EGHT - 8x8: Business Model Looks Potentially Unsustainable

2023-09-27 10:30:17 ET

Summary

- 8x8 should have been one of the major beneficiaries of the global lockdown due to the pandemic, but the company failed to absorb huge tailwinds.

- The secular trend I do not like much in the company's financial performance is shrinking profitability despite massive revenue growth.

- My valuation analysis suggests the stock is overvalued with a double-digit downside potential.

Investment thesis

8x8 ( EGHT ), in theory, should have been one of the primary beneficiaries of the global lockdown due to the COVID-19 pandemic. However, the company's financial performance in 2020-2021 suggests that it failed to absorb huge temporary tailwinds, and its balance sheet became very weak in these years. Now that workers are returning to offices, the company's future growth prospects look cloudy. The recent financial performance demonstrated solid improvement in profitability metrics, but they are still far from enough to improve the balance sheet, notably even during the next multiple quarters. Moreover, the valuation looks very unattractive. All in all, I assign EGHT a "Sell" rating.

Company information

8x8 offers software based on a global cloud communications platform in various areas as a service to its clients. EGHT delivers its platform to clients on a SaaS basis.

The company's fiscal year ends on March 31 with a sole reportable segment. EGHT disaggregates its revenue by geographic areas. According to the latest 10-K report , about 30% of the company's sales were generated outside the U.S.

Financials

The company demonstrated stellar revenue growth over the past decade, compounding annually by 21.5%. On the other hand, EGHT's profitability metrics deteriorated despite the business scaling up notably over the decade. When I see a company with revenue and profitability metrics moving in opposite directions, I start having doubts regarding the viability of its business model. That is a big red flag to me.

{kind=link}

The latest quarterly earnings were released on August 8, when the company missed consensus estimates. Revenue declined by 2.3% YoY, but the adjusted EPS expanded from $0.09 to $0.13. Relative strength in the bottom line was due to the expanded gross and operating margins. The gross margin reached 70%, while the operating margin is now close to zero after -14% in the same quarter last year. The profitability metrics improved due to the management's focus on cost efficiency, which is a good sign for investors.

Seeking Alpha

Despite demonstrating notable improvement in profitability in the latest reportable quarter, the company's free cash flow [FCF] margin is still modest, and it does not allow for substantial improvement in the balance sheet, which suffered a lot in recent years of volatile profitability and profoundly negative FCF margin in FY 2019-2021. EGHT is in a substantial net debt position, far beyond a hundred percent leverage ratio. While the current liquidity looks sound, I still consider the company's balance sheet weak. That might be a problem for future growth.

Seeking Alpha

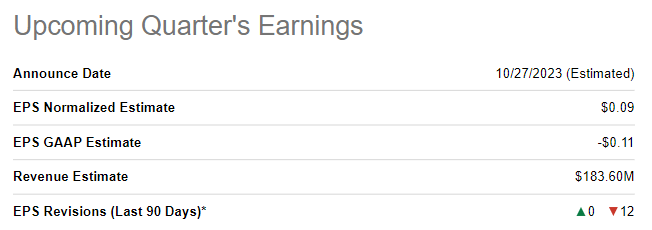

The upcoming quarter's earnings are scheduled for release on October 27. Consensus estimates forecast quarterly revenue at $183.6 million, which indicates a 2% YoY revenue decline. The adjusted EPS is expected to decline sequentially from $0.13 to $0.09. I would also like to underline that there were 12 downward EPS revisions in the last 90 days.

{kind=link}

Overall, I do not like secular trends in the business's financial performance. A 21.5% revenue CAGR for the last decade looks very impressive, but it looks like growth for the sake of growth to me. Not the growth to build long-term value for shareholders. That said, I believe there is a high probability that the company's business model is unsustainable and not economically viable. The recent improvement in profitability despite declining revenue might look solid. However, it does not impress me since profits still look far from enough to improve the company's balance sheet to prepare for fueling the next impressive long-term revenue rally.

As a cloud communication platform, the company's one-in-a-century growth opportunity, the pandemic, has gone. According to Forbes , nine out of ten companies in the U.S. will require employees to Return to the office. That means that a huge momentum for the company has gone. I would also like to underline that EGHT's worst years from a profitability metrics point of view were in the pandemic years of 2020 and 2021. That is also a big red flag to me because the company could not absorb massive tailwinds, which indicates the weakness of the business model.

Valuation

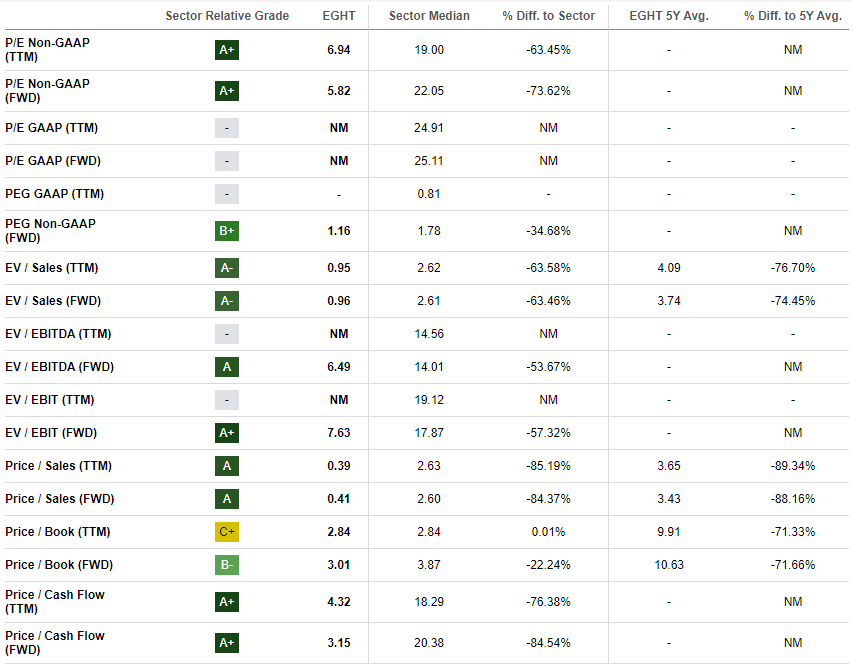

The stock's price plunged 43% year-to-date, a significant underperformance compared to the broader U.S. market. Seeking Alpha Quant assigns the stock a solid "B+" valuation grade with multiples substantially lower than the sector median and historical averages.

{kind=link}

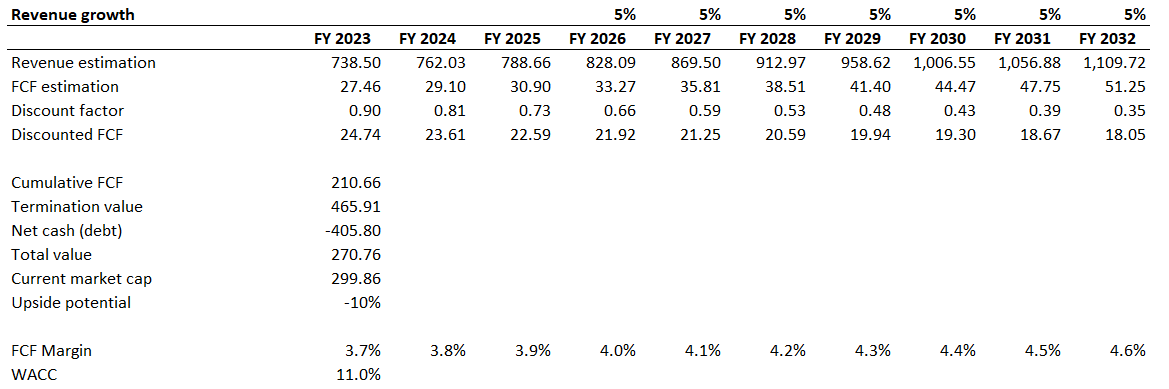

The company has not paid cash dividends on its common stock yet and does not plan to pay any in the foreseeable future. Therefore, I will continue my valuation by simulating the discounted cash flow [DCF] model. I will discount at an elevated 11% WACC since the company’s financials were volatile historically. I have revenue consensus estimates up to FY 2026 and project a 5% CAGR for the years beyond. I use a TTM FCF ex-SBC margin, which is at 3.7%, and expect it to expand by ten basis points yearly.

{kind=link}

According to my simulation, the business's fair value is approximately $270 million, which is about 10% lower than the current market cap. The stock is about 10% overvalued, with a fair price of $2.25.

Risks to consider

As a growth company, EGHT faces substantial risks of not delivering the projected growth trajectory. The company's revenue growth in the past decade has been impressive, and many investors expect EGHT to continue delivering the same growth pace. But consensus estimates forecast a substantial revenue growth deceleration. Despite modest revenue forecasts, the company still can underperform its actual revenue growth, highly likely leading to investor disappointment and a stock sell-off.

It is also crucial to underline an unfavorable trend of the escalating net debt over recent years. Substantial net debt growth poses significant challenges to the company's financial planning since a considerable portion of profits is allocated to servicing its debt. This limits further business development and expansion opportunities. The mounting debt also increases the risks of not weathering adverse macroeconomic conditions.

Bottom line

To conclude, EGTH stock is a "Sell". The company could not absorb its massive tailwinds due to the COVID-19 pandemic, and it was a "once-in-a-century" opportunity for the company to expand its business and profitability, in my view. However, historical financial performance suggests that the company failed to deliver strong results even in a favorable environment. Future revenue growth prospects look cloudy, and the balance sheet is weak. Moreover, the valuation does not look attractive.

For further details see:

8x8: Business Model Looks Potentially Unsustainable