MSGE - A Deep Dive Into Sphere's Unit Economics And Valuation

2023-10-19 10:00:00 ET

Summary

- The Las Vegas Sphere is a $2.3 billion entertainment venue that is described as a "game changer" in live entertainment.

- Sphere Entertainment Co.'s unique asset and content structure will likely produce higher gross margins than Street estimates.

- This $2.3 Billion cash-burning behemoth is about to turn into a $200m+/yr cash printing machine.

Quick Take

Sphere Entertainment Co. (SPHR) is a publicly traded company that operates two major segments, MSG Networks and Sphere Las Vegas. The latter segment is a very interesting asset that has little operating history or comparable data. The market is currently valuing it based on traditional entertainment venue operations that are likely inappropriate. The error is due to the fact that the Sphere segment owns 90%+ of its content (unlike a stadium that relies on independently owned sports teams or musical performers). As a result, SPHR gets to keep the majority of its box office, concession sales, and advertising revenues. In contrast, a traditional venue often pays 50%+ of these revenues to the team/artist/performer.

SPHR's gross margins should be north of 80% versus analyst forecasts of 50%, which results in 3-10x higher levels of profitability. This $2.3 Billion cash-burning behemoth is about to turn into a $200m+/yr cash printing machine, and nobody knows yet.

Introduction

Social media is abuzz with Sin City's latest flashy spectacle: Sphere Las Vegas. This massive $2.3 Billion superstructure that launched on September 29th, 2023 has been described in media reports as a "game changer" in the area of live entertainment venues. Being a regular Las Vegas patron myself, my interest is piqued by this spectacle and the potential valuation puzzle surrounding the publicly traded stock: Sphere Entertainment Co.

Motivation

Before we get deep into the analysis, I want to quickly review the motivation for why I think it's worth looking at SPHR, and the possible sources for why this stock could be mispriced:

- It's a first of its kind in terms of technological build-out and business model. This makes the company very hard to comp in terms of margins or multiples. Nobody has ever spent this much to create a performance theater with the primary purpose of hosting proprietary content.

- The company has provided little/no guidance about the expected revenues, operating costs, or content pipeline. This means people need to do a lot of groundwork, channel checks, etc. in order to even calibrate a starting point.

- Wall Street estimates from Sell-Side brokers are highly disperse. This means the market expectations are dispersed with a wide range of outcomes, resulting in a volatile stock price. The sell-side research reports are riddled with fundamental inaccuracies and inconsistencies.

- It's a recent spinoff, so historical financials are very messy and/or absent. Quant/algorithms cannot price this security very well using the financials due to the incomplete set of historical data and low sample size.

- The business model has high operational leverage. This means that small changes in revenue result in large changes in free cash flow (and valuation) once its fixed costs are covered.

- It's a catalyst driven business turnaround. Investors aren't good at pivoting, and the current investor base is incredibly exhausted of the Sphere cost overruns. It's hard for them to get excited and look at the business in the new light that shines upon them.

For these reasons, I think a careful analyst/investor can have an edge over an otherwise very wise market consensus. Sphere has the potential to be worth a lot, or a little, depending on how its operations shape up in the coming year. This article will attempt to address the business operations and build a reasonable forecast of where we may end up. Now let's dig into the company.

Valuation of two business segments

The Sphere business can be broken down into two very different distinct segments:

- MSG Networks - The regional sports and entertainment networks that operate various streaming services and media delivery networks in the New York Area.

- Sphere - The giant 20,000-person (17,600 seated) live event theater located on the Las Vegas strip.

The company has a market capitalization of $1.2 Billion (based on a $35 stock price), plus $1.3B of debt, and $600M of cash which means the current enterprise value of the business is about $1.9 Billion.

(As of August 18th, the firm has $341M of unrestricted cash on the balance sheet , and in September , they announced the sale of a large block of MSGE shares that they held for $256M. That means that the company currently holds about $600M of cash on hand.)

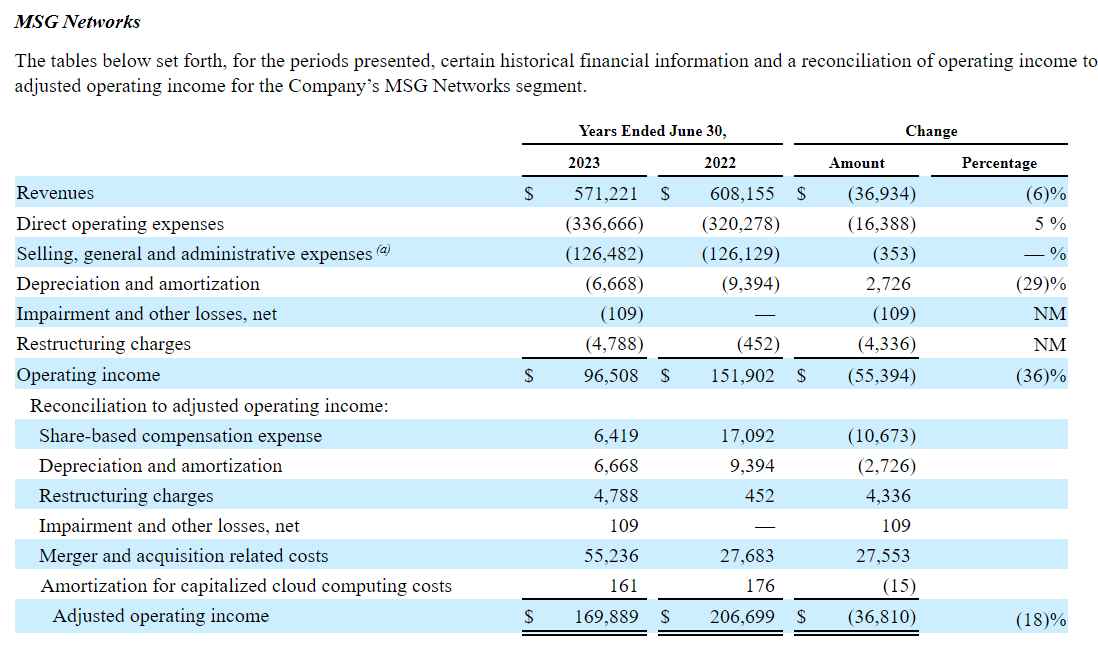

The MSG Networks portion of the business is a mature, somewhat steady (but declining) business. You can see that it generated $170M of adjusted operating income last year, and $200M the year prior:

{kind=link}

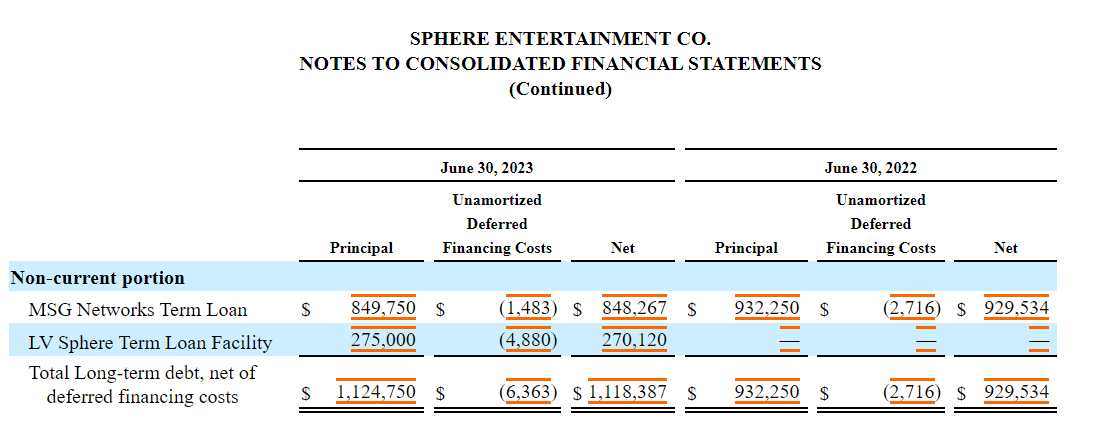

For the sake of our analysis, we can do an interesting trick, which is that we can ignore the entire MSG Networks segment and deduct its debt from the enterprise value to simplify our valuation problem. There are two reasons why we want to do this: First, the business itself isn't terribly interesting to analyze and given that it's a developed business, the valuation shouldn't be dramatically mispriced. Second, there is ~$930M of debt on the SPHR balance sheet that is written against the MSG Networks business and non-recourse to Sphere. That means that if it defaults, the lenders can only take the MSG Networks business (and all of its cashflows) away from SPHR but can't touch any of SPHR's assets or business.

In theory, SPHR can easily jettison that entire part of the business at will (practically speaking, it wouldn't, but a spinoff of separation of the business isn't out of the question). So, we can value that portion of the business at $930M because that's the size of the loan written against it.

{kind=link}

If we start with the $1.9B Enterprise value, subtract the value of the MSG Networks of $930M* ($850M of Non-current, and $80m of current), and a parcel of land in Stratford London that they hold worth ~$100M, we're left with the Sphere being valued by the market at about $870M.

I believe The Sphere can generate as much as $200M of Adjusted Operating Income in FY2025, and would be appropriately valued at 15x. That would imply nearly a $3 Billion valuation compared to the current market-implied value of $870M, and, combined with the rest of SPHR's parts, garner a $90 share price versus the current price of $35.

* Note: We're basically saying the equity value of the MSG Networks business is zero, which I think is conservative. We will revisit this later with some upside sensitivity analysis.

The Sphere's operations

The Sphere's physical operations are comprised of two main locations:

- The Sphere in Las Vegas - 20,000 person theater located on the Las Vegas strip.

- Sphere Studios - 68,000 square foot development facility and 28,000 square-foot quarter sized version of the Sphere. Located in Burbank, CA.

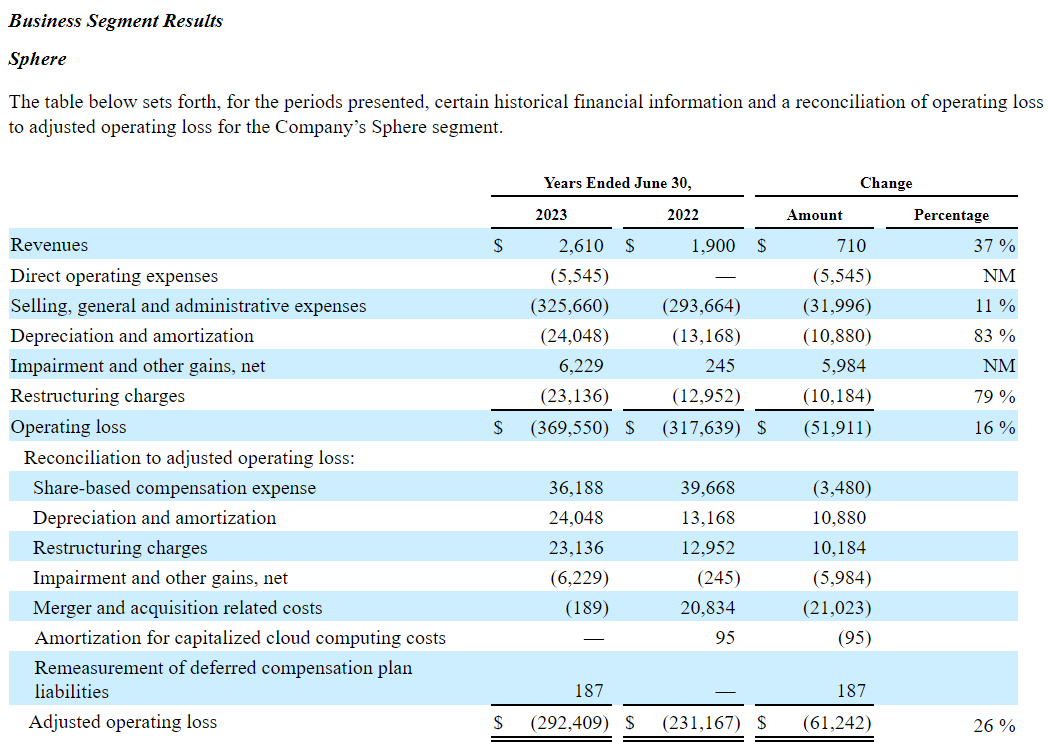

Quite naturally, the Sphere Studios is where all of the R&D, testing and content development takes place. And the Sphere Las Vegas is where everything is showcased to paying audience members. This is the segment level reporting for The Sphere for the last two years. Historical revenues are essentially zero, since the Sphere only opened on September 29, 2023.

{kind=link}

As you can see from the historical operating results, the Sphere has been losing an incredible sum of money, with adjusted operating losses of $231M and $292M, with no meaningful corresponding Revenues. Now that the Sphere has opened, we can start to forecast FY2024 and FY2025.

Revenues

It's always fun starting with zero revenues because whatever you forecast will almost always be quite wrong. You have no number to start with, no growth rate to use, and no guidance. Fortunately, we have started to see some audience data and reviews from the opening shows of U2 and Postcard from Earth that we can use to extrapolate.

Sphere's revenues come from 5 different sources: Live Artist Residencies, Immersive Experiences (i.e., custom films), Corporate Takeovers, Executive Suite Sales, and Exterior Advertising & Signage. Here are my expectations:

Author's model

Note that the increase from FY2024 to FY2025 is primarily due to the fact that FY2024 only has 3 quarters of revenue generating operations, versus FY2024 has 4 quarters. Now, lets jump into the assumptions that drive each of the Revenue lines:

Live Artist Residencies

Author's Model

Stadiums are rented out to performers for a set price (premium stadiums are about $500k per night), and the performer/act then takes on the economic risk of the event. According to the LV Review Journal, U2 will receive 90% of ticket revenues and the Sphere will receive the other 10% plus most of the services fees. I think the uniqueness of the Sphere will allow them to negotiate a better cut over time with subsequent artists.

My forecast of FY2024 residency nights of 55 is based on the 25 nights that U2 is committed to perform in CQ4'2023, and an additional 15 nights in the subsequent two quarters. U2 has a two-year option to renew their residency and, given the huge response to the first 25 nights, it's hard to imagine they won't renew. The full occupancy of Sphere is 20,000 (including General Admission), and I estimate the average price for a U2 ticket is about $330. These are the U2 ticket prices before they increased prices.

{kind=link}

I expect Sphere will sign at least one new artist residency that will start performing towards the second half of the calendar year, which will likely get us close to 70 nights in FY2025. I've used 18,000 (90% capacity) and $300 ticket prices to account for potential future resident artists being less popular than U2. Given the high prices of drinks at the venue (and Vegas in general), as well as the premium ticket price, as well as the 23 suites that cater towards big spenders, I expect the average concession/merch spend to be $35-$40 per person.

Immersive Experiences ( Postcard from Earth )

The Sphere currently operates its first immersive experience, Postcard from Earth , directed by Darren Aronofsky. They spent about $61M to film and produce this movie, and it runs 3-4 times per day, whenever the Sphere is not being used by a live act or a corporate booking. Currently, it is sold based on a 5000 seat capacity (only the middle section of the Sphere, and no standing room/GA area). Tickets range from $49 to $249. This product (and future experiences like it) is expected to be a very high-margin business for the Sphere.

Author's Model

Since opening day, ticket sales have been steady (~65% utilization) for Postcard and I expect them to continue at a moderate/high capacity on a daily basis. It may seem odd that the "Bull Case" has fewer show dates, and that's because the "Bull Case" has higher corresponding live-artist and corporate booking dates. The theater's section and pricing breakdown is as follows, with a full sell-out show generating $580k of revenues with an average ticket price of $114. (Based on October 2023 data).

Author's Model

A large driver to the economic success of the Sphere comes from selling these seats on a consistent basis. I believe this is possible given the enormous volume of tourists (40M/year) that visit Vegas annually. I think a very good comparison point for demand is Cirque du Soleil which runs 6 different shows nightly in ~1800 person theaters (with two shows many nights). Similar to Cirque, I don't see the Postcard experience to be the primary reason to visit Vegas, but rather, something people do while they're in Vegas. This is generally aligned with management's view where they compared this to the Christmas Spectacular show that they run in New York. Last year, they sold 930,000 tickets across 181 performances and achieved revenues of more than $130 million all in the span of 8 weeks.

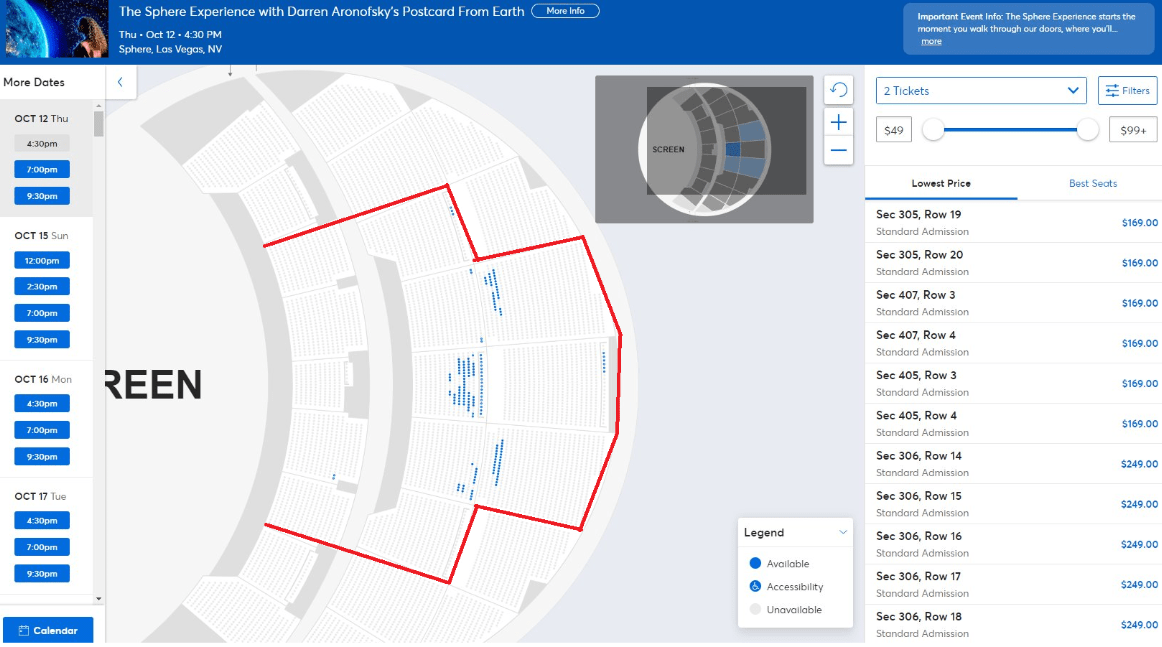

Here's a recent screenshot of the Thursday Oct 12th, 4:30PM showing that is almost entirely sold out. (The red section is the 5,000 tickets available for a Postcard showing. The other seats are currently only available for concerts).

{kind=link}

It's important to understand that the audience in Las Vegas is very temporally homogeneous. In a typical city, when you run a "new show," it's new for 3-6 months but the local audience eventually gets fully saturated. Due to Las Vegas' enormous annual tourist draw, every month " Postcard from Earth at The Sphere " is new to an entirely different audience cohort. For that reason I believe early utilization data (~65%) is indicative of base demand at least 1 year out, and realistically longer. In addition, they will refresh their content with new experiences in addition to Postcard from Earth .

You can read the Ticketmaster reviews for Postcard here . The current rating is 3.6/5.0 stars which may seem low, but if you read the detailed reviews (I urge you scroll through them for context) nearly all of the negative reviews are due to logistical problems, not the show content or technology. I expect the company to have worked out the early venue frictions very soon, and for the rating to increase dramatically.

I expect a moderate level of upside in these revenues over the coming years as they have the following levers:

- Adding extra shows on peak days

- Optimizing the ticket/section prices (it's not very granular right now)

- Offering "mini-content" packages that are differentiated from full feature productions like Postcard from Earth .

- Increasing the ticketed areas (from 5000 to 8000)

- Adding new shows (as good as Postcard is, it's the first feature they've made and I'm sure they'll come up with better content over time).

It's easy to dismiss the Postcard from Earth as an overpriced IMAX movie that isn't going to succeed. It's also easy to underestimate the earnings potential of a proprietary content offering. To help provide context, I want to dig a little deeper into the "Christmas Spectacular" that the CEO, James Dolan has referenced multiple times, because I don't think people appreciate how valuable that asset is.

We feel we're kind of uniquely qualified to look at this part of the business because maybe one of the most similar kind of businesses that's out there is the Christmas Spectacular. (James Dolan, CEO, Sphere).

The Christmas Spectacular is a 90-minute show in New York City that runs annually during Christmas. It's a live dance show featuring the famous Rockettes dancers. During its typical 8-week run, it generates 15% of MSG Entertainment's (MSGE) entire annual revenues. To understand how disproportionate that is, the show run represents just 2.5% of MSGE's entire seat-calendar capacity for the year, it punches a whole 6x its weight in terms of revenue generation efficiency. Even more extreme, is the fact that Morgan Stanley estimates that the show's 60% gross margin generated $79M of Gross Profit in 2023, compared to MSGE's company-wide Gross Profit of $372M, or 21.2%.

Morgan Stanley

What Dolan set out to do is recreate the financial model of the Christmas Spectacular , and apply operating leverage to it by requiring nearly zero exhibition costs (compared to paying dancers, stage crew, production people, etc.), offering it in a 20,000-seat theater instead of 6,000 seat theater, and running it year round. This operational leverage was very expensive, they spent $2.3 Billion to build a platform to do this, but lucky for present day investors, this has been paid for by investors of the past. Provided they can keep Postcard from Earth (and subsequent films) moderately utilized, the Sphere will generate an enormous amount of cash consistently.

Corporate Takeovers

The Sphere will rent the facilities to corporations that want to use it for special events. It has been confirmed that they already booked Formula 1 and the Superbowl week dates, as well as CES. There will likely be other high profile dates throughout the year that will naturally fit corporate/branding needs.

Author's Model

They have not released the prices, but I believe it will be at least $2M per day, if not significantly higher. Corporate takeovers happen on very high-traffic days and then the Sphere needs to forgo showing Postcard (which would generate $1.5M+ assuming 3 sold out shows to accommodate the booking). Given that over ten F1, Superbowl, and CES days have already been booked for FY2024, getting to 20 seems quite plausible. Given my pretty conservative price estimate of $2M/day, even if they don't sell the corporate booking, they'll sell seats to Postcard instead and the revenue differential will not be dramatically different. There is significant upside if the corporate takeover price is > $3M per day, which is entirely possible. A price of $5M per day during Formula 1 would not surprise me- as I expect the Sphere to shoulder a significant burden of costs to develop unique content for the corporate takeover.

Executive Suite Sales

The Sphere has 23 suites, each with 32 seats. These will be leased to corporations/individuals who want to own the suite, similar to the way suites work at stadiums. A suite for a single U2 show is likely worth about $30K given typical ticket prices. If there's 50 residency nights next year, that makes the suite's sticker price land at $1.5M. However, typical suites at stadiums cost $500k-$1M per year. I've used $1M as it provides a reasonable discount to the ticketed face values.

Author's Model

A key differential in this suite model compared to the sister-company MSG Entertainment (owning Madison Square Garden, etc.) is that when the Garden leases a $1 Million suite, 67.5% of it goes to MSG Sports . Presumably for the Sphere, they keep the entire revenue stream for suite sales (minus some ticketing pass through that would go to the artist on a per night basis).

Marketing Ad Sales

The exterior of the sphere, or Exosphere as they call it, is available to rent as advertising space. Media reports suggest the rate is about $450,000 per day, or $600,000 per week to rent space.

Author's Model

The company has a ton of experience selling advertising on MSGS' various stadium properties, billboards, etc. In this segment, I've completely ignored the naming rights (worth $10m/year+, and other interior signage branding opportunities). Once established, I think the marketing segment can potentially generate in excess of $30m/year.

Total Sphere Revenues

Author's Model

SG&A and Direct Operating Expenses

What strikes me is the enormous SG&A costs for FY23 of $325 Million. Note, this is not directly related to the $2.3B construction cost of The Sphere which is a capital expense. This is also not related to the $61M that the company spent to create its first feature film (Postcard from Earth), which is also capitalized. On a cash basis, SPHR burned about $1.3 Billion (~1B of Capex in FY2023 to complete the Sphere).

I believe that the $325M of expenses from FY2023 contained large amounts of one-time ancillary expenses associated with building out the Sphere and Burbank campus that will not be recurring in FY2024. If so, they will likely spike in FY24Q1 (the last 3 months leading up to the opening of Sphere), and then taper off starting in FY24Q2. On the latest conference call, the CFO alluded to this when discussing the FY23Q4 results:

This included $90 million of adjusted operating loss in the Sphere segment, which primarily reflects corporate overhead expenses related to Sphere Studios and associated content and technology development, as well as costs related to the Las Vegas venue as we prepare for the opening next month. (Gautam Ranji, CFO, Sphere).

And more:

We expect Sphere operating costs to increase in fiscal '24 first quarter as we ramp up operations in Las Vegas. (Gautam Ranji, CFO, Sphere).

This likely means that the ~$90M of SG&A that the firm realized in Q4 of FY2023 will increase in FY2024Q1. However, they are not explicitly stating what will happen in the remainder of FY2024. Assuming an increase from $90M to $100M, and a straight line run-rate for the year, one would expect SG&A to increase to $400M for FY2024. I've forecasted $350M because I strongly believe this will decline in the back half of the year.

In order to actually open and operate the Sphere, they'll need to hire an army of ushers, concession stand operators, security, etc. Those will be considered Direct Operating Expenses . This is also mentioned in the conference call:

And this from James Dolan, the CEO:

All right. Let me take the first part of that one. So, let's start with our own original content, which really is sort of the backbone of the business. That is basically a high margin business because you've already invested your capital. You've made your show, you've built your attraction, and now your running costs are basically things like ushers, security, merch, those kinds of things. (James Dolan, CEO, Sphere).

We have no operating history to rely on, but I've built up the operating costs from the ground up based on the following assumptions:

- $50 Million for Facility Staff ($60k/yr x 800 FTE employees)

- $25 Million for Electrical, Utilities, Maintenance, etc. ( $10M/yr of Electricity )

- 5% gross cost on Food, Beverage and Interchange Fees ( Beverage Prices )

- Note: I'm recording Ticketmaster revenues based on the net ticket prices ($50 + $7 service charge, this means Sphere gets $50 and Ticketmaster gets $7. There's a world where Sphere gets $57 with a $7 COGS charge to Ticketmaster which would decrease margin % but be neutral margin $).

{kind=link}

Author's Model

Valuation

As you can see in FY2025 (the first full year of matched revenues and expenses), the Sphere generates an immense amount of adjusted operating income (similar to EBITDA). I've used a 15x multiple based on the uniqueness of this premium venue, and its high growth potential. This is how I arrive at a $2.8B valuation on the Sphere segment. If you add back the cash, London land, and MSGE network, you end up with a total enterprise value of $4.3B, market capitalization of $3.1B, and price per share of ~$90.00

There is a clause that the Venetian hotel will get rights to 25% of the after-tax profit of the Sphere, after certain return hurdles have been met. Given the massive capex, I presume the return hurdle will be quite high, but can't model it precisely. For now I've ignored it but it will become relevant once the company starts to make significant amounts of money.

Sources of valuation discrepancies

My claim is that Sphere is worth $90+ versus professional Wall Street Analysts suggesting it's worth closer to $25 needs to be reconciled. At a broad level, I would say the primary driver of the different forecasts come from the gross margin assumptions. Here's Morgan Stanley's model for the Sphere segment:

{kind=link}

I think the gross margin number is based on the analyst community incorrectly using MSG Entertainment, (which owns/operates Madison Square Gardens, The MSG Theatre, Radio City Music Hall, The Beacon Theatre, The Chicago Theatre) to incorrectly comp the direct operating costs. The cost structure of MSGE is dramatically different than Sphere, because MSGE doesn't own the majority of its content (i.e. sports and concerts in the theatres). As a result, MSGE (MSG Entertainment) has to pay MSGS (MSG Sports) a full 50% of sports concession profits , 67.5% of suite rental fees , a cut of the marketing/signage fees , leases, and licensing fees. These are all recorded as direct operating expenses and decrease gross margins. One way to look at it is that the Morgan Stanley margin estimate for Sphere closely resembles their estimate for the Christmas Spectacular of 60%. However, that show is live and requires a plethora of performers and stage and production crew, which all are charged against gross margin.

For my bottom's up build of Direct Opex, I cannot see what direct operational costs exist for SPHR other than staffing the building to take tickets, sell tickets, security, utilities, admin/maintenance, and wholesale food/beverage costs. This is mostly validated by both the company's 10K, and the CEO's statement:

That is basically a high margin business because you've already invested your capital. You've made your show, you've built your attraction, and now your running costs are basically things like ushers, security, merch, those kinds of things. So the return on that is pretty strong. (James Dolan, CEO, Sphere).

Morgan Stanley has also modelled a tapering of SG&A in the coming years (in agreement with me), and surprisingly has significantly higher audience estimates than I do. In fact, their 6000 average attendance exceeds the company's (currently) stated capacity. However, given the huge gross margin differential, I'm forecasting nearly double the Adjusted Operating Income with about 20% less revenues.

Here's a summary of different forecasts:

Author

The Macquarie model has similar gross margins as Morgan Stanley, but strangely they arrive at their revenues in a significantly different way. They're using a 9,000 seat arena, and a $70 average ticket price (this mathematical combination is impossible given current prices). They've also hardcoded a 49% Opex cost into their model. They're also recording the residency revenues as a venue fee of about $31M, versus Morgan Stanley is recording the ticket sales from residencies at $150M, a 5X difference of revenue for a similar number of shows. Despite one recording gross and the other recording net revenues, their gross margins on the top line are similar.

{kind=link}

The point of this isn't to point out different model errors or projections. I'm sure my model also has errors. But when I model something and it's drastically different from the street- my first, second and third assumptions are that I'm wrong. On the surface, I'm uncomfortable with the gross margin assumption that I've used, especially because it is so different from the street. However, when I review their assumptions, there are core issues that are objectively incorrect (or very questionable to say the least). Given the models have somewhat simple errors in them, it's entirely plausible that more complex values (like Gross Margin) could also be significantly different from reality- and closer to my estimate. Although my estimate of 80% gross margins may not be realized, I strongly believe my forecast is directionally correct, and that the realized gross margins will be substantially higher than the current market consensus.

I'll also add that this discrepancy isn't unusual given the circumstances of the company. They're about to pivot the business from "A company that was building Sphere" to "A company that operates Sphere," and those two businesses should look almost entirely different. In addition, to date, the company has provided very little guidance for people to calibrate off of. As a result, having an opinion that is differentiated the market, that has been well researched and is ends up being correct, will be incredibly valuable.

Sensitivity analysis (upside)

Here is a list of factors, and their accompanying change in valuation:

| Change to Model |

| Share Price |

| MSG Networks Equity worth $400M instead of $0 (Only upside) |

| + $12 |

| $30M annual naming rights sold (Only upside) |

| + $14 |

| Every $5/person change in Food and Beverage sales |

| +/- $7 |

| Every 5% Seat Occupancy above/below 75% |

| +/- $11 |

| Every 5% reduction in gross margin assumption |

| - $15 |

Sanity Check

Here are a few high level notes that I'm using as a sanity check:

- The company spent $2.3B to build an asset, and that asset has exceeded expectations (Based on consumer and professional/media reviews). It's not crazy that the asset is now worth $2.8B.

- The business model (before they started building) could not possibly be expected to spend $300M/Year on SG&A to support a $1B asset build. The SG&A number must be excessively high due to one-time costs, and if they choose to cut aggressively I believe they can bring this down to $150M and still create/produce new original content and support Sphere 1 operations. As a result, as long as a moderate level of revenues persists, I think they will "right-size" their fixed costs to drive solid profitability. Or that high SG&A will be justified with high expansion/growth results.

- Macquarie is valuing Sphere at $333.6M. That is comically low, and is really hard to justify given that U2 just sold $170m of tickets over 25 nights in the venue.

- My forecast of a 30% adjusted operating margin is very high, but this is the most ambitious entertainment build-out, in the entertainment/tourism capital of the world. If there's one place that's most likely going to allow you to succeed at generating abnormal returns on investment, it's in Vegas.

- The market implied value of $870M for the Sphere is very low given the $2.3B build cost. Unless you expect the operation to excessively burn its very high contribution margin dollars on pipe-dream expansion plans (which is possible!), this asset should be worth quite a bit.

Upcoming catalysts to watch For...

- Announcement of U2 Residency being extended

- Announcement of additional residencies

- Announcement of naming rights to the Sphere being sold

- Monitor Ticketmaster sales data to see how Postcard sales are tracking (I have an automated scraper to track daily sales and occupancy levels)

- New/frequent new ads showing up on the Sphere ( livestream )

- Q1'2024 Earnings released in early/mid November - Management will provide some guidance (we'll also see 2 days of U2 revenue recognition on the Q1 numbers). Realized gross margins will likely be bad due to September start-up costs vs 2 days of revenues.

- Q2'2024 Earnings released in early/mid February - We'll see a full operating quarter and see realized Q2 gross margins (60% or 80%?), as well as hear about future SG&A plans.

For further details see:

A Deep Dive Into Sphere's Unit Economics And Valuation