REG - 9.5%-Yielding CTO Realty Looks Appealing Near 52-Week Low

2023-10-09 08:10:00 ET

Summary

- CTO Realty Growth offers an attractive opportunity with a 9.5% dividend yield and potential from value-add activities.

- The company has a track record of dividend growth and internal growth drivers that could mitigate risks.

- Risk-tolerant investors may want to take a look at CTO while being mindful of its higher leverage.

REITs are not a popular place to be right now in the investment world, given their perceived risks around higher interest rates. That's why many of them are trading at 52-week and even multi-year lows.

However unpopular they may be, this creates long-term opportunities for patient investors willing to wait out the current rate cycle, all the while getting paid a high yield.

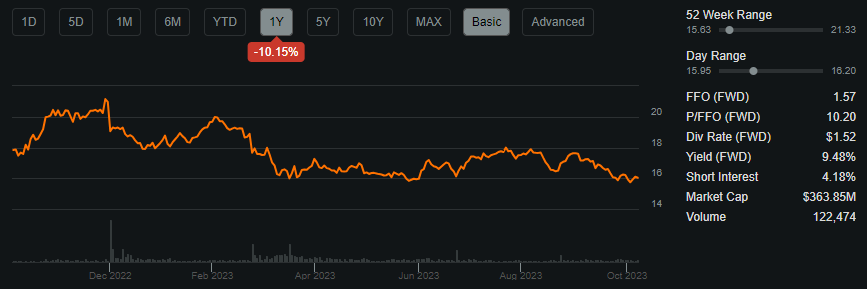

This brings me to CTO Realty Growth ( CTO ), which I last covered here back in April with a 'Buy' rating. CTO hasn't been one of my best performers, with the stock declining by 4.6% since my last piece, but thanks to dividends, the total return is flat, meaning that investors haven't lost anything unless they sold during this time period.

At present, the stock sits at the low end of its 52-week range and pays a 9.5% dividend yield. In this article, I discuss the CTO's operating fundamentals and why it's an appealing buy at present for high income, so let's dive in!

{kind=link}

Why CTO?

CTO Realty Growth is a self-managed REIT with focus on owning and acquiring high-quality retail real estate across the U.S. Unlike Net Lease REITs that simply shepherd deals through the pipeline each year, CTO adopts a more roll-up-their sleeves approach, seeking to buy properties that are well under market value and performing value-added activities to 'lease-up' the properties.

At present, CTO carries a $1 billion enterprise value with an asset base that includes 24 properties covering 4.2 million square feet. It also has a $39 million stake in the Net Lease REIT, Alpine Income Property Trust ( PINE ), acting as its external advisor and resulting in an additional steady income stream for CTO.

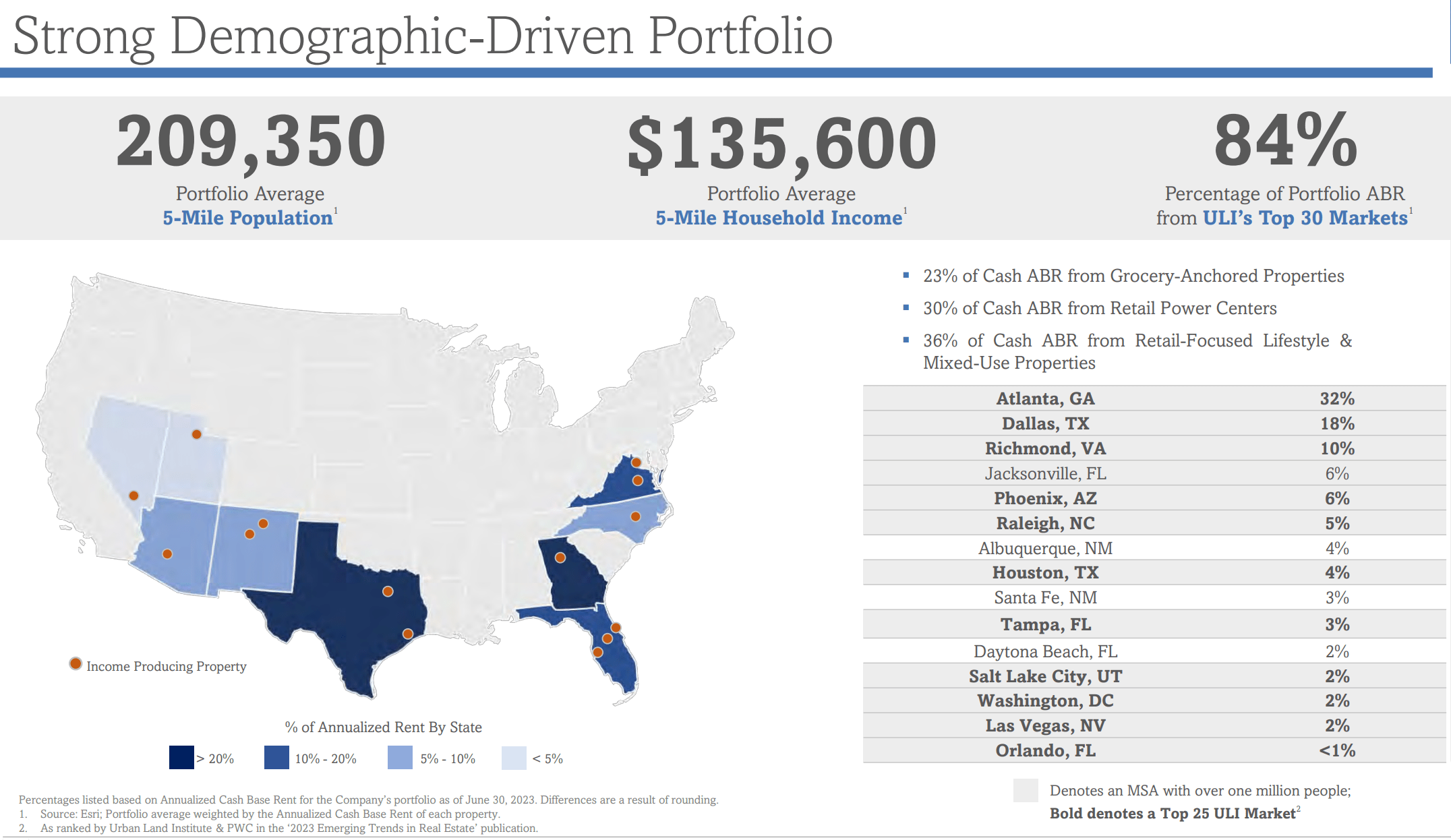

CTO is focused on markets that have outsized job and population growth with favorable business climates. Its properties are focused on retail-based, multi-tenanted assets that have grocery, lifestyle, or community-oriented themes. It also has a number of legacy assets that management believes could unlock value as they are sold and proceeds are redeployed into core strategy assets

Most of CTO's properties are located in the growing Sunbelt region of the U.S. It carries a high population density around a 5-mile radius with high average household income. Plus, 84% of its annual rents come from markets that are ranked in the Top 30 by the Urban and Land Institute.

{kind=link}

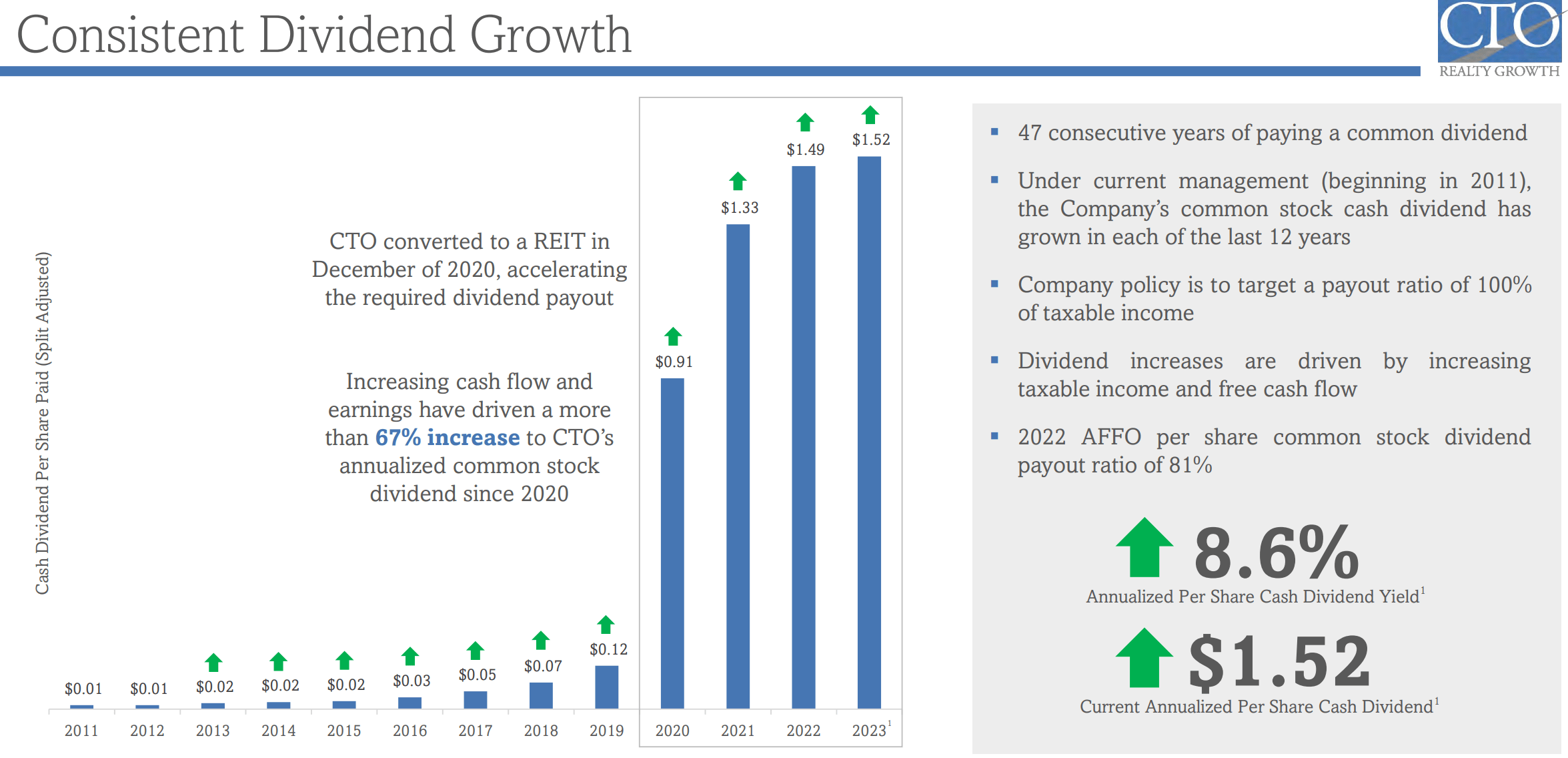

CTO's track record of value creation is reflected by its dividend record, with 47 consecutive years of paying a common dividend. Under the current management team, which began in 2011, CTO's cash dividend has grown every year over the past 12 years. Importantly, CTO's dividend growth is driven by increasing taxable income and cash flow. As shown below, CTO has meaningfully grown its dividend since 2020, when it converted to a REIT.

{kind=link}

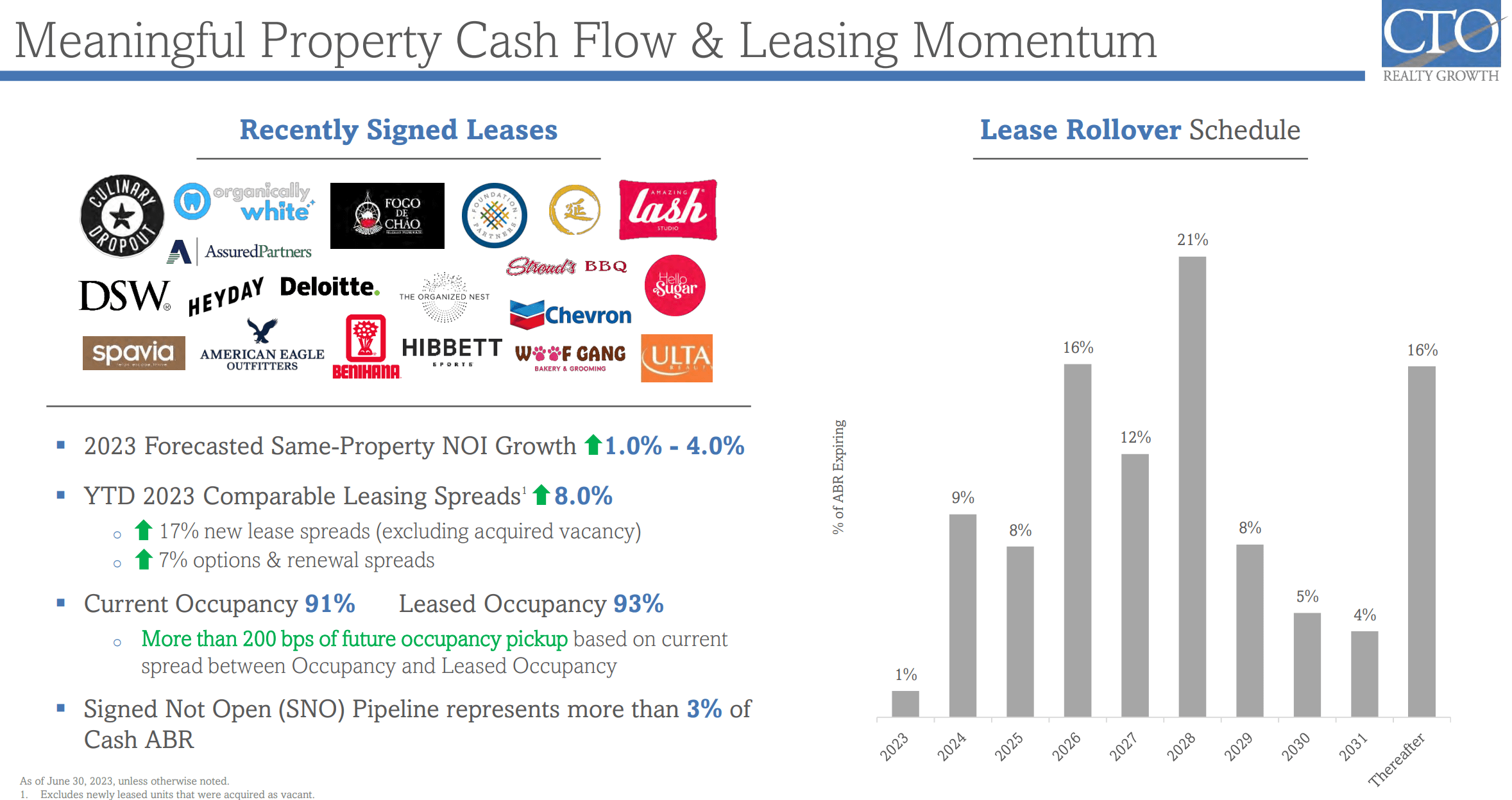

Risks to CTO include the current higher interest rate environment, which makes taking on new debt to fund growth prohibitively expensive. However, CTO does have internal growth drivers, including portfolio recycling. This is reflected by the recent sale of one property for $2.1 million at a 4.8% cap rate while simultaneously investing 3 multi-tenant retain properties at an attractive going-in cash cap rate of 8.0%.

CTO also has a re-development pipeline, including Ashford Lane in Atlanta, which it's repositioning to become a premier lifestyle, shopping and dining center. It also has 2 other recent acquisitions in Atlanta with mixed-use and repositioning potential as well as 1 in Richmond, VA, which is anchored by Whole Foods ( AMZN ).

This property was acquired in late 2022 at $239 per square foot, which management estimates is significantly below replacement cost, and it has 68K square feet of vacancy as of the last reported quarter, which could drive future cash flow. As shown below, CTO has significant lease-up potential over the next few years as leases roll over. This could build upon the 8% cash lease spreads that CTO expects for the current year, driving 1% to 4% same property NOI growth.

{kind=link}

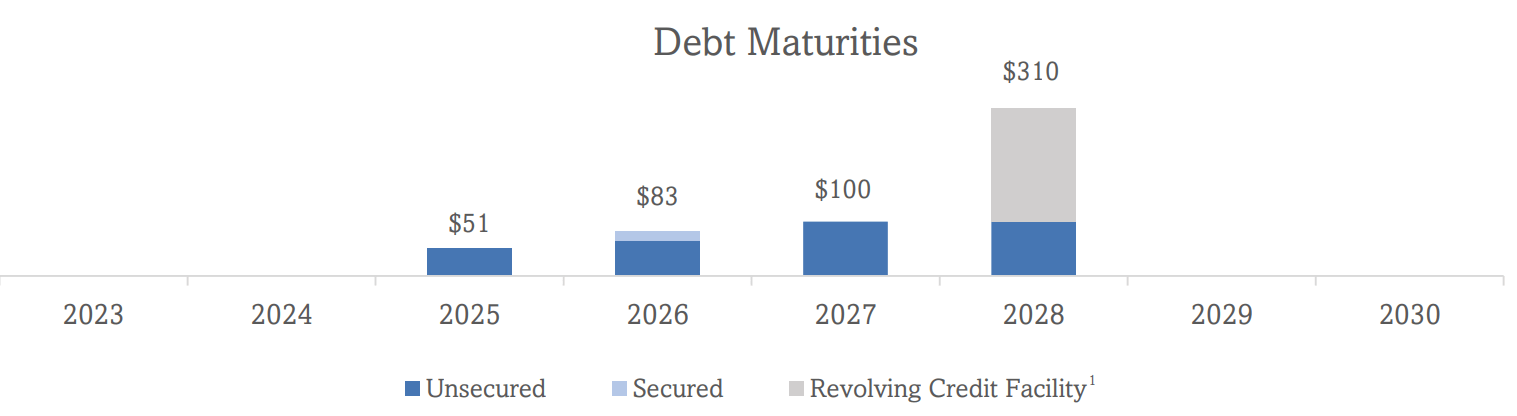

Admittedly, CTO isn't a sleep well at night type of holding, as carries higher leverage with a net debt to EBITDA of 7.9x, sitting above the 6.0x level generally considered to be safe by ratings agencies. However, this could change for the better, as properties in the re-development pipeline begin reaping the benefits through higher tenancy and NOI, and the debt to total enterprise value stands at a more reasonable 53%. As shown below, CTO has no debt maturities until 2025.

{kind=link}

Meanwhile, CTO currently pays a 9.5% dividend yield. While the dividend to AFFO payout ratio is a bit higher than what I'd like to see at 91%. There is potential for that to decline through NOI growth.

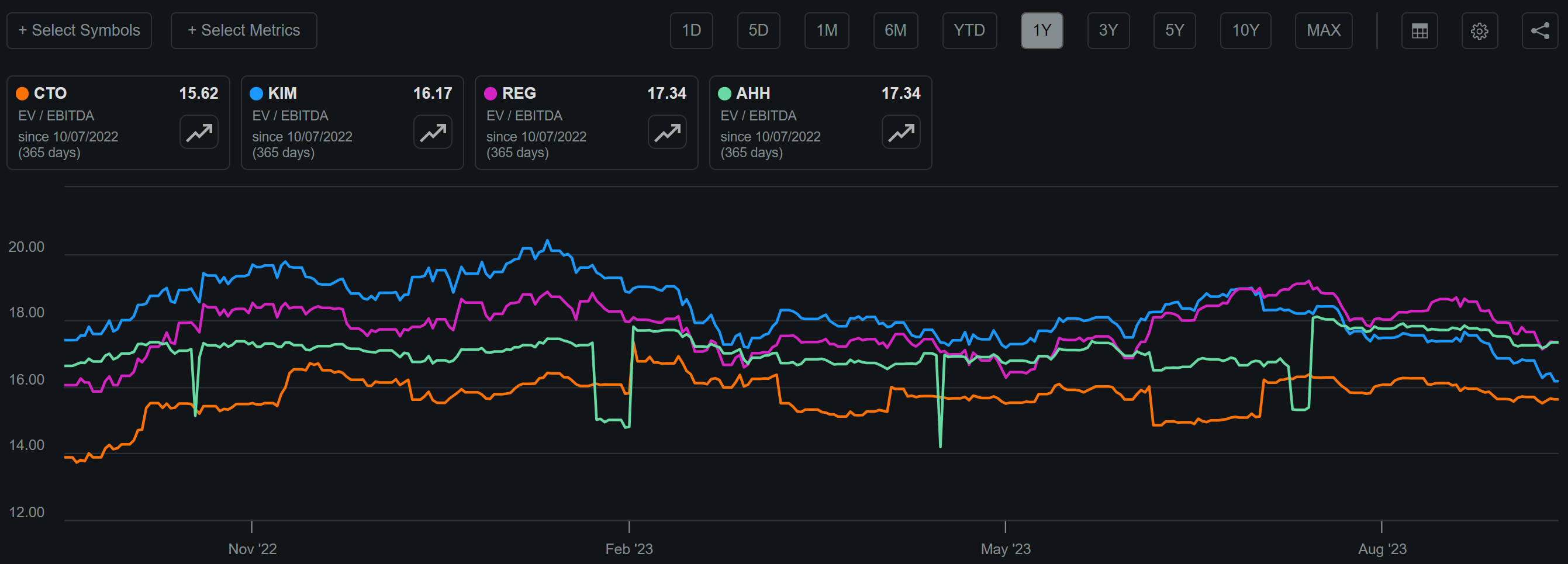

At the current price of $16.03 with a forward P/FFO of 10.2 and a 9.5% dividend yield, investors appear to be well-compensated with the risks in this higher interest rate environment. As shown below, CTO trades at a discount to shopping center REITs Kimco Realty ( KIM ) and Regency Centers ( REG ) as well as diversified REIT Armada Hoffler Properties ( AHH ), with an EV/EBITDA of 15.6

{kind=link}

Investor Takeaway

Overall, CTO Realty Growth presents an attractive opportunity for high income investors seeking exposure to retail real estate with a value-add component. While there are risks associated with higher leverage and potential interest rate increases, the company has a track record of dividend growth and internal growth drivers that could mitigate these risks in the near to medium term, considering that it doesn't have debt maturities until 2025. With a current dividend yield of 9.5% and potential for NOI growth, CTO may be appealing to risk-tolerant investors seeking high income and value.

For further details see:

9.5%-Yielding CTO Realty Looks Appealing Near 52-Week Low