PSX - 60% Gains Plus Dividends With Phillips 66 If Elliott Is Right

2023-12-05 14:43:27 ET

Summary

- Activist investor Elliott Investment Management enters Phillips 66 with a $1 billion stake and proposes a strategic overhaul.

- Elliott identifies underperformance and operational lapses as key issues and calls for cost-cutting, divestitures, and a commitment to shareholder value.

- Phillips 66 responds positively to Elliott's proposals, indicating a promising future for the company.

Introduction

On November 20, I wrote an article titled 3.6% Yield And Undervalued - Phillips 66 Is A Top-Tier Income Play . As that wasn't very long ago, I wasn't planning on writing another article.

However, sometimes major changes require a closer look, especially when it comes to major activist investors that could reshape the future of a company.

In my November article, I discussed a number of key issues, including the company's focus on chemicals, its massive refining footprint with benefits like flexible feedstock, its focus on shareholder distributions, and efforts to streamline the business.

Since then, Phillips 66 ( PSX ) has risen by 9%, beating the market by roughly 850 basis points.

As one can imagine, I'm not the only one monitoring these developments, especially as the company has significantly underperformed its pure-play refining peers over the past few years.

On November 29, Elliot Investment Management wrote an open letter to the board of Phillips to show shareholders what the company is doing wrong, how it can improve its business, and why this can result in 75% capital gains for shareholders (60% after its recent surge).

{kind=link}

Bloomberg

In this article, I'll walk you through that letter and explain what this means for existing and potential future Phillips 66 investors.

So, let's get to it!

What's Elliott?

Established in 1977, Elliott Investment Management is one of the world's largest activist funds in the world.

Founded by star investor Paul Singer, the fund started to pursue distressed debt, and going after issuers through court battles of debt was left unpaid.

Currently, it is a business that gets involved with corporations if it sees hidden value. They have a particular focus on technology, financial services, and energy.

The firm takes equity-oriented positions in several of its strategies , and takes on such positions in a variety of forms. It is less common for the firm to take on long equity positions which are just driven by valuation considerations. Elliott seeks out positions in particular which are uncorrelated with other positions in the portfolio or with the risks and expected price movements of equities generally, or where value and protection against risk can be enhanced by the firm’s manual efforts . - Elliott Investment Management (emphasis added)

As I had the privilege of working with people who applied a similar strategy in the past (on a much smaller level), I have always been impressed by the impact some funds can have on companies - especially when they unlock equity value without hurting a company's long-term position.

After all, it is possible to increase short-term shareholder value while wrecking a company's survival chances.

That's not the case at Phillips 66.

There's Tremendous Value In Phillips 66

Phillips 66 is Elliott's new target. The company has revealed a $1 billion stake in the company, which would make it a top seven investor, according to my data.

As I already briefly mentioned, on November 29, the company wrote a letter to the board of Phillips 66, explaining its dissatisfaction with the current state of the company.

In this article, I will share a few quotes from the letter, which can be accessed here: Elliott's letter to Phillips 66 .

As we have explained in our discussions with CEO Mark Lashier and the executive leadership team over the past several weeks, we are investors in Phillips 66 today because of our strong confidence in the path to realizing significant value-creation at the Company.

Essentially, Phillips 66 was off to a great start when it spun off from ConocoPhillips ( COP ), one of the world's largest upstream energy companies.

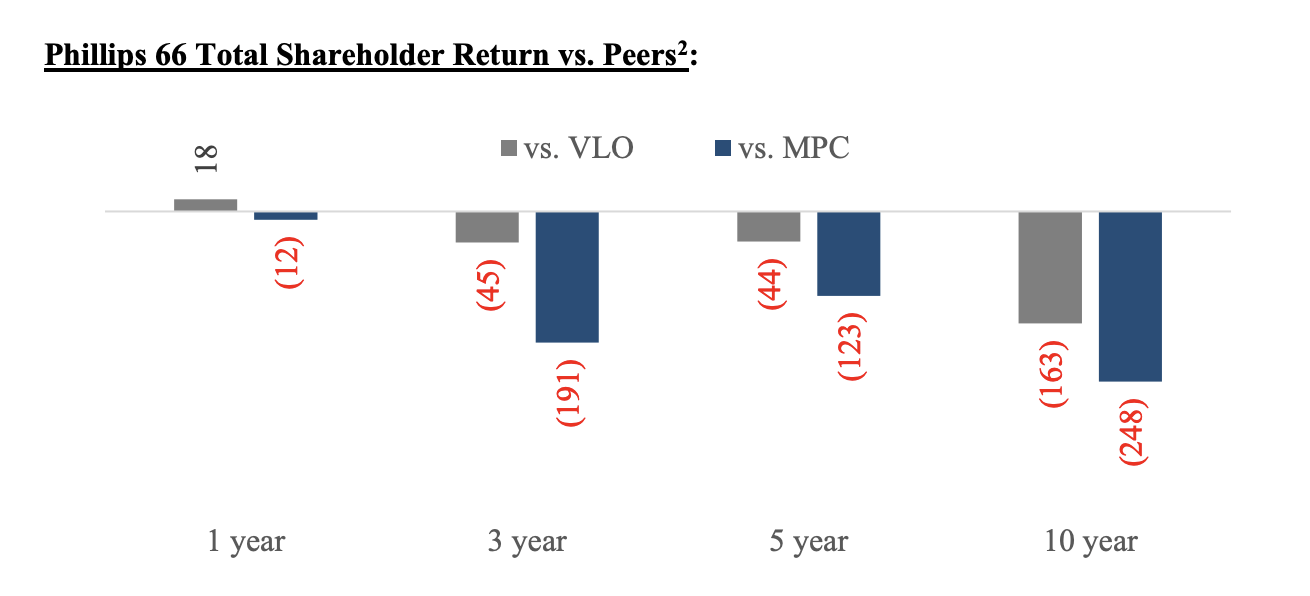

Unfortunately, in recent years, PSX has turned into a significant underperformer, as its pure-play peers Valero Energy ( VLO ) and Marathon Petroleum ( MPC ) benefited from the refinery super-cycle when post-pandemic supply was constrained while demand came roaring back.

As both VLO and MPC were printing money, PSX lagged behind, admitting earlier this year that "We have taken our eye off the ball a little bit with respect to refining." That's a quote from the Elliott letter, which also contained the following chart:

{kind=link}

Elliott Financial Management

Basically, Elliott believes that the loss of confidence is based on two drivers:

- The company's underperforming stock price.

- Its poor execution when it comes to cost-reduction efforts isn't helping either. After all, when costs are an issue, we can assume that the company will continue to underperform more efficient peers.

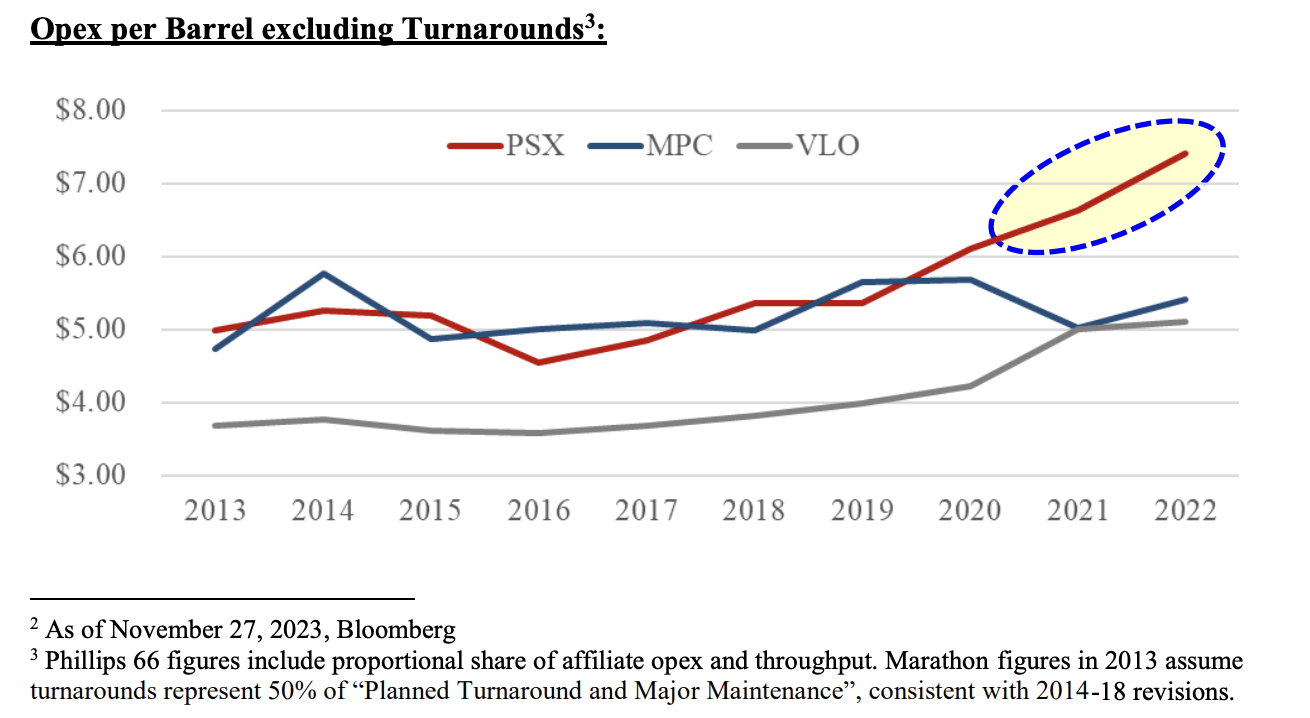

As we can see below, the company has increasingly struggled with rising costs. Its refining operating expenses per barrel have shown a significant divergence compared to its peers starting slightly before the pandemic.

{kind=link}

Elliott Financial Management

Elliott believes that the lack of discipline in operational expenses is a key factor contributing to Phillips 66's stock underperformance.

Furthermore, the AdvantEdge66 program, initiated in 2019 to reduce costs, resulted in disappointment as Phillips 66 witnessed cost increases relative to peers.

This lack of success has led to investor skepticism and a crucial need for the company to regain trust in its cost-cutting abilities.

[…] in 2019, you laid out a similar cost-cutting program, and it actually looks like costs increased over that period on an absolute basis, stripping out energy and maintenance costs on a per unit – on a per barrel basis and relative to peers. So to instill some confidence maybe in this program that you're about to embark on, can you discuss maybe what went wrong in that 2019 to 2022 program and how you expect to maybe not incur those same issues?” – Cowen, November 2022 (Via Elliott)

In light of these challenges, Elliott sees opportunities.

For example:

- It believes in the company's $14 billion mid-cycle EBITDA target by 2025, with more than $1 billion in improvements from the refining segment via both operating cost and commercial improvements.

- The company is selling $3 billion of non-core assets.

- The company is increasing its long-term capital return policy.

The first part was also discussed in my prior article when I highlighted the company's focus (and success) on raising its EBITDA outlook.

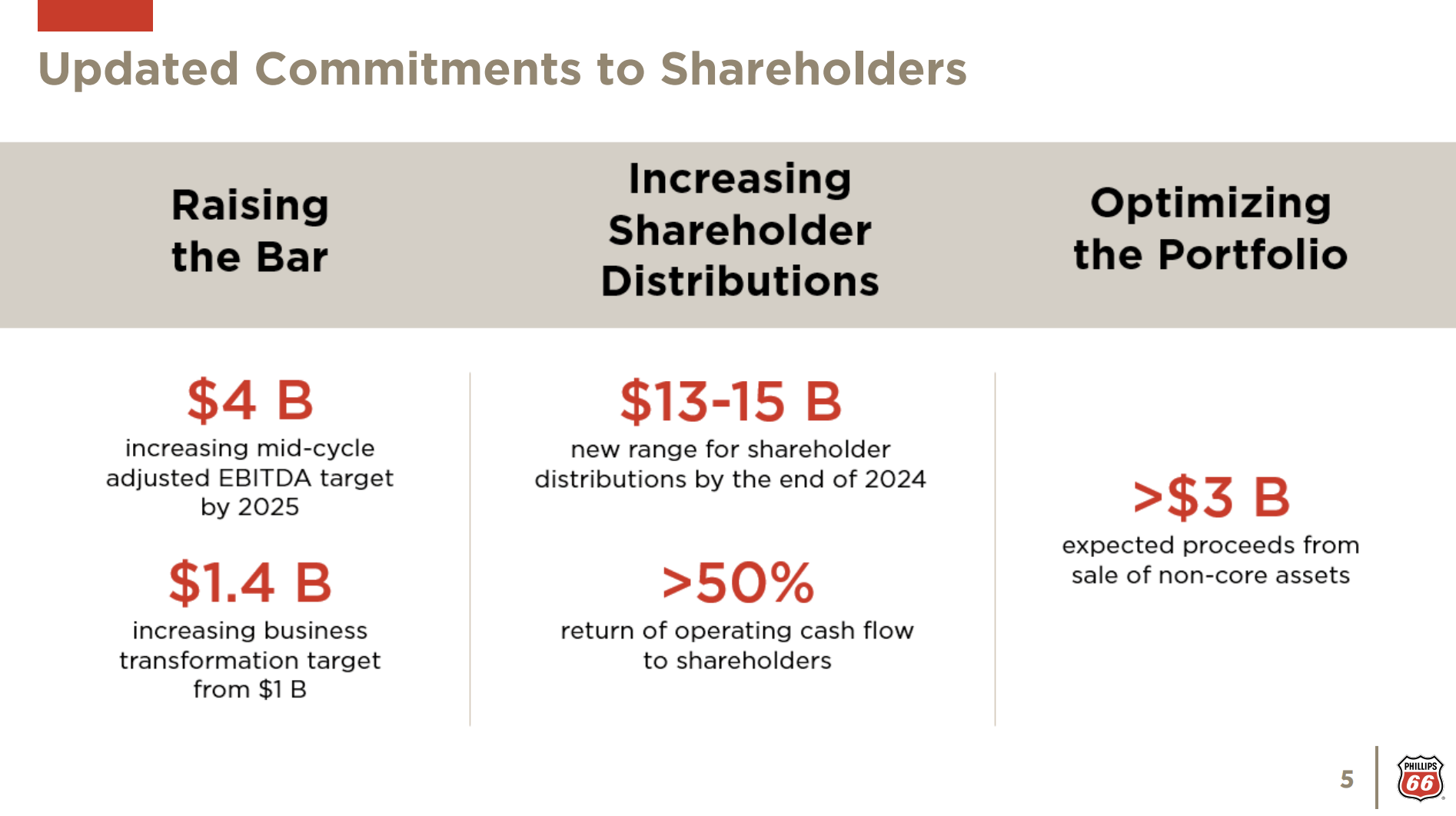

Related to the aforementioned developments, the company has raised its mid-cycle adjusted EBITDA growth target from $3 billion to $4 billion by 2025. This includes additional value from business transformation, midstream synergies, and commercial contributions.

Phillips 66

Furthermore, the business transformation target has been increased to $1.4 billion.

{kind=link}

In fact, the company is committed to higher shareholder distributions. It now targets $13 to $15 billion between July 2022 and the end of 2024.

It aims to distribute 50% of operating cash flow to shareholders.

Phillips 66

The current dividend yield is 3.3%. It is protected by a sub-25% payout ratio and a balance sheet with a BBB+ rating. The five-year dividend CAGR is 12.8%.

Based on the company's growth potential, Elliott sees tremendous shareholder value.

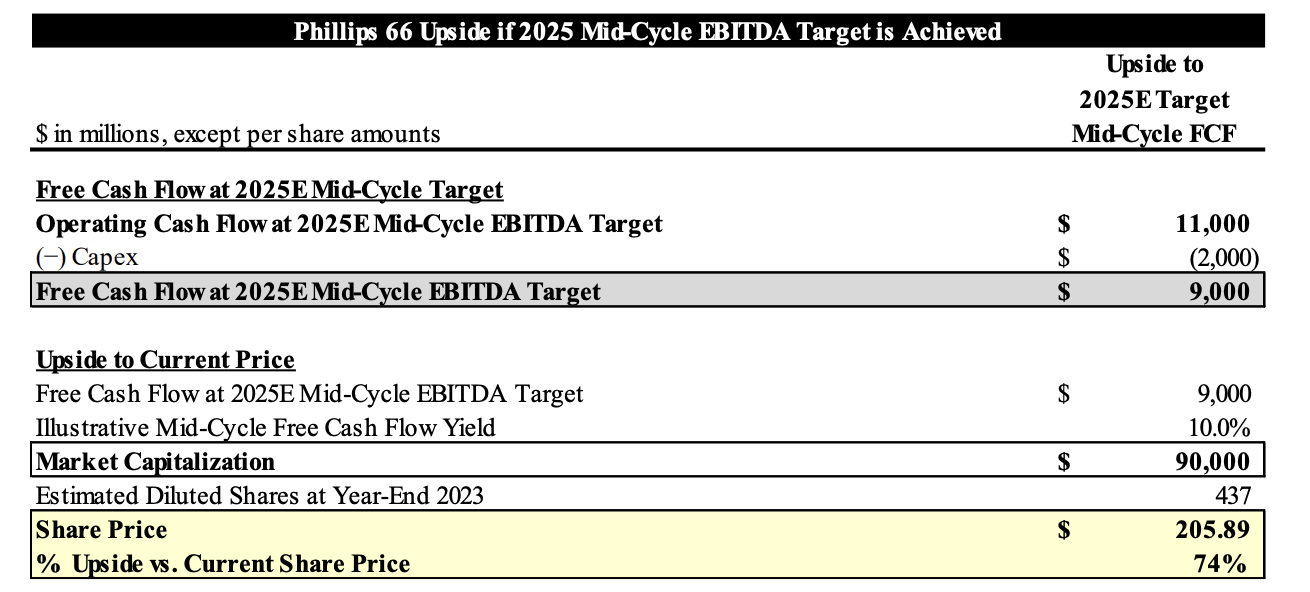

Using $14 billion in 2025E mid-cycle EBITDA, the company could generate $9 billion in free cash flow.

Applying a 10% free cash flow yield (free cash flow as a percentage of the company's market cap), the company should trade above $205 per share.

Elliott estimates that Valero trades at a 7% FCF yield, which gives PSX a bigger margin of safety. Over time, that discount could further shrink if PSX improves its business, which could mean longer-term outperformance.

When Elliott published its letter a short while ago, a $205 target price implied a 74% upside. Currently, that number is still 60%.

{kind=link}

Elliott Financial Management

Over time, I think the market will apply an 8-9% free cash flow yield valuation, which means that the fair value is probably still 70% to 80% above the current price - excluding dividends and buybacks.

With all of this said, Elliott is getting involved to make sure that the company is successful in turning around its business.

That's where the aforementioned "manual efforts" come into play, as the fund is looking to get two new directors appointed to the board. The company has identified multiple candidates with deep industry knowledge that are expected to be in a good spot to monitor the company's strategic plans.

Furthermore, the company wants Phillips 66 to commit to an exit strategy that could result in a total strategic overhaul if it fails to achieve its current goals.

However, should Phillips 66 fail to show material progress toward its 2025 targets over the next year, we believe that the Company should at that point pursue its best available option by making a strategic pivot and following a path that mirrors Marathon’s recent transformation.

In 2019, MPC started a massive turnaround that included the appointment of a new director, a new CEO, massive operating cost improvements, and the sale of its retail operations that operated under the Speedway brand. As most shareholders will remember, that led to massive buybacks.

In general, MPC is a buyback-focused company.

Over the past 12 months alone, MPC has bought back 16% of its stock.

Elliott hopes that Phillips 66 can see similar results by making the aforementioned changes, closing the $2-$3 per barrel refining EBITDA gap with its peers, and generating at least $15 billion after-tax proceeds from the sale of its stake in CPChem, its chemical joint venture with Chevron ( CVX ).

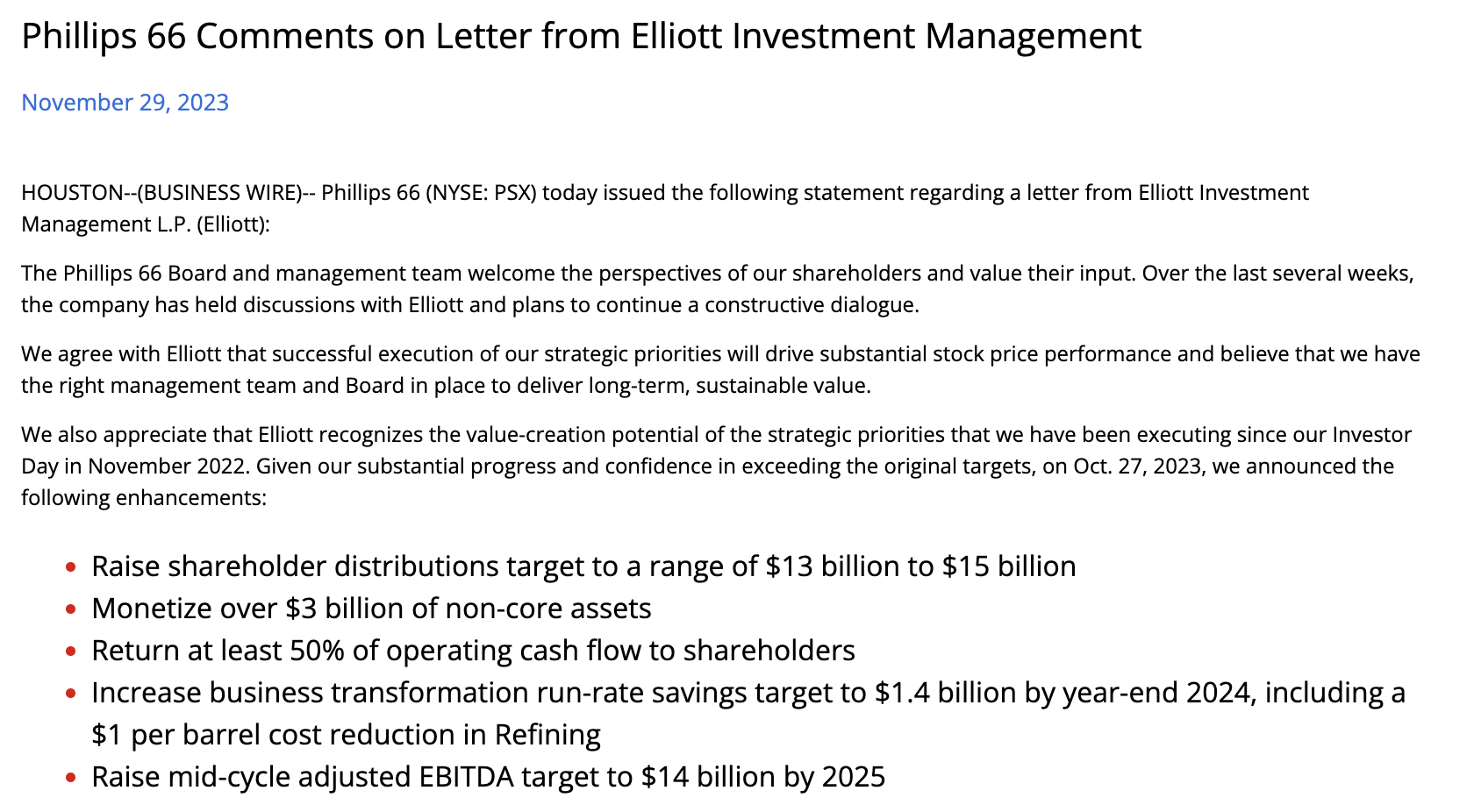

These changes were welcomed by Phillips, which responded positively to the letter. While it doesn't look like Phillips 66 is welcoming to the idea of changing the board, it did reiterate its plans to boost shareholder value.

{kind=link}

Phillips 66

Looking at the bigger picture, I'm very happy with Elliott's involvement.

- The fund is not only putting pressure on Phillips 66 to achieve its targets but also working on measures that go beyond its current targets (like divestitures).

- Elliott's proposal for an exit strategy in case current measures fail is another great point.

- Although PSX's 3% yield isn't very juicy, its free cash flow growth potential is impressive, which puts both income and total return investors in a good spot.

- I believe that PSX's fair value is between 60% and 70% above its current price.

In general, I believe that my initial thesis has been strengthened. The cost cutting and efficiency targets were a part of my thesis already. Now, we get the benefit of a major player fighting for the implementation of these targets.

Although current economic headwinds could keep the stock price from continuing its current momentum, I'm convinced that PSX's future looks very bright!

Takeaway

Since my November article on Phillips 66, activist giant Elliott Investment Management has entered the scene with a $1 billion stake and a bold letter to the board.

Identifying key issues like underperformance and operational lapses, Elliott proposed a strategic overhaul. The company responded positively, welcoming changes.

With a focus on cost-cutting, divestitures, and a commitment to shareholder value, Phillips 66's future seems promising.

Despite economic headwinds, Elliott's involvement strengthens my initial thesis, reinforcing the potential for substantial gains and a brighter future for PSX.

For further details see:

60% Gains Plus Dividends With Phillips 66 If Elliott Is Right