PEB - 8.4% Yield At A Discount With Pebblebrook Preferred G

2023-04-27 05:57:58 ET

Summary

- Hotels are a tough industry, but PEB is one of the best operators.

- Its strong hotel portfolio along with seasoned management provides a certain stability to PEB.

- This stability bodes well for Preferred shares which provide outside yield as well as capital gains potential.

Pebblebrook Hotel Trust ( PEB ) is a large hotel REIT owning high end resorts and urban business hotels. It is long tenured in the space and has consistently been one of the most conservatively run hotel REITs. At a significant discount to Net Asset Value ((NAV)) and a roughly 7X multiple on stabilized FFO I think there is an argument that could be made for owning PEB.

However, I am more bearish than most on the hotel space so I am neutral on the common. That said, in analyzing the full capital stack I think the preferreds are significantly undervalued and can provide a strong total return even if my more bearish than consensus view on the industry ends up being correct.

Let me begin with where I differ from consensus and then discuss the merits of Pebblebrook preferreds.

Hotel industry history and outlook - consensus and my view

Understanding the hotel industry outlook requires some background information on the recent past.

Hotels are a cyclical industry. Demand fluctuates with GDP, but with a higher amplitude. Normal recessions will substantially reduce profitability, but the earnings quickly recover with the economy as travel budgets are restored. That is the typical behavior in typical recessions, but COVID was something else entirely.

Hotels were closed down for a significant portion of the COVID lockdown which took FFO negative for most of the hotel REITs. Many of the debt covenants are based on ratios of EBITDA to interest expense so as EBITDA collapsed there were covenant breaches. Hotel REITs made deals with their lenders which resulted in collateralization of previously uncollateralized debt. In most cases the new terms were less favorable to the REIT and more favorable to the lender.

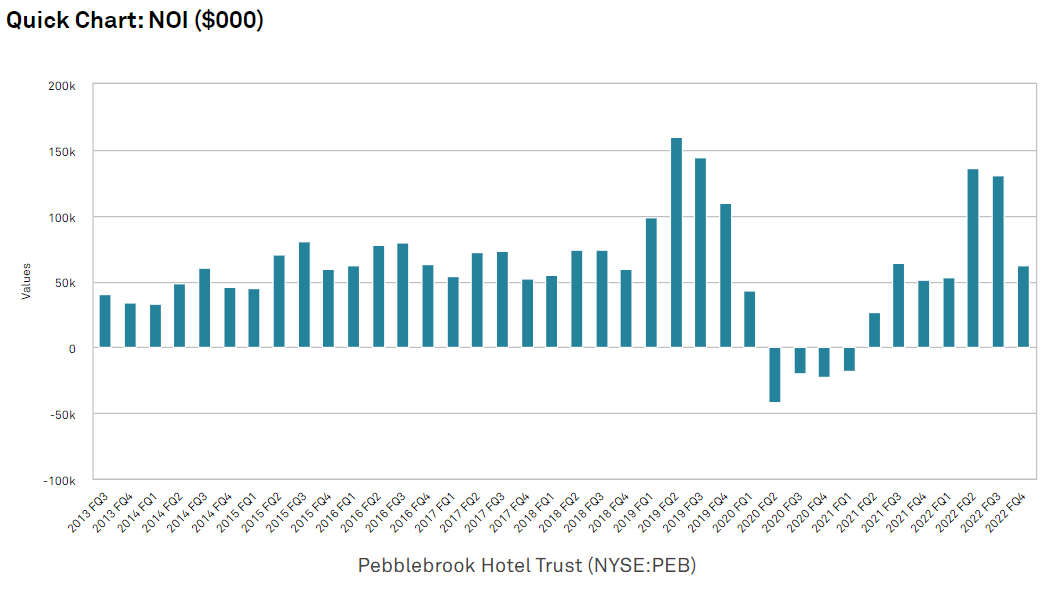

Pebblebrook went into the pandemic with a significantly lower level of debt and more liquidity which allowed it to largely avoid renegotiation of debt terms. On the revenue side, however, it was just as impacted as everyone else. FFO turned negative with -$1.46 per share in 2020 followed by -$0.32 per share in 2021.

In 2022 the hotel market started to fully reopen and PEB recovered to $1.69 per share of FFO but it is still well below 2019 FFO of $2.63.

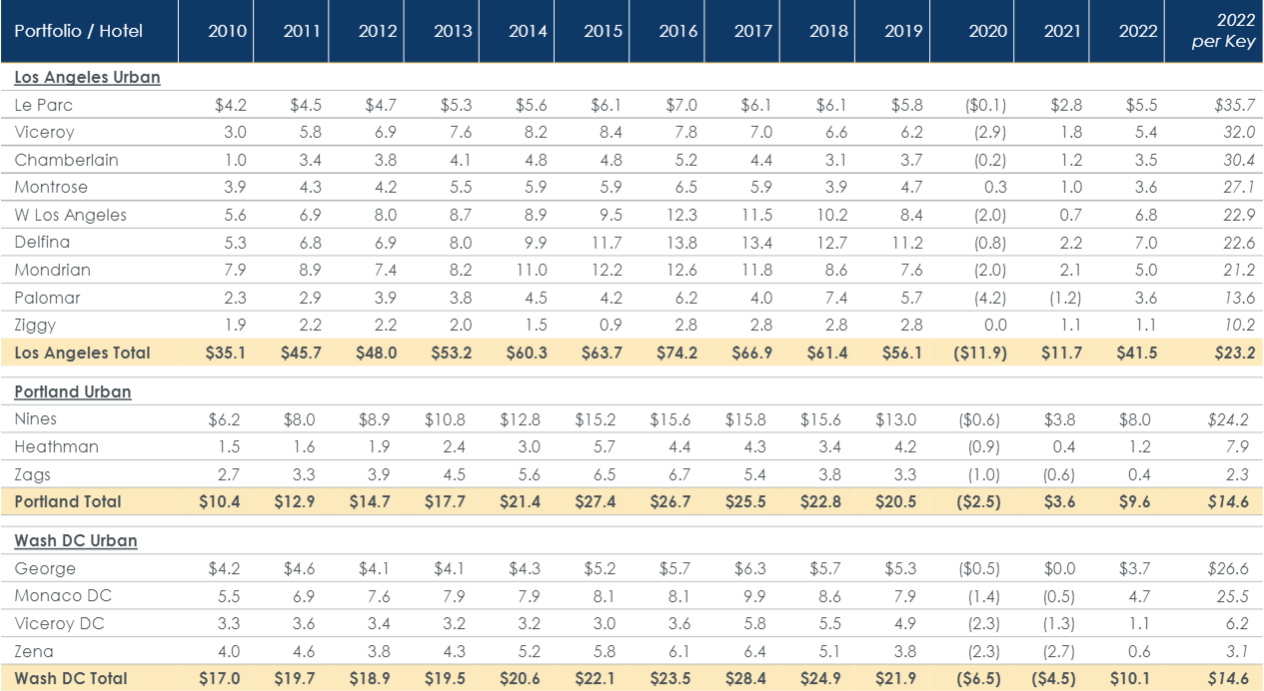

The recovery has been exceedingly lopsided so far with leisure and particularly resort hotels reaching record levels of profitability while more business or conference focused hotels have lagged. Below are PEB's numbers on its resorts.

PEB

PEB has an impressive portfolio of beachfront resorts, many of which are located in Florida. These are high end properties with average daily rates of $432 in 2022. Beyond rooms guests frequently buy food, and other services which takes total revenue per occupied room to $782 per night in 2022. This is fully 43% higher than the already high $546 in 2019.

The resort business is the best it has ever been. Business travel has been more sluggish to recover. Below are some of PEB's urban located, business travel focused hotels.

{kind=link}

In each submarket, 2022 EBITDA is still lagging significantly behind 2019 levels.

In recent quarters, there have been some signs of business travel revival. Analysts are broadly expecting business travel to continue to rebound resulting in FFO trending back up toward pre-pandemic levels.

{kind=link}

At the levels of FFO predicted by Wall Street analysts, PEB would be a screaming buy as it is trading at less than 10X current FFO with fast growth over the next few years.

While I largely agree with the FFO numbers, I don't think FFO tells the whole story.

Myriad of challenges facing hotel REITs

- True earnings are much less than FFO

- Embedded cost structure

- Unclear threat from rental sites

Hotels are a high capex property type. Customers expect the properties to be fresh, fancy and in-line with current trends. In the short term, renovations do come with a revenue increase, but over time revenue falls back to trend. Over the long run, the renovations are more revenue maintaining rather than growth capex. As such, I view them as a real expense.

The kicker here, and why cheap FFO multiples are not necessarily a buy signal is that renovation capex does not run through FFO. When capital is spent to renovate a property, the investment is capitalized on the balance sheet and then depreciated over time. Depreciation expense is added back for FFO according to the standard NAREIT definition.

In most types of real estate the NAREIT definition of FFO gets fairly close to the true earnings number, but because hotels are so capex intensive, I find FFO significantly overstates their earnings.

Embedded cost structure

Too many entities are taking a bite out of hotel revenues. I have discussed this in the past so I will be brief here, but both brands and online travel agencies are capturing an unfair share of the profits. Online travel agencies get as much as 20% of revenue when rooms are booked through Expedia or one of their peers and brands like Marriott ( MAR ) collect a percentage of revenues up front.

This industry structure is unfavorable for the hotel owners because it is the owner that is taking the risk as well as contributing the capital (in the form of the properties). The other players are getting a significant portion of the profits without much contribution.

Unclear threat from rental sites

Airbnb ( ABNB ) and other similar sites are not competing on a level playing field. Hotels have to comply with hotel taxes, health codes, security standards and every other regulation while the rental sites can often get away with circumventing many expenses. The onus falls on the individual putting up their property for rent rather than on Airbnb which makes the regulations almost entirely unenforceable.

If the individual skips out on paying $100 of hotel taxes there is functionally nothing enforcement agencies can do because the cost of enforcement would be greater than the realization. If a hotel owner like PEB tries to not pay hotel taxes the amount is in the millions and would be enforced swiftly.

As long as rules remain so loose on Airbnb and equivalents, they present a very real threat to the established hotel industry.

By now it is probably obvious that I am bearish on hotels as I just spent the first 1000 words of a bull thesis discussing what has and will continue to go wrong in hotels. So what is it that makes PEB preferreds opportunistic?

The Preferred buy thesis

One of the most misunderstood concepts in investment is how different the risk and reward profiles of preferreds are compared to the common equity of the same issuer. I think this is best explained through scenario analysis.

We have placed 5 scenarios in the table with the approximate value of common and preferred shares in each scenario.

{kind=link}

Note that these boxes are not equally likely. The bull, bear and baseline are by far the most likely with the 2 boxes on the right being tail risks if some sort of black swan event happens.

Sell side analysts are predicting somewhere between the bull scenario and baseline scenario while I am anticipating closer to the bear scenario.

The key idea here is that preferreds are worth a fixed liquidation preference so their value does not change when a company is wildly successful. If things go great for the hotel industry and PEB continues its excellent operations, the common could legitimately double. In such an outcome the preferred would still just be worth the $25 liquidation value per share plus the stream of dividends.

On the other side, however, preferreds do not lose value when a company struggles until such a point when the company fails entirely and the liquidation value of the real estate is not enough to pay the preferreds out in the waterfall.

If, for example, business travel remains muted and leisure travel subsides due to moderate to severe recession, FFO could drop back down to somewhere around $1.00 per share. The lower profitability hurts the common shares and assuming a similar FFO multiple, the common would be worth about $10 per share.

For preferreds, anything over $0 per share in FFO is enough to finance the preferred dividend as the dividend is a before FFO expense. The income of preferred holders would not change and their liquidation preference would stay at $25.

The scenario in which preferred value becomes impaired is if properties are impaired so severely and permanently that the value of those properties goes below the sum of debt and preferred liquidation preference.

I see this as quite unlikely for 4 reasons:

- Hotel demand is sustainable on a long term basis

- Leverage at PEB is quite low

- Premium quality portfolio

- Stress tested

Demand for travel strikes me as a constant. There are times when people's ability to travel is impaired due to financial reasons, but the desire never seems to go away. This is backed up in the numbers.

{kind=link}

The pandemic was arguably the worst downturn for hotels in modern history and yet demand has bounced right back.

In 10, 20, 50 years people will still want to travel and when they do they will want to stay at beautiful resorts such as the ones PEB owns. This doesn't guarantee that the properties will be worth more than they are today, but, in my opinion, it does nearly guarantee they will have some value.

Low debt

To get paid in full, preferreds merely need there to be enough property value to overcome the debt plus preferred liquidation preference. The bigger the pool of common equity underneath, the greater the cushion. PEB has low leverage and billions in common equity.

PEB

With over $6.7B in assets and just over $2.3B in securities ranking senior to the preferreds, asset value would have to fall an extreme amount for preferreds to not be made whole.

Even in the pandemic, trophy assets did not lose 50% of their value. That sort of thing just has not happened and I don't see it as likely. 50% value loss would typically require some sort of catastrophic event and even in that case PEB seems well protected.

Stress tested - Hurricane

Hurricane Ian did some serious damage to La Playa, one of PEB's more valuable beach resorts. It would appear that most of the damage Is going to be reimbursed by insurance. Insurance is not only paying for repairs, but also business interruption according to the earnings call:

"We have received $25 million so far from our insurance providers to complete the necessary repair and remediation work. We expect additional proceeds from our insurers for the work needed to fully restore this fantastic resort shortly. Upon completion, it will be better than ever, and we expect it will be quickly returned to its pre-hurricane performance. We're also expecting the first preliminary installment of business interruption proceeds. In this case, $7.2 million for lost business during the fourth quarter of 2022, which is net of our $2 million PI deductible. This has been incorporated into our Q1 outlook and will hit other income and benefit adjusted EBITDA and adjusted FFO. We expect to receive additional BI proceeds for Q4 2022 and 2023 later in the year or by the time we reach a final settlement, and we'll update you quarterly as we progress in this area."

Why the preferred is better than the common

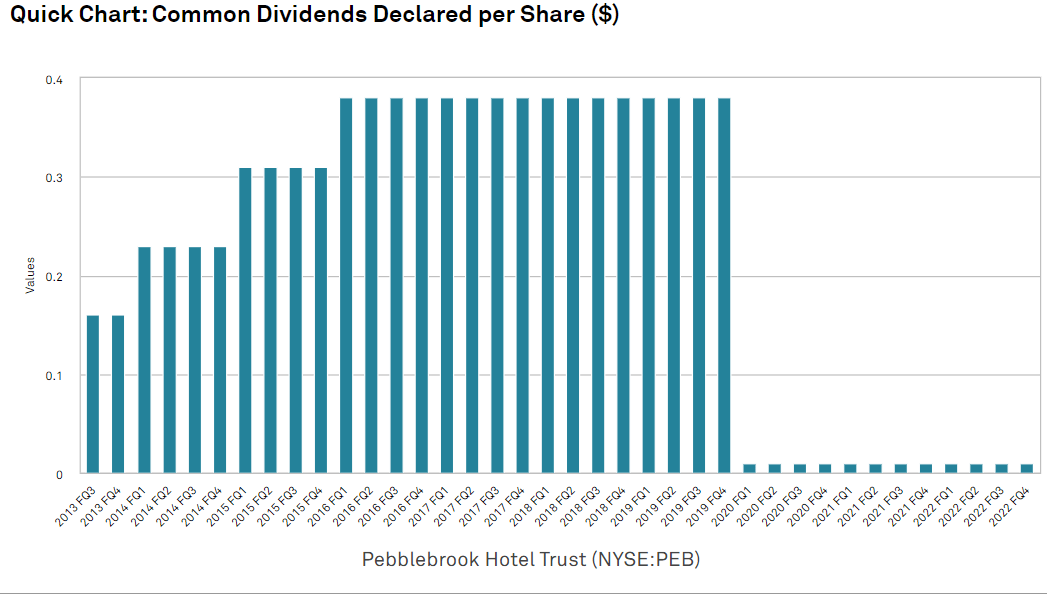

I think the hotel business will continue to be challenging which has resulted in common dividends being cut to near zero.

{kind=link}

Unlike common dividends, preferred dividends are cumulative and accrue to liquidation preference even if suspended.

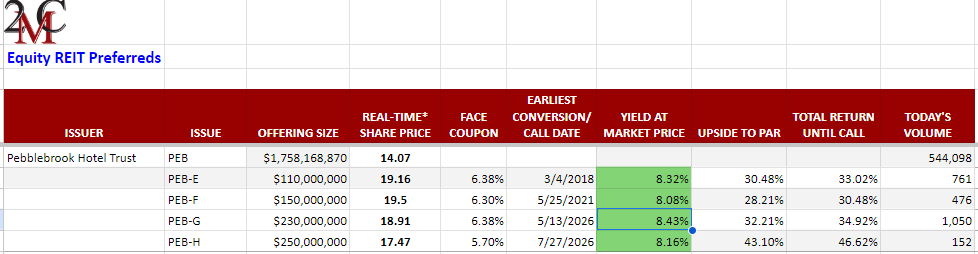

So while the common stock requires hotels broadly to improve as an industry, the preferred can be a great investment even in a muddle along sort of scenario. Within the preferred stack I am partial to the Series G (PEB.PG)

Portfolio Income Solutions Equity REIT Preferred tracker as of 4/24/23

{kind=link}

At $18.91 it offers 32.2% upside to par along with a 8.43% current yield.

The $25 liquidation preference is protected by a billion of dollars of equity cushion underneath it. I find this to be far too high of a yield for what I view as fairly low risk. Over time, I think PEB.PG will trend up toward its par value of $25, allowing those who invest today to collect up to 32% capital gains on top of the 8.4% yield while they wait.

For further details see:

8.4% Yield At A Discount With Pebblebrook Preferred G