KMLM - A Deep Dive On Managed Futures

2024-01-16 00:44:36 ET

Summary

- Managed futures have robust evidence supporting their inclusion in long-term investment portfolios.

- Adding managed futures to a portfolio can lead to lower standard deviation, higher returns, and higher Sharpe/Sortino ratios.

- Managed futures provide an uncorrelated source of return and can increase withdrawal rates in retirement.

A recent discussion broke out on my last piece Designing a Balanced Portfolio for Retirement , on managed futures and their merits. As I received a number of questions on the topic, I thought it worth going through a deep dive on the subject. What they are, how you can use them, and what role they serve in a portfolio over the long run. So, let's dive in.

Evidence on Managed Futures

The evidence on managed futures is quite robust. While I will only cover a sampling of the many research studies concerning managed futures, the following will serve as sufficient evidence to make the case for managed futures in long-term investment portfolios.

The most logical place to start this analysis is in the landmark study by John Lintner as discussed in The Hedge Fund Journal :

John Lintner first widely published several of these benefits in his seminal 1983 paper, "The Potential Role of Managed Commodity-Financial Futures Accounts (and/or Funds) in Portfolios of Stocks and Bonds." In the paper he concluded that every well diversified portfolio would benefit from exposure to managed futures."

A further analysis showed that:

The findings of his work, namely that portfolios of equities and fixed income exhibit substantially less variance at every possible level of expected return when combined with managed futures, remain as true as ever more than 25 years later.

But the best evidence is from Lintner himself:

Indeed, the improvements from holding efficiently selected portfolios of managed accounts or funds are so large - and the correlations between the returns on the futures portfolios and those on the stock and bond portfolios are surprisingly low (sometimes even negative) - that the return/risk trade-offs provided by augmented portfolios consisting partly of funds invested with appropriate groups of futures managers (or funds) combined with funds invested in portfolios of stocks alone (or in mixed portfolios of stocks and bonds), clearly dominate the trade-offs available from portfolios of stocks alone (or from portfolios of stocks and bonds). Moreover, they do so by very considerable margins. The combined portfolios of stocks (or stocks and bonds) after including judicious investments in appropriately selected sub-portfolios of investments in managed futures accounts (or funds) show substantially less risk at every possible level of expected return than portfolios of stock (or stocks and bonds) alone. This is the essence of the "potential role" of managed futures accounts (or funds) as a supplement to stock and bond portfolios suggested in the title of this paper. Finally, all the above conclusions continue to hold when returns are measured in real as well as in nominal terms, and also when returns are adjusted for the risk-free rate on Treasury bills." [Lintner, pages 105-106]

Further exploration of the evidence on managed futures takes us to the 1994 paper "Managed Futures and Their Role in Investment Portfolios," by Don M. Chance. The paper is a thorough analysis of managed futures including a primer for beginners. In later chapters of the text, he explores the performance of managed futures within investment portfolios. This lays down the foundation for using managed futures as part of portfolios.

Managed Futures and Their Role in Investment Portfolios, Chance, 1994

{kind=link}

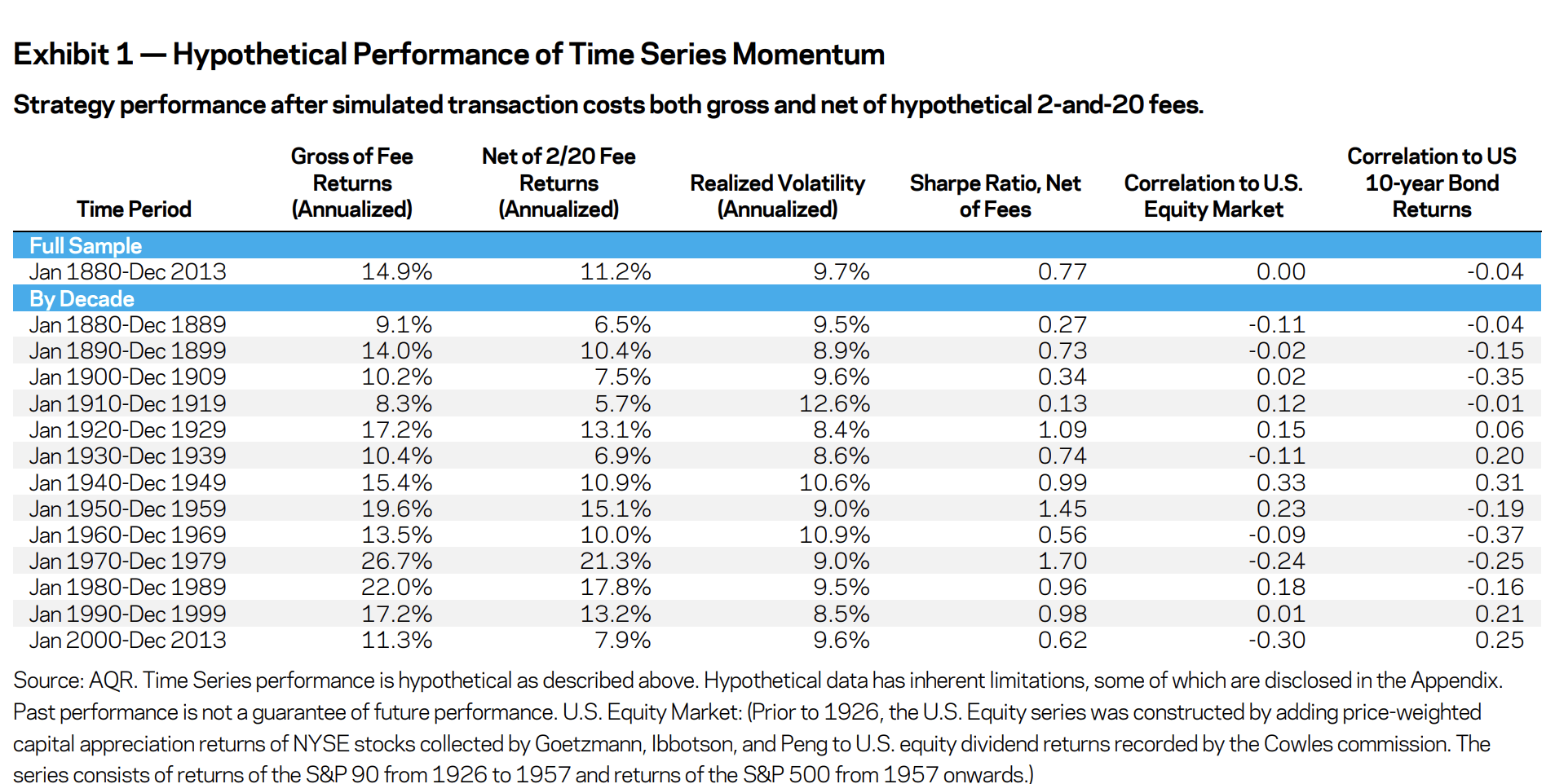

A continued exploration of the evidence comes from Brian Hurst, Yao Hua Ooi, and Lasse H. Pedersen, Ph.D., of AQR wrote a paper entitled "A Century of Evidence on Trend-Following Investing." They look at time series momentum offering both a definition of the strategy and describing their data set:

going long markets that have been rising and going short markets that have been falling, betting that those trends continue. We create a time series momentum strategy that is simple, without many of the often arbitrary choices of more complex models. Specifically, we construct an equal weighted combination of 1-month, 3-month and 12-month time series momentum strategies for 67 markets across four major asset classes - 29 commodities, 11 equity indices, 15 bond markets and 12 currency pairs - from as far back as January 1880 to December 2013."

They then show the merits of the strategy being its strong returns and negative correlation to US equity and fixed-income markets. In the past, these strategies were only offered to accredited investors who paid high fees of 2% plus 20% of gains, which is why the returns in the "net of 2/20 fee returns" column are lower. However, today investors can access these strategies from mutual fund and ETF structures at a more reasonable cost.

a large body of research has shown that price trends exist in part due to long-standing behavioral biases exhibited by investors, such as anchoring and herding [and I would add to that list the disposition effect and confirmation bias], as well as the trading activity of non-profit-seeking participants, such as central banks and corporate hedging programs."

{kind=link}

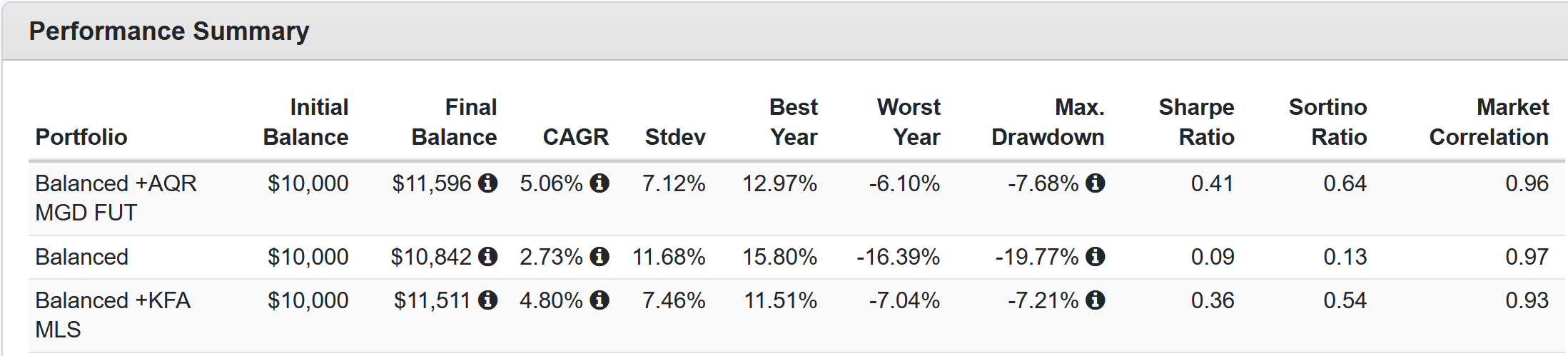

Below, I ran an additional analysis looking at live products and their correlation coefficients in relation to a balanced portfolio. For this analysis, I used a mutual fund strategy AQR Managed Futures Strategy ( AQMNX ), KFA Mount Lucas Strategy ETF ( KMLM ), and added them to a balanced portfolio reducing it from 50% stocks and 50% bonds to 40% stocks and 40% bonds adding 20% to each respective managed futures fund. I looked at the period of 2021-2023 which is all the data available for these funds. The usefulness of this data is that it is mostly noise, but still an interesting recent example of how managed futures performed during a left tail as we saw in 2022.

The results were as expected from the larger data set from AQR. Adding managed futures led to lower standard deviation, higher returns, and higher Sharpe/Sortino ratios.

Portfolio Visualizer Portfolio Visualizer

{kind=link}

{kind=link}

The real value of managed futures is their negative correlation to traditional asset classes. As I have explored in other pieces the way to market beating returns depends far more on avoiding losses than on hitting home runs. A catastrophic loss can result in the need to wait for an extended period just to get back to even. Therefore, adding uncorrelated assets such as managed futures has many benefits to the portfolio in its role as an uncorrelated asset.

X/Twitter

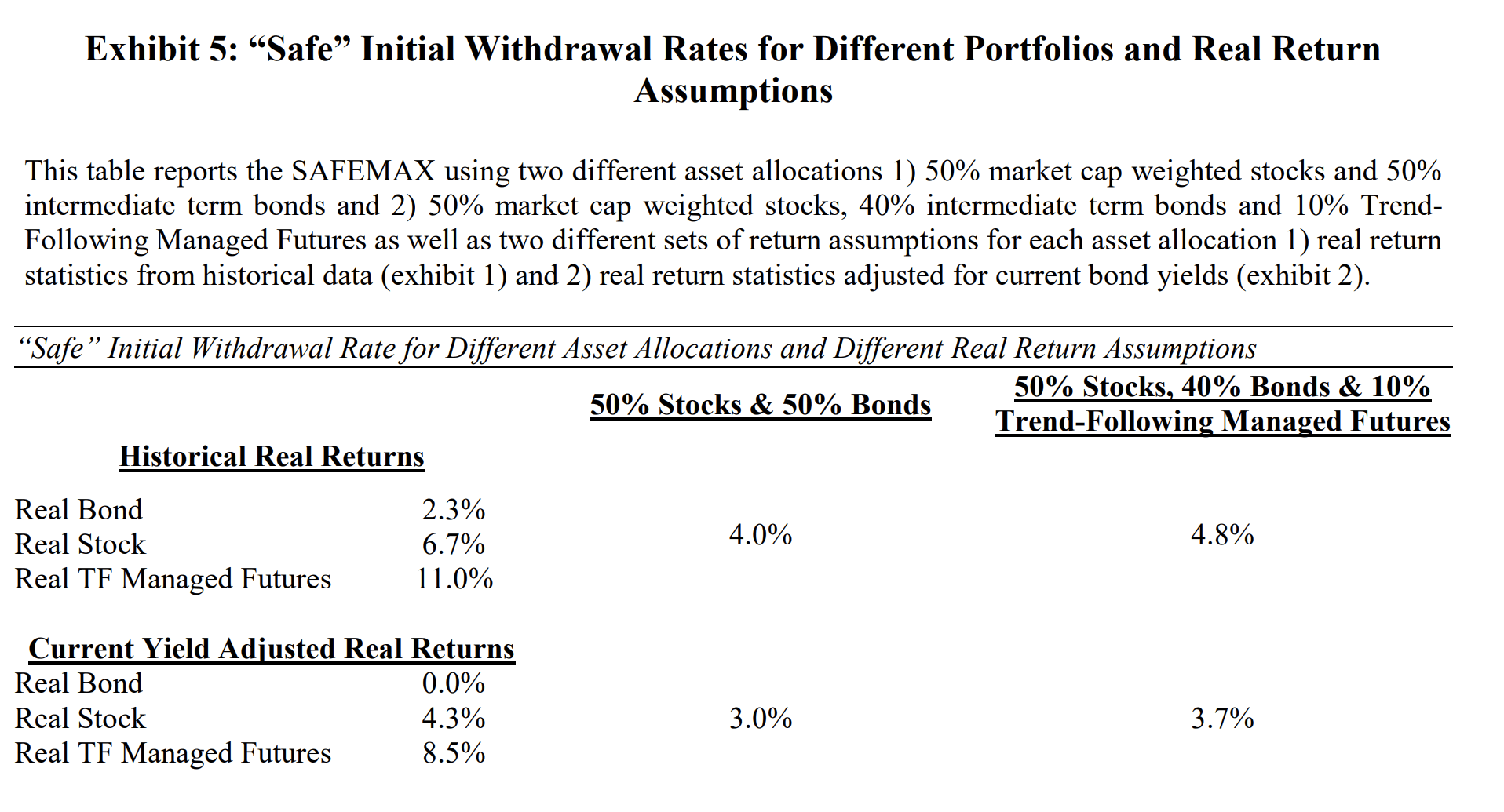

Additional literature has broad implications for retirees as well. Research shows that adding managed futures to a portfolio can increase withdrawal rates in retirement. Stating:

Using the trend-following Managed Futures time series data from Hurst, Ooi and Pedersen (2012), a 50% stock, 40% bond and 10% trend-following managed futures portfolio (50/40/10) is created. The 50/40/10 portfolio has a similar level of volatility as a 50% stock and 50% bond portfolio (50/50) over the period 1926 through 2012, as well as a similar beta to the Mkt-Rf risk factor over the same time period. The 50/40/10 portfolio was able to support a higher initial withdrawal rate using either the historical returns from the Hurst, Ooi and Pedersen (2012) or using a return series which discounts the return series from Hurst, Ooi and Pedersen (2012) to reflect lower current cash yields.

This study used data that ended in 2012 and thus assumed lower bond yields than we have today. However, even with higher bond yields, the case for managed futures in a portfolio is well founded.

{kind=link}

The authors conclude:

This paper illustrates that investors don't have to passively accept lower "safe" withdrawal rates. By using Trend-Following Managed Futures, it is possible to create a portfolio with the same standard deviation and MKT beta as a traditional 50% market cap stock and 50% intermediate term bond portfolio. Therefore, an investor should be largely indifferent between the two portfolios from a risk perspective."

An alternative body of evidence has questioned the findings on trend following and managed futures role in portfolios. The argument being that they are just the result of static bets and capturing normal factor premia. This argument was questioned by Abhilash Babu, Ari Levine, Yao Hua Ooi, Lasse Pedersen and Erik Stamelos, in their paper " Trends Everywhere " featured in the Journal of Investment Management. They conclude their paper with the following answer to the question:

The strong historical performance of trend-following strategies is robust across a large number of instruments, and this strong performance is neither explained by volatility scaling nor static exposures, but, rather, out-of-sample evidence of the trending nature of capital markets around the world."

The Behavioral Case for Managed Futures

The central argument for managed futures is that they go up when stocks and bonds experience left tails. Because managed futures are uncorrelated with traditional asset classes they tend to result in portfolios with higher long-term returns, lower volatility, and higher overall Sharpe ratios. A further benefit for growth investors is the ability to hold more in risk assets. Under normal circumstances, many investors believe that they can hold 100% equity portfolios, but when the market begins to take the elevator down, they bail on their strategy, thus locking in their losses.

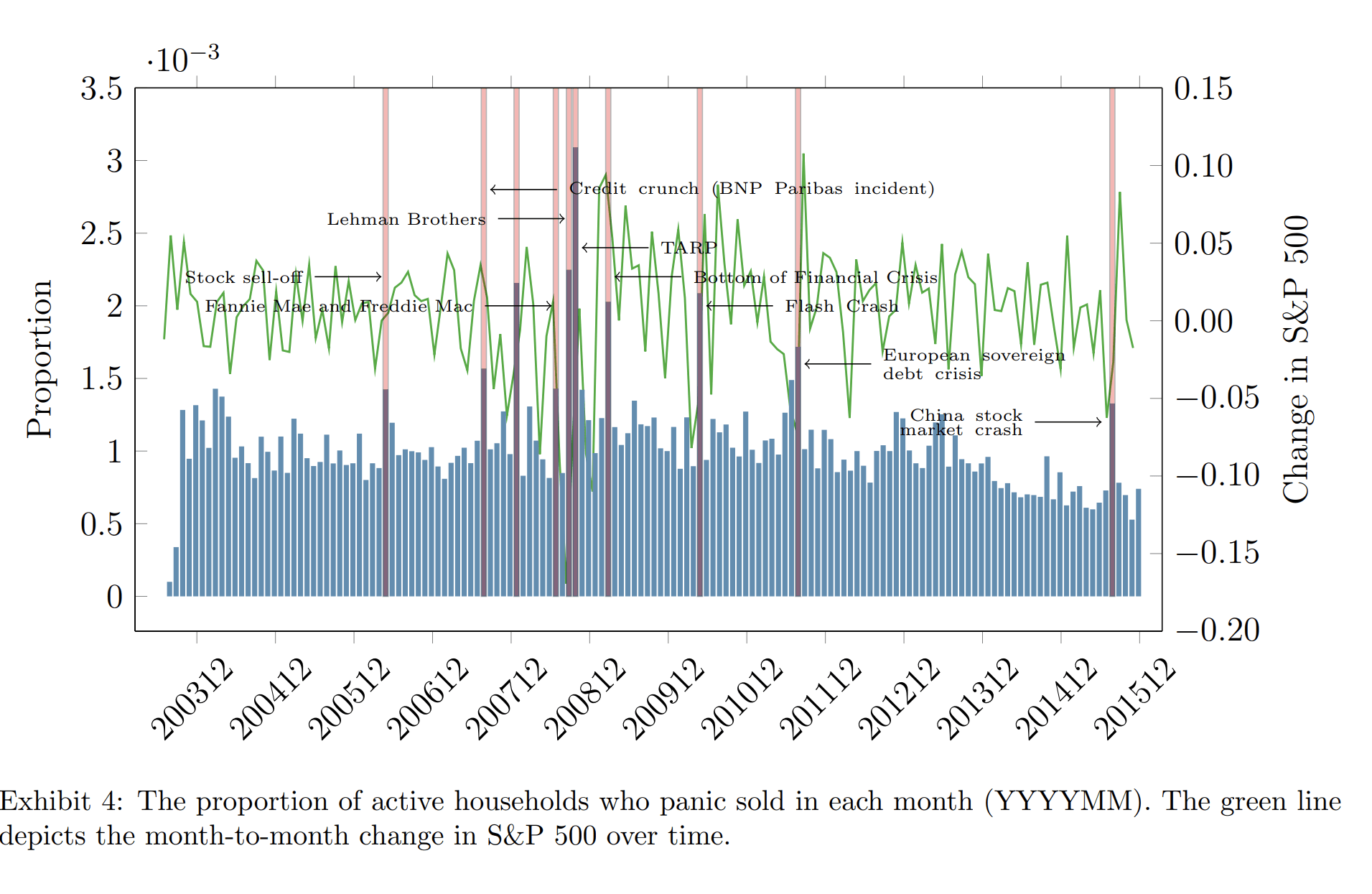

A study by the MIT Laboratory for Financial Engineering entitled "When Do Investors Freak Out? Machine Learning Predictions of Panic Selling" by Daniel Elkind, Kathryn Kaminski, Andrew W. Lo, Kien Wei Siah, and Chi Heem Wong, developed a heuristic to identify characteristics of investors who sell a substantial part of their portfolio in a severe left tail event.

MIT Laboratory for Financial Engineering

{kind=link}

When we look back at 2008 specifically, we see that investors earned extraordinary returns from managed futures during this left-tail event such that even a small 10% allocation to managed futures would have had a significant impact on the overall portfolio.

John Lintner's fine work...survived the ultimate litmus test through the historic financial meltdown of 2008. In the depths of the crisis, managed futures strategies, collectively, were one of the very few bright spots for investments (both alternative and traditional). While the post-crisis environment has been especially challenging, the intrinsic properties of these strategies could again play a vital role in protecting portfolios in future crises and beyond, as they have done during each sustained crisis over the last several decades." -A Quantitative Analysis of Managed Futures Strategies

Losing less means investors spend more time increasing their wealth rather than trying to make back what they lost. A typical 100% stock portfolio lost nearly 40% of its capital in 2008. A 40% decline requires a 67% return to get back to even. It took this investor until 2012 just to get back to a total return of 0%. A more extreme example comes from the Great Depression, where the market peaked in 1929 and would not return to those highs until 1953, 24 years later.

Lipper/Dalbar

Additionally, this assumes that the investor did not bail out of their portfolio during the relentless drawdown in the Fall of 2008. Research on the behavior gap shows a significant deviation between the returns of funds vs the actual returns earned by investors. Previous studies have shown that this gap can be as much as a 50% reduction in returns. Managed futures being added to the portfolio can alter human behavior during a panic sell moment offering ballast to the portfolio when you need it most.

CAIA Association

It is important to note that left tails tend to result in rapid increases in managed futures funds. Seeing as this is held more as a hedge and not an actual investment, it is important for investors to rebalance after a rapid rise in managed futures funds to avoid an unintended overweight. A quick note on tax considerations. Managed futures strategies tend to be tax-inefficient, so they are best held in tax-advantaged portfolios.

Conclusion

If I have seen further it is only by standing on the shoulders of giants..."

- Sir Isaac Newton

In conclusion, the evidence is robust in support of managed futures products. Even when the conclusions are questioned, a retesting of assumptions around managed futures presented above found that the sources of premia are robust and provide noted portfolio benefits in the form of an uncorrelated source of return.

In Managed Futures: A Risk Off Solution? by Aric Light in the CFA Blog Enterprising Investor.

we have two important observations:

1. Trend-following has a long-run positive expected return and, moreover, a positive expected return in both bull and bear markets.

2. Managed futures have an asymmetric return profile. They generally fail to keep pace with equities in bull markets but can still produce solid returns. In bear markets, however, they significantly outperform stocks, generating positive returns or, at minimum, much less downside.

A final resource is found in the paper "A Quantitative Analysis of Managed Futures" The paper seeks to update John Lintner's findings with more modern data. What they found is that Lintner's work was so influential it provided the foundation for future research. Furthermore, it could be validated decades later with new live data. In the ten years since this analysis was published managed futures have continued to perform as expected and have ample evidence to earn a role in investment portfolios. Allocations from 5-20% have been supported by the evidence. The authors' ringing endorsement for managed futures is a fitting conclusion to this analysis on the subject.

It is remarkable just how solid Lintner's long-term argument has remained through the test of time even when the performance of the recent challenging years is included in the analysis, as it has been here, through 2013.The inclusion of managed futures in an institutional portfolio leads to better risk-adjusted performance (either through the mean-variance framework, or through the more modern Omega analysis). The results are so compelling that the board of any institution, along with the portfolio manager, should be forced to articulate in writing their justification in not having an allocation to the liquid alpha space of managed futures. "

For further details see:

A Deep Dive On Managed Futures