STR - A Conservative Way To Play Higher Oil Prices: Viper Energy Partners

Summary

- We see significantly higher oil prices in the second half of the year.

- Viper Energy Partners LP is one of the best-managed public royalty companies and owns high-quality acreage with a long productive life.

- The units offer a significant upside to higher oil prices and a margin of safety in the event prices decline.

- We rate Viper Energy Partners LP units a Buy and increase our price target to $36.00.

We believe oil prices will surge higher in the second half of the year as the oil market supply balance brings forth a supply deficit. China will transition from a 600,000 barrel per day (bpd) drag on demand in 2022 to a significant tailwind, while Russia and OPEC production will keep supply low enough to reduce inventories at a steep clip.

Investors looking to play higher oil prices without the risks inherent in E&Ps would do well to consider oil and gas royalty trusts. These vehicles are also a way for investors to boost income amid higher prices because most free cash flow is distributed to equity owners.

Viper Energy Partners LP ( VNOM ) is one of our favorite royalty trusts. VNOM is an MLP that involves a K-1, which we believe is a minor inconvenience given the attractiveness of the equity.

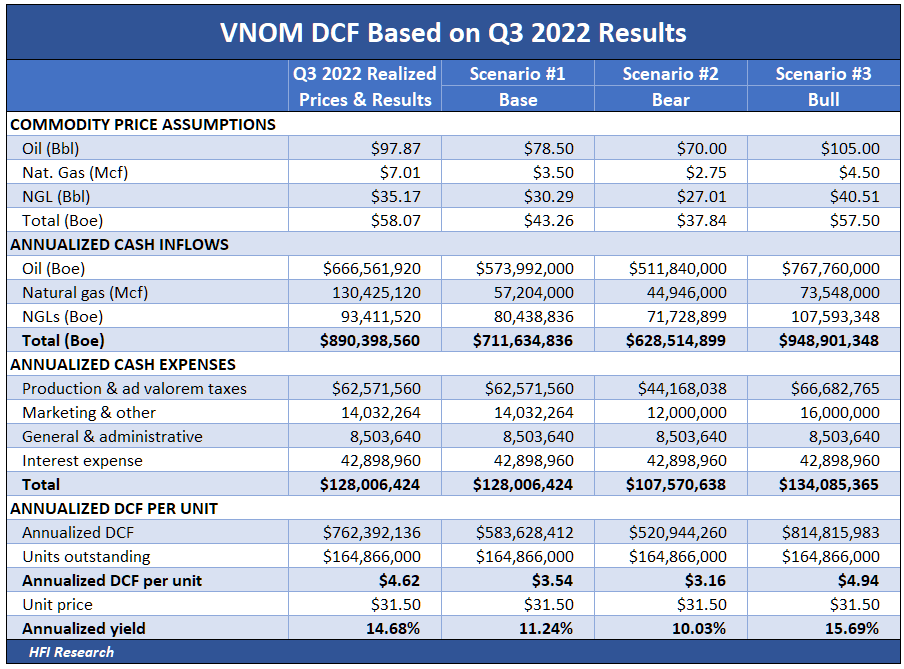

Since we last covered the name in May 2022, the company has outperformed our expectations. We expected annual distributable cash flow ((DCF)) of $550 million, but VNOM generated $621 million of DCF over the past four quarters. In response to the outperformance and the company's superb capital allocation, we're raising our price target on VNOM units to $36.00.

VNOM units currently trade at a 7.6% distribution yield, roughly in line with the midstream average, though slightly lower than peers such as Black Stone Minerals ( BSM ) and Sitio Royalties ( STR ). However, if we view the yield based on VNOM's total DCF - of which only two-thirds has been paid out as distributions to common unitholders - its units trade at a 10.9% yield using our Base case commodity price assumptions.

We believe VNOM units should be valued using total DCF and that a 10% yield is appropriate. This relatively high yield provides a cushion against the multitude of risks to which passive outside shale royalty investors are exposed.

Given the $3.54 of DCF implied in our Base case, in which oil averages $78.50 per barrel and natural gas averages $3.50 per mcf, VNOM units are worth $35.40, 12.4% above their current price of $31.5.

{kind=link}

VNOM units also offer protection against a downside commodity price scenario. Our Bear case implies that the units would trade at a 10.0% DCF yield at their current price if WTI averaged $70.00 per barrel and natural gas averaged $2.75 per mcf. In such a scenario, their value would be roughly equal to today's market price.

By contrast, in a Bull scenario in which WTI averages $105 and natural gas averages $4.50, the units would trade at a 15.7% yield at their current price. If their market price increased to maintain a 10% DCF yield in our Bull scenario, the units would trade up to nearly $50, a full 56.8% from their current price.

VNOM's 78% weighting to crude oil and NGLs is another advantage relative to its peers, many of which are weighted more heavily toward natural gas. As oil bulls, we consider the $105 per barrel in our Bull scenario more likely to be sustained over the next few years than the $70 per barrel in our Bear scenario. We, therefore, believe the units are more likely to appreciate from their current price even if natural gas prices remain depressed.

Another attractive feature that sets VNOM apart from many of its royalty company peers is the long productive life of its acreage. VNOM's depletion charge implies it has 23 years of production at its current rate, significantly more than most royalty companies. VNOM's long-lived asset portfolio makes its units more likely to sustain an EV/EBITDA multiple of more than ten times for many years if the company continues to be run with little debt.

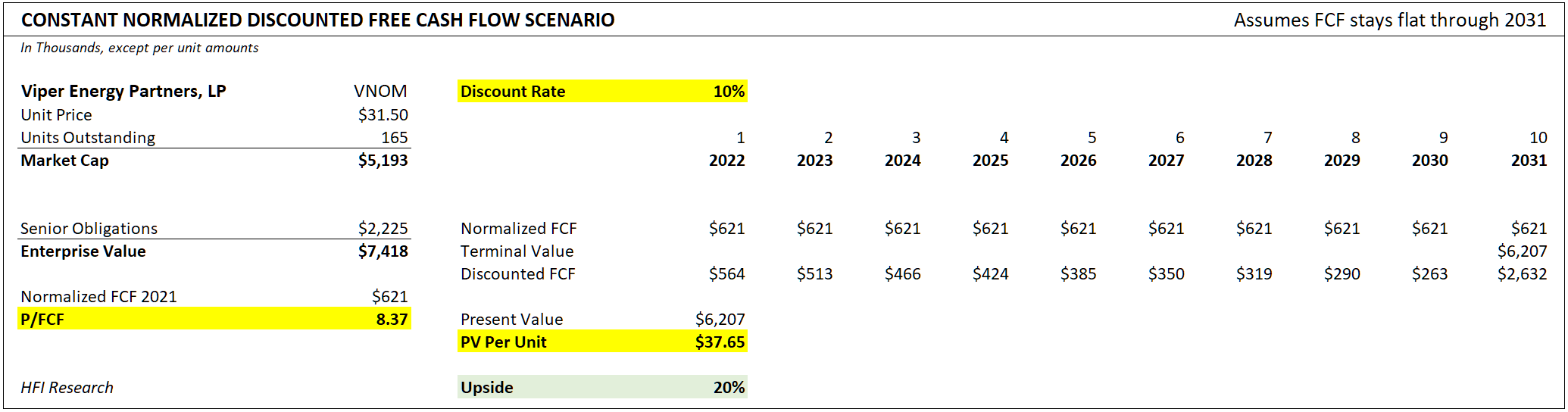

VNOM's long-lived asset portfolio allays concerns about its terminal value in a ten-year discounted cash flow valuation. Under such a scenario in which the past twelve months of free cash flow are sustained over ten years, VNOM units are worth $37.65 per share, which implies a 20% upside from its current unit price of $31.50. VNOM is yet another example of an unduly cheap MLP equity, albeit one that has elected to be taxed like a corporation.

{kind=link}

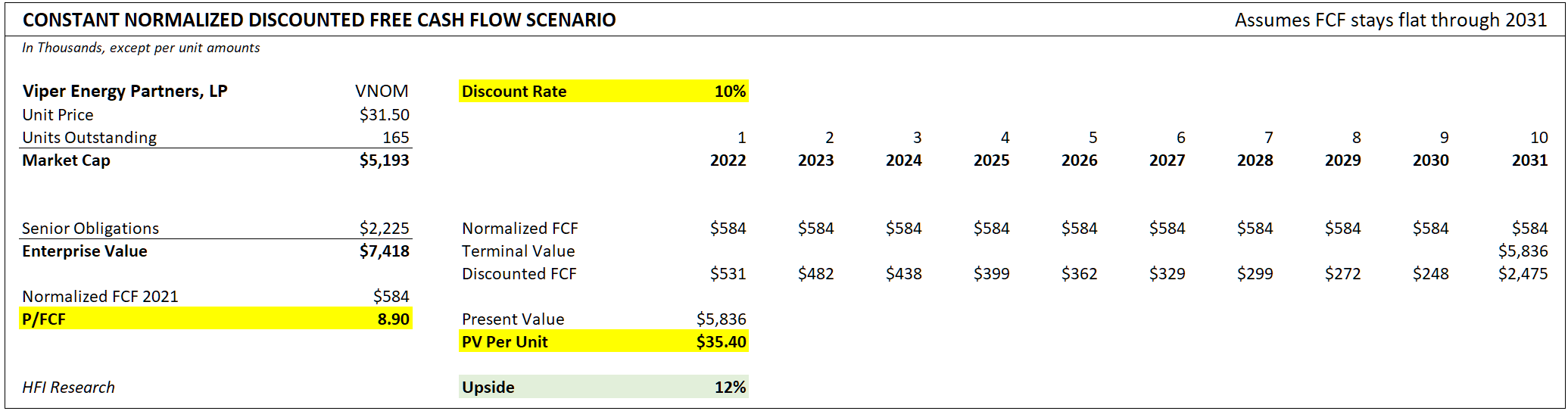

If, instead, we use the $583.6 million of distributable cash flow implied in our Base case shown above in a discounted cash flow valuation, the units are shown to be worth $35.40, 12% above their current price.

{kind=link}

The low price relative to value is advantageous to unitholders as management uses VNOM's excess cash flow to repurchase units, which is a good use of capital as long as the units are priced at a discount.

Capital Allocation to Remain Favorable for Unitholders

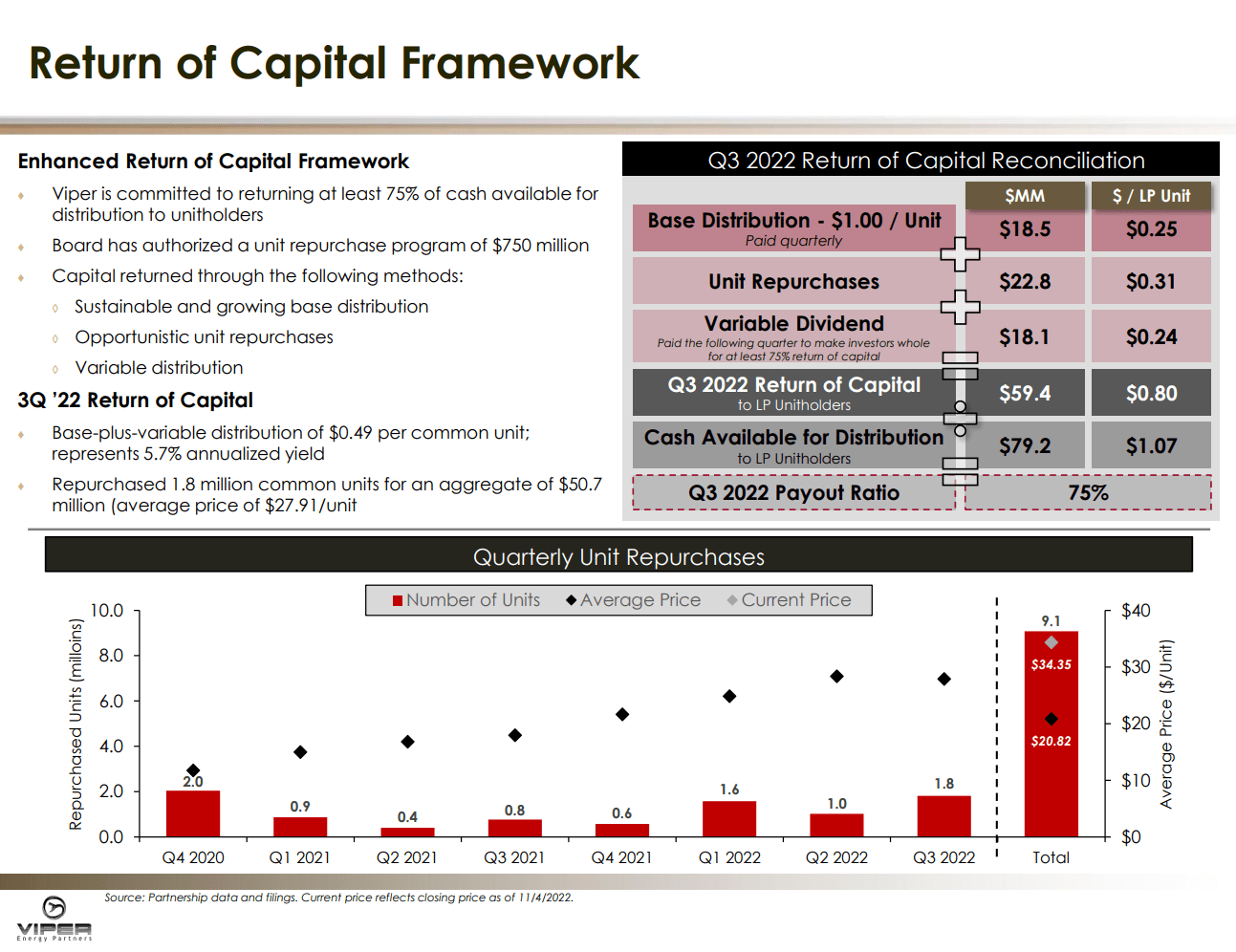

Viper Energy Partners LP management plans to return 75% of capital to unitholders through a combination of a base distribution, a variable distribution, and unit repurchases. We expect management to use the remaining 25% of undistributed cash flow to pay down debt and acquire additional royalty interests to replace reserves.

The following graphic lays out management's capital allocation plan. The framework is similar to that of VNOM's sponsor, Diamondback Energy ( FANG ), though, for VNOM, it's weighted more toward distributions than repurchases .

{kind=link}

In the third quarter, VNOM repurchased 1.8 million units, or more than 1% of the company's total unit count. The repurchases increased the company's oil production per unit by 2% from the previous quarter despite production being essentially flat. Since initiating its repurchase program in late 2020, VNOM has repurchased nearly 6% of its outstanding units at an attractive average price of $21 per unit.

As for production growth, management has clear visibility into Diamondback's capex plans. It has been reported that Diamondback is targeting approximately 10% growth on VNOM acreage in 2023. Since Diamondback represents approximately 60% of VNOM's total acreage, its growth should keep VNOM's total production growth in the mid-single-digit range.

Our valuation scenarios don't assume any benefit to VNOM's DCF from production growth, so any growth would provide an upside to our valuation.

Conclusion

Viper Energy Partners LP produces prodigious cash flow at current commodity prices, and we estimate its cash flow will increase by more than 30% if our Bull case assumptions are met. As such, we believe Viper Energy Partners LP is an attractive alternative for investors who seek exposure to higher oil prices without the risks and higher costs associated with oil and gas E&Ps. We rate Viper Energy Partners LP a Buy, increase our intrinsic value range to $34.00 to $38.00, and raise our VNOM stock price target to $36.00.

For further details see:

A Conservative Way To Play Higher Oil Prices: Viper Energy Partners