VTIP - A Close Look At Short-Term TIPs As Inflation Continues To Go Down

2023-04-30 04:49:04 ET

Summary

- Inflation continues to go down, reaching 5.0% in March.

- As inflation goes down so does the yield and expected returns of TIPs.

- VTIP invests in short-term TIPs, and has been negatively impacted by these trends.

Author's note: This article was released to CEF/ETF Income Laboratory members on April 26th.

With interest rates and broader economic conditions in flux, thought to have a close look where short-term treasury inflation-protected securities, or TIPs, rates stand today. Using the Vanguard Short-Term Inflation-Protected Securities ETF ( VTIP ) as a benchmark, short-term TIPs currently yield 0.60% plus inflation, and could see small capital gains as interest rates continue to stabilize.

By my calculations, short-term TIPs should outperform comparable treasuries with inflation higher than 2.8%. For reference, annual inflation currently stands at 5.0%, monthly at 1.2%. In my opinion, VTIP is a solid inflation hedge, and reasonable investment opportunity, but with inflation moderating, focusing on other asset classes seems best.

VTIP - Yield and Prospective Return Analysis

VTIP currently yields 0.60% plus inflation, and could see small capital gains as interest rates continue to stabilize. To understand why this is the case, let's have a close look at the fund's holdings, starting with a specific TIP. The following is VTIP's fourth-largest holding, and representative of the fund's portfolio.

VTIP

One could interpret the above as follows.

VTIP invested $2.88 billion (face amount) in a TIP yielding 0.125% (coupon rate) plus inflation. TIPs always have an inflation component to their yields, as that is a characteristic of these securities. The market value of this specific TIP has dropped to $2.82 billion (market value), as higher interest rates have decreased demand for lower-yielding bonds, leading to lower prices. The TIP matures in 07/15/2024, at which point VTIP will receive its $2.88 billion back, notwithstanding recent price movements.

Investor returns will consist of yield and capital gains, if any. As mentioned previously, this TIP currently yields 0.125% plus inflation. Capital gains would be equivalent to the difference between the bond's face value, which investors will receive at maturity, and its market price. Currently, these stand at 2.2%.

The above figures are for one specific bond. The fund as a whole currently yields 0.6% plus inflation, and should see around 2.1% in capital gains at maturity, in 2.6 years. This averages to around 0.8% per year. Add the fixed rate yield component and the expected capital gains, and you get 1.4% per year in returns (plus inflation).

Lots of numbers, and a bit more complicated than usual, but this is generally the case for TIPs, and other niche securities.

In most cases, the figures above are provided by most bond ETFs. TIP ETFs are something of a special case, due to their complexity / inflation-protection characteristics. Some of these ETFs do provide these figures, but different managers calculate them a bit differently, so I prefer to go through the figures myself.

Short-term TIPs in general, and VTIP in particular, seem to offer reasonable yields right now. Although that 0.6% rate seems awfully low, investors also receive an inflation adjustment, which can be very hefty. Annual inflation currently stands at 5.0%, a rather strong figure. Monthly inflation is much lower, at around 1.2% annualized, but with heavy volatility. Investors would get some capital gains too, at least if these bonds are held to maturity.

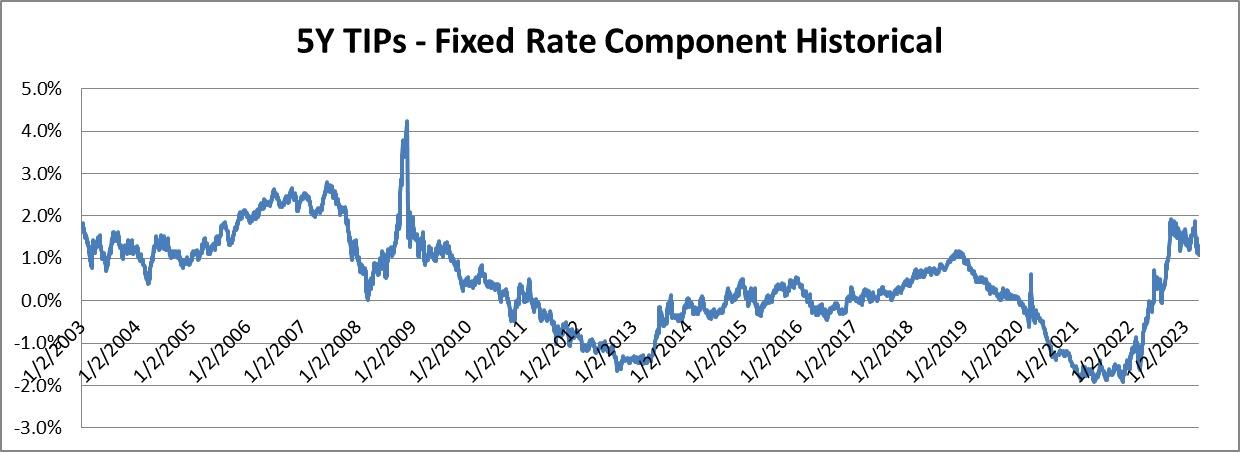

Short-term TIP yields are at historically elevated levels. As per the U.S. Treasury, the fixed rate on longer-term TIPs is around 1.0% - 1.5% higher now than in the prior decade. Fixed rates were a bit higher between 2006 and 2007, more than 15 years ago. Short-term TIP rates were not readily available, but I'm confident that these broadly track their more long-term partners.

{kind=link}

Short-term TIP composite yields, including inflation, are also at historically elevated levels, as inflation remains high. Annual inflation reached historical highs a few months back, and remains at elevated levels. Monthly inflation is much lower, but with heavy volatility.

Data by YCharts

VTIP's yield is strongly dependent on inflation, and would decline if inflation continues to go down. Right now , yields and prospective returns look quite strong. On the other hand, with inflation rapidly decreasing, I believe that future yields and returns will decrease in turn.

VTIP - Short-Term Treasury Yield Comparison

VTIP's expected returns currently stand at around 1.4% plus inflation. 2 year treasuries, closest in maturities to VTIP's portfolio, currently yield 4.2%.

Data by YCharts

From the above, it seems that VTIP's breakeven inflation rate stands at around 2.8%. If inflation averages higher than 2.8% these next 2-3 years, VTIP should outperform short-term treasuries, underperform otherwise. Results are broadly consistent with longer-term breakeven rates, although these are a bit lower. It seems that the market is pricing-in a bit more short-term inflation, which seems rational.

Data by YCharts

In my opinion, short-term breakeven rates seem reasonable enough. I lean towards thinking inflation will drop to its 2.0% target soon enough. As this implies short-term TIPs underperformance, I prefer short-term treasuries . Other investors might believe that inflation will remain somewhat elevated for longer, or that an inflation-hedge investment makes sense, underperformance notwithstanding. These investors might prefer short-term TIPs, including VTIP, over short-term treasuries.

Conclusion

By my calculations, short-term TIPs should outperform comparable treasuries with inflation higher than 2.8%. I believe that inflation should stabilize around 2.0% in short order, so would focus on normal treasuries over short-term TIPs under current conditions.

For further details see:

A Close Look At Short-Term TIPs As Inflation Continues To Go Down