MDV - 8% Yielding 'Strong Buy' REIT Preferred Shares

2023-05-30 08:05:00 ET

Summary

- Many preferred stocks are now heavily discounted and offer high yields.

- Since real estate is well-known for its cash generation capabilities, REIT preferreds often offer better risk-to-reward.

- We discuss two REIT preferreds with yields above 8% for your consideration.

Co-produced by Austin Rogers

There's a lot of uncertainty and confusion surrounding preferred stocks among retail investors, but they are a very simple form of capital.

While they have redemption dates at which they can be redeemed, many can be perpetual forms of capital that need never be redeemed or refinanced. That makes them a bit like equity.

But having a fixed dividend and a par/redemption value (almost always set at $25 per share) makes them a bit like a bond.

Preferred stocks also trade like bonds, selling off when interest rates rise and trading up to (or higher than) par value when interest rates fall.

See, for example, how the InfraCap REIT Preferred ETF ( PFFR ) plunged in price as long-term interest rates surged higher:

At High Yield Landlord, we think that the preferred stocks of real estate investment trusts ("REITs") ( VNQ ) are a great place to look for high and safe yield, as real estate is well-known for its high cash generation.

If you believe, as we do, that interest rates are at or near their peak (at least for this cycle), then now is a great time to look for deals in the realm of REIT preferreds.

Here are two particularly interesting opportunities to consider. We own a position in the first one and we are considering the second:

Arbor Realty Series F Fixed-To-Floating Preferred Stock ( ABR.PF )

Arbor Realty Trust ( ABR ) is an internally managed mortgage REIT and one of the most successful short-term commercial real estate lenders on the public market. They primarily extend bridge loans backed by multifamily and single-family residential properties.

By focusing overwhelmingly on highly defensive, mostly Class B apartment properties, ABR has generated extraordinarily strong returns, handily beating both commercial mREIT peers ( STWD , BXMT , LADR ) and the broader real estate index ( VNQ ):

Aside from its focus on defensive residential properties, ABR has a few other big strengths in its favor:

- Top-notch management, led by founder and executive chairman Ivan Kaufman, that is long-tenured and strongly aligned with shareholders through ~12% insider stock ownership.

- In addition to balance sheet loans, ABR also generates highly stable, annuity-like revenue streams through loan originations, securitizations, and servicing.

- A little over half of ABR's balance sheet loan book is backed by real estate in four of the hottest Sunbelt states: Texas, Florida, Georgia, and North Carolina.

{kind=link}

That said, despite ABR's skillful loan portfolio curation and navigation of tricky environments over the years, the stock is not without risk. It wouldn't offer a 13%+ dividend yield if it was!

Unsurprisingly, ABR's primary risks come from debt. Its balance sheet loan portfolio has a weighted average loan-to-value of 76%, which is on the high side (although by no means egregiously high), and ABR also uses a large amount of debt to finance its investments. Around 85% of ABR's total enterprise value is in the form of debt and preferred equity.

Debt on top of debt means that if something did go wrong with a big enough portion of ABR's portfolio (unlikely, but possible), it could cause a self-reinforcing negative cycle.

If residential property values or rent rates fall significantly enough, it could cause severe problems for both ABR and its customers.

That said, we view this negative scenario as unlikely, for multiple reasons:

- Today, unlike in 2007-2009, we have a housing shortage rather than a housing surplus . Rents are still increasing, and residential property values are by no means crashing.

- ABR's payout ratio is conservatively low at around 70%, and management just hiked it by 5%!

- Management expressed strong optimism on the Q1 2023 conference call and have been buying back stock recently.

- Multiple members of the management team, especially Kaufman, have been buying ABR shares recently.

Even so, we recognize that ABR's risk profile is not suitable for every investor.

That's why we instead like the Series F 6.25% Fixed-to-Floating Cumulative Redeemable Preferred Shares ((ABR.PF)). We prefer it for several reasons:

- As important as common stock dividends are for both shareholders and insiders alike, ABR cannot pay a penny in common stock dividends until the preferred stock dividends are paid.

- ABR's preferred stocks make up only 4% of the company's total enterprise value, and as such, their preferred dividends are a small fraction of fixed costs.

- ABR.PF's shares are still trading at a remarkable ~40% upside to par (or redemption) value.

- ABR.PF has a very unique fixed-to-floating feature that distinguishes it from most other preferred stocks, including ABR's other two classes of prefs.

Basically, here's how ABR.PF's preferred dividend works:

- Fixed 6.25% at par value ($25) from now until the redemption date on October 30th, 2026

- Thereafter, a floating rate of 3-month SOFR plus 5.442% with a floor of 6.125%

The earliest ABR can redeem ABR.PF is October 2026. If management does not redeem this series of prefs that month, the payment structure will switch the floating rate formula above.

As of April 19th, the 3-month SOFR sits at 4.78%. If the floating feature kicked in today, it would trigger a floating rate a little over 10% at par. That is far higher than the fixed coupon yields of ABR's other two preferred stocks that do not have fixed-to-floating features.

- Arbor Realty Preferred Series D ( ABR.PD ) - 6.375% at par

- Arbor Realty Preferred Series E ( ABR.PE ) - 6.25% at par

But notice that the 10% yield at which ABR.PF would trade if the floating feature was in effect today is at par . But ABR.PF is trading at about a ~30% discount to par! So, the yield at present value would actually be slightly over 14%!

Of course, the floating rate feature is not in effect today, so instead the yield at present value (based on a par yield of 6.25%) is about 8.8%.

Earning an 8.8% yield plus 41% upside to par sounds like a pretty good deal to us.

And we do think that it is likely we will see that ~40% upside, one way or another.

If interest rates are high in October 2026, then management will be highly motivated to redeem the shares in order to avoid paying a double-digit yield. If interest rates fall, then preferred stock yields will likely come down accordingly, which means that ABR.PF's stock price will likely rise.

Modiv Series A 7.375% Preferred Stock ( MDV.PA )

Modiv Inc. ( MDV ) is a new triple-net lease REIT focused on mission-critical industrial real estate, specifically manufacturing facilities.

Slightly over 2/3rds of the portfolio are in industrial properties that feature a 14.5-year weighted average remaining lease term and annual rent escalators of 2.4%. Another 20% of the portfolio is in retail properties that are long-term holds, and the remainder (13% of NOI) is in non-core retail and office properties that MDV is gradually selling in order to recycle capital into industrial properties.

MDV's focus going forward is on industrial-manufacturing properties. Right now, the portfolio's weighted average remaining lease term sits at 13.3 years, and 38% of rent derives from investment grade tenants.

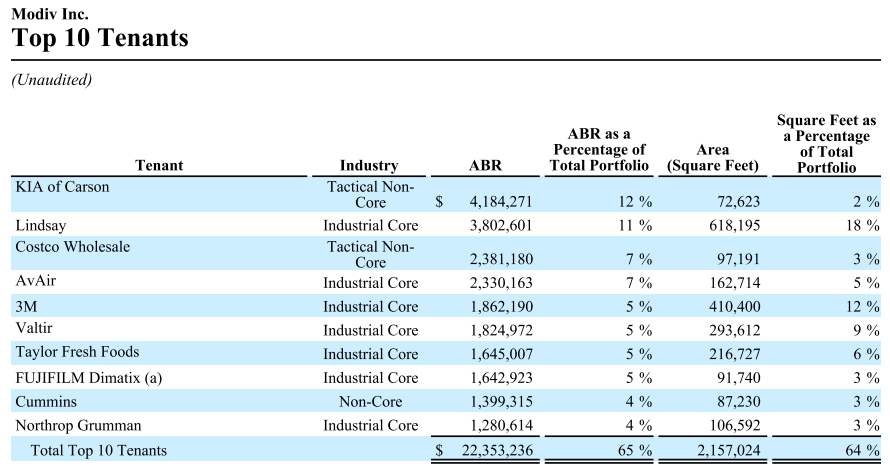

Though you might think that MDV's portfolio would be very low quality given its cheap stock valuation, the truth is nearly the opposite. The portfolio is populated by tenants like Costco ( COST ), 3M ( MMM ), Cummins ( CMI ), and Northrop Grumman ( NOC ).

{kind=link}

Year-to-date, MDV invested $100 million into 10 industrial/manufacturing properties, an investment volume that represents about 27% of its current market capitalization. These acquisitions were completed at a weighted average initial cap rate of 7.7%.

Despite largely funding these acquisitions through capital recycling, MDV generated revenue growth of 7.7% and AFFO per share growth of 3.4% in Q1, which shows that these recycling efforts have been accretive so far.

Despite a common stock price that has languished in the low double digits to mid-teens, MDV has demonstrated an ability this year to issue OP units of its stock at $18 per share for acquisitions.

While net debt to EBITDA of 7.0x sounds a bit on the high side, it's notable that MDV's total debt to total asset value is only 40%, a very healthy ratio.

And the maturity ladder by no means signals trouble ahead:

- $13.2 million mortgage -- 4.5% interest rate -- maturing 3/9/2024

- Credit revolver (fully undrawn) -- 6.7% interest rate -- maturing 1/18/2026

- $170 million term loan -- 5.0% interest rate -- maturing 1/18/2027

- $12.4 million mortgage -- 3.85% interest rate -- maturing 11/1/2029

- $18.9 million mortgage -- 4.85% interest rate -- maturing 1/1/2030

With that said, there are some notable risks to the common stock.

First, the company is tiny at a market cap of only about $105 million and with less than 100 properties owned.

On top of that, the $0.2875 quarterly dividend is only barely covered by Q1 AFFO per share of $0.30.

Lastly, MDV's single-tenant office properties may be operating just fine and current on contractual rent, but MDV is trying to sell them in a very difficult environment for office real estate. As CEO Aaron Halfacre mentioned on the Q1 conference call, "office" is basically a six-letter curse word in the world of commercial real estate right now.

Fortunately, MDV has the Series A preferred stock that currently offers an even higher yield than the common stock.

- MDV.PA -- 8.3% yield

- MDV -- 8.2% yield

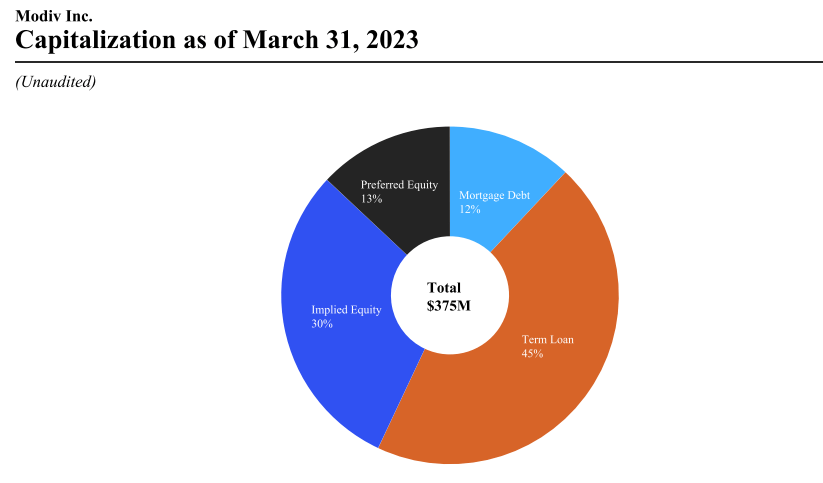

What's more, despite being a tiny company, MDV.PA represents only 13% of total capitalization.

{kind=link}

In Q1 2023, MDV's adjusted EBITDA was $7.5 million, while cash interest expense came in at $2.3 million and $0.9 million in preferred dividends. In other words, MDV.PA's dividends enjoy a 5.65x coverage ratio, or an 18% "preferred dividend payout ratio."

And, of course, remember that MDV has to pay its preferred dividends in full before it can pay a penny toward common dividends.

And management is very motivated to keep paying the common dividends. Insiders have been buying more and more shares of MDV as the stock price has dropped.

MDV.PA's redemption date comes in September 2026, which gives investors almost 3.5 years before management even becomes able to redeem preferred shares at the $25 par value.

As of this writing, MDV.PA has about 12% upside to par value. Adding that to the yield of 8.3% should provide a total return of 11-12% per year.

Bottom Line

While yield used to be very scarce just 3-4 years ago, now investors have ample high-yield opportunities available to them.

That doesn't mean every high yield stock or preferred stock is a good buy. Just look at the office REITs (and REIT preferreds) that have cut their dividends recently. Selectivity is key in every form of capital investment, including preferreds.

For income investors on the hunt for both 8%+ yields and safety, we think you could do a lot worse than the two REIT preferred stocks above. We own several such opportunities in our Retirement Portfolio at High Yield Landlord.

For further details see:

8% Yielding 'Strong Buy' REIT Preferred Shares