ONL - 9 REITs Blown Apart Holding Serious 2024 Rebound Potential

2023-10-06 17:32:19 ET

Summary

- Sharply higher long-term borrowing costs for real estate during late summer have been a huge headwind for REIT operations and investment valuations.

- The demand for commercial real estate, especially office space, is being questioned with the appearance of stay-at-home living/work trends.

- However, things change. A slower economy into 2024 could reverse interest rates lower and pinpoint a bottom in REIT pessimism.

- Acquiring beat-up REIT names at low valuations soon could prove one of the smartest sector turnaround plays since the oil/gas bust of early 2020.

The commercial real estate market has entered a period of serious turmoil during the sharp 2021-23 rise in interest rates. Real Estate Investment Trusts [REITs] have increasingly come under selling pressure. Worries over rising borrowing costs on one hand, and the reality of falling asset prices on another (especially in the office building sector), have only been compounded by the growing realization no quick fixes are around the corner as a recession approaches. In fact, the unexpected late summer rise in long-term rates in America (those affecting real estate deals and values the most) has really put the screws on the whole ownership valuation argument. At this stage, even the strongest blue-chip REITs like Realty Income ( O ) and Alexandria Real Estate ( ARE ) have sold off by -20% to -30% since July.

And, with stay-at-home work trends a make-or-break perk for employees (perhaps the single most important long-lasting life change from the COVID-19 pandemic), everyone is questioning the need (demand curve) for real estate, again with office building owners under tremendous scrutiny.

Being a contrarian investor and having watched/invested in the market daily since 1986, I have noticed and successfully participated in some of the biggest sector rebounds from monumental busts. I owned and recommended real estate plays at the Great Recession bottom, plus a long list of oil/gas names after the pandemic panic ended in April 2020. The winning formula is to find an industry that has underperformed for a period of at least two years, where wholesale panic selling and near universal thinking believes a return to normal business conditions is all but impossible.

In fact, REITs have now underperformed the S&P 500 by a wide margin fully for five years, back to 2019. In particular office building, shopping center, and hotel portfolio owners have been leaders on the downside. It's not hard to understand why, as individuals have become less likely to leave their homes during the pandemic (myself included).

The next step in identifying specific companies that could rebound substantially 2-3 years into the future is to find selections with incredible value supporting characteristics people are dismissing. When the bottom comes, assuming an up move from worst performance to first in sector capital rotation will almost surely produce amazing rewards for those with backbone.

For example, many beaten down left-for-dead real estate-related companies rose to amazing heights for investment returns between early 2009 and 2010. Again, "going out of business" oil buys in the middle of 2020 turned into the most desired/attractive to own of all equities by investors during the Russian invasion of Ukraine in early 2022. I am not kidding, gains of +500% to +1,000% became reality for those willing take on an enormous amount of what I call "implied" risk (under flawed conventional wisdom assumptions).

The one constant on Wall Street in particular is things change. You have to parse the difference between implied risk and actual real-world risk. Today, if the economy goes into a freefall real estate recession, no doubt a majority of REITs will have to sell off properties well under accounting book value cost. Sure, excessive leverage during a period of sharply higher interest rates could push many REITs into insolvency.

However, you have to remember, interest rates will fluctuate next year. Perhaps they will go down appreciably with a slowing economy. Another positive for large portfolio firms is debts can be paid down by selling individual properties. Time can be bought waiting for an eventual real estate turnaround by slashing dividends and putting off building rehab plans (reducing capital expenditures). In dire straits, new trust units might be offered, mergers and partnerships might be entered, etc. to prevent bankruptcy and a zero price for REIT shareholders.

Anyway, I have been spending more of my time each week hunting for some interesting REIT turnaround ideas. There are literally hundreds of names that look like decent long-term investments today. In addition, if we get one final large down move with a general U.S. stock market tank into the end of 2023, I will wager an important cycle bottom for REITs could materialize. Why? Because already low REIT valuations will become incredibly cheap, likely rivaling the Great Recession bottom. At the same time, pressure will be put on the Federal Reserve to aggressively reverse tightening policies and actually ease credit conditions with a new round of QE and far lower bank interest rates. A combination of these two factors could easily open up the exact timing when REITs become the most attractive sector of all to own.

My Seeking Alpha REIT Screen

I ran a screen last night using this website's basic sorting tool available to premium subscribers. Here are the real estate-focused results of my cross between a strong overall Valuation Factor Grade of "A" with low price to sales, cash flow, and book value. A high dividend yield was also part of the criteria, above 5% on a trailing basis.

Seeking Alpha - Stock Screener - Looking for Cheap REITs

{kind=link}

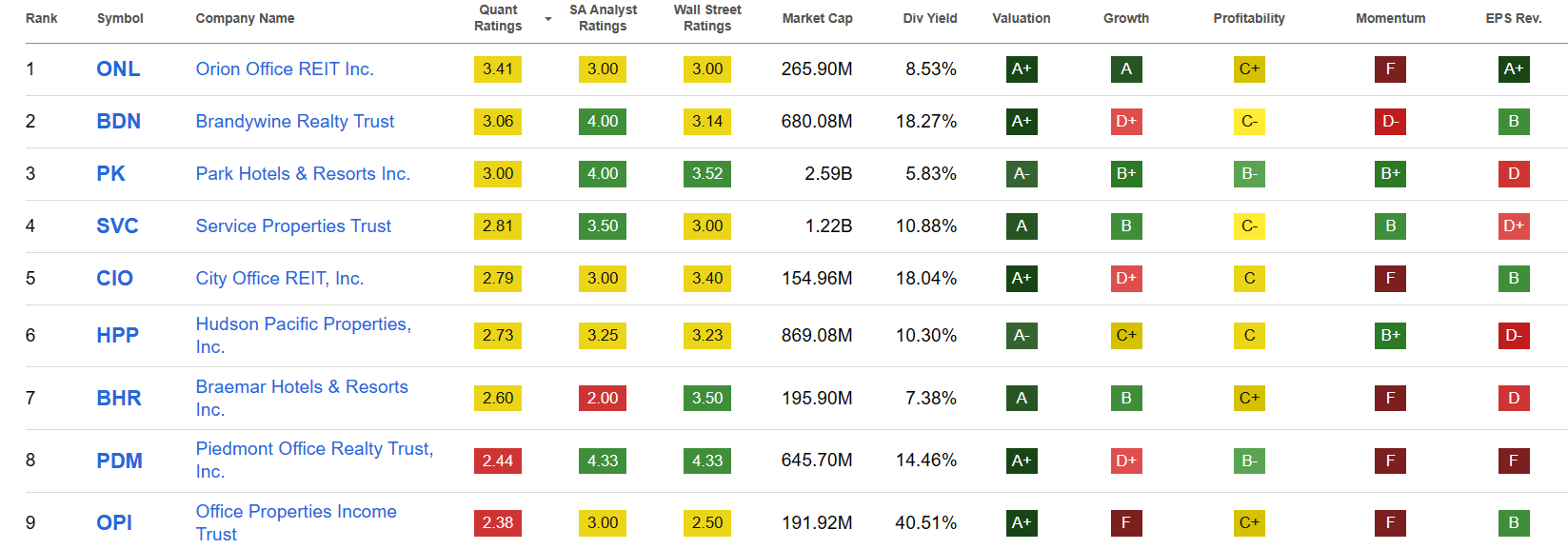

The results came back with 9 REIT names to research further. For me, this basic screen list is representative of the types of fundamentals to grab at a major sector bottom in pricing. The group (sorted for order by SA's Quant Rating for momentum) includes Orion Office ( ONL ), Brandywine Realty ( BDN ), Park Hotels ( PK ), Service Properties ( SVC ), City Office ( CIO ), Hudson Pacific Properties ( HPP ), Braemar Hotels ( BHR ), Piedmont Office Realty ( PDM ), and Office Properties Income ( OPI ).

Seeking Alpha - Stock Screener - Cheap REIT Sort Results

{kind=link}

The whole group has performed quite poorly for total returns over the last two years (including above-average dividend payouts), the minimum length of time for my starting point to look for a sector-wide reversal.

YCharts - Sorted REIT Picks, Total Returns, 2 Years

I have drawn some direct comparison charts of the fundamentals I used in the search, including price to sales, cash flow, and book value. Each is already quite inexpensive and could become even cheaper if an exhaustion panic move is next. You will notice the group keeps getting cheaper and cheaper over the last 12 months, despite only a small dip in actual operating results. Bears will say the group is discounting a rotten future, although such is not guaranteed.

YCharts - Sorted REIT Picks, Price to Trailing Sales, 1 Year

YCharts - Sorted REIT Picks, Price to Trailing Cash Flow, 1 Year

YCharts - Sorted REIT Picks, Price to Book Value, 1 Year

Individual Company Summaries

One of the ways you can tell REITs are quickly morphing into the most hated and despised sector on Wall Street is high/rising short interest selling levels. The investing masses (including analysts, brokerages, hedge funds, financial experts, and retail investors) are all coming to the same conclusion: REITs can only decline in price.

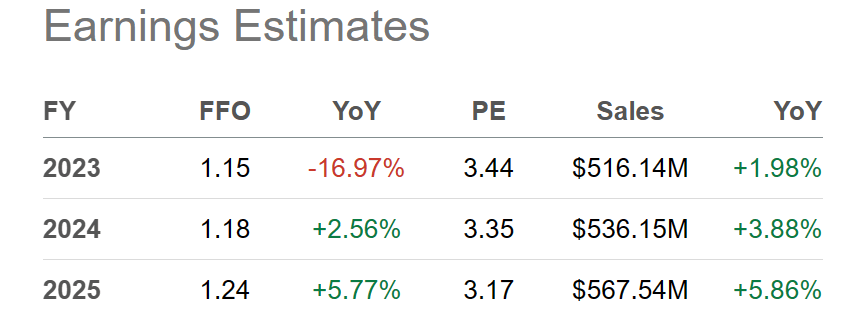

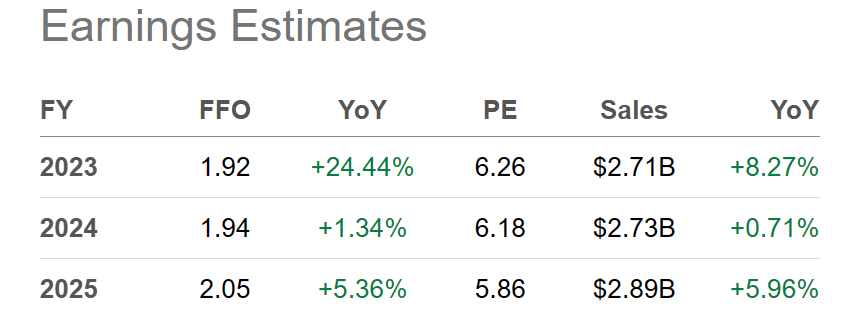

Despite trading well below book values and paying some of the highest dividend yields in the marketplace, fewer and fewer investors want to own them. A sobering fact for those rushing to sell is all but 1 of the 9 REITs are trading at "forward" price to FFO (funds from operations) ratios under 5x. And, several are trading under 2x "free" cash flow generation. Conversely, if artificial intelligence [AI] dreams and hopes are involved, technology stocks can trade at 30x to 50x earnings and free cash flow. These are the two emotional extremes (fear/greed) front and center for investors to contemplate.

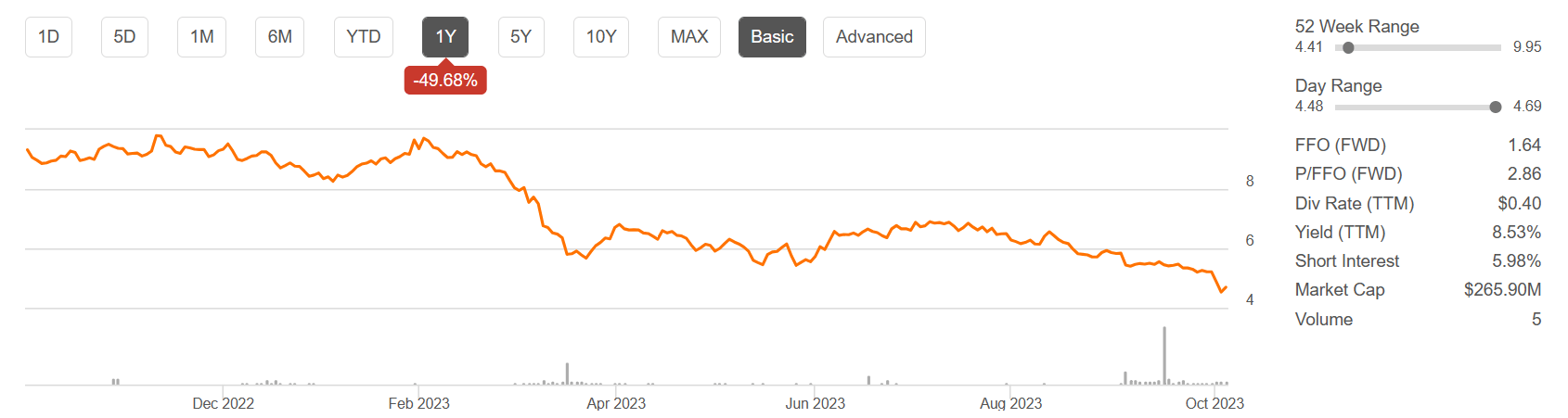

A 1-year price/volume graph of daily action, forward dividend yields, short interest positioning and FFO forecasts by Wall Street experts are presented for each REIT below.

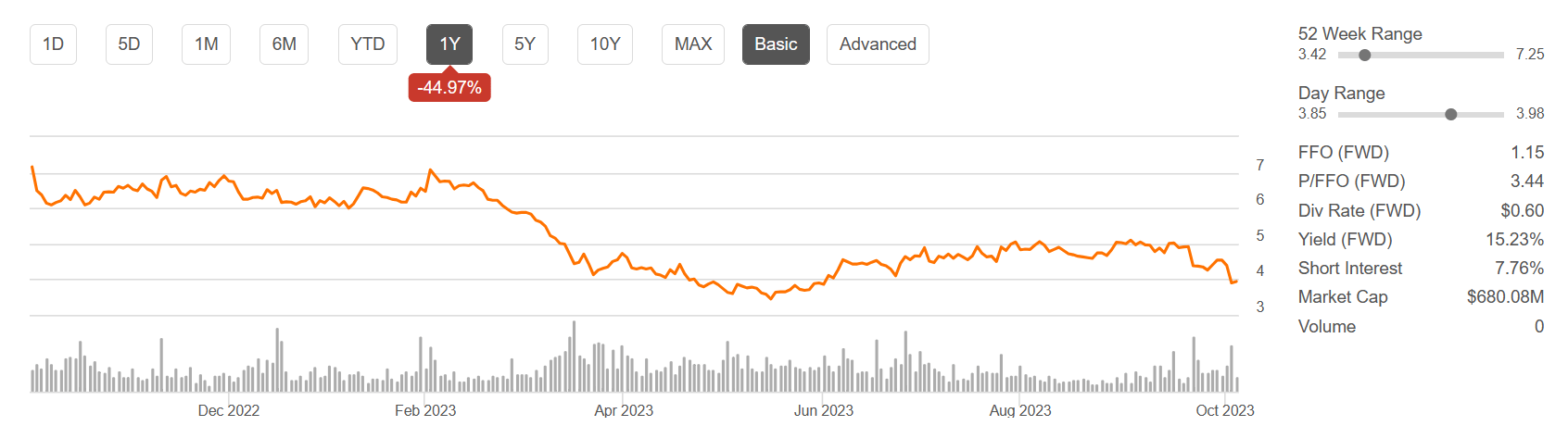

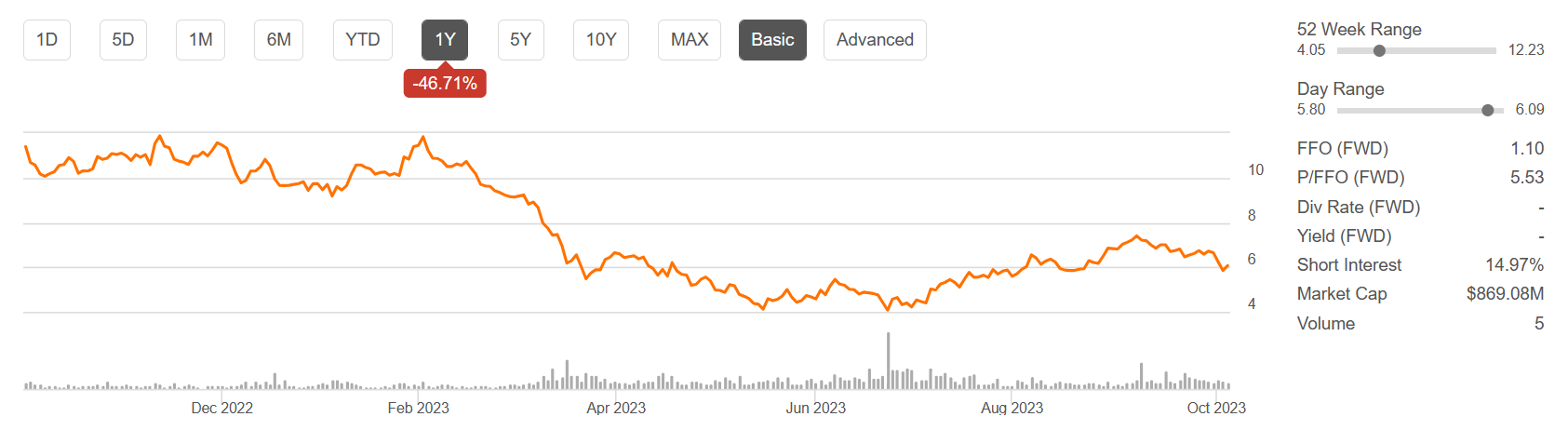

Orion Office

Orion owns office buildings all over America, with its largest concentration in the southern Sun Belt states with Texas #1 for asset concentration. Its top two tenants are the federal government and Merrill Lynch . From the company website ,

The Orion portfolio consists of 81 wholly-owned properties and 6 unconsolidated Joint Venture properties diversified by tenant, geography and industry. None of Orion's tenants represent more than 12.4% of the portfolio by ABR. The diversity of Orion's portfolio and the high credit quality nature of the tenancy are expected to provide the company with a strong, stable source of recurring cash flow from which to grow the business.

The portfolio is cycle-tested and its rent collection rate during the pandemic demonstrates the creditworthiness of the tenant base and our ability to continue to occupy these key office locations. The portfolio has 73.7% investment grade tenancy by ABR as of June 30, 2023.

I will say Orion appears to be using the least amount of financial leverage on its balance sheet of the 9 sort names returned. However, using less debt has not exactly prevented the stock from sliding this year.

Seeking Alpha - Orion Office, Basic Data Set & 1-Year Chart

{kind=link}

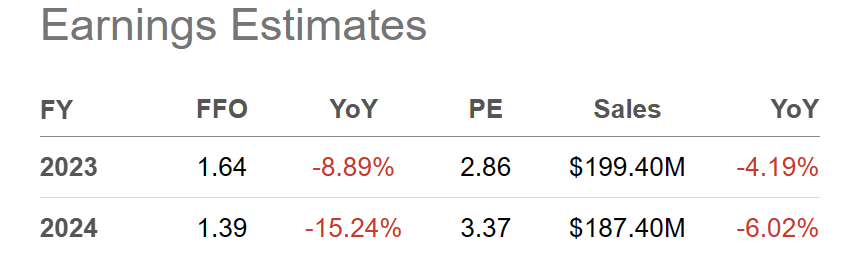

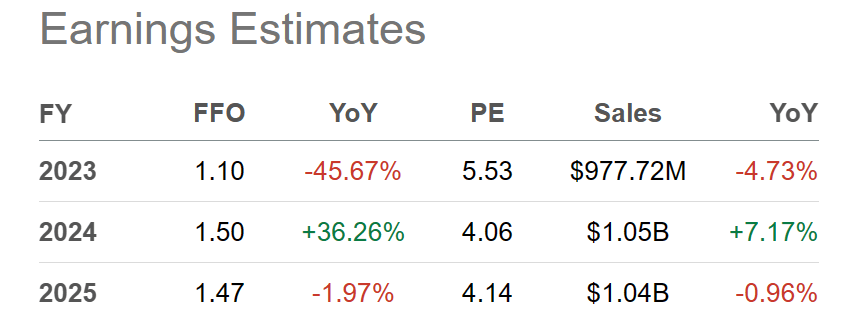

Seeking Alpha Table - Orion Office, Analyst Estimates for 2023-24, Made October 4th, 2023

{kind=link}

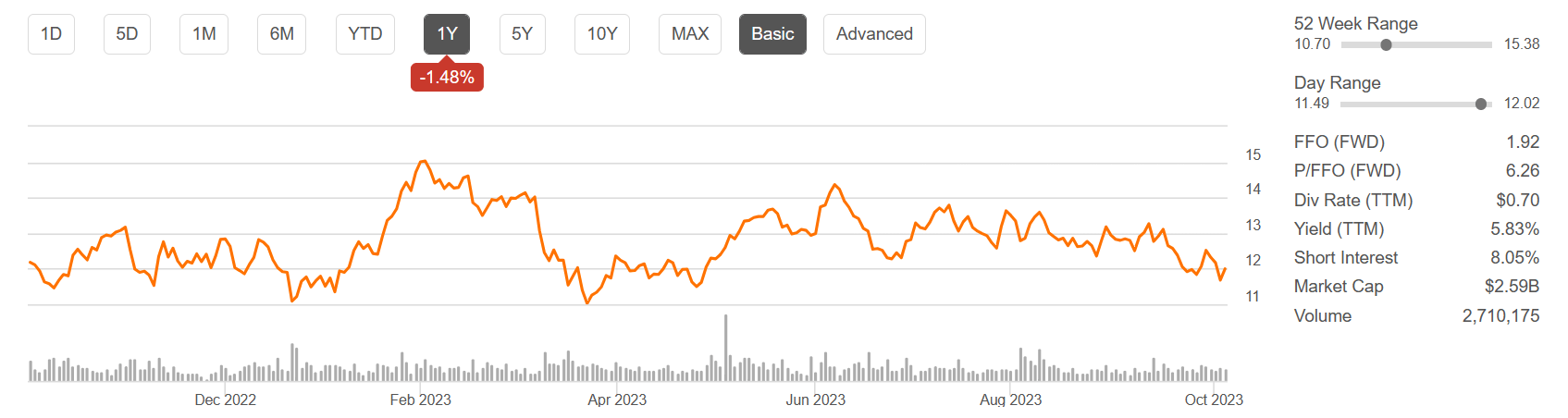

Brandywine Realty

Brandywine's primary ownership focus for its office buildings are Philadelphia, PA, Washington DC, and Austin, TX. 24 million square feet of space is owned in total, while $2.6 billion in development projects are in process or under construction. BDN has been in business for 25 years. From its website ,

Organized as a real estate investment trust, we own, develop, lease and manage an urban, town center and transit-oriented portfolio. Our purpose is to shape, connect and inspire the world around us through our expertise, the relationships we foster, the communities in which we live and work, and the history we build together. Our deep commitment to our communities was recognized by NAIOP when we were presented with the Developer of the Year Award - the highest honor in the commercial real estate industry.

Seeking Alpha - Brandywine, Basic Data Set & 1-Year Chart Seeking Alpha Table - Brandywine, Analyst Estimates for 2023-25, Made October 4th, 2023

{kind=link}

{kind=link}

Park Hotels & Resorts

Park owns 45 premium-branded hotels and resorts, with 29,000 rooms. 88% of the clientele served are considered luxury and upper-scale markets. The vast majority of properties are Hilton- branded, followed by Hyatt , Double Tree and several other high-end names. Many are located in major cities across America like New York, Boston, Chicago, San Francisco, Seattle, and New Orleans. The largest concentrations are in Florida and Hawaii.

My favorite picture of the company website is of the Hilton Hawaiian Village - Waikiki Beach Resort, with 2,860 rooms.

Park Hotels Website - Hilton Hawaiian Village - Waikiki Beast Resort

{kind=link}

Seeking Alpha - Park Hotels, Basic Data Set & 1-Year Chart Seeking Alpha Table - Park Hotels, Analyst Estimates for 2023-25, Made October 4th, 2023

{kind=link}

{kind=link}

Service Properties Trust

At the end of June, Service Properties owned 221 hotels with over 37,000 guest rooms throughout the United States (46 states), with 1 hotel in Puerto Rico and 2 hotels in Canada. SVC also owned 763 retail service-focused net lease properties totaling approximately 13.5 million square feet throughout the U.S. SVC is managed by The RMR Group ( RMR ).

On a cautionary note, this REIT is also the most leveraged financially (weakest balance sheet) of the group in this article, offsetting perhaps the strongest diversification of real estate assets by type and location.

Seeking Alpha - Service Properties, Basic Data Set & 1-Year Chart Seeking Alpha Table - Service Properties, Analyst Estimates for 2023-25, Made October 4th, 2023

{kind=link}

{kind=link}

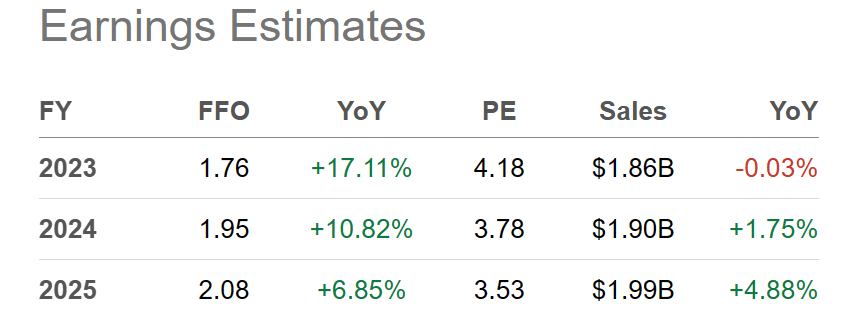

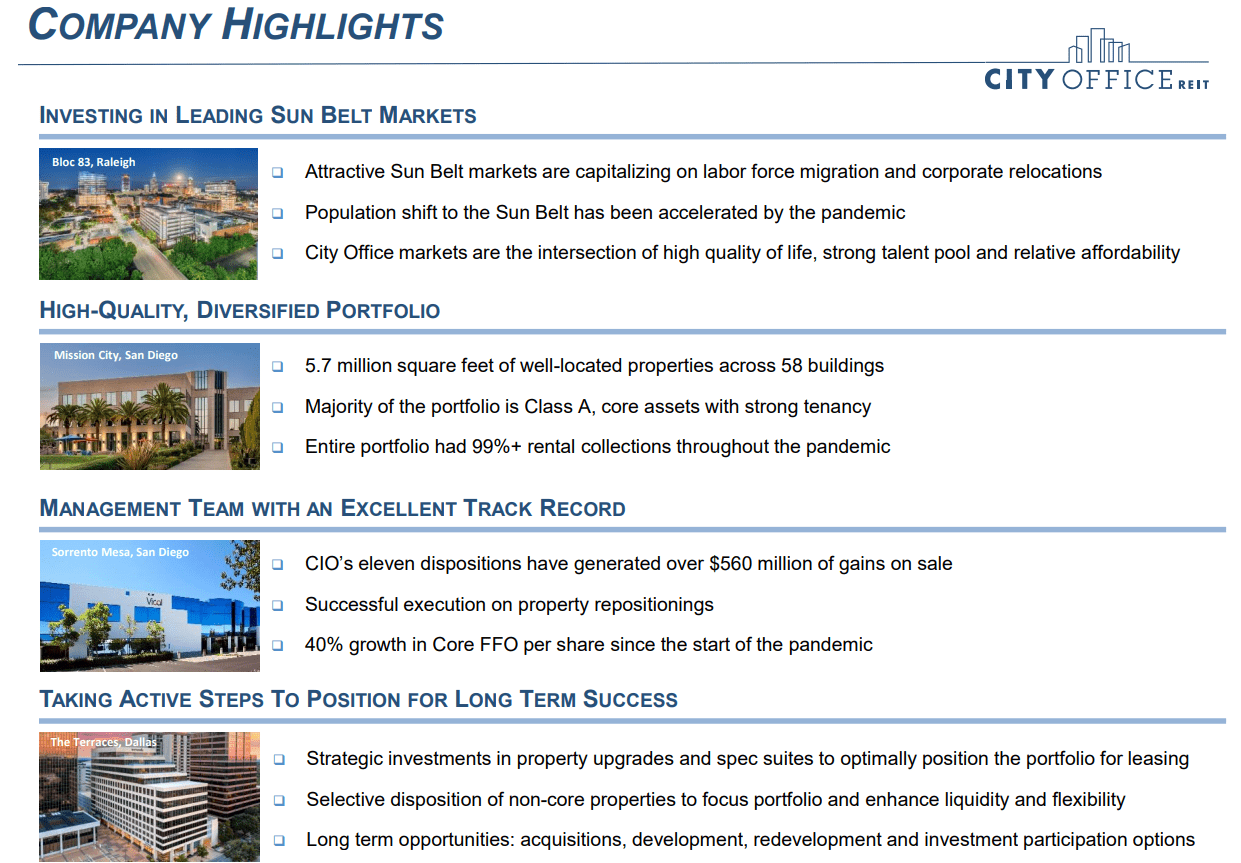

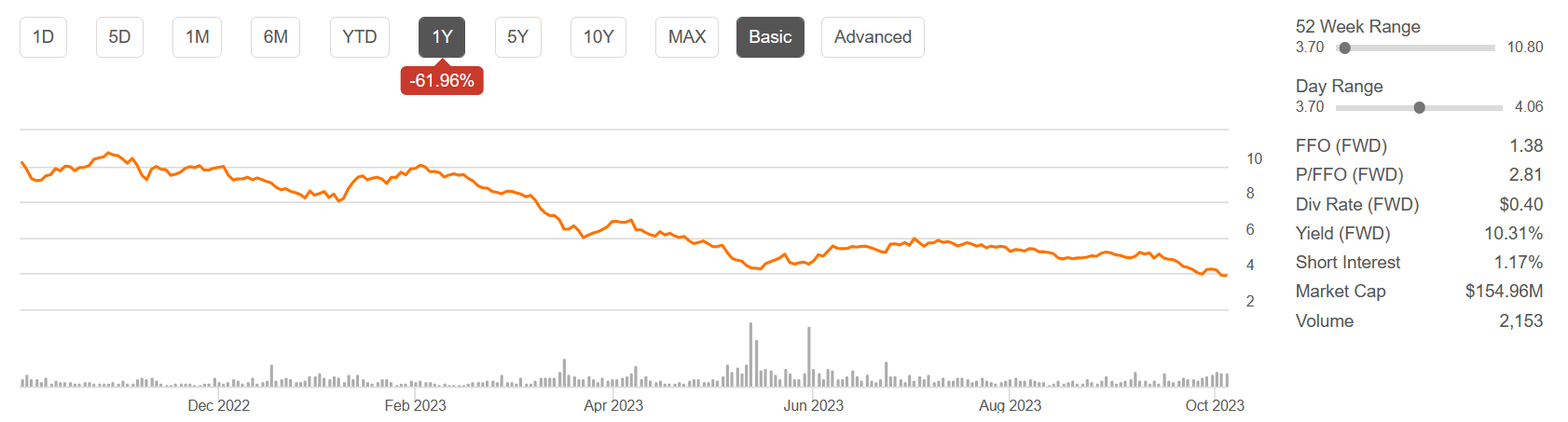

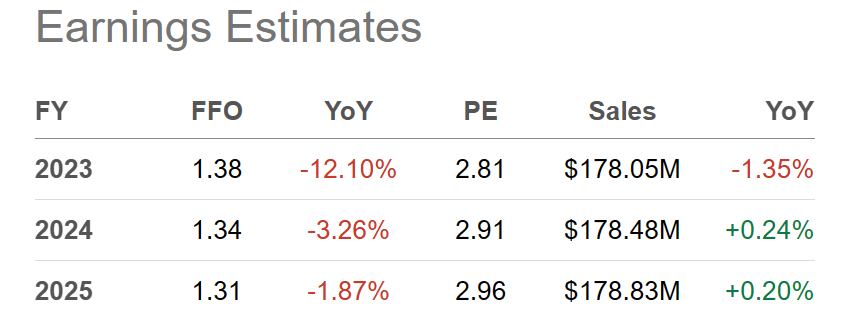

City Office REIT

City Office primarily owns properties in the fast-growing Sun Belt states. The firm currently owns 58 office buildings with a total of approximately 5.7 million square feet of net rentable area in the metropolitan areas of Dallas, Denver, Orlando, Phoenix, Portland, Raleigh, San Diego, Seattle and Tampa. Nearly half of properties are owned in Florida and Arizona.

Below is a nice company description summary taken from its August 2023 investor presentation .

City Office Website - August 2023 Investor Presentation Slide

{kind=link}

Seeking Alpha - City Office, Basic Data Set & 1-Year Chart Seeking Alpha Table - City Office, Analyst Estimates for 2023-25, Made October 4th, 2023

{kind=link}

{kind=link}

Hudson Pacific Properties

Around 80% of Hudson's revenue in the first half of 2023 was derived from 50 office building rentals in total, mainly located in the Los Angeles and San Francisco areas, with several more found in Seattle and Vancouver, Canada.

Hudson also owns Sunset Studios , sound and film/video stages located in Los Angeles, London and New York City to help multimedia, audio, podcast and music entertainment recorders/creators. Other assets include vehicles, plus lighting and production supplies for offsite media creation.

According to the annual 10-K filing for 2022 ,

As of December 31, 2022, our portfolio included:

• Office properties comprising approximately 15.9 million square feet;

• Studio properties comprising approximately 35 stages and 1.5 million square feet of sound stages and production-supporting office and other facilities;

• Land properties comprising approximately 3.6 million square feet of undeveloped density rights for future office, studio and residential space; and

• Production services assets, comprising approximately 1,622 vehicles, lighting and grip, production supplies and other equipment and the lease rights to an additional 27 sound stages.

Hudson did eliminate its dividend payment lately, in hopes of shoring up its balance sheet, while the company prepares for higher interest expense on debt ($40 million greater than the first half of 2022). In addition, it sold two properties in Los Angeles for $72.5 million weeks ago. These actions were partly necessary to offset the negative cash flow effects of the Hollywood writers and actors strikes this summer.

Seeking Alpha - Hudson Pacific, Basic Data Set & 1-Year Chart Seeking Alpha Table - Hudson Pacific, Analyst Estimates for 2023-25, Made October 4th, 2023

{kind=link}

{kind=link}

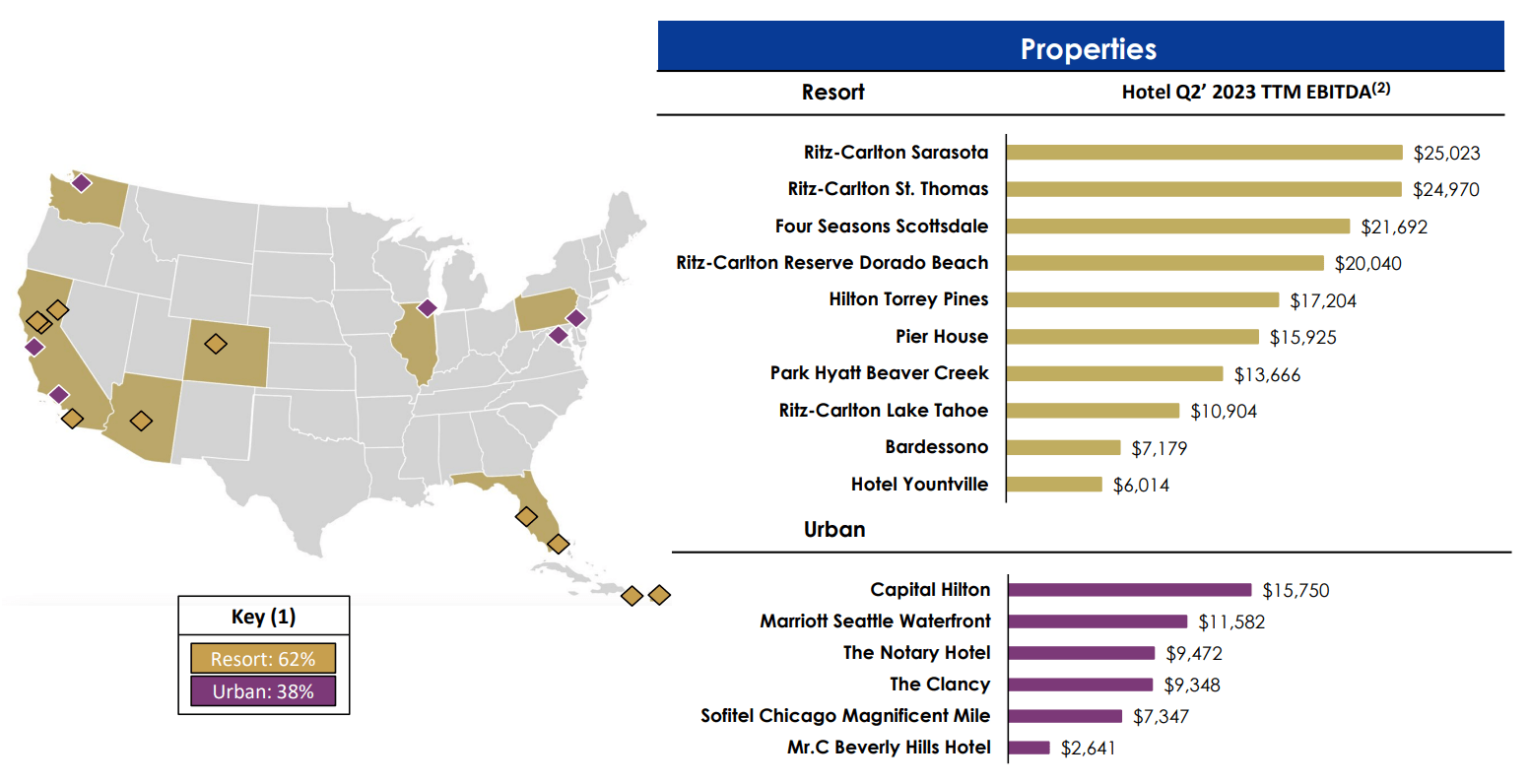

Braemar Hotels & Resorts

Braemar owns 16 luxury hotels in places like Beverly Hills, CA, Beaver Creek, CO, and Key West, FL. Some of the branded names include Ritz-Carlton, Hilton, Hyatt, Four Seasons and Marriott. Many are uniquely named, with independent management and hospitality structures.

A listing of trailing annual EBITDA for each resort is listed below, taken from the Q2 2023 earnings presentation.

Braemar Q2 2023 Earnings Presentation

{kind=link}

The good news is 2023 occupancy is back to pre-COVID 2019 levels, and rates/revenue per customer are approaching the same level adjusted for inflation over the last five years.

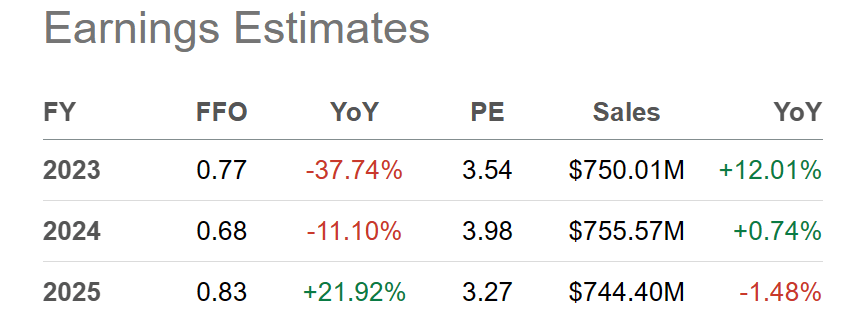

Seeking Alpha - Braemar Hotels, Basic Data Set & 1-Year Chart Seeking Alpha Table - Braemar Hotels, Analyst Estimates for 2023-25, Made October 4th, 2023

{kind=link}

{kind=link}

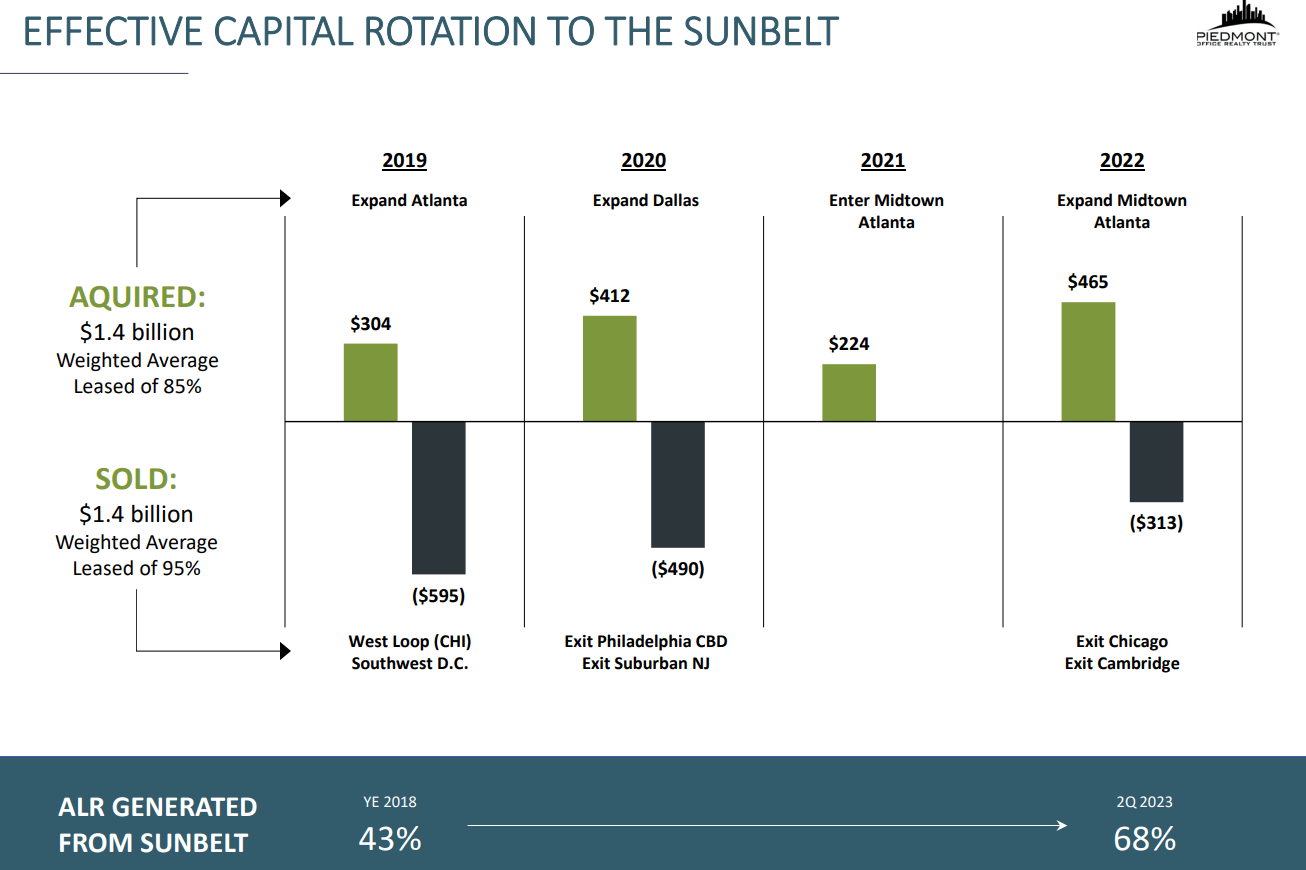

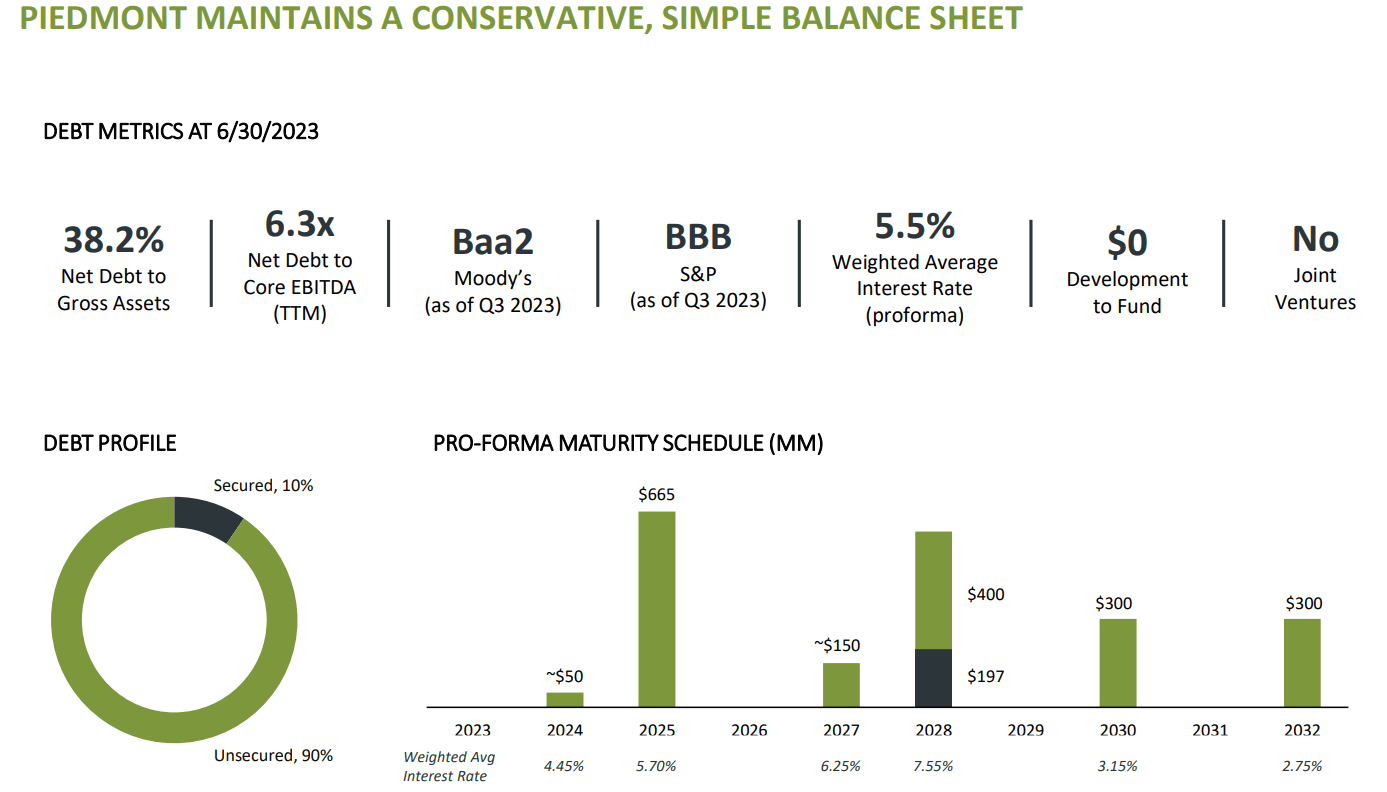

Piedmont Office Realty

Piedmont rents 17 million square feet of high-quality Class A Sun Belt office building space. Based in Atlanta, its core focus is Georgia, Florida, and Texas for locations. Minneapolis, Boston, New York, and Washington DC are other areas with properties. Over the last 5 years, management has built up its southeastern U.S. presence to 68% of the real estate portfolio.

Piedmont Office - September 2023 Investor Presentation

{kind=link}

The company does not have significant debts due for refinancing until 2025.

Piedmont Office - September 2023 Investor Presentation

{kind=link}

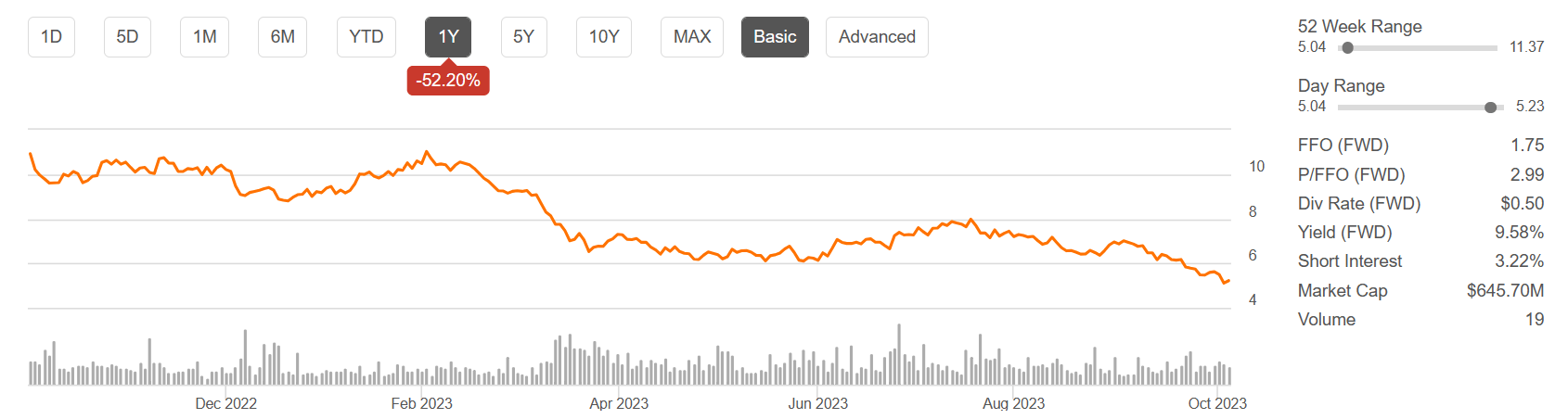

Seeking Alpha - Piedmont Office, Basic Data Set & 1-Year Chart

{kind=link}

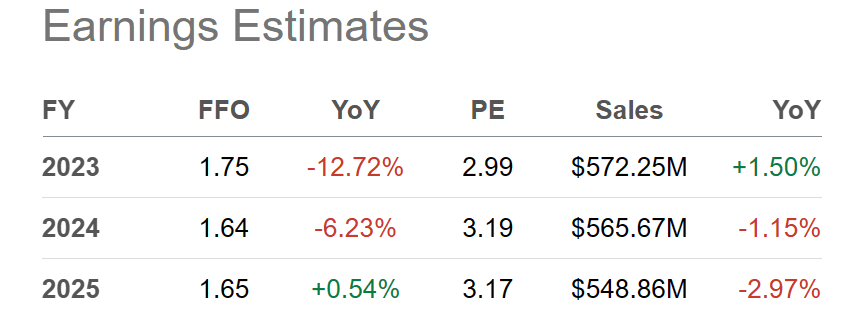

Seeking Alpha Table - Piedmont Office, Analyst Estimates for 2023-25, Made October 4th, 2023

{kind=link}

Office Properties Income

Office Properties owns and leases high quality office and mixed-use properties in U.S. markets. As of June 30, 2023, approximately 63% of OPI's revenues were from investment-grade rated tenants on 155 properties, with approximately 20.8 million square feet located in 30 states and Washington, DC. The primary goal is to rent to single tenants per building through government leases or corporate headquarters for others.

OPI is one of the more leveraged selections of the 9 sorted. This is counterweighted by perhaps the highest dividend payout expectation of the group. At the current/forward yield of 25% annually, contrarian investors may be able to get back their initial investment over four years. Eventually, you could own your position at almost no net cost for the rest of your life (or the company's). Just remember, a severe recession could send the quote closer to zero and slash the dividend to nothing in 2024-25.

Seeking Alpha - Office Properties, Basic Data Set & 1-Year Chart Seeking Alpha Table - Office Properties, Analyst Estimates for 2023-25, Made October 4th, 2023

{kind=link}

{kind=link}

Final Thoughts

Each REIT has different leverage profiles. Each holds different debt maturities and borrowing costs. Properties can have wonderful or rotten locations. The buildings can be newer/upgraded or older and in disrepair. It's important to do more research before committing any investment capital.

Many investors will want to refrain from buying overleveraged names, however, this is the group that often delivers the biggest gains in a sector upturn. My suggestion is to own a bunch of REITs with various characteristics to increase your odds of success. Concentrating on cheap valuations with price below cost accounting book value, real cash coming in the door, and a lower than industry average setup on underlying business sales are critical, in my view.

YCharts - Sorted REIT Picks, Debt to Equity Ratio, 1 Year YCharts - Sorted REIT Picks, Total Liabilities to Assets, 1 Year

Please own a basket of names to reduce risk. For example, if you equally weight 9 companies, just one company delivering a +1,000% total return over the next 2-3 years means the other 8 can decline to zero, and you will still earn a little bit of money. Many of these companies have already witnessed price declines on the magnitude of -70% to -90% over five years or less. The reality is another big dump in price will allow for the mathematical chance of +500% total returns on any positive shift in variables favoring ownership.

Let's say interest rates actually do decline dramatically over the next 12-18 months on a recession, and a recovery in the real estate market begins in the second half of 2024. Let's visualize the mentioned REITs not only stay in business, but a combination of lower borrowing costs and rising real estate values in a major Fed reflation effort next year actually encourages investors to bid REITs to average or even above-average valuation levels over 24-36 months. Further consideration, while you wait for higher quotes you get juicy cash dividend yields for a number of years. Putting the whole bullish picture together, it's quite possible there will be a number of +200%, +300% or better gainers off their eventual 2023 price bottoms, out of the 9 in this sort list.

It is likewise possible, investors in 2-3 years will kick themselves for not having more conviction/courage to buy REITs at a 10-year or 15-year bottom in sector pricing/valuations. If you believe the Fed is stuck printing money in ever-increasing amounts each economic cycle (like I do) to keep Uncle Sam's $33 trillion in basically unpayable debts and the U.S. economy's maze of IOUs from imploding, owning real estate should remain a wonderful inflation hedge proposition.

Who knows? Maybe after a couple of years, working in the office (at least some of the time) will allow the office building marketplace to stabilize. Maybe overnight travel stays and shopping in stores will become a bigger traffic reality over time, at least more than the vast majority of analysts and investors are forecasting today.

I don't particularly like the Wall Street cliches of being greedy when others are fearful , or buying when there's blood on the street . It's more of a Mr. Potter thing from the movie " It's A Wonderful Life " starring James Stewart as the everyday hero. Oversized trading profits happen when you buy something of value, as everyone else is emotionally convinced selling is the only decision to be made. Remember, going against the crowd is a critical skill at major tops and bottoms in price, else everyone would be rich. They are not, because investing and trading can be a difficult emotional game, not an easy one.

Currently for REITs, I only own blue-chip Realty Income (which I discussed last week here ) and SL Green Realty ( SLG )'s prime New York City assets mentioned in a bullish article during June here . I am waiting patiently for a scary and "disorderly" stock market selloff that forces the Fed off its tightening stance. At that point I will likely buy 10-20 other REIT names, some from this article, with a truly strong upside setup for 2024 investing profits.

Thanks for reading. Please consider this article a first step in your due diligence process. Consulting with a registered and experienced investment advisor is recommended before making any trade.

For further details see:

9 REITs Blown Apart, Holding Serious 2024 Rebound Potential