EGHT - 8x8 Inc.: A Compelling Investment In SaaS?

2023-09-27 10:43:46 ET

Summary

- 8x8, Inc. distinguishes itself in the SaaS landscape with innovative AI/ML integrations, strategic alliances, and notable acquisitions.

- The company has a strong financial profile, with a robust FCF, low debt, and an attractive valuation.

- Despite intense competition in the SaaS communication solutions sector, 8x8, Inc. focuses on margin expansion and operational efficiency for long-term success.

- My DCF valuation model suggests the company is undervalued and has an upside potential of roughly 46.8%.

In the SaaS landscape, 8x8, Inc. ( EGHT ) distinguishes itself with its innovative AI/ML integrations, strategic alliances, and notable acquisitions such as Fuze . This article will analyze EGHT, highlighting its robust financials, operational advancements, and unique positioning amidst intense competition. While industry giants and burgeoning startups dominate the SaaS communication solutions domain, 8x8, Inc. has successfully established a significant presence. Given its trajectory and valuation, I posit that EGHT presents a compelling investment opportunity with a bullish outlook.

Business Overview

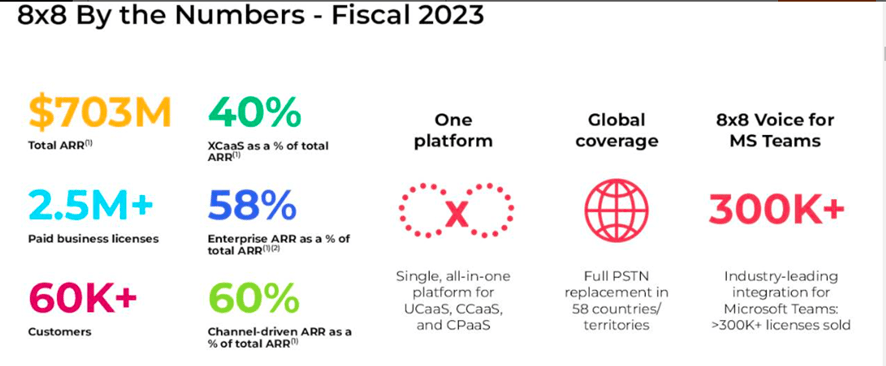

8x8, Inc. provides a cloud-native communications platform called XCaaS (eXperience Communications as a Service), which integrates tools like voice communications and video meetings tailored to businesses. The company has successfully garnered revenue by serving over 60,000 customers across 180 countries, boasting over 2.5 million paid business licenses. I believe that EGHT's distinct edge in the market arises from its capacity to provide real-time business analytics across multiple channels, enhancing user experiences and offering valuable data-driven insights. Their recent collaboration with OpenAI in fiscal 2023 adds an intriguing AI aspect to their services, which, in my opinion, holds significant potential for the future.

Hence, EGHT is uniquely in a sector where agility and innovation are crucial. The company's strategic acquisition of Fuze and partnerships with industry leaders like Microsoft ( MSFT ) highlight its commitment to expanding its market footprint and fostering rapid innovation. Financially, EGHT has a robust balance sheet that provides ample liquidity, especially in uncertain economic climates. EGHT has $137.6M in liquid assets as of June 30, 2023. Its balance sheet indicates total assets standing at $828.5M. Notably, current assets have seen a marginal uptick to $274.5M from $273.1M in March 2023. On the liabilities side, there's a noteworthy reduction from $741.9M in March to $723.6M in June 2023. I believe this decrease, driven partly by the strategic repayment of $25M on its term loan, signals prudent financial management.

A Promising Niche Player in SaaS

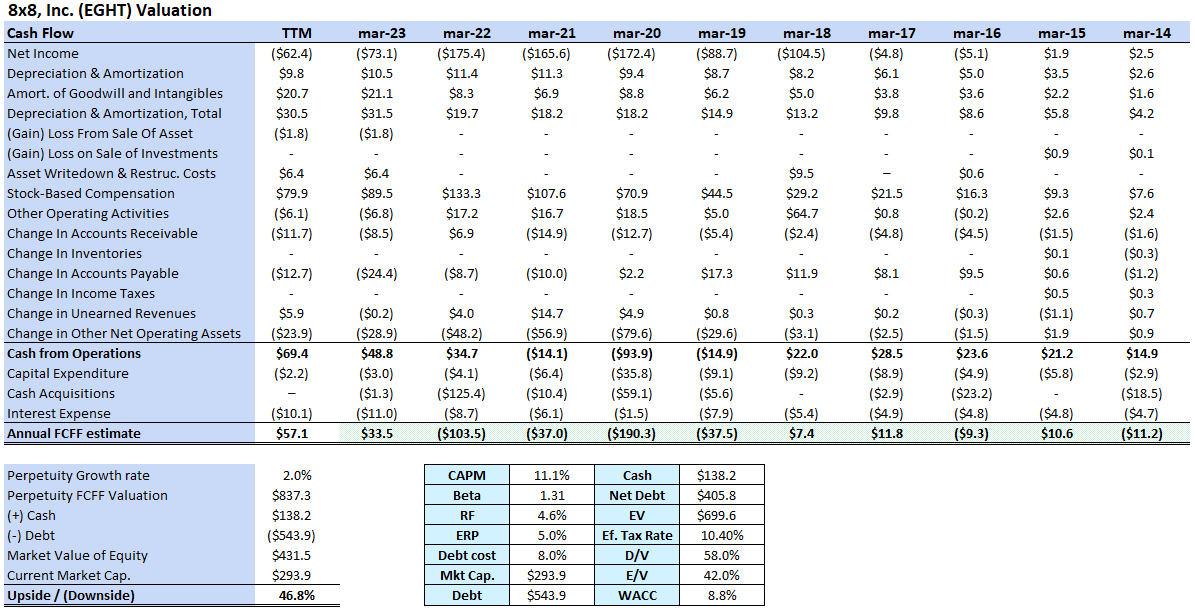

Moreover, compared to its peers, EGHT has a strong FCF profile and a relatively low debt-to-FCF ratio , underscoring its financial stability. Looking at its historical figures , I believe EGHT's FCF run rate could easily sustain at least $50 to $60 million annually, further emphasizing its financial strength (more on this later). Also, with a market capitalization of $293.9 million and an enterprise value of $699.6 million , 8x8, Inc. appears to be trading at an attractive valuation.

{kind=link}

Path to profitability

Furthermore, EGHT has showcased significant operational efficiency strides over recent years, underscored by its improved financial metrics . A key indicator of this progress is the company's EBIT margin. In December 2020, EGHT reported a concerning EBIT margin of -25.79%. Fast forward to June 2023, and this metric has seen a commendable turnaround, approaching break-even at -0.77% of total revenues. This transformation highlights the company's focused efforts refining its operations and indicates a clear trajectory toward operational profitability. Such a shift aligns with the management's goal of prioritizing sustainable profitability over mere topline growth.

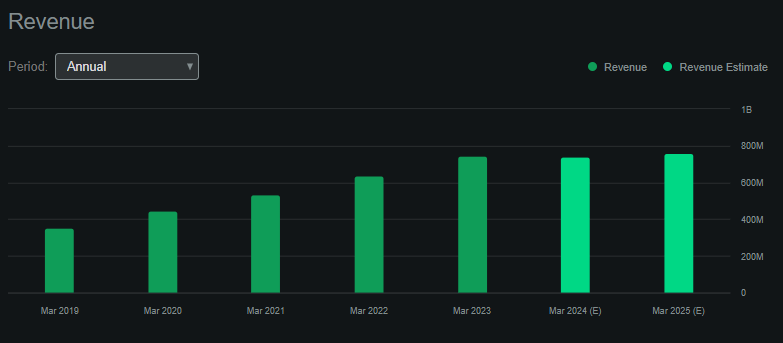

However, it's essential to contextualize these internal achievements against the broader industry backdrop. The SaaS communication solutions sector is marked by intense competition. Zoom ( ZM ) has expanded beyond its video conferencing roots to offer services like Zoom Phone and Zoom Chat , directly competing with 8x8's voice communications and team collaboration tools. Alphabet's ( GOOG ) Google Meet and Google Chat , part of the broader Google Workspace, offer integrated solutions that challenge 8x8's XCaaS platform. Meanwhile, Amazon ( AMZN ) brings Amazon Chime to the table, backed by the robust infrastructure of Amazon Web Services , making it a potential competitor for enterprises already invested in the AWS ecosystem. Given these tech giants' vast resources and brand recognition, they present significant challenges for emerging players like EGHT. This competitive landscape, dominated by Zoom, Alphabet, and Amazon, might contribute to EGHT's seemingly plateauing revenues.

{kind=link}

Examining EGHT's revenue streams, we observe that their service quarterly revenues are at $175.2M, showing a modest decrease from $179.2M during the same period in 2022. While this decline is noteworthy, it's essential to consider that the company has effectively reduced its operating expenses by 13.8%, from $214.4M in 2022 to $184.7M in 2023. This reduction is significant as it has narrowed the net loss from $26M in 2022 to $15.3M in 2023. If EGHT maintains this financial discipline, there's a strong possibility of achieving profitability in the not-so-distant future.

CAPEX and Strategic M&A

While 8x8, Inc. ((EGHT)) shows promise as a potential FCF machine in the future, its CAPEX caught my attention. A particular concern is the evident depreciation of its property, plant, and equipment (PPE). In particular, Net PPE has declined from $173.3 million in March 2020 to $105.0 million by June 2023. This decline signals potential upcoming CAPEX needs when contrasted with a $94.3 million increase in accumulated depreciation during the same timeframe. If not proactively addressed, this could necessitate substantial financial commitments in the future for asset maintenance or replacements, possibly explaining EGHT's relatively healthy FCF.

{kind=link}

Hence, EGHT's noticeable decrease in PPE and the uptick in accumulated depreciation indicate that its assets are aging, which may soon necessitate either increased maintenance or complete replacements. Having a state-of-the-art infrastructure is essential in the dynamic SaaS communication domain. Aging infrastructure can lead to operational inefficiencies, potential service disruptions, and heightened security vulnerabilities. This is why I believe 8x8, Inc. may eventually have to raise its maintenance CAPEX, whether upgrading servers, enhancing data protection, or adopting new communication technologies. Their extensive global operations, with centers in various countries, suggest a potential need for capital to expand or upgrade these facilities. Moreover, M&A often demands additional capital for integration and alignment. But currently, it seems these CAPEX are not happening, which investors need to monitor in the future.

But other than that, EGHT’s financials appear solid and position it favorably for strategic M&A transactions. The acquisition of Fuze, Inc. is particularly interesting because of its enterprise cloud-based communications offerings. The price tag was an estimated $250 million in stock and cash. But strategically, this move enhanced 8x8's product portfolio and strengthened its XCaaS profile. Dave Sipes, the CEO of EGHT, has articulated the company's vision to integrate the best of both platforms. But more importantly, EGHT reaffirmed its ambition to broaden its enterprise clientele, solidify its global footprint, and aim for an aspirational target of $1 billion in annual revenues. While I believe this revenue milestone might seem ambitious in the near term, it underscores the management's forward-looking strategy and commitment to growth.

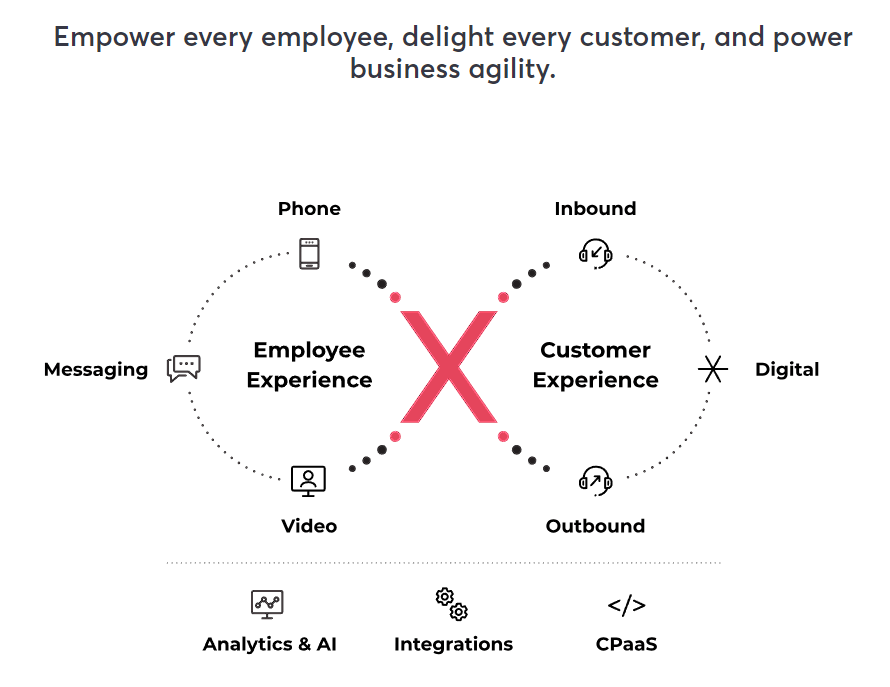

Indeed, I think integrating Fuze's capabilities will likely facilitate a smooth transition for enterprises from traditional on-premises systems to a comprehensive, single-vendor cloud solution. This solution would encompass contact centers, voice communications, team chats, video meetings, and CPaaS embeddable APIs. By bridging the gap between Unified Communications as a Service (UCaaS) and Contact Center as a Service (CCaaS), 8x8, Inc. is positioning itself to elevate employee and customer experiences, which should streamline customer interactions. So, as a whole, I think EGHT's product suite and competitive edge improved, which is a testament to management's savvy strategic thinking.

Investment Perspective

Fiscal 2023 marked a noteworthy milestone for 8x8, showcasing a 16.6% surge in total revenue. Yet, it's imperative to note that, excluding Fuze's contribution, the growth would stand at a conservative 3%. This underscores the transformative impact of strategic M&As on growth trajectories, but it also shows that EGHT's revenue growth would have been negligible without it.

In assessing EGHT’s valuation, I've based my assumptions on the company's historical performance and prevailing economic trends. I've selected a 2% perpetuity growth rate, which aligns with standard GDP growth, particularly in light of EGHT's present revenue pattern. Utilizing the CAPM, I've used the 10-year yield as the risk-free rate, a common practice in financial evaluations. Historically, EGHT has obtained financing at rates between 1.2% and 11.0%. Given the current trend of rate increases and EGHT's existing debt profile, I believe that an 8% cost of debt is a pragmatic projection for the future. I've also treated the company's recent free cash flow as a perpetuity. In my view, this approach is prudent, as it might be overly optimistic to anticipate significant growth based on EGHT's recent trajectory.

Seeking Alpha plus author's elaboration

{kind=link}

According to my model, EGHT appears to be trading at an attractive valuation. Based on these calculations, I believe EGHT might offer an upside potential of up to 46.8%. When combined with the company's financial stability, operational efficiency, and strategic direction, this potential suggests that EGHT could be a sound investment opportunity. Given its current trajectory and what I view as a favorable valuation, I rate EGHT as a "buy" with a positive outlook.

{kind=link}

Conclusion

8x8, Inc. has demonstrated a steady capability to adapt and innovate within the SaaS industry. Through its strategic collaborations, M&A endeavors, and focus on operational efficiency, EGHT has secured a notable presence in the market. While the company faces challenges from its competitive landscape and potential CAPEX concerns, its acquisition of Fuze, Inc. is a testament to its forward-thinking approach. This acquisition and EGHT’s operational improvements suggest a promising direction for the company. Based on my valuation model, I believe there's a 46.8% upside potential for EGHT. Hence, given its history of adaptability and strategic moves, 8x8, Inc. presents a compelling investment opportunity at its current price levels.

For further details see:

8x8, Inc.: A Compelling Investment In SaaS?