VTR - 8%-Yielding Healthcare Realty: Cash Flow Is Sanity

2023-11-30 08:10:13 ET

Summary

- Healthcare Realty Trust has experienced a significant drop in share price over the past 12 months.

- HR owns and leases out medical office buildings, which have high rent coverage and are mostly situated on or adjacent to hospital campuses.

- Demographic tailwinds and low new supply make HR an attractive long-term investment with a high yield.

Healthcare real estate remains an attractive asset class due to demographic tailwinds, but it appears that the market hasn't gotten the memo with respect to REITs in this segment. This includes Healthcare Realty Trust ( HR ), which I last covered here back in June, highlighting its quality portfolio and revenue stream.

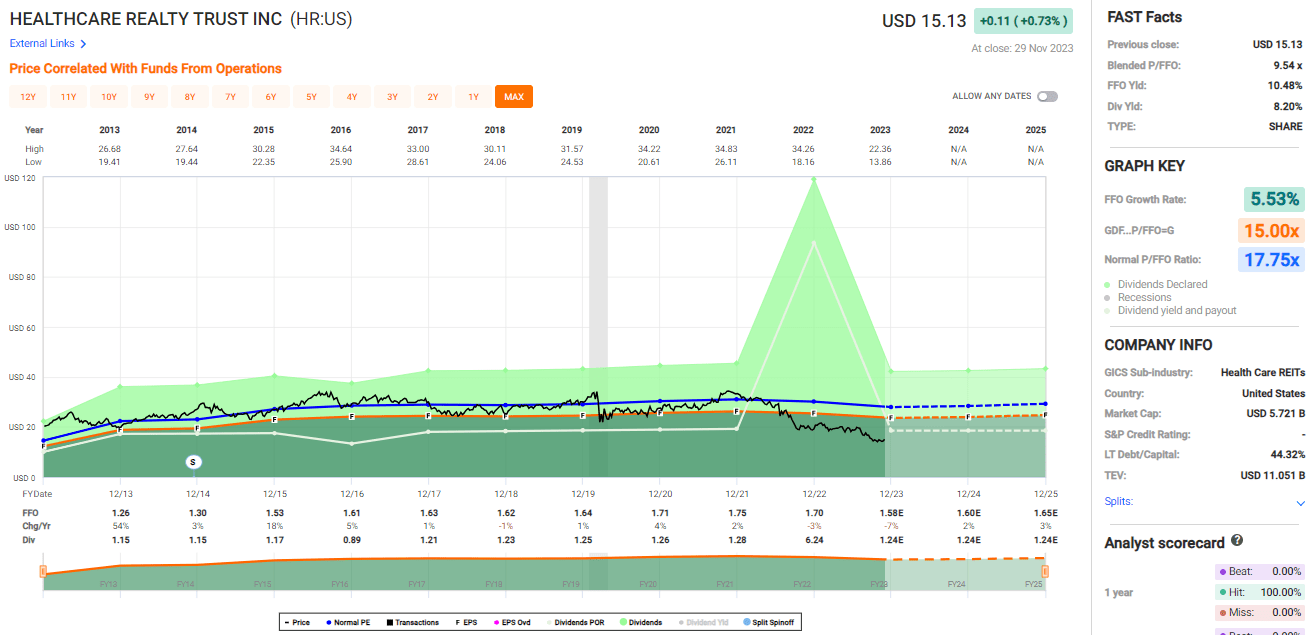

Market action around the stock has been brutal this year, to say the least, with HR's share price having fallen by 24% over the past year, and higher interest rates have been a strong contributing factor to the drop. In this article, I highlight recent developments and discuss why now is an opportune time for income investors to layer into the stock, so let's get started!

Why HR?

Healthcare Realty is a self-managed REIT that's focused on owning and leasing out medical office buildings, which comprise 92% of its annual base rent. MOBs are arguably one of the most durable healthcare asset classes given their high rent coverage compared to skilled nursing facilities, think Omega Healthcare ( OHI ), and better "immunity" from pandemic-related problems that plagued senior housing properties, think Ventas ( VTR ).

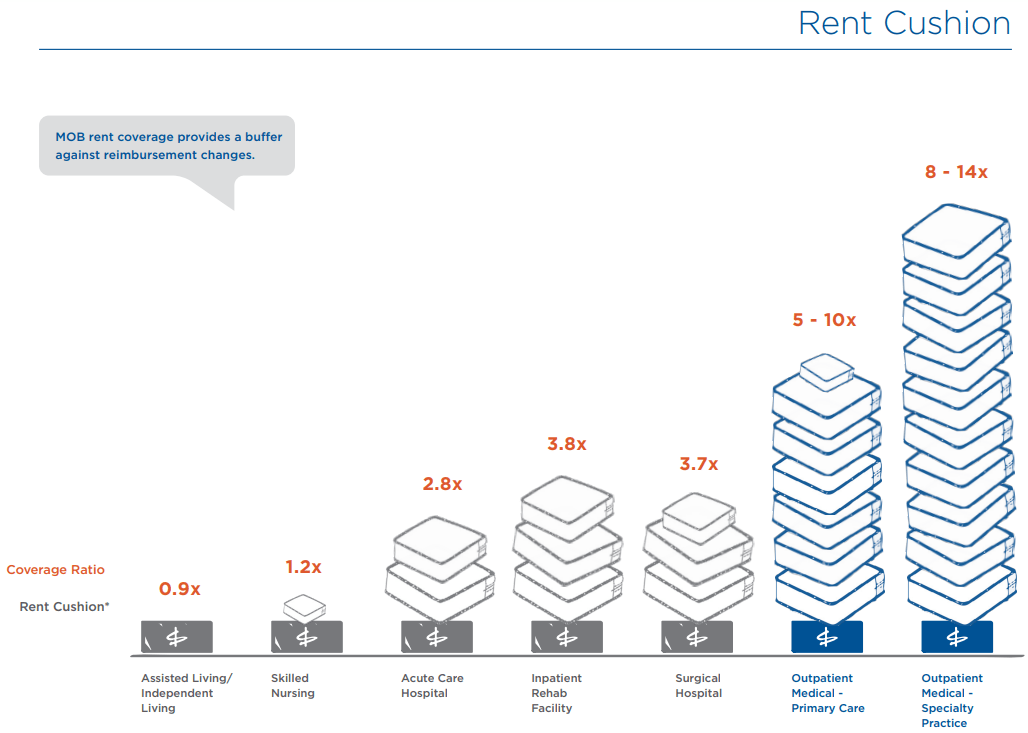

This durability is also reflected by the strong rent cushion that HR's tenants in the outpatient medical space enjoy relative to other healthcare asset classes. As shown below, this segment has the highest rent coverage compared to hospitals, skilled nursing facilities, and assisted living/independent living facilities.

{kind=link}

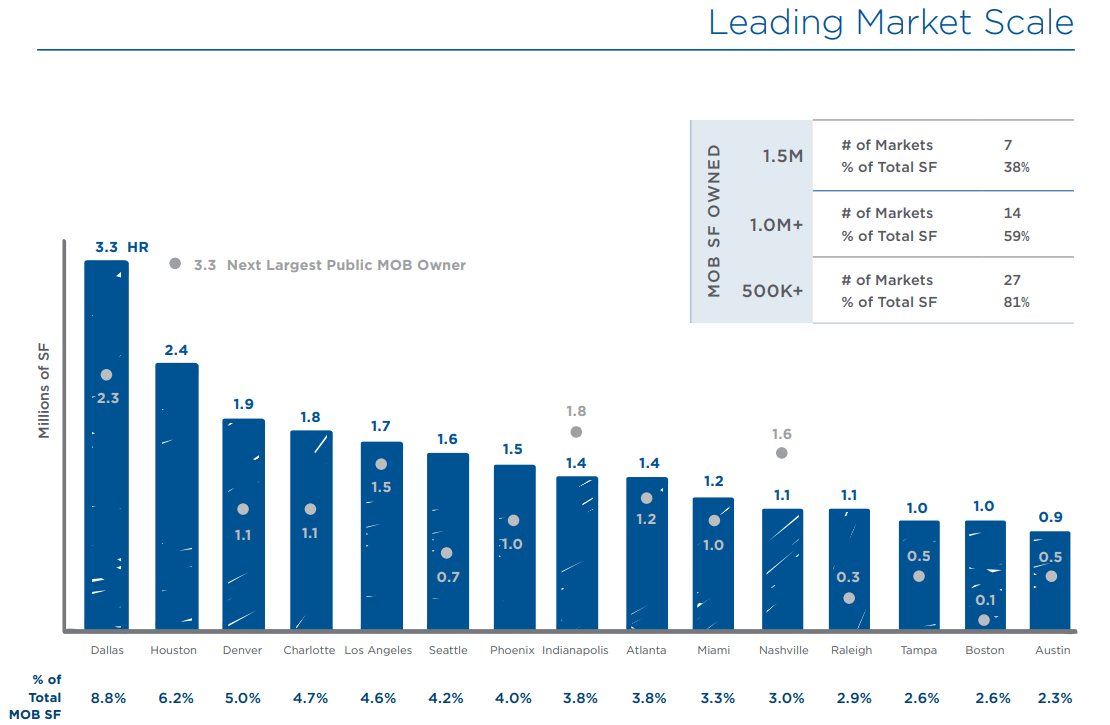

HR merged with Healthcare Realty Trust last year, and at present, owns 697 properties that are spread across 35 states. It also benefits from having most of its properties (72%) being on or adjacent to hospital campuses, which drive patient visits. As shown below, Dallas, Houston, Denver, Charlotte, and Los Angeles represent HR's top 5 markets, and it holds a leading share in most of its markets.

{kind=link}

A real estate landlord like HR isn't going to see the explosive growth that tech companies like NVIDIA ( NVDA ), but in exchange, investors get steady growth and a far more reasonable valuation and yield. This is reflected by HR's same-store cash NOI growing by 2.3% and 2.8% YoY for the third quarter and the first nine months of the year, respectively. This was driven by average in-place rent increases of 2.8% and weighted average MOB re-leasing spreads of 4.8%. Going forward, HR will see higher inflation-adjusted annual contractual rent increases of 3.0% on leases commencing during the current fourth quarter.

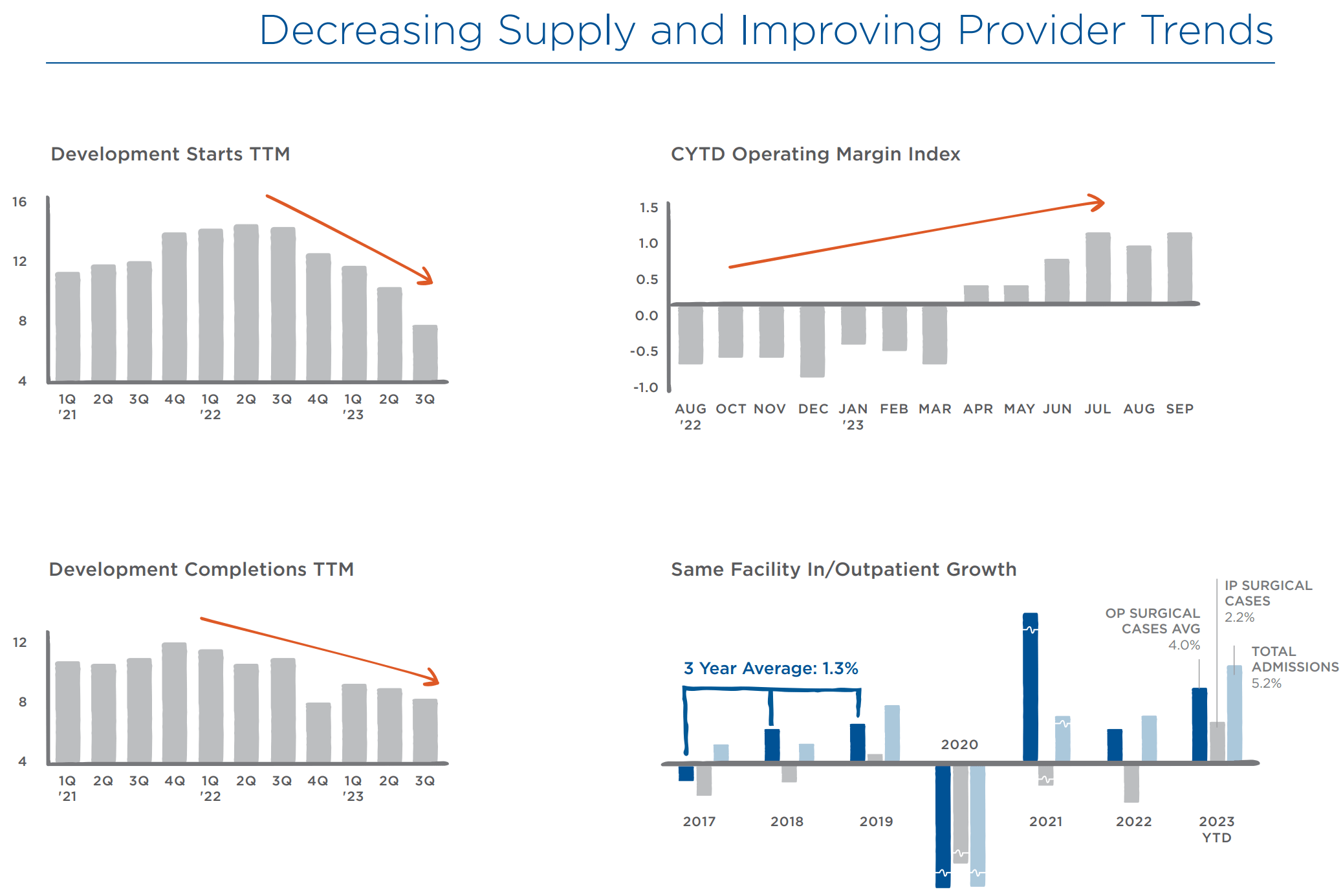

Besides inflation, higher interest rates have put pressure on new supply due to elevated construction costs, which means less competition for tenants and higher demand for HR's existing properties. New development starts in the last reported quarter were at the lowest level since at least the beginning of 2021.

At the same time, demographic tailwinds continue to support the long-term growth thesis for HR. This is supported by research that estimates 1 in 5 Americans will be 65 years or older by 2040, up from 1 in 6 as of 2020. Moreover, recent trends are working in favor as outpatient growth in HR's same facilities currently sits well above the 3-year pre-pandemic average, as shown below.

{kind=link}

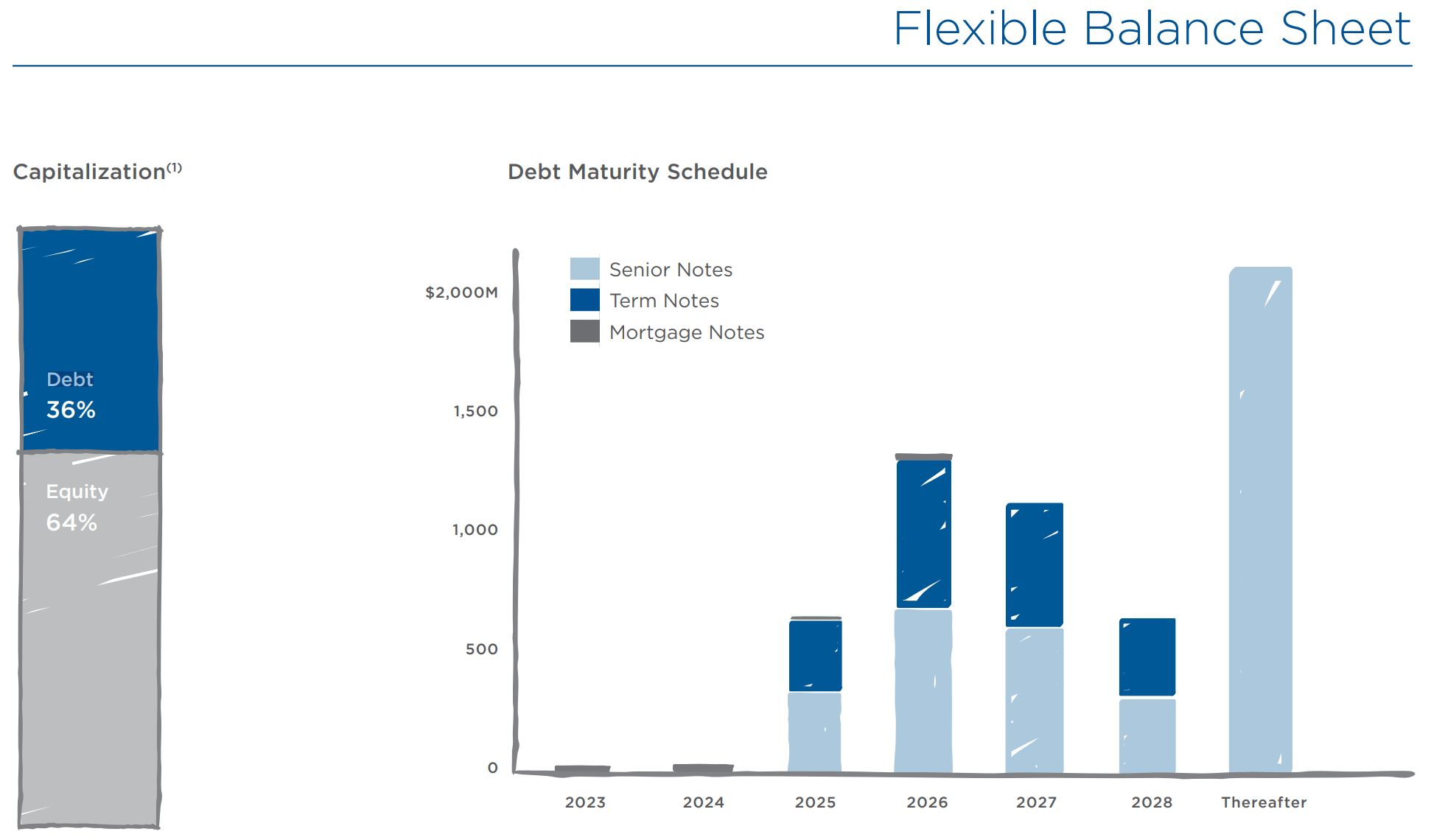

Headwinds to HR include higher interest rates and a depressed share price, which means that seeking growth capital in debt and equity markets is off the table. This means that investors should be accustomed to seeing little or no top-line growth for the time being. Plus, HR currently carries a net debt to adjusted EBITDA ratio of 6.6x, which sits slightly higher than its 6.0 to 6.5x range. However, HR has insignificant debt maturities between now and the end of next year, as shown below.

{kind=link}

Looking out to 2025 and beyond, I would expect for debt maturities to be handled with a combination of refinancing and debt paydown. This is supported by management's comments on the last earnings call stressing balance sheet discipline and the expectation that they will be net sellers in the current environment. This means avoiding new developments and pursuing only selective redevelopments.

Meanwhile, HR currently yields an attractive 8.2% and the dividend is well-covered by a 77.5% payout ratio. While I wouldn't expect there to be meaningful dividend growth in the near term, I believe the high yield more than makes up for it. I also see value in the stock at the current price of $15.13 with a forward P/FFO of 9.6, sitting well under its normal P/FFO of 17.8. While I wouldn't expect HR to return to its normal valuation anytime soon, I do believe the current discount is too wide for an enterprise with durable cash flows and long-term tailwinds in place.

{kind=link}

Investor Takeaway

In summary, HR is an attractive income stock for investors looking to diversify their portfolio with a healthcare REIT with strong fundamentals. With its strong rent coverage and stable tenant base in the outpatient medical space, supported by demographic tailwinds, the company is well-positioned for long-term growth.

While current headwinds such as higher interest rates may impact near-term performance, I believe HR's attractive yield and discounted valuation more than makes up for it. With many tech stocks back at bubble valuations while giving investors a low to no dividend yield, I view HR as being a sane choice for income and total return-oriented investors. Reiterate 'Buy' rating.

For further details see:

8%-Yielding Healthcare Realty: Cash Flow Is Sanity