EPRT - A Calm Quantitative Look At The W. P. Carey Spinoff

2023-09-25 06:30:00 ET

Summary

- W. P. Carey announced a spinoff and sale of its office properties, leading to a dividend cut and a negative market reaction.

- The company's heavy external growth model and high payout ratio have hindered dividend growth and overall growth per share cash earnings.

- The spinoff and dividend cut may allow W. P. Carey to use retained earnings for more growth, but the success of the strategy remains uncertain.

You are almost certainly aware that W. P. Carey ( WPC ) announced a spinoff and sale of their office properties last Thursday, along with a pending dividend cut. Mr. Market seemed to really hate it, selling off 8% on that day and a few more the next.

But in reality Thursday was a very red day for REITs, with some selling off more than 8% and others less. At this instant, the relative drop looks like 6%, give or take.

{kind=link}

It was entertaining to see the diversity of reactions. My own initial reaction was quite positive.

Seeking Alpha author Samuel Smith posted a strongly negative article both publicly and to members on Thursday (but it was still a Strong Buy rating). Meanwhile, SA author Jussi Askola posted a strongly positive article to members on Friday.

One can see reasons for the negativity:

- Income investors never like dividend reductions.

- That reduction also will end dividend aristocrat status for W. P. Carey.

- This in turn will put downward pressure on the stock price as certain ETFs exit.

- This seems a bad time to sell office properties, whose valuations are depressed.

I first suggested two years ago that W. P. Carey might want or need to cut the dividend in order to enable more growth. More recently, it appeared to me that they were on a path to higher growth without that, although they still had some distance to go.

Several other authors have weighed in as well on last week's news. We are up to four public articles at the time of writing, no doubt with more to come. My expectation is that you will find the depth of analysis here unique.

We discuss below why dividend growth went awry. Stay with me and let's look more deeply at the issues.

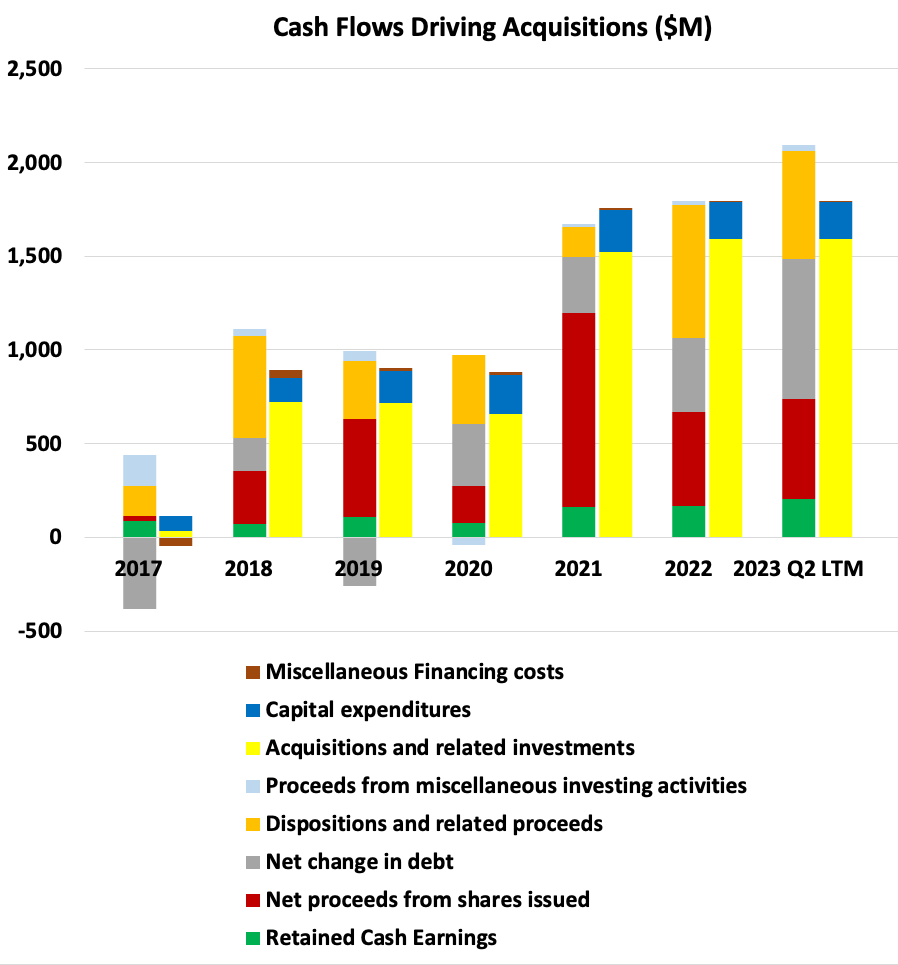

The W. P. Carey Business Model

The cash flows tell us how W. P. Carey has been operating their business. There are a couple of important implications.

{kind=link}

For each year shown, the bars on the left are sources of funds and the bars on the rights are uses of funds. The green shows retained earnings. These are always small for W. P. Carey, a contrast from NNN REIT ( NNN ) and from the new focus of EPR Properties ( EPR ).

Instead, the funds available have come primarily from issuing stock (red) and from new debt (gray). Dispositions (orange) have been significant in recent years, but this may only reflect the shedding of unwanted properties from the two recent mergers (discussed in prior articles).

Nearly all of the funds used have been for acquisitions (yellow). There is also some capital expenditures (blue).

These capital expenditures were mostly for development and redevelopment in 2022. However, a concern is that re-tenanting large office properties can be quite expensive and can soak up capital which otherwise could fuel growth. This was mentioned in the discussion of the spinoff.

W. P. Carey has been running a heavy external growth model. The main capital for growth has come from issuing new shares and placing new debt.

They have in recent years added a decent amount of capital recycling (funded by the dispositions). But their capital from retained earnings has been tiny.

This last reflects their large payout ratio, which has been running well up into the 80s or higher. They have been slowly working it down, but that is a tough road to hoe.

Why W. P. Carey Was Stuck

The problem with pure external growth models is that Mr. Market can close the door on your ability to grow per share cash earnings. This has happened to W. P. Carey this year, and perhaps to other REITs running this model.

Here is how it works. Issuing stock raises cash at the cost of giving a fraction of current cash earnings (here represented by AFFO, for Adjusted Funds From Operations) to those who buy the stock.

The Traded Yield is the ratio of AFFO/sh to current stock price. If the Traded yield is 10%, and one sells 10% of the prior AFFO by issuing stock, this dilutes all AFFO after the sale by 110%. The AFFO/sh becomes 91% of its prior value and one has raised cash equal to 10% of the Market Cap.

Here are two relevant Traded Yields for WPC:

RP Drake

Simultaneously with the spinoff, W. P. Carey is settling $385M of existing equity forwards. These were placed at an average price of $83 and so have a 6.6% Traded Yield. Raising that $385M will cost the existing shareholders about $24M of AFFO.

In contrast, the Traded Yield is 10% at the current price of WPC. Today it would cost the existing shareholders about $35M of AFFO to raise the same cash.

The growth model is to invest that cash so as to increase overall AFFO/sh for all shareholders. This requires that the Investment Yield exceed the Traded Yield. (In detail, the spread must be large enough to overcome the dilution of the other sources of increased AFFO/sh such as rent growth, but the main point here does not depend on that aspect.

The next table shows the calculation of the Investment Yield:

RP Drake

Here the first section shaded gold shows the key parameters. There are columns for interest rates of 4% and 5%. These are in the likely ballpark and show the sensitivity.

From these parameters, one can obtain the ratio of interest expense to Net Operating Income, or NOI (row shaded orange). It is near 25%.

The rows shaded blue show that the current ratio of General & Administrative expenses to NOI runs about 6% and recurring capex is small. The result (first row shaded green) is that AFFO/NOI is about 70% for newly acquired properties.

The cap rate and debt ratio imply that the NOI produced by newly invested equity is 12% (second row shaded green). The result, shown on the row shaded yellow, is that the Investment Yield is in the 8's.

Now compare an Investment Yield in the 8's with the AFFO Yields above. Investing the cash from those equity forwards produces a net gain. The spread is large enough that overall AFFO/sh increases from the combination of stock issuance and new investment.

In sharp contrast, the present stock price produces a Traded Yield far above the Investment Yield. It would take an 8.5% cap rate to make them equal and more than that to make issuing stock accretive.

This is why W. P. Carey was stuck. They cannot grow by issuing shares in today's market. They can grow very little from their very small, retained earnings. This is the long-term result of setting the dividend too high when they became a REIT 10 years ago, a common mistake.

They are generating capital by dispositions. However, dispositions followed by acquisitions most often produce little net growth unless one rotates out of high demand properties, as Spirit Realty Capital ( SRC ) is actively doing.

Where one can really make money is dispositions followed by development, which AvalonBay , the other big apartment REITs, and the Shopping Center REITs do. But that is not W. P. Carey's game.

What the Board Saw

The first story about 2023, when the guidance has been for minimal AFFO/sh growth, is that there was a one-time effect due to increased interest rates. The reality is that interest costs have risen by several percent of AFFO, enough to offset reasonable growth from other sources.

Beyond that, it must have been distressing for the board to realize that Mr. Market was now preventing further external growth. It may not have been clear to them previously why pure external growth models are risky. (They should have read my articles or thought about things Chris Volk has published, starting in 1999.)

Apparently the board did realize some months ago their current inability to grow AFFO/sh beyond the anemic level produced by rent increases and perhaps by recycling capital. The discussion of the spinoff mentioned several times becoming able to grow from retained earnings, and that this will be made possible by reducing the payout fraction to the low 70s.

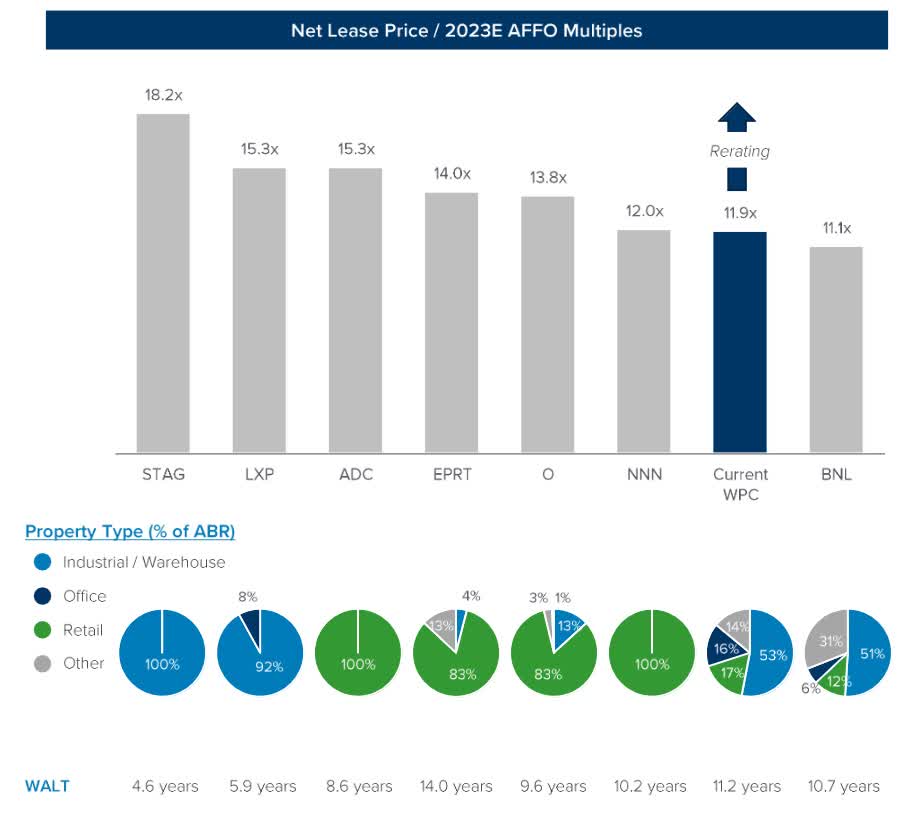

But the board also was clearly also aware of the following comparison, shown in their presentation on the spinoff:

{kind=link}

Staring at the details here can lead one to conclude that the path to a higher AFFO multiple is to shed the office properties and add more industrial ones. So that is what they are doing.

Will this work? Maybe, maybe not.

The difference in lease term between W. P. Carey and the two industrial REITs is significant. In the present phase of industrial, Mr. Market is loving the soaring rents realized as those short leases expire. In contrast, the net lease model features long leases and ends up leaving a lot of potential rent on the table in hot sectors.

It is also far from clear that shedding office will produce a higher multiple. The Price/FFO ratio of Realty Income did not rise significantly across their merger with VEREIT and spinoff of office properties.

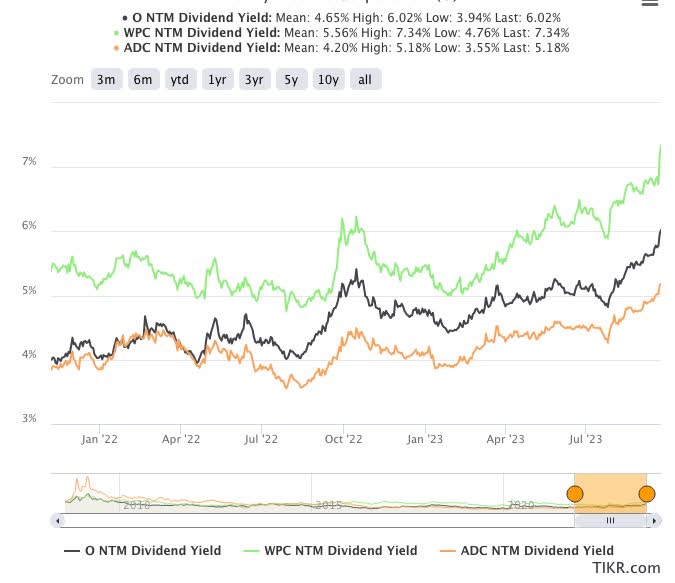

To make matters worse, both Agree Realty and Realty Income run external-growth models that are even more extreme than that of W. P. Carey has been. Their dividend yields have been rising and they could end up stuck too. Their AFFO multiples might close with that of WPC by coming down.

{kind=link}

Beyond that, the higher valuation of Agree Realty ( ADC ) and Realty Income ( O ) may reflect the track record of growth that they have and W. P. Carey does not. It may take time for Mr. Market to give W. P. Carey credit.

But alternatively, it is NNN REIT that already runs a more robust model with substantial internal growth . Perhaps all four will cluster near their multiple, especially if the market does not recover.

Despite all the above, you have to admit that selling off office is better than cutting the dividend solely because the Board feels unloved by Mr. Market, as we see so often. But there is something of the same sense of changing something hoping for a higher earnings multiple that we see in those cases. Perhaps W. P. Carey, their Board, and their investors will get lucky.

The Dividend and Dividend Growth

As an income investor, my focus is not primarily on earnings multiples. Several of my articles, beginning with this one , discussed the reality that retirees should not count on them.

My concern is also not superficially with dividend yield. I mostly or entirely avoid the high yields one can get with financial engineering.

What I want is relatively high dividends that have a good chance of growing enough to keep up with inflation, because they come from solid companies. My refusal for several years to join Jussi and Samuel in WPC reflected my view that dividends were, at best, not ready to grow.

W. P. Carey has long been working to get to the point that they could grow the dividend. My most recent previous article detailed the conclusion that they were very close to that point. I did go long WPC this summer when the dividend yield briefly became quite close to that of Simon Property Group ( SPG ). This diversified my portfolio out of some of my large SPG position.

My view, though, was that dividend growth might still be slow for a while as they continued to work their payout ratio down. Well, that is getting fixed now under the cover of the spinoff.

Here are my notes about what may happen to the AFFO and the dividend:

Several factors will increase AFFO in 2024.

- Paying down debt with cash will save something like $40M in interest costs.

- Investing the $385M from the equity forwards will increase AFFO on net by about $7M and increase the share count only 2%.

- Investing the $350M being taken back from NLOP will increase AFFO by about $30M.

- The reinvestment of about $350M from other dispositions may be accretive, but likely not by a lot. If they net 100 basis points, that will be perhaps $3M.

- Same-store rent growth, guided in the Q2 earnings call to be about 3%, should add about $30M on the remaining properties.

These items altogether total around $110M of AFFO increases.

Some factors will decrease AFFO in 2024.

- The loss of 10% of ABR (average base rent), combined with the payoff of a bit more than 10% of debt, will decrease AFFO by about 10%, or $110M.

- The use of the proceeds from the $800M of internal office sales will likely be dilutive. But if the difference is, say, 300 basis points in cap rate then the impact on NOI and AFFO will be about $24M.

On net then, the above seven items may drop AFFO by $24M, which is less than 3%.

Suppose the 2024 AFFO becomes 97% of its pre-spinoff run rate and that the payout ratio drops to 70% from 80%. The dividend would drop by 15%.

That would decrease today's yield from 7.4% to 6.3%, which is hardly the end of the world. On top of that, one would get some value from NLOP.

NLOP will have $635M of debt at a reported debt ratio of 43%, suggesting a total asset value of $1.5B, also consistent with the reported gross real estate book value for them. This gives a NAV of $865M, or just over $4 per share, comparable to the current annual dividend from WPC.

So suppose you sell NLOP at either $4 per current share of WPC or half that, and that the WPC dividend is cut by 15% or 25% but grows going forward by 4%. Your cumulative income looks like this, as a fraction of the no-spinoff case (the current dividend with 1% dividend growth):

RP Drake

My estimate of the cut is 15%. In that case you would never fall behind in cumulative income. For a 25% cut, you would still not drop below 90% and would slowly recover from there.

Takeaways

Mr. Market has broken the growth model for W. P. Carey and may be on the edge of doing so for Realty Income and Agree Realty. On top of that, any REIT holding single-tenant office properties has got to be nervous about the future.

By spinning off or selling their remaining office properties, W. P. Carey gets clear of those negatives and gains more than $1B to support new investments or debt reduction.

By resetting their dividend to a payout ratio of 70% or a bit more, they create the ability to use retained earnings to support more growth. Forward growth of AFFO/sh and the dividend at 4% seems plausible to me and they might do better.

My attempt to put together the pieces says the dividend cut will be near 15%. If that happens and you can sell your NLOP at 50% of NAV, then your cumulative income will never drop below that from the current dividend growing at 1%.

This works for me. I applaud the move.

For further details see:

A Calm, Quantitative Look At The W. P. Carey Spinoff