TROW - 5 Stocks In The Dividend Growth Sweet Spot

Summary

- Finding companies with a high initial yield and rapid dividend growth is difficult. I present my criteria for finding such companies.

- At present, there are 16 companies meeting my initial screening requirements. Using additional metrics, these are reduced to five.

- Projecting future dividend growth requires multiple assumptions. Looking at the right factors can make it reduce the risk.

Dividend growth investing is a balancing act. An investor wants as high an initial yield as possible and a quickly growing dividend. And, of course, there is the concern for dividend safety. After all, the point of dividend growth investing is to increase income, and dividend cuts are the fastest way to curtail income growth.

It is easy to find companies that have high yields, and it is easy to find companies that have fast dividend growth, but finding the two together is unusual. A company with a high yield and rapid growth almost always has some serious headwinds. Usually, this means that the dividend growth rate is likely to slow, or possibly even a dividend cut may be in store.

Enterprise Products Partners ( EPD ) and Lowe's ( LOW ) are prime examples of the extremes. EPD typically yields in the 7.5% range but only grows the dividend at around 3%. Meanwhile, Lowe's typically yields sub-2% but has a dividend growth rate of nearly 20%.

T. Rowe Price ( TROW ) is a perfect example of a company that appeared to have both a high yield and a high dividend growth rate. During the past year, TROW could be purchased at a better than 5% initial yield while having a double-digit dividend growth rate. It was clear that something was likely to give, and unsurprisingly the company announced a paltry 1.7% increase for 2023.

All three companies in the above example are dividend champions, with well over 25 years of dividend growth. Using a long growth history as a starting criterion is one of the simplest ways to identify "safe" dividends.

Selection Criteria

When searching for dividend growth companies, I often use a 3%/7% guideline. This means that I want a 3% initial yield and 7% sustained dividend growth. Using the rule of 72, we know that 7% dividend growth equates to doubling the dividend approximately every ten years (72/7). The 3% initial yield is a reasonable target expectation, and if an investor reinvests dividends at a 3% initial yield, the combined income growth (3%+7%) equates to doubling the income every seven years.

The second piece of my initial search is years of dividend growth. While past performance is no guarantee of future success, it shows a commitment to the dividend and the ability to grow through various challenges. I generally like to see at least 12 years of dividend growth, but I strive for longer.

Here is a list of my full selection criteria:

- Approximately 3% initial yield and 7% dividend growth (1-yr, 3-yr, 5-yr, and 10-yr)

- At least 12 years of dividend growth

- Low cyclicality / Steady adjusted earnings

- Flat(ish) payout ratios

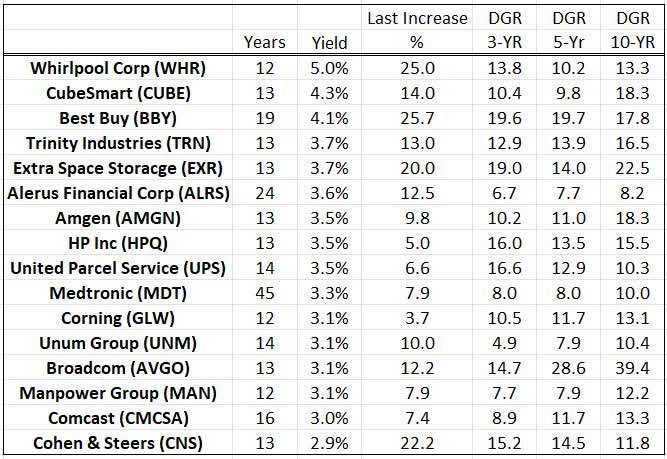

I like to use the Dividend Champions (Champions, Contenders, and Challengers) list for my initial research. I exclude regional banks for the most part from my research. Currently, many regional banks are meeting my initial screen and are omitted here. Additionally, I exclude utilities as I see them as massively overvalued at this time. Presently only 16 companies are meeting the initial screen on yield and dividend growth, as shown below.

Assembled by Wyo Investments data from a variety of sources

{kind=link}

However, the list dwindles rapidly when I exclude companies with obvious headwinds, like Medtronic ( MDT ) and Best Buy ( BBY ), and then apply the rest of my criteria. Both the REITS, CubeSmart ( CUBE ), and Extra Space Storage ( EXR ), cut their dividends during the 2008-2009 recession, so they have been cut from final consideration.

All companies meeting the initial screen have shown a significant ability to grow the dividend rapidly for over a decade. Many are solid companies and will continue to grow their dividend well into the future. Those failing to make the final cut should be given extra consideration and may entail more risk going forward.

Steady Earnings

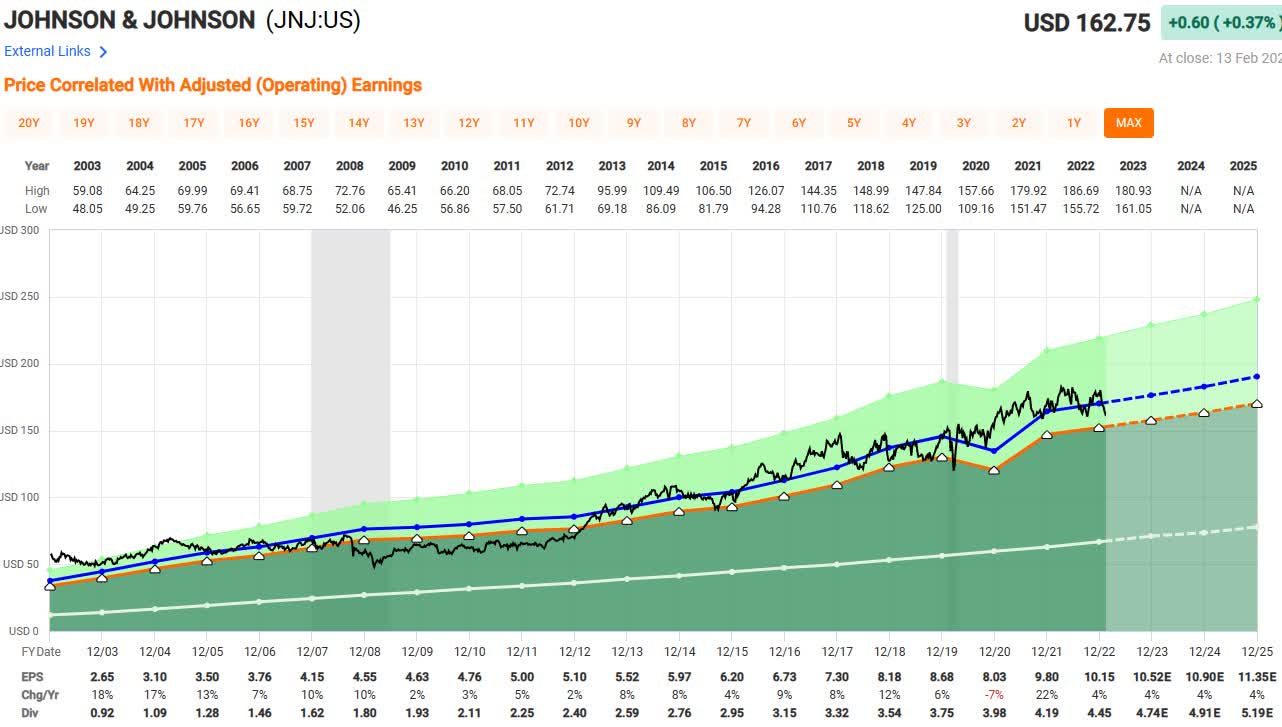

If you look at the earnings for most of the dividend champions, companies with at least 25 years of dividend growth, you will see they have one thing in common; They are generally consistently growing. In the Fastgraph below, you can see from the dark green area that the earnings per share ((EPS)) for Johnson & Johnson ( JNJ ) has grown consistently over the past twenty years and is projected to continue.

{kind=link}

While JNJ has had the occasional down year, the swings are mild and quickly recovered. I chose JNJ as it is the prototypical safe dividend growth company. However, if you look at the charts of nearly all top dividend growth companies, you will see this same pattern.

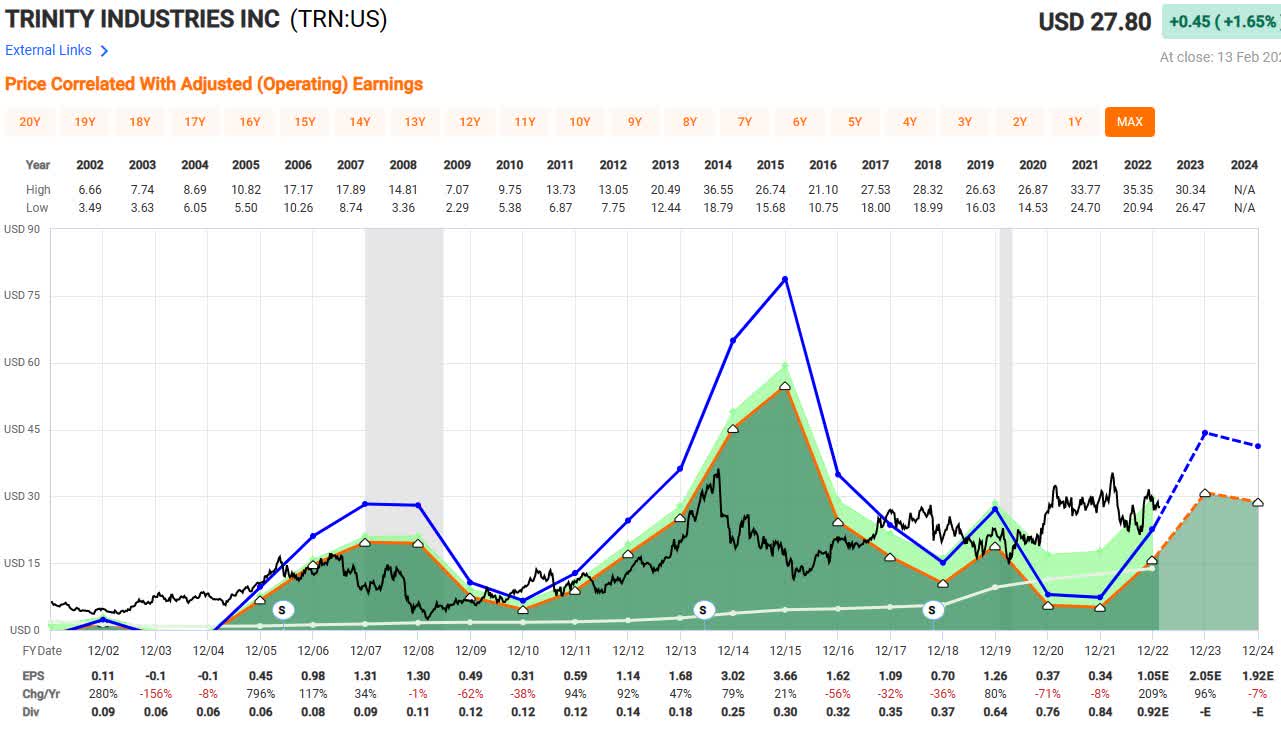

Contrast the JNJ graph to that of Trinity Industries ( TRN ), shown below. Trinity is a dividend contender with 13 years of growth and has consistently grown the dividend in the low double digits. However, very few companies make it to 25 years of dividend growth with highly cyclical earnings. The odds are not in Trinity's favor of becoming a dividend champion one day.

{kind=link}

Low Cyclicality

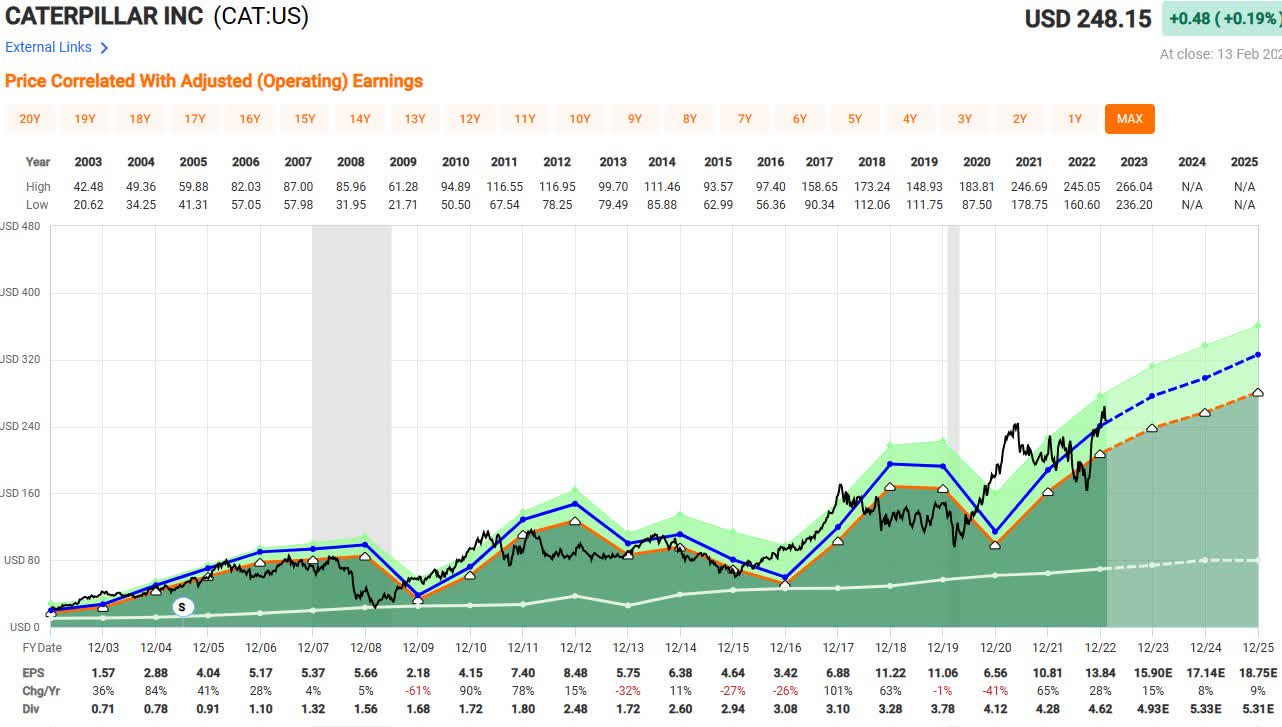

There are a few companies that do become dividend champions while operating in cyclical industries. It takes good management to maintain a streak through the down cycle. The poster child for such a company is Caterpillar ( CAT ). CAT has a 29-year dividend growth streak, consistently increasing the dividend by about 8% annually over the past ten years.

{kind=link}

Companies in highly cyclical businesses can achieve very long dividend growth streaks. However, they are hardly the sleep-well-at-night stocks that make dividend growth investing simple. That doesn't mean they should be avoided entirely, but they require more work, and timing is important when buying them.

Below is a Fastgraph of ManpowerGroup ( MAN ). Notice the extreme fluctuations during recessions. Given its being in the people-for-hire business, any economic downturn will likely hit the company hard.

{kind=link}

Flat Payout Ratios

The last criterion to consider is the payout ratio. While the overall payout ratio can help determine a dividend's safety, the rate of change is of equal importance when considering a company for its dividend growth potential.

A company that has grown the dividend by 10% annually over the past ten years while keeping a flat payout ratio is in a much stronger position than a company that doubled the payout ratio over the same period. Once a company has expanded the payout ratio, they rarely reduce it. Additionally, if the dividend was grown by significantly expanding the payout ratio, it is unlikely that the company will be able to duplicate the dividend growth rate in the future.

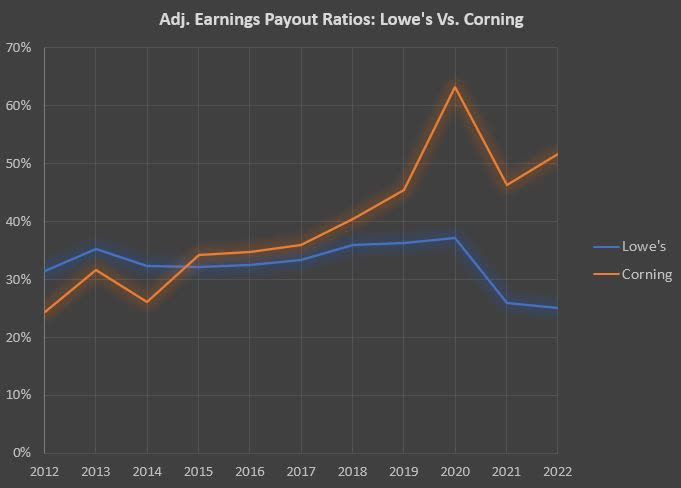

Lowe's has a ten-year dividend growth rate of over 20%. Since 2010, the adjusted earnings payout ratio has stayed flat at 29%. This indicates that the company was able to grow the dividend through earnings. Having a low ratio and primarily using earnings to grow the dividend allows the company flexibility during lean years, increasing it slightly as needed and then reducing it as earnings catch up. This is shown in the chart below.

One of the companies making the initial cut at 3% yield and 10% growth is Corning ( GLW ). It has a ten-year dividend growth rate of 13%. However, since 2012, the payout ratio has grown from the mid-20% to over 50%. While the dividend isn't at risk, the growth rate will likely not continue at such a rapid clip and will probably move in line with earnings in the future. A chart contrasting the payout ratio histories of Lowe's and Corning is shown below.

Wyo Investments with data from fastgraphs.com

{kind=link}

The Final Cut

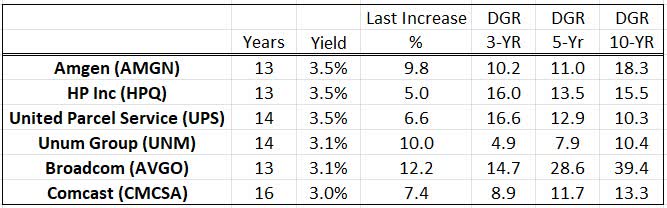

The list below shows the six companies that made the final cut. Except for Comcast and Broadcom, all of these companies have some flaws based on my criteria. Some degree of cyclicality in earnings and payout ratio creep has to be accepted. As a whole, however, most of these companies have a good chance of maintaining a 7% dividend growth rate well into the future.

Assembled by Wyo Investments data from a variety of sources

{kind=link}

Unum Group ( UNM )

Unum Group has doubled its payout ratio over the last ten years, but it is still at a low 20%. However, the payout ratio is now primarily in line with its peers, so it will likely not expand much going forward.

Over the next five years, earnings estimates for UNUM are between 5% and 9%, indicating that even without expanding the payout ratio further, the company is likely to maintain 7% dividend growth.

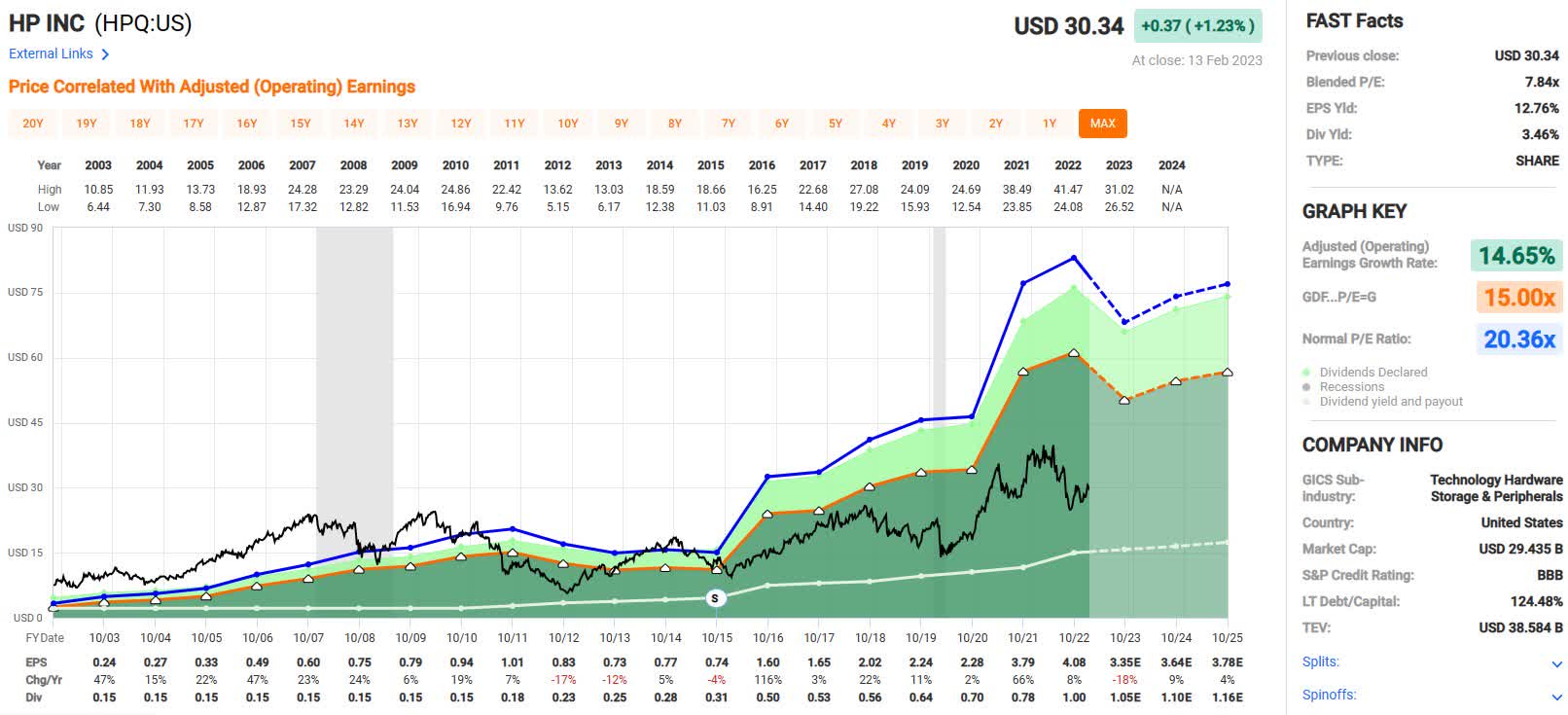

HP Inc. ( HPQ )

HP Inc often comes up on screens, but I find it difficult to get excited about it. The earnings aren't super cyclical like a Whirlpool ( WHR ), but it doesn't have the steady earnings growth that many dividend champions do. This is shown in the Fastgraph below.

{kind=link}

While HPQ has had incredible dividend growth and sports a low-to-falling payout ratio, it has abysmal earnings growth projections. Over the next five years, analysts are only looking for very low single-digit earnings growth or, in some cases, even shrinking earnings. While the company has a low enough payout ratio to continue growing the dividend, it's hard to imagine a sustained 7% growth rate in the near term without expanding the payout ratio.

United Parcel Service ( UPS )

UPS currently yields solidly above 3% and has a ten-year dividend growth rate above 10%. In fact, its dividend growth rates are accelerating, but this is primarily due to the 50% increase in 2022. This year's increase came in at 6.6%.

The company has maintained a steady 50% payout ratio throughout the past decade. This will likely be tested in the next year or two, as UPS does experience some cyclicality during economic slowdowns. During the Great Recession, UPS did freeze the dividend for a year. However, we will unlikely see such a severe recession this time.

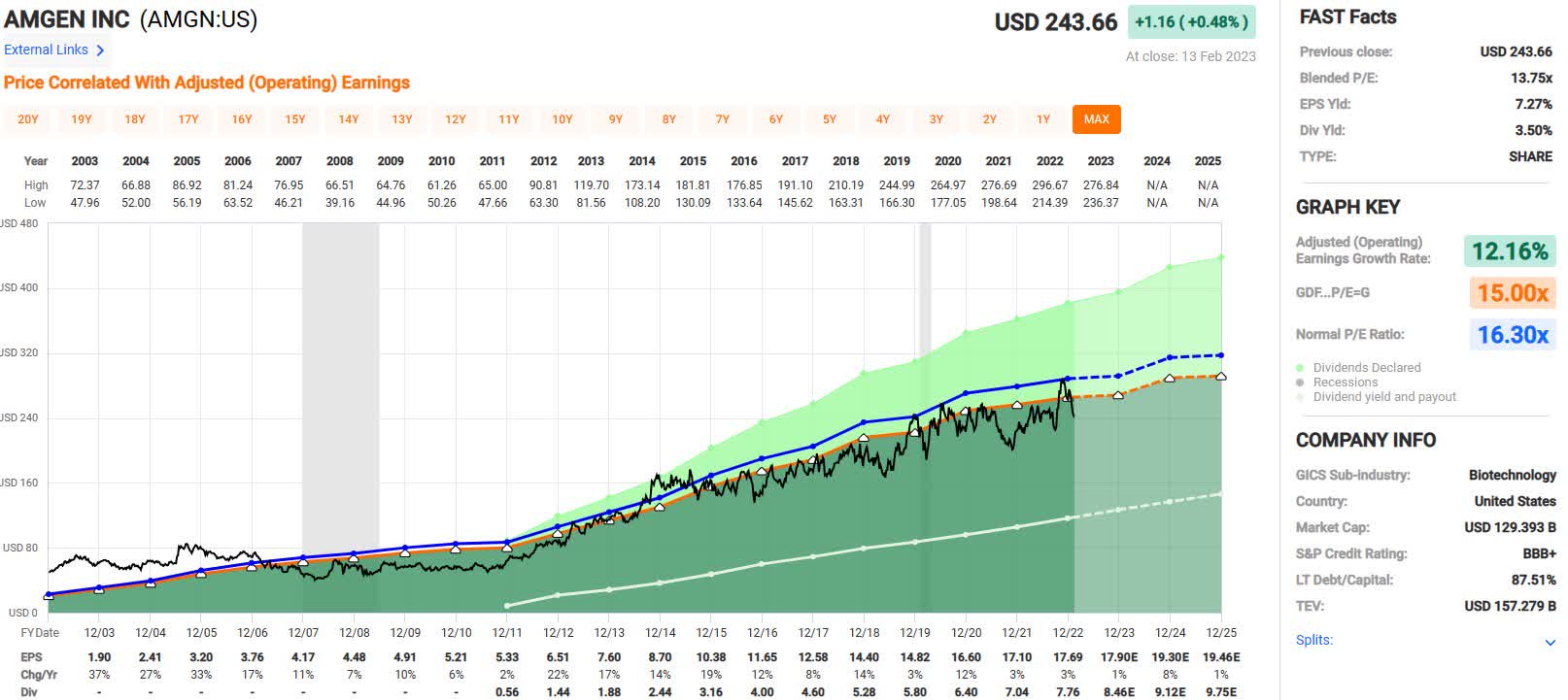

Amgen ( AMGN )

The fastgraph below shows how incredibly steady Amgen's earnings have been over the past twenty years. Not a single negative year. The company regularly comes in with dividend increases above 10%, with this year's at 9.8%. The biggest concern I have is with their payout ratio growth.

{kind=link}

It's hard to evaluate the first few years of a company initiating a dividend because it is often ramped up quickly. Amgen started the dividend in 2011 and ramped the payout ratio to the mid-30% range by 2016. Today the ratio is in the low 40%. The rate of change has slowed, but it is still growing. Their incredibly consistent earnings growth has earned them a pass for now. However, the 5-year growth forecasts range from 0-7% per year. It may be possible the company will be unable to maintain the 7% dividend growth in the future.

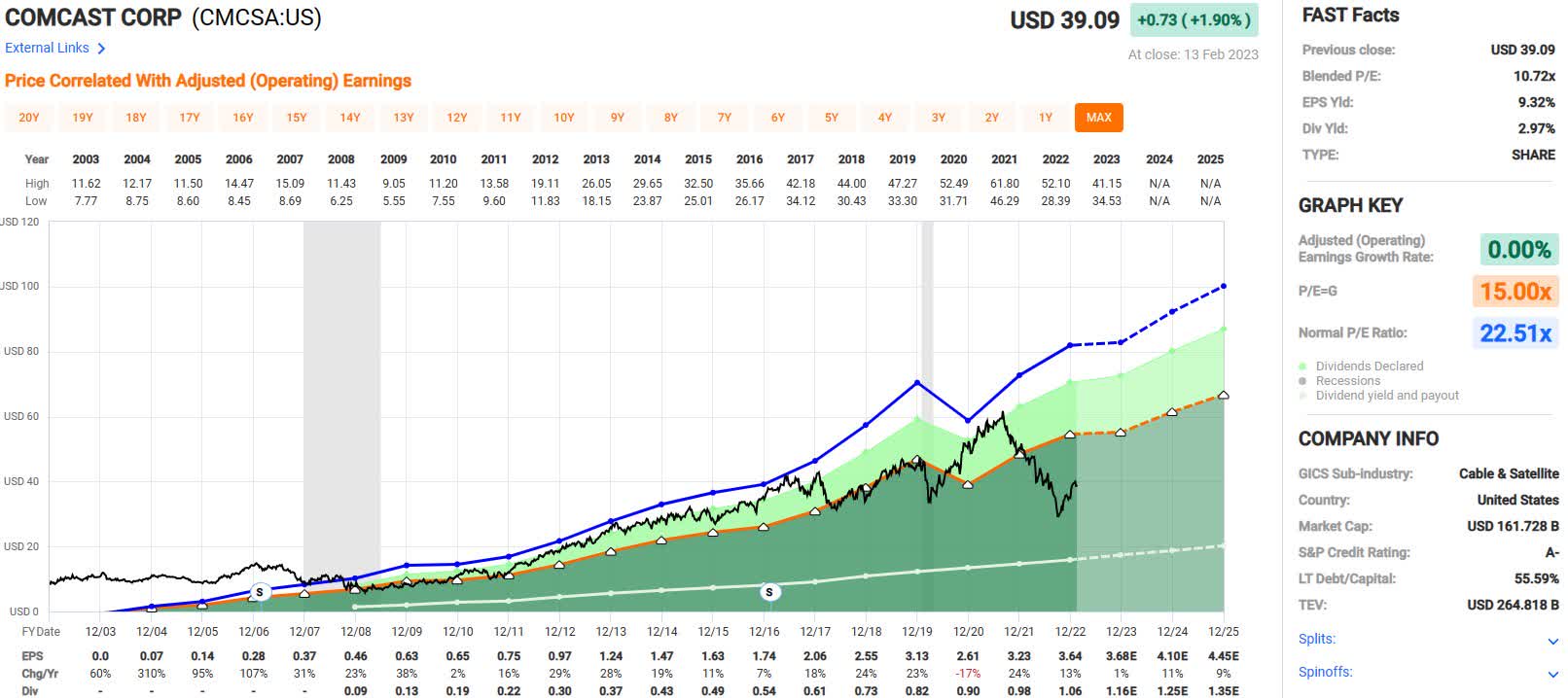

Comcast ( CMCSA )

Comcast has had a payout ratio of about 30% for over a decade. During this time, they have a ten-year dividend growth rate of 13%. However, this has been falling. The most recent increase announced in January was 7.4%. Comcast looks well-positioned to continue providing 7% raises into the future.

The fastgraph below shows Comcast's remarkable consistency in earnings. With the only blip being in 2020. There is no doubt that they are in an industry that's hard to like, and any number of concerns exist. However, long-term EPS growth is still estimated in the 5-9% range, and the company generates an abundance of cash.

{kind=link}

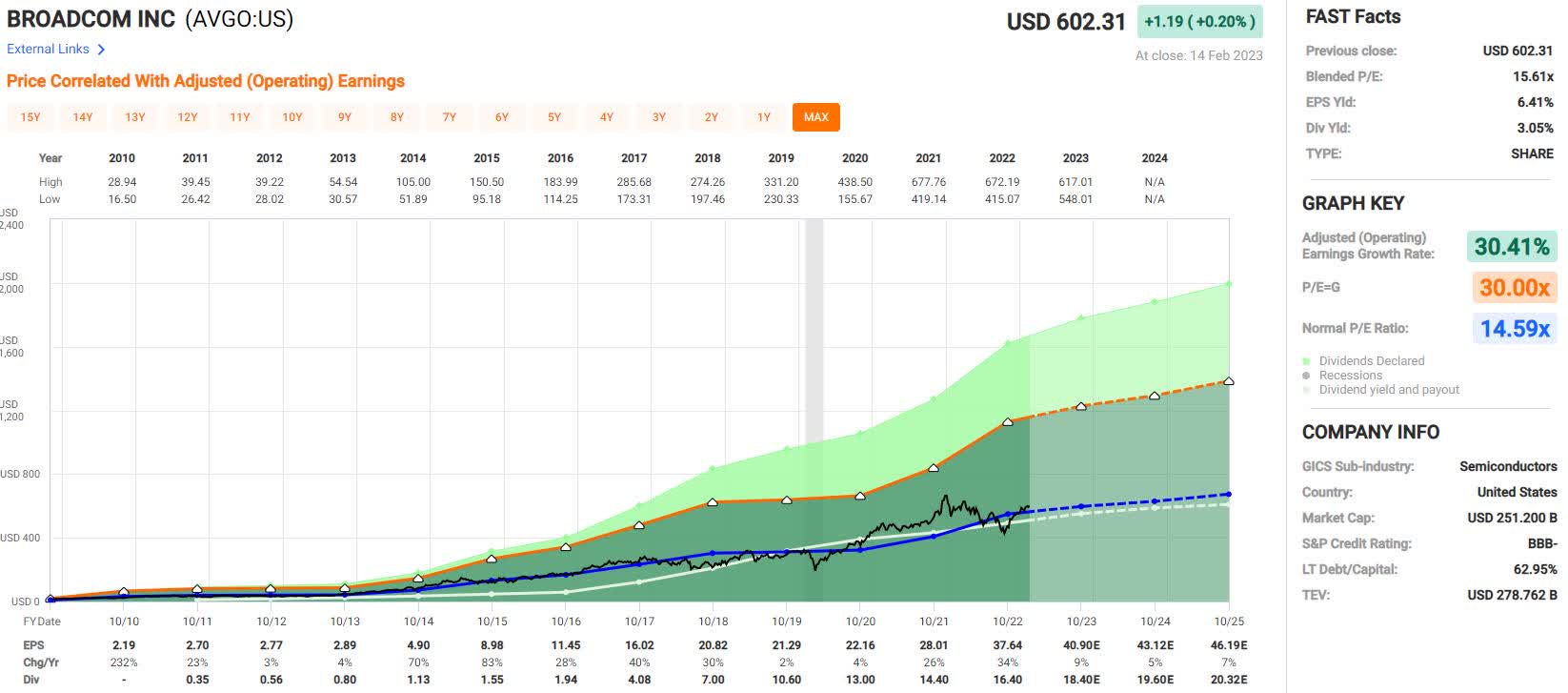

Broadcom ( AVGO )

It's hard to find anything not to like about Broadcom. The biggest knock on them in the screening process is the change in the payout ratio. They get a pass here because they had a significant shift in dividend policy which has since stabilized. From 2016 to 2019, they increased the dividend by more than five times. This rapid dividend growth took the payout ratio from 16% to over 50%. However, they appear to have stabilized the ratio around the 50% mark.

While investors shouldn't expect such massive dividend growth in the future, the company should be able to achieve the desired 7% dividend growth. While the fastgraph below doesn't show much cyclicality in the earnings, some should be expected, given the industry-however, long-range forecasts for Broadcom's growth range from 7-15% per year.

{kind=link}

Final Note on Dividend Growth

There are three things a dividend growth investor should consider in a company: The initial yield, the dividend safety, and the dividend growth rate. Initial yield is a hard fact. Dividend safety in the near term is relatively easy to determine. However, diving into projecting dividend growth is another story altogether.

There are many variables and assumptions that come into play when projecting dividend growth. The only hard facts with dividend growth that I stick to are that payout ratios can't increase indefinitely, EPS needs to grow to continue growing the dividend, and dividends are paid out of cash flow.

For further details see:

5 Stocks In The Dividend Growth Sweet Spot