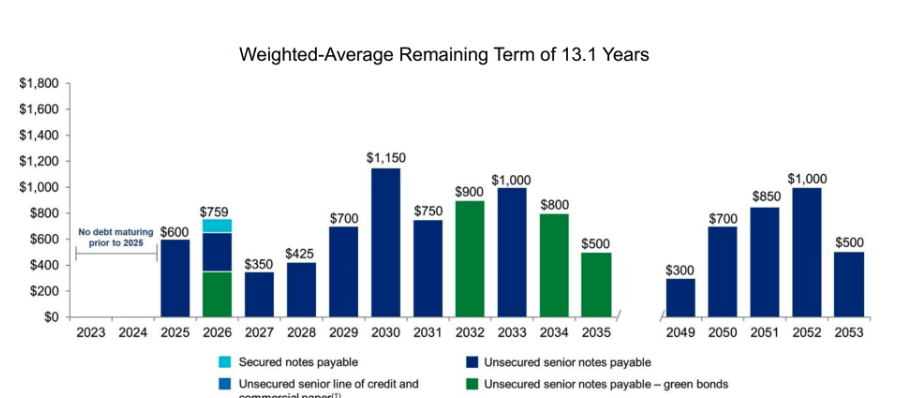

In addition, its balance sheet has:

- 99% of fixed-rate debt,

- an unusually long weighted average debt maturity of 13.1 years,

- and no debt maturities until 2025.

{kind=link}

In short, ARE's forward FFO growth is very visible at around 6% per year. Add to that a 4.1% dividend yield and potential upside (when rates drop) and investors could easily earn 15-20% annual returns over the coming years.

Bottom Line

REIT prices have been low all year, giving investors plenty of time to buy quality REITs at discounted prices.

But as we enter next year, it is quite possible that the Fed will cut rates in the second half of the year and spark a major rally in REITs. And because the market always looks at least 6 months ahead, there may not be much time left. Today, we gave you five examples of REITs that we are buying ahead of this anticipated rally.

Happy Christmas Shopping!

For further details see:

5 REITs To Add To Your Christmas Shopping List