BRSP - 5 REITs With Major Insider Purchases

2023-09-28 08:05:00 ET

Summary

- REITs have crashed and are now opportunistic.

- Insiders are making multi-million-dollar purchases!

- We highlight 5 REITs with major insider buys to consider today.

The real estate investment trust, or REIT, sector ( VNQ ) has declined by over 30% since the beginning of 2022 and this has created a historic opportunity to buy quality real estate at a heavily discounted price.

But the REIT sector is vast, with over 200 different companies to choose from, and the fact that valuations are down across the board doesn’t mean that all REITs are a buy today.

On the contrary, many REITs are quite risky at the moment, mostly because they are over-leveraged, face occupancy issues, or their subsector has fallen out of favor. As an example, recently we have highlighted 5 REITs that are likely to cut their dividends in the near future. These are:

- BrightSpire Capital ( BRSP )

- Blackstone Mortgage Trust ( BXMT )

- Global Net Lease ( GNL )

- Easterly Government Properties ( DEA )

- Sabra Health Care REIT ( SBRA )

Our job as investors is to separate the wheat from the chaff, try to minimize risk, and only invest in quality companies that are likely to perform well over the long run.

We spend a lot of time looking for the best opportunities in the market today, but there is only so much that we can analyze looking from the outside in.

That’s where insider purchases come in.

No one knows a company better than its own management which is why significant insider purchases are a great tool to reinforce a buy thesis or to identify a potential buy candidate.

Today we highlight 5 REITs with significant insider purchases over the past months.

Agree Realty Corporation ( ADC )

Agree Realty is a net lease REIT that's similar to Realty Income ( O ), and we believe that it is one of the safest REITs to add income to your portfolio and to benefit from a potential bull market in real estate, if the right catalysts play out.

In one word, ADC represents safety .

Unlike O, which focuses on smaller $2-5 Million properties leased to fast food restaurants, car washes, and gyms, ADC focuses on big box stores leased to some of the biggest and most well-known retailers on the planet, such as Home Depot ( HD ) or Walmart ( WMT ). This means that the company has one of the highest proportions of investment-grade tenants of all REITs at 68%, which results in perfect rent collections.

Moreover, a high portion of these tenants operates in recession-resilient sectors, such as grocery stores, convenience stores and dollar stores, which together account for over 25% of ABR. Occupancy stands at 99.7% and with less than 10% of leases expiring before 2026, the risk of increased vacancy in minimal.

Agree Realty Corporation

On top of an all-star tenant roster, the REIT is also involved in ground leases which account for about 12% of ABR. I will talk about ground leases in more detail below, but the point is that they generally provide another layer of protection relative to building ownership, because, in case of default, the land owner - ADC - keeps the building free of charge.

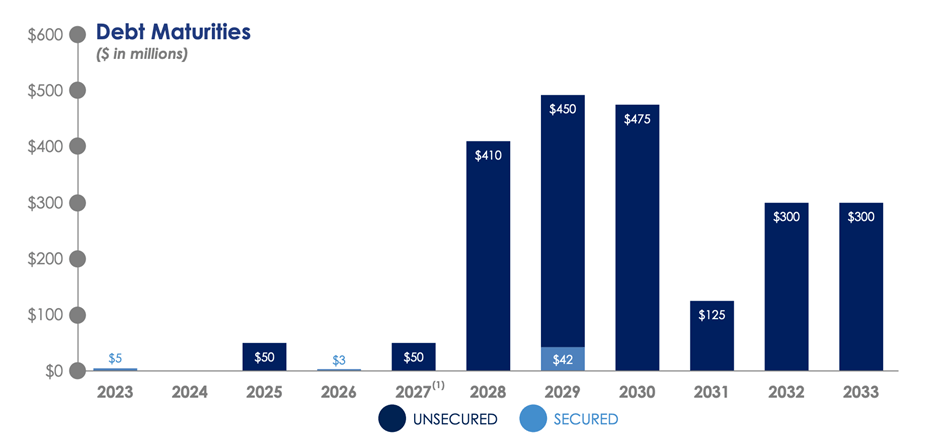

Continuing with the safety theme, Agree Realty has one of the best balance sheets in the sector with a low leverage of 4.1x, no material debt maturities until 2028, and all outstanding debt has a fixed rate.

{kind=link}

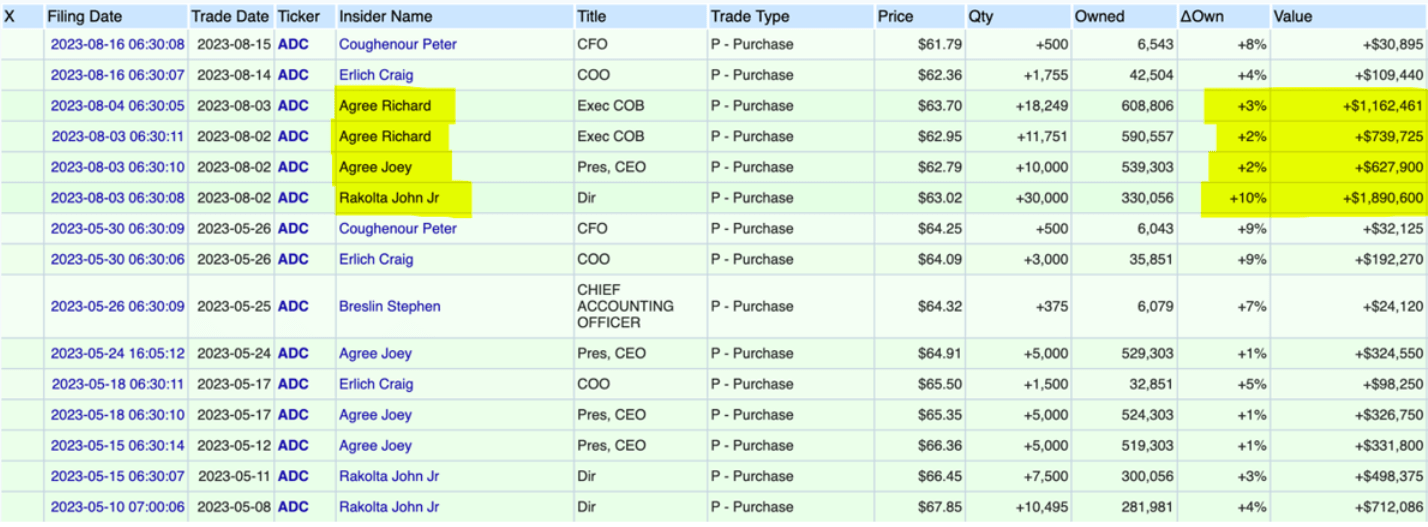

And, of course, the REIT is run by a very competent and shareholder-friendly management team that believes in the future of the company as confirmed by recent multimillion-dollar insider buys.

{kind=link}

The investment case for ADC is compelling. The company pays a 4.7% dividend yield and will likely continue to grow its FFO per share by about 5% per year thanks to its contractual rent increases and acquisitions at cap rates above its cost of capital. Moreover, over the next three to five years, we also expect 25% upside from a re-rating to a multiple that's closer to its historic norm.

All in all, the stock should provide double-digit returns going forward with relatively low risks, and it appears that management agrees.

Safehold Inc. ( SAFE )

Safehold is a one-of-a-kind REIT that focuses exclusively on ground leases.

{kind=link}

Ground leases are pretty simple. The landlord owns the land and leases it to the tenant, usually for a period of 99 years. The tenant then develops the building and makes rent payments to the land owner. If the tenant defaults, the land owner gets to keep the building free of charge.

The structure is a win-win for both sides. The tenant doesn’t have to incur large upfront costs for land acquisition and essentially gets to finance it at reasonable terms. The landlord (SAFE in this case) gets very predictable rental income and no usual risks associated with owning real estate, such as vacancies or maintenance capex.

SAFE’s revenues are very visible. The REIT has an average remaining lease term of 93 years with most rents having 2-3% annual rent escalators and with nearly all tenants investment grade, rent collections are bound to be very good, especially since the tenants would lose valuable buildings if they defaulted.

Their BBB+ rated balance sheet matches the nature of their business by a very long weighted average maturity of 23 years, and except for their revolving credit line, has no maturities until 2031 and all debt is fixed-rate.

So far, you’re probably thinking that SAFE is living up to its name, providing very predictable income by earning the spread between their rent payment and cost of capital.

But every coin has two sides.

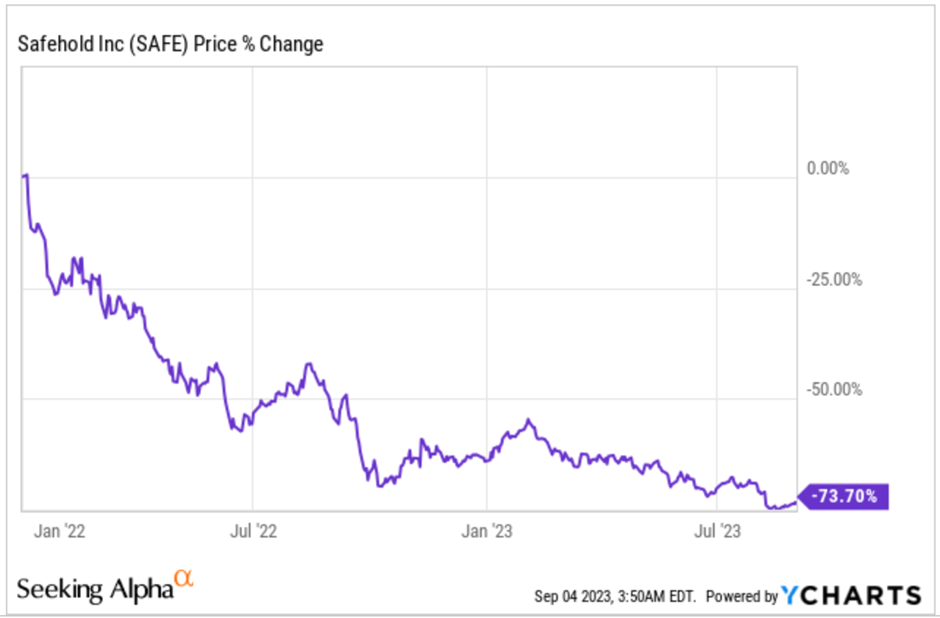

Because they lease to very strong tenants for extremely long lease terms and are set to receive steady rent hikes as well as a building for free when the lease expires, the initial cap rate (yield) that they achieve tends to be low – 3.4% on a cash basis. Such low yield makes the valuation very sensitive to interest rate fluctuations, which is why the stock price plummeted by 70% over the past year and a half.

But volatility works both ways and with interest rates potentially peaking, SAFE can be one of the best ways to benefit from a potential decline in interest rates.

{kind=link}

The CEO, Jay Sugarman, has recently bought $1.4 Million worth of shares, adding 3% to his already large $42 million stake in the company.

{kind=link}

SAFE is riskier than most other REITs in our portfolio, but once interest rates decline, the stock price could easily double or even triple from today’s levels, and it seems that the CEO agrees.

American Assets Trust, Inc. ( AAT )

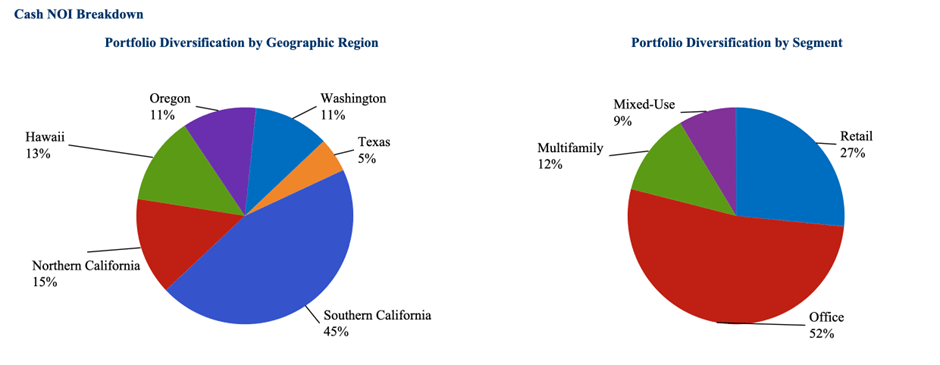

AAT is a lesser-known and relatively small REIT with a market cap of $1.3 billion. The REIT holds a diversified portfolio of offices (52%), strip centers (27%), and apartment communities (12%) located predominantly on the West Coast and in Hawaii.

{kind=link}

Frankly, AAT hasn’t been on our radar, partly because of its smaller size and partly because we have stayed away from the office in this market environment. Recently, however, the CEO of the company Rady Ernest has made a significant $17 Million addition to his $240 million stake in the company, representing the largest recent insider buy of any REIT I know of.

{kind=link}

This made us look closer, and this is what we found.

The REIT’s office portfolio, which accounts for over half of NOI, consists of 12 properties with an average occupancy of 87%.

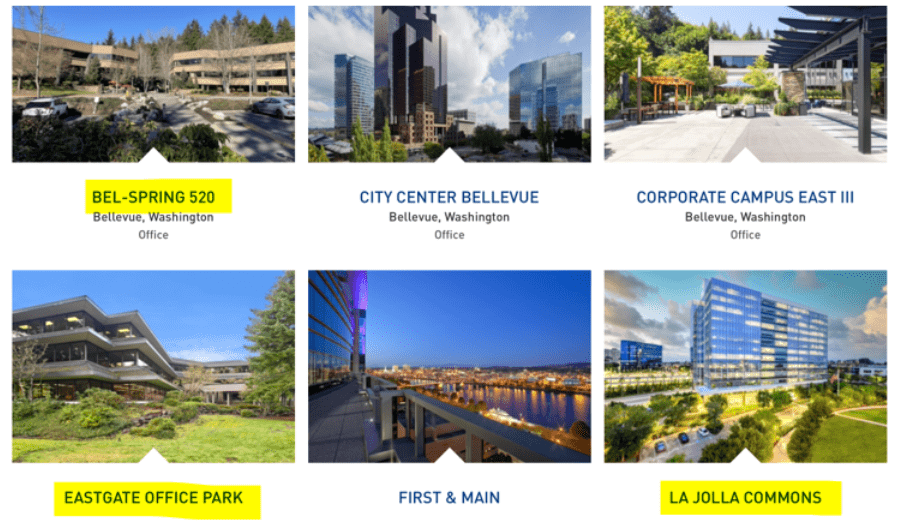

Their properties in California are mostly A-Class (La Jolla Commons), but the Washington and Oregon portfolio consists mainly of B/C-Class properties with occupancy as low as 58% (Bel-Spring 520 and Eastgate office park).

{kind=link}

The retail portfolio, which accounts for another 27% of NOI, comprises another 12 properties that can largely be characterized as strip centers and have an average occupancy of 94%.

{kind=link}

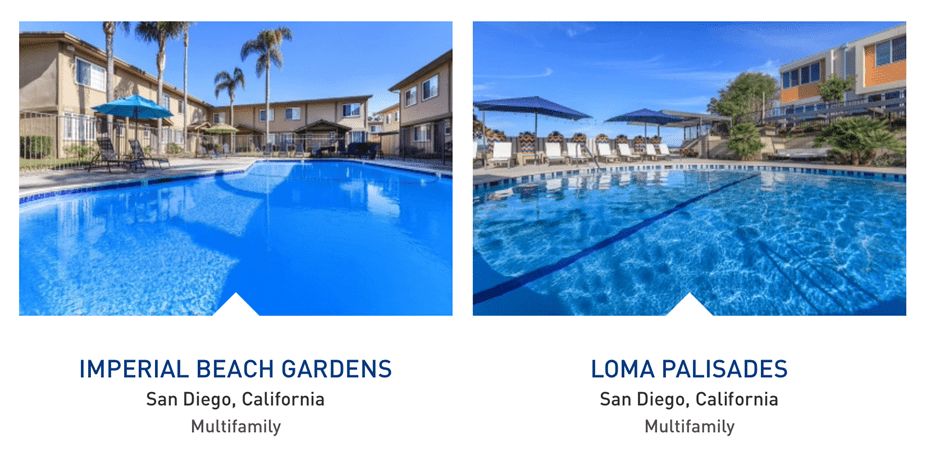

Finally, their 2,100-unit multifamily portfolio has 8 locations and a low average occupancy of 85%. These apartment communities are mostly B-Class and quite old, some were built as early as 1959.

{kind=link}

In summary, their portfolio is quite underwhelming. While most of their retail properties are doing well, they own a significant number of old office and residential properties which are likely to struggle going forward.

To value AAT’s portfolio, it’s best to look at each sector separately. I find the quality of their office portfolio comparable to that of Brandywine Realty Trust ( BDN ) which trades at 4x FFO. The strip mall portfolio is somewhat similar to Whitestone’s ( WSR ) which trades at 10.4x FFO, but because of size and lower quality, I’ll value AAT’s retail at 9.5x. Finally, their multifamily portfolio is quite a bit worse than Essex’s ( ESS ), which trades at 16x FFO, so I’ll use 14x FFO for AAT.

Using the appropriate weights yields a fair P/FFO of (at most) 7x, yet the stock trades at 9.3x FFO.

American Assets Trust

This goes to show that one should not blindly follow insider buys. Mr. Ernest sure has his reason for investing heavily in AAT, but from my perspective, I see better opportunities in the market today and will pass on AAT for now.

Uniti Group Inc. ( UNIT )

Uniti is another REIT where the CEO has made a significant $1 million purchase, increasing his company holding by 20%. This is a clear sign of confidence in the future performance of the stock and is a slap in the face of the bears that have sold the stock on fears of high leverage.

{kind=link}

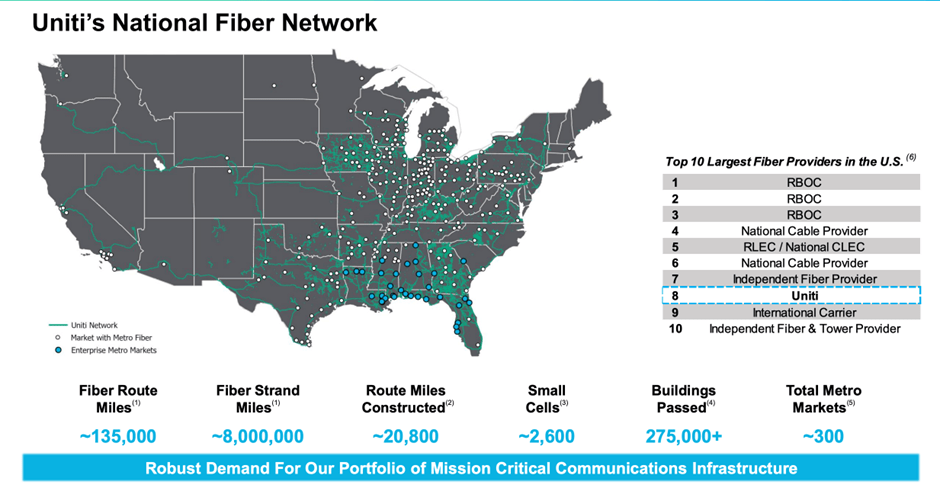

UNIT is a specialized REIT that owns key infrastructure for the telecommunications industry, primarily fiber optic networks.

{kind=link}

It was the first REIT to get involved in the space and has capitalized on its first-mover advantage by already becoming the second biggest independent fiber optic provider in the U.S.

Prioritizing investment and growing their network aggressively has resulted in increased leverage of 6x EBITDA. But the company has now reached a point where the investment is starting to pay off as fiber-optic revenue is expected to increase by 6-8% YoY this year.

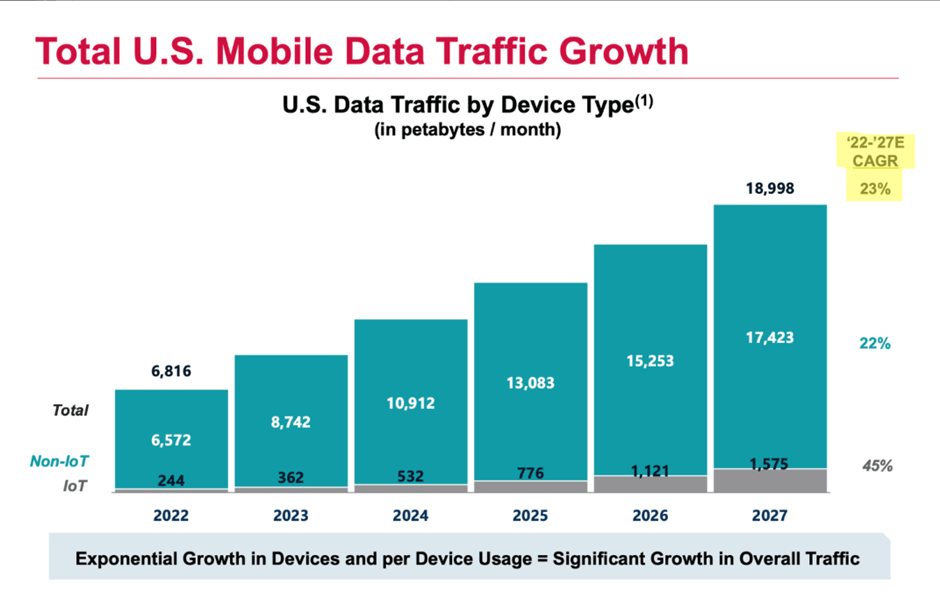

Going forward, data traffic is expected to grow by a CAGR of 23%, and with more data comes more need for optic fiber networks. This makes for a very long growth runway for UNIT and should enable it to capitalize on its investment.

{kind=link}

The company has also refinanced all of its debt due before 2027, addressing a large part of interest rate-related fears, and aims to reduce its leverage to 4-5x EBITDA by 2030 as its investment starts to pay off.

We find the story for Uniti quite compelling, especially because the REIT now trades at a low valuation of just 3.7x FFO, which is only half of its historical average.

The growth in FFO won’t happen overnight, but with a 10% dividend yield and high double-digit upside when interest rates decline, the stock deserves a spot in the REIT portfolio of a higher risk-tolerant investor.

The significant insider purchase only reinforces this view.

Mid-America Apartment Communities, Inc. ( MAA )

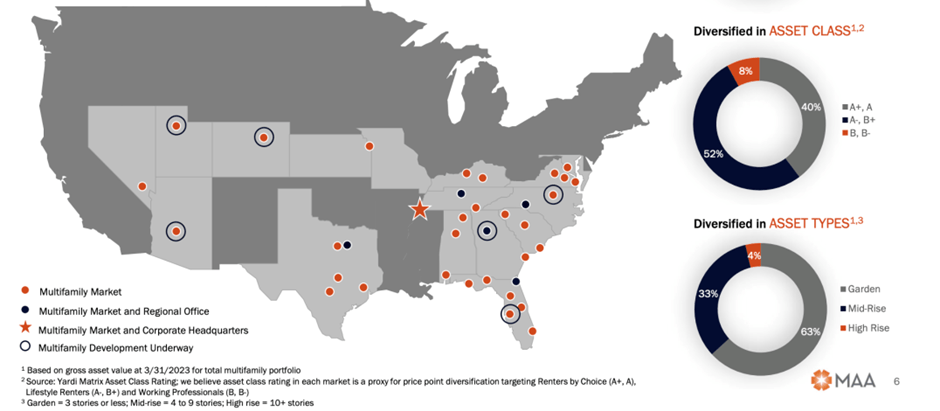

MAA is a major residential REIT that has become very popular amongst investors in recent years because it has no exposure to legacy markets in the Northeast and on the West Coast. If you’re looking for a residential Sunbelt pure-play, this is it. Moreover, the REIT focuses on high-quality A-Class properties that are leased to affluent tenants with rent coverage of nearly 5x.

{kind=link}

There is a lot to like about MAA.

The REIT has been able to grow its NOI by 17% last year and following solid Q2 2023 earnings, management has raised their NOI growth guidance for this year by 5 bps to 6.35% at midpoint. If management delivers, core FFO per share could reach $9.14, which would represent a 7% YoY increase.

The company maintains an A-rated balance sheet with one of the lowest levels of leverage in the sector of only 3.5x EBITDA. Their near-term interest rate exposure is small, with 100% of the debt fixed rate and well-laddered and manageable debt maturities.

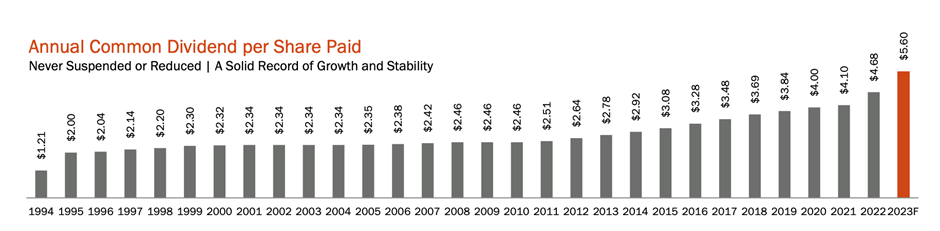

MAA also pays a very reliable dividend, which has never been cut in the 29 history of the company and now yields nearly 4% with a very reasonable forward payout ratio of 61%.

{kind=link}

All things considered, the company has an attractive portfolio a fortress balance sheet , and is doing very well, so it should be expected to trade at a premium valuation.

But at 16.2x FFO, the valuation is more than fair relative to peers such as Camden Property Trust ( CPT ), AvalonBay Communities ( AVB ), or Essex Property Trust ( ESS ), especially if you prefer the Sunbelt over legacy markets.

| REIT |

| P/FFO |

| MAA |

| 16.2x |

| CPT |

| 15.7x |

| AVB |

| 17.6x |

| ESS |

| 16.0x |

And from recent insider buys it appears that management shares the same view, as one of the main directors of the firm has recently purchased nearly $900,000 worth of shares, increasing his stake by 15%.

{kind=link}

One caveat, which may already be priced into the valuation, is that A-Class residential space in some markets in the Sunbelt may come under pressure over the next two years as new supply peaks.

This is part of the reason why we prefer to hold a position in a REIT that specializes in B-Class residential space, which we expect to be much more resilient to oversupply.

Bottom Line

REIT valuations are down across the board. In some cases, the drop in price is justified by deteriorating fundamentals, but then in other cases, it is pure market over-reaction.

Insider buys are a great indication to that and reaffirm our view that REITs are today offering a historic buying opportunity.

For further details see:

5 REITs With Major Insider Purchases