MLPS - 9% Yield - MPLX Is A Top Pick For Low-Stress Energy Income

2023-10-05 11:05:55 ET

Summary

- MPLX LP is a midstream company with a 9% yield, offering stability and potential growth without direct commodity price exposure.

- Backed by a strong relationship with Marathon Petroleum, MPLX is poised for solid long-term growth.

- With a well-covered dividend, a robust balance sheet, and ongoing expansion plans, MPLX presents an attractive opportunity in the midstream sector.

Introduction

I'm a long-term oil and gas bull. By now, I doubt this comes as a surprise. I have close to 20% energy exposure. Almost all of it is invested in upstream companies, which are the ones that get the commodities out of the ground.

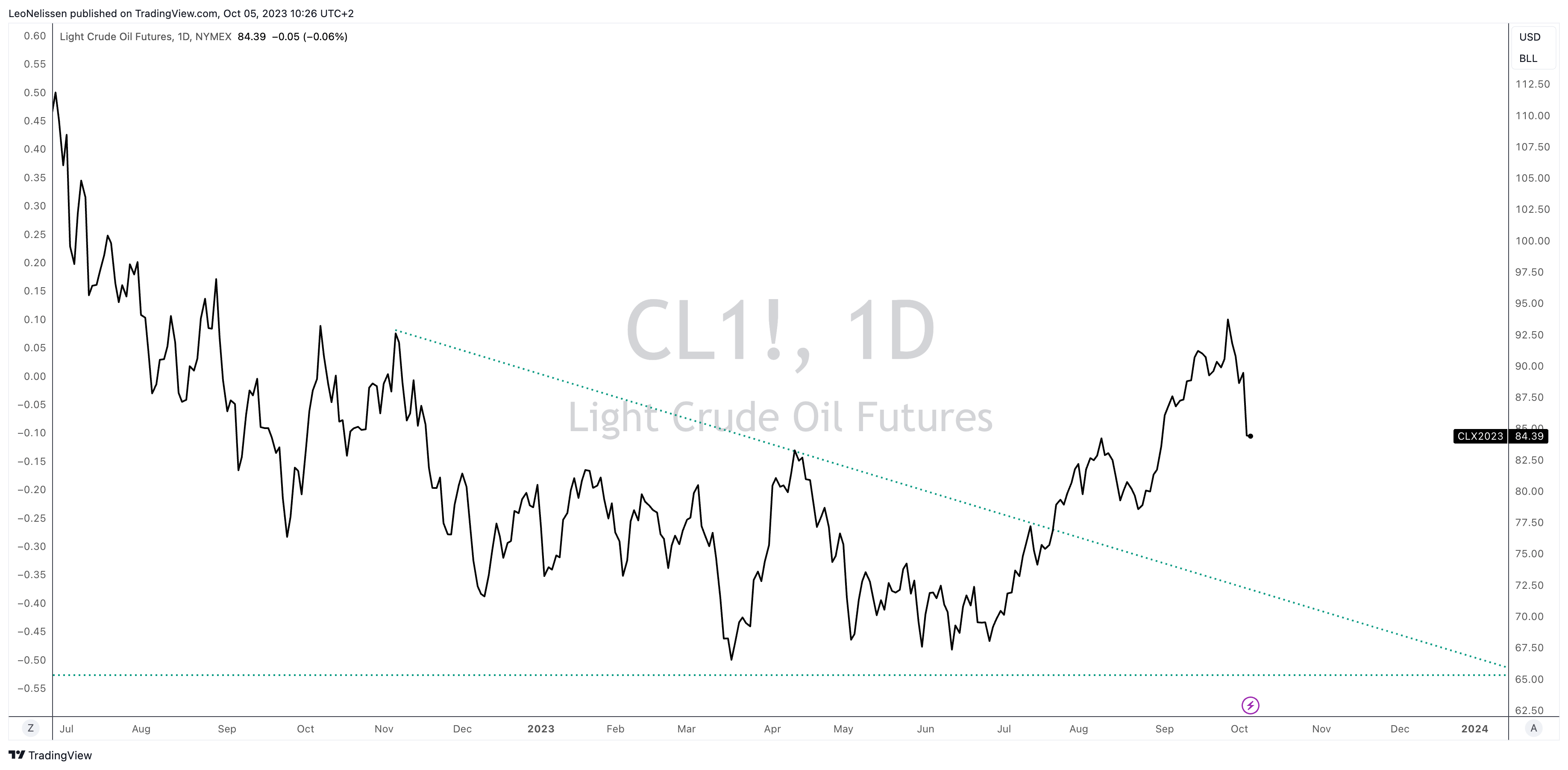

Right now, we're in a very volatile period. After coming close to $95 WTI, oil prices are rapidly declining again as demand fears have hit the market like a wrecking ball.

{kind=link}

As mentioned in previous articles , a pullback to $80 is expected due to demand risks and overcrowding in the oil trade.

In general, the issue with upstream companies is their volatile behavior. While it shouldn't be an issue for seasoned investors who know what they are getting into, some investors are better off buying income with less volatility, even if it comes with limited upside potential in case oil prices continue to rally on a long-term basis.

That's where midstream companies come in!

Unlike upstream companies, midstream companies do not produce oil and gas. They store and ship it, connecting producers to customers. It also means they do not have direct commodity price exposure.

The biggest risk for midstream companies is an event where commodity prices are so low that producers reduce output or demand destruction that's so bad that throughput volumes implode. Other than that, it won't make much difference to most midstream players whether oil is trading at $70, $80, or $100.

Eland Cables

This brings me to MPLX LP ( MPLX ) .

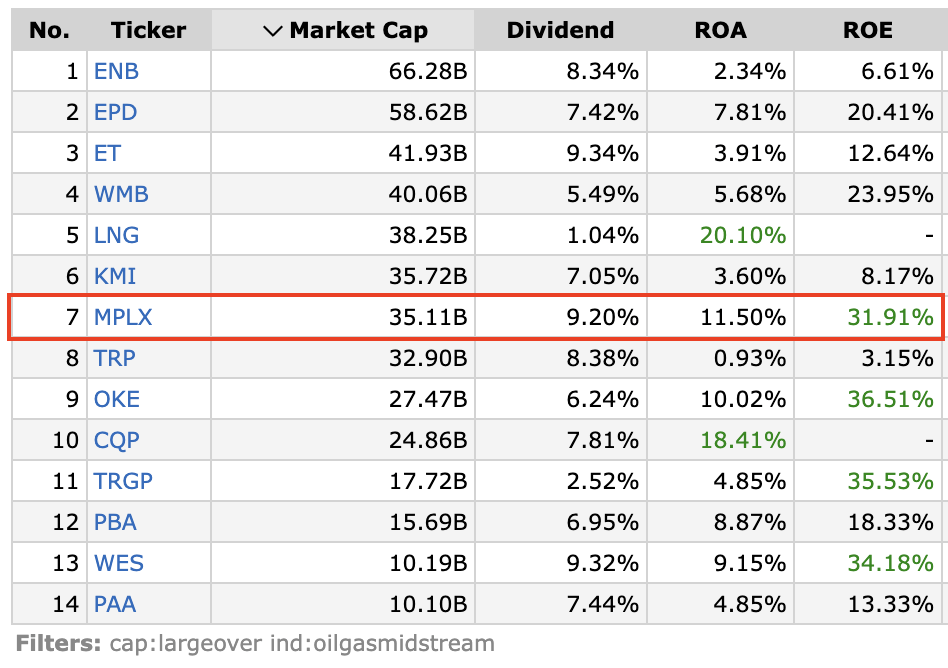

This Master Limited Partnership, which issues a K-1 form, is one of just three midstream companies in North America with a yield of 9% or more! Please note that I excluded smaller midstream companies with a market cap of less than $10 billion in the table below.

**On a side note, please note that when dealing with Master Limited Partnerships, shares are called units. Dividends are called distributions. However, I often still go with dividends after I explain the difference, as I have felt that this is easier for most people to understand. However, please be aware of this difference and the potential tax implications of holding MLPs.

{kind=link}

On a side note, it also has top-tier profitability when looking at the elevated return on assets and return on equity.

In this article, I will explain why this well-covered 9% yield is a great way to buy income without having to worry about the oil price on a daily basis.

So, let's get to it!

An Essential Wide-Moat Business

Every midstream company is different.

MPLX, for example, was formed by America's largest pure-play refiner, Marathon Petroleum ( MPC ), in 2012. MPC owns 12 major refineries and is an essential part of North America's energy industry, especially in the Midwest, where it is headquartered.

The company owns and manages a range of midstream energy infrastructure, including pipelines, marine operations, terminals, storage facilities, and natural gas processing units.

MPLX LP

MPLX operates in two primary segments:

-

Logistics and Storage (L&S): Engages in the gathering, transportation, storage, and distribution of hydrocarbon-based products. In 2022, roughly 88% of L&S segment revenues were generated from MPC.

MPLX LP

-

Gathering and Processing (G&P): Involves gathering, processing, and transportation of natural gas, along with transportation, fractionation, storage, and marketing of NGLs.

MPLX LP

Not only does MPC account for most of the company's L&S revenues, but it also owns 65% of MPLX and general partner shares. In 2022, MPC accounted for 47% of MPLX's total revenues.

Usually, concentrated revenues are a risk. However, in this case, the risk is limited. After all, MPC needs these assets. It cannot switch to a competitor. Also, because of its significant interest in MPLX, there is no need to invest billions in alternatives.

If anything, I believe the connection with MPC lowers shareholder risks, as MPLX has a customer it can count on.

Furthermore, since its birth, MPLX has returned 182%, including dividends (distributions). Excluding dividends, that number is 29%. The Alerian MLP ETF ( AMLP ) has returned just 18% during this period - including dividends!

Having said that, let's take a closer look under the hood, including the company's juicy dividend.

A Well-Covered Dividend

MPLX pays a $0.775 per share per quarter dividend. This translates to an annual payout of $3.10. Given the current stock price of $35, we get a yield of 8.8%.

The company's dividend has never been cut. The same cannot be said about a lot of peers. Most investors are still scarred from the Kinder Morgan ( KMI ) cut and remember Energy Transfer's ( ET ) cut during the pandemic.

On November 1, 2022, the company hiked its dividend by 9.9%.

At the end of 2021, the company paid a special dividend of $0.575 per unit, which explains the spike in the chart above.

According to Seeking Alpha data , MPLX has a 5-year dividend CAGR of 4.9%, which isn't bad for a stock yielding 9%, and the fact that the past five years included a devastating pandemic.

Furthermore, the company uses buybacks for additional distributions. Over the past three years, the company has bought back roughly 4% of its outstanding common units. It's not a lot, but it is very unusual in this industry and another positive that sets MPLX apart from its peers.

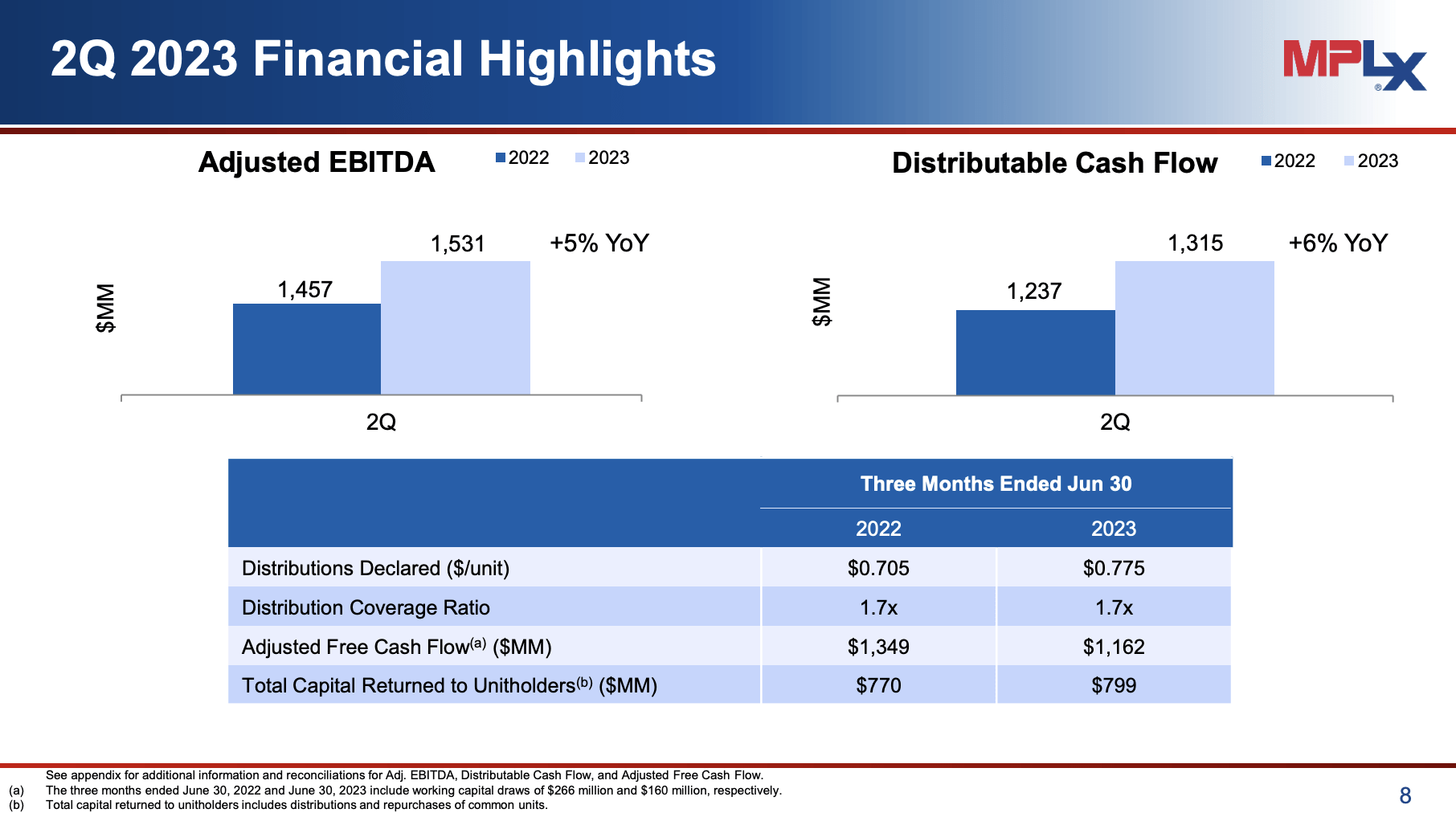

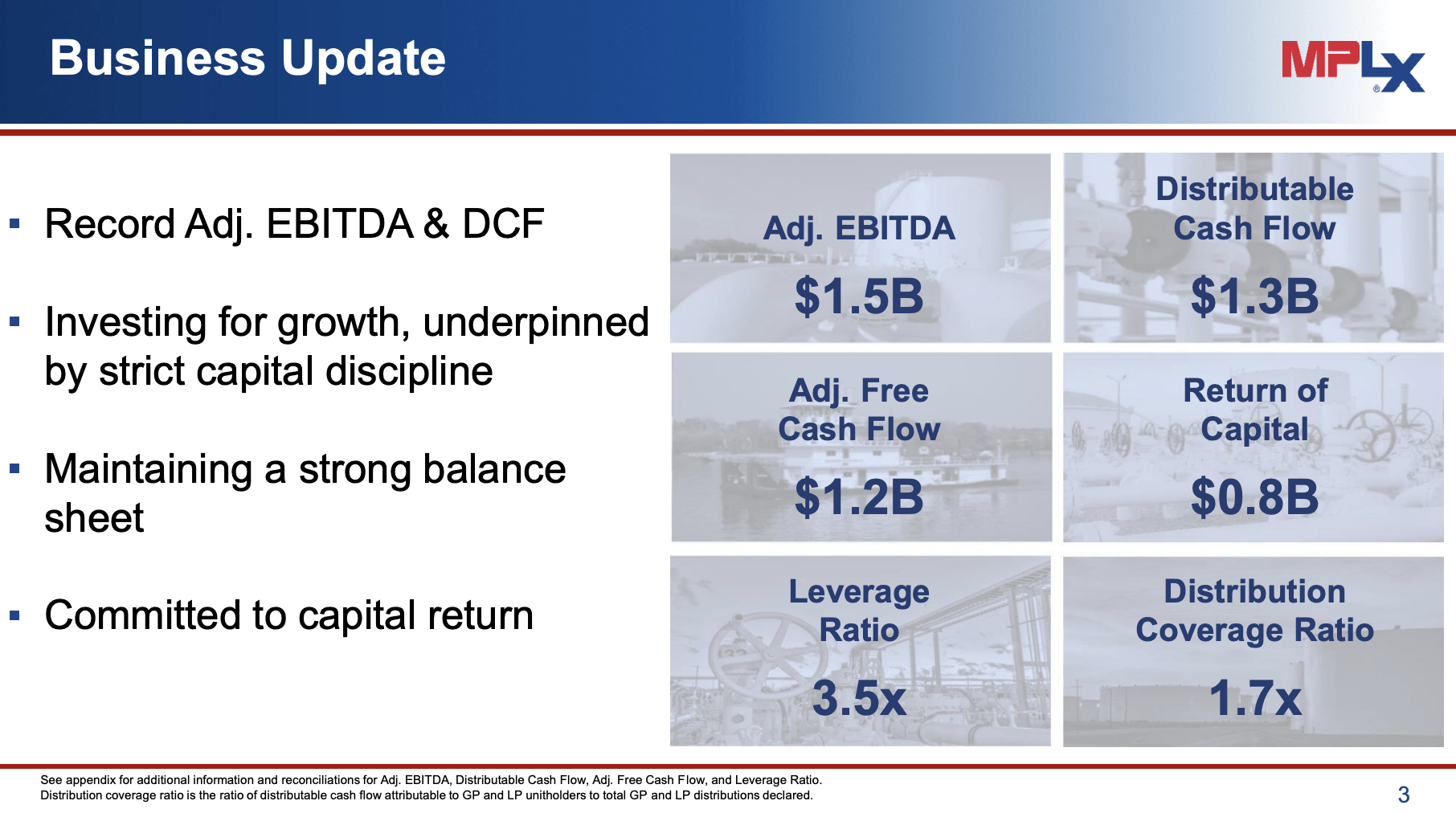

Having said that, these shareholder/unitholder distributions are backed by a solid business. For example, in the second quarter, the company reported a record adjusted EBITDA of $1.5 billion, marking a 5% year-over-year increase.

{kind=link}

Distributable cash flow also reached a new high at nearly $1.3 billion, up by 6% compared to the previous year. This led to a distribution (dividend) coverage ratio of 1.7x, meaning its 9% yield is in a very good spot.

{kind=link}

Furthermore, despite lower natural gas and NGL prices compared to the previous year, MPLX's long-term production outlook for its G&P producer customers in key basins remained largely unchanged.

In the Marcellus, where development costs remained low and below current commodity prices, maintenance-level drilling activity was expected to continue.

Also, during its earnings call, the company noted that the recent U.S. Supreme Court decision supporting the MVP pipeline construction was seen as beneficial for natural gas development in the region.

In the Permian, the production outlook was stable due to strong crude prices and the limited impact of associated gas prices on producer activity. MPLX believes that its integrated footprints in these resilient basins positioned the partnership for steady earnings and growth opportunities. It's hard to disagree with that.

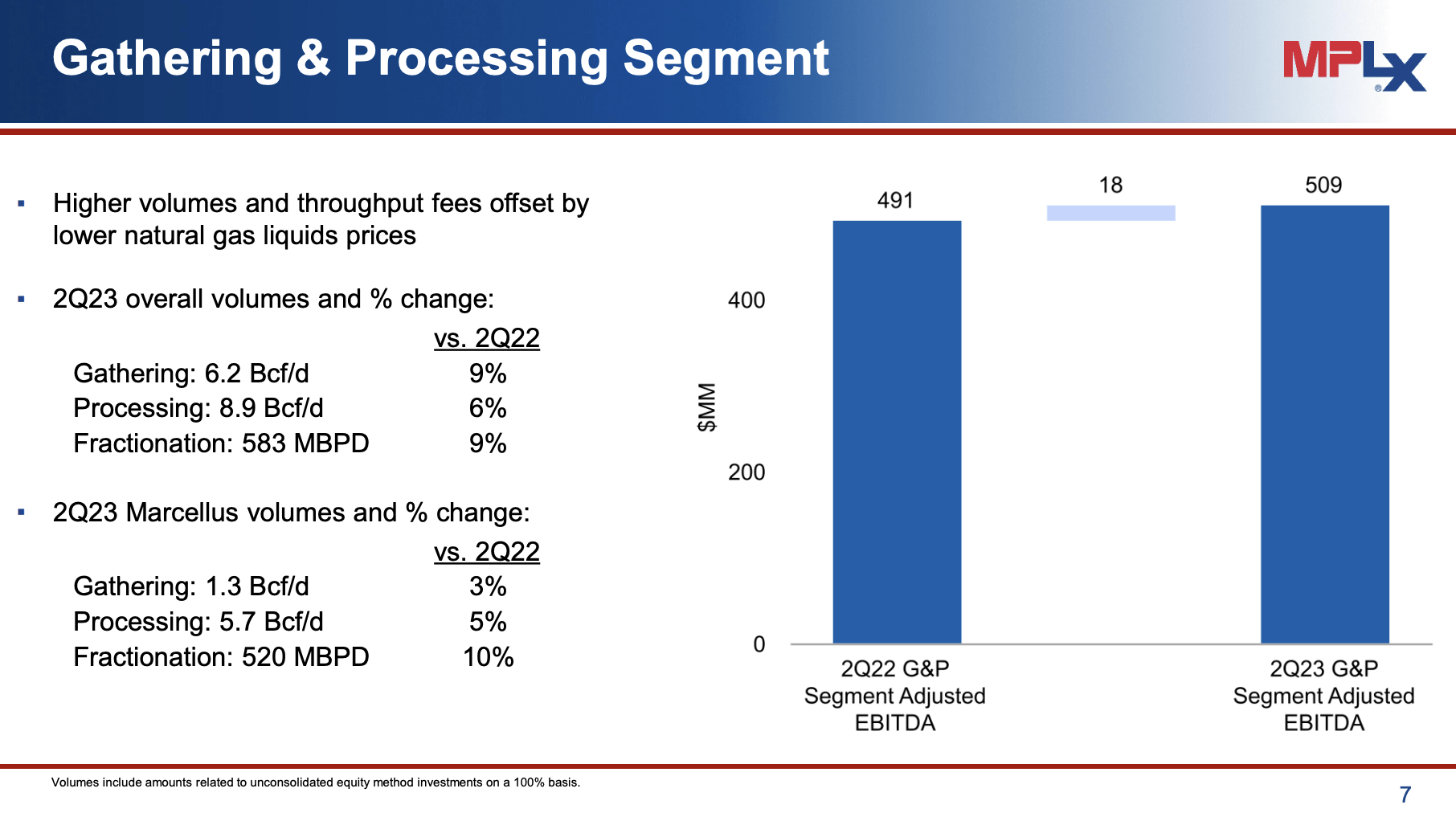

MPLX's Gathering and Processing segment experienced an $18 million increase in adjusted EBITDA compared to the second quarter of 2022, driven by higher volumes and throughput fees, although this was partially offset by lower NGL prices.

{kind=link}

While the G&P segment was predominantly fee-based, it still had some sensitivity to NGL prices, which averaged $0.63 per gallon during the quarter, compared to $1.18 in the same quarter of the previous year.

The company is also further expanding.

MPLX's capital program outlook for 2023 remained at $950 million, including $800 million for growth capital and $150 million for maintenance capital.

The company is making progress with joint venture projects in the Permian, including the expansion of the Whistler natural gas pipeline to 2.5 billion cubic feet per day, which was expected to be completed in September.

MPLX also planned to expand the BANGL joint venture pipeline to 200,000 barrels per day to enhance its participation in the NGL value chain.

This is expected to result in strong EBITDA growth. Last year, the company did $5.8 billion in EBITDA. That number is expected to gradually grow to $6.3 billion by 2025.

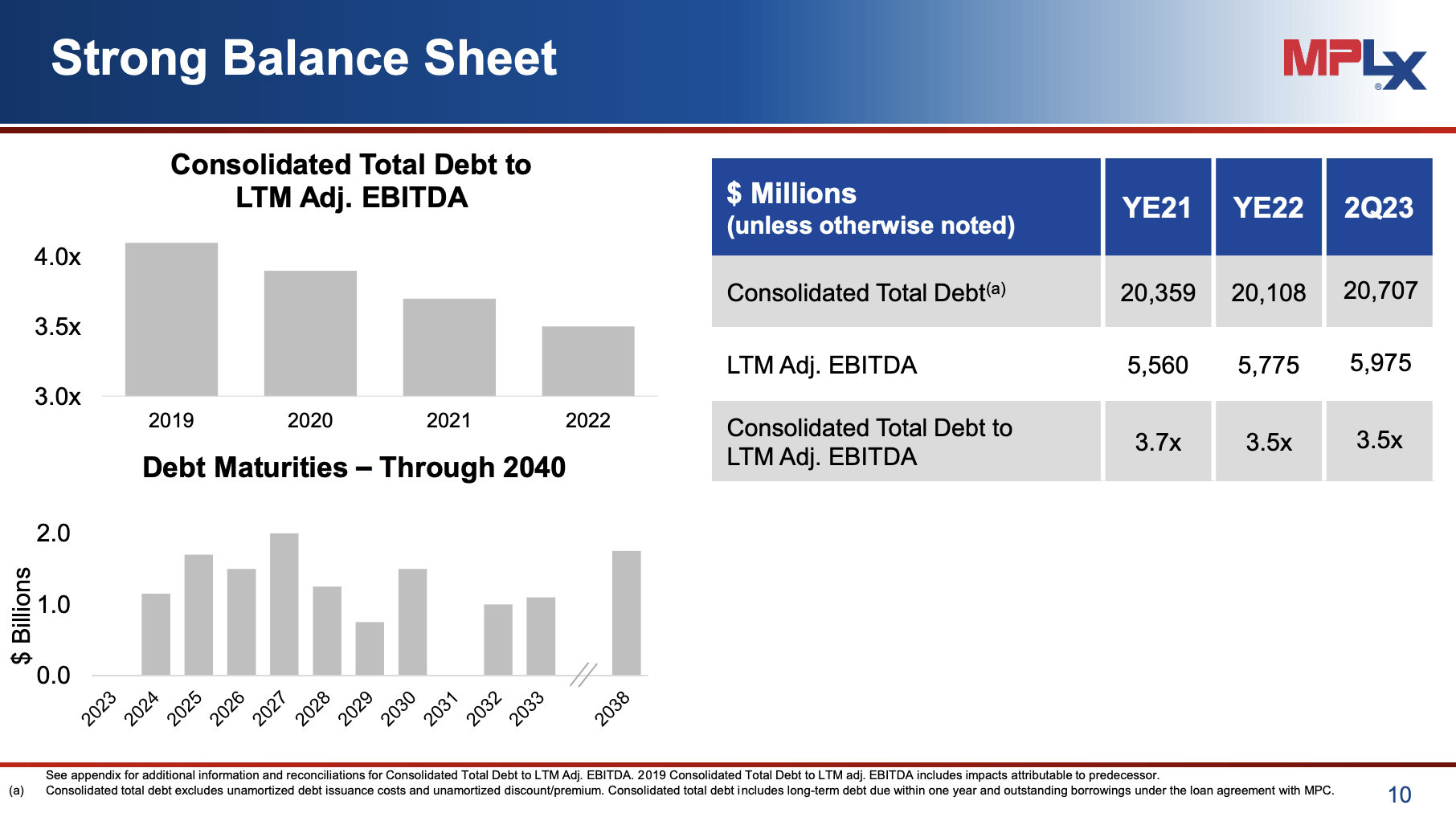

Also, the company has a well-covered dividend and a healthy balance sheet.

Since 2019, the company has significantly lowered its leverage ratio. It also has no maturities in 2023.

{kind=link}

So, what about the valuation?

Valuation

I believe that MPLX is attractively valued. This isn't just based on its 9% yield, which I expect investors will push down to 8% over the next few months (depending on the economy), but also its ability to grow its EBITDA and distributable cash flow over time.

The company is trading at 9x forward EBITDA, which is right in the middle of all major midstream companies - both MLPs and C-Corps.

Analysts give the stock a consensus price target of $40, which is 14% above the current price.

Investors interested in buying a high distribution yield may benefit from buying in intervals. Start small and add over time. If the economy deteriorates further, we could see some selling in MPLX, allowing investors to average down.

On a long-term basis, I have little doubt that the dividend will keep growing, backed by a rock-solid business. This will likely continue to lead to outperforming total returns.

If I were focused on income over dividend growth, I would likely be an owner of MPLX shares (although I currently cannot buy American MLPs).

Takeaway

For investors seeking steady income and insulation from oil price volatility, MPLX stands as a compelling choice.

MPLX, a midstream company with a 9% yield, offers stability and potential growth without direct commodity price exposure.

Backed by a strong relationship with Marathon Petroleum and consistent dividend payments, MPLX is poised for solid long-term growth.

With a well-covered dividend, a robust balance sheet, and ongoing expansion plans, MPLX presents an attractive opportunity in the midstream sector.

For further details see:

9% Yield - MPLX Is A Top Pick For Low-Stress Energy Income