AGNC - A Dozen Income Picks Yielding 12% Or More

2023-07-07 15:38:46 ET

Summary

- I recommend several high-yield income-oriented investments, including business development companies (BDCs), real estate investment trusts (REITs), and a closed-end fund (CEF) that holds midstream assets or master limited partnerships (MLPs).

- Regulated investment companies (RICs) offer high-yield distributions due to tax laws that regulate them and require them to distribute at least 90% of net income to shareholders.

- I provide specific recommendations for BDCs, REITs, and CEFs, including Trinity Capital, FS KKR Capital, Cion Investment Corp., and others that yield 12% or more annually.

In my most recent essay regarding income-oriented investments for those seeking high yield income in retirement, I reviewed 14 funds that yield 15% or more. It was a popular choice with readers, garnering more than 5,000 views in the first 2 days after it was published. There is apparently an appetite among investors seeking income that offers a substantial return in the form of monthly or quarterly distributions. In that article, I covered mostly CEFs and ETFs that pay dividends or distributions on fixed income, CLOs, or option premiums. In this installment of high yield income-oriented picks, I would like to add some BDCs (business development companies), a couple of REITs (real estate investment trusts), and a CEF that holds midstream assets or MLPs (master limited partnerships).

Many RICs (regulated investment companies) offer high yield distributions because of tax laws that regulate them and they are structured as RICs because they do not have to pay taxes on their earnings as long as they distribute at least 90% of net income to shareholders.

Additionally, an RIC must derive a minimum of 90% of its income from capital gains, interest or dividends earned on investments. Further, an RIC must distribute a minimum of 90% of its net investment income in the form of interest, dividends or capital gains to its shareholders. Should the RIC not distribute this share of income, it may be subject to an excise tax by the IRS.

BDCs to Consider

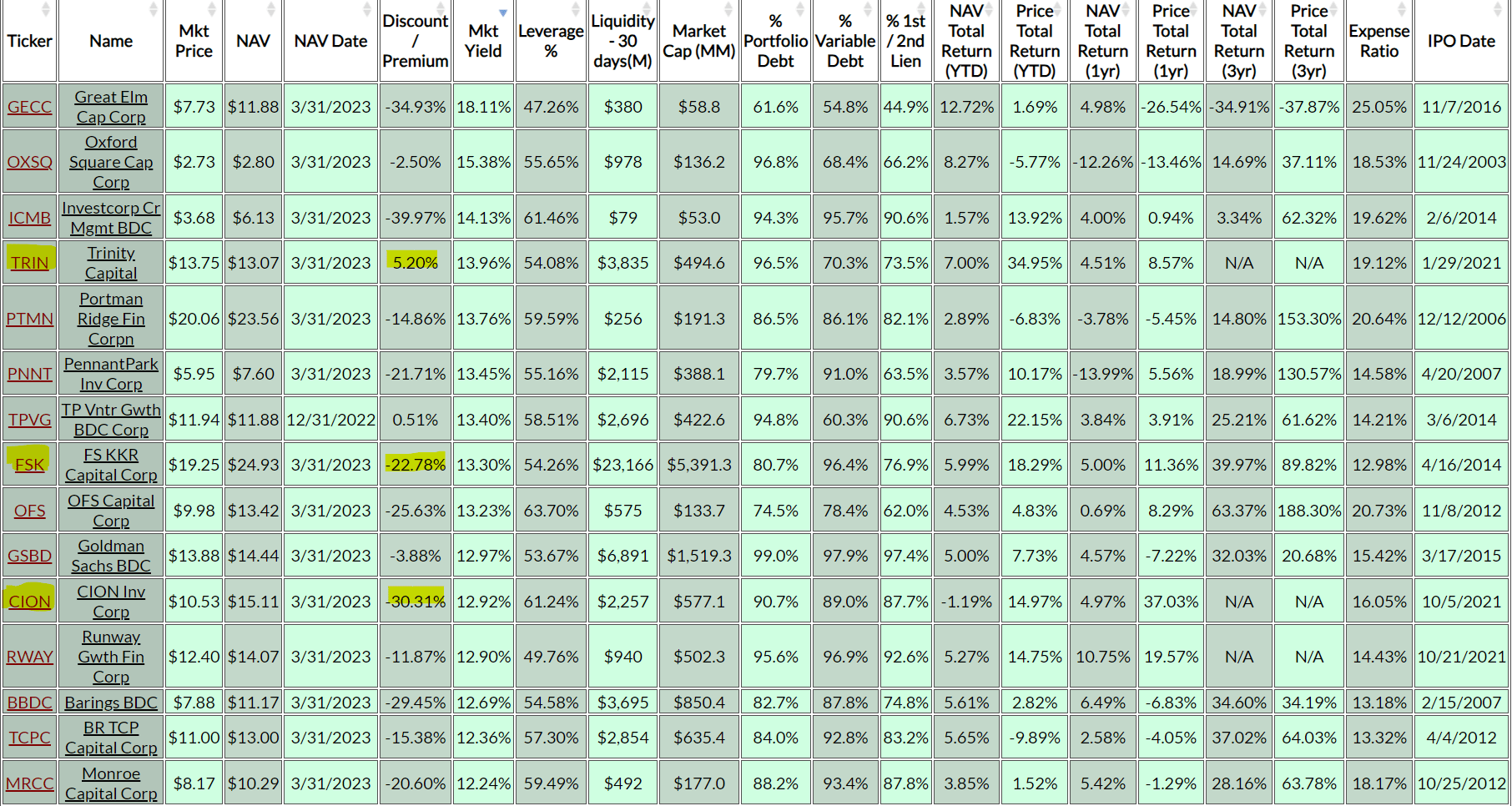

There are many publicly traded companies that are RICs classified as BDCs. As of July 3, 2023, the website CEFData.com shows a total of 48 companies in the BDC Universe that it covers. Of the 48 covered, more than a dozen of them offer current market yields in excess of 12%. I own 3 of those and will briefly discuss the 3 that I own and recommend for further research if you are so inclined.

{kind=link}

TRIN

I reviewed Trinity Capital ( TRIN ) in May, shortly after the collapse of Silicon Valley Bank where I explained how the collapse of SVB was likely to be good for BDCs like TRIN. At that time, TRIN was offering a yield exceeding 15% and had raised the dividend for 9 consecutive quarters since its IPO in 2019. Since the time that I published that article, TRIN has provided a total return over 31%. They also announced yet another dividend increase on June 15 to $0.48 per quarter plus a $0.05 supplemental payable July 14.

Seeking Alpha

FSK

Another BDC that I own and recommend for further due diligence, is FS KKR Capital (FSK). I last covered FSK in March of this year when I wrote that the BDC was trading at a substantial discount to book value and offered a yield over 16%. At that time, I made the observation that over the past 3 years FSK had outperformed its two largest peers, ARCC and ORCC based on total return. Since then, ORCC has caught up with FSK due to the dramatic price drop that occurred in March that impacted FSK more than it did ORCC. Yet FSK still trades at a much bigger discount to book value and offers a much higher yield. Currently, FSK trades at a price that is more than -22% below NAV and offers a yield of about 13% (not including specials). On May 8, the company declared a $0.70 quarterly dividend, in line with previous, but also declared special distributions of $0.15 to be paid in 3 installments. Therefore, in addition to the regular quarterly dividend, a special distribution of $0.05 will be paid each quarter in May, August, and November.

CION

Another BDC that I have covered in the past is Cion Investment Corp (CION). CION traded privately for about 10 years prior to going public in 2021 so it flies under the radar of many BDC investors. However, over the past year it has substantially outperformed other top rated BDCs including ARCC, ORCC, and MAIN.

{kind=link}

I last wrote about CION in April of this year and discussed how the regular quarterly dividend had just been raised by 10%. On May 10 they announced another quarterly dividend of $0.34, in line with previous. With a reported NII of $0.54 during the quarter that dividend is well covered, and I expect them to announce a dividend raise or special distribution later this year to distribute the excess NII.

REITs to Consider

Many REITs are also registered as RICs and thus pay out 90% of NII in the form of dividends to shareholders in order to avoid taxes on that income. With rising interest rates, many REITs have suffered over the past several years and especially in 2022 due to the rapid increase from near zero interest rates to a base rate now approaching 5% or higher. With the Fed likely to hike rates at least once more this year, the pressure on REITs that are impacted by rising rates is likely to continue at least for another few months, however, the bottom may be approaching quickly, and the trend may turn positive sooner than many expect. There are signs of improvement in the economy including the latest ADP jobs report showing nearly 500,000 jobs added to the private sector in June.

AGNC

{kind=link}

One REIT that I like at this level is a residential mortgage REIT, AGNC Investment Corp ( AGNC ) that deals with mostly agency-backed loans, such as those guaranteed by Freddie Mac and Fannie Mae. Due to the ongoing concerns regarding inflation and additional rate increases, the price of AGNC stock has been reduced to near the cheapest price since the GFC of 2008, according to a recent report from JP Morgan and is likely to find support around the $9 price in my opinion based on recent technical levels.

Meanwhile, the stock pays a monthly dividend of $0.12 that results in a yield of more than 14% at the current price. The dividend history shows that the same monthly dividend has now been paid for the past 3 years after the post-Covid dividend reduction from $0.16 that occurred in April 2020.

{kind=link}

As CEO, Peter Federico stated on the Q1 earnings call , AGNC is in one of the best positions of any buyers of agency MBS due to the Fed and bank repositioning of balance sheets after the multiple bank collapse events that occurred in March.

For much of the last 15 years, we have competed with the world's largest and most price and sensitive buyer of Agency MBS. As the Fed and now banks repositioned their balance sheets, we find ourselves in the favorable position of being one of the few permanent capital vehicles dedicated to Agency MBS at a time when valuations are historically attractive and appear poised to remain that way for some time.

Also important, unlike banks, our interest rate exposure is conservatively hedged and our portfolio is fully mark to market. As such, when you invest in AGNC today, you are buying into a levered and hedged portfolio priced at today's historically attractive valuation levels, making this opportunity very similar to 2009, which was one of AGNC's most favorable periods.

There is likely to be continued volatility in the months ahead, but I believe long-term investors who seek reliable monthly income will be richly rewarded by buying shares at these low prices while they last. And if you are concerned about the safety of the common shares, AGNC offers several preferred shares that may be of interest with potential price appreciation along with dividend income.

EFC

Another REIT that offers a high yield, monthly dividend that is on my radar as a Strong Buy opportunity at current prices is Ellington Financial (EFC). EFC is a small cap (market cap of $900M) mREIT that specializes in RMBS and commercial loans. The summary from the SA company profile offers this overview:

Ellington Financial Inc., through its subsidiary, Ellington Financial Operating Partnership LLC, acquires and manages mortgage-related, consumer-related, corporate-related, and other financial assets in the United States. The company acquires and manages residential mortgage-backed securities ((RMBS)) backed by prime jumbo, Alt-A, manufactured housing, and subprime residential mortgage loans; RMBS for which the principal and interest payments are guaranteed by the U.S. government agency or the U.S. government-sponsored entity; residential mortgage loans; commercial mortgage-backed securities; and commercial mortgage loans and other commercial real estate debt. It also provides collateralized loan obligations; mortgage-related and non-mortgage-related derivatives; corporate debt and equity securities; corporate loans; and other strategic investments. In addition, the company offers consumer loans and asset-backed securities backed by consumer and commercial assets.

{kind=link}

On June 21, EFC declared a monthly distribution of $0.15, in line with previous, that results in a current annual yield of about 13.5%. The most recent estimate of book value as of May 31 was $14.55, which means that the stock currently trades at about a 10% discount to book value. In addition, and perhaps most importantly, the company recently announced two separate acquisitions.

On May 30, EFC announced their intention to acquire another mREIT, Arlington Asset Investment ( AAIC ) in a deal that should increase the company's scale and liquidity. That acquisition is expected to add to EFC's earnings in 2023 and to its book value within a year of closing. They also expect to improve operating expense efficiency by spreading fixed expenses over a larger asset base.

Then on July 3, EFC announced a deal to acquire Great Ajax ( AJX ) for a price equal to $7.33 per share. Each AJX share will be converted to 0.5308 shares of EFC stock, resulting in about 12.5M shares of EFC stock in aggregate. That deal is also expected to increase the scale and enhanced access to securitization markets.

"We are extremely excited about the opportunity to add a significant portfolio of strategic assets, including over $1 billion of highly creditworthy first-lien residential RPL and NPL investments at attractive prices, which complement our existing investment portfolio nicely and align with our expertise and existing management platform," stated Laurence Penn, Ellington Financial's Chief Executive Officer. "We believe that the benefits of this acquisition also include greater operating efficiencies, a larger market capitalization, and a closer relationship with Gregory Funding, Great Ajax's highly respected affiliated mortgage servicer. We believe that this transaction will position us well to drive accretive earnings growth and provide strategic and financial benefits to our stockholders."

Wall Street analysts like the stock as well with 1 Strong Buy, 4 Buy, and 3 Hold ratings.

Seeking Alpha

Fixed Income CEFs Yielding 12% or More

Several CEFs (closed-end funds) that did not make the list of my 15% yielders include 3 that hold mostly fixed income investments to generate high yield income. Those three include 2 that trade at a premium to NAV and have never cut the distribution since inception. They are Guggenheim Strategic Opportunities fund ( GOF ) and Brookfield Real Assets Income fund (RA). The third CEF that I want to mention here is KKR Income Opportunities fund (KIO).

GOF

I last covered GOF in May of this year when I discussed how it trades at a consistent premium to NAV while paying a 14% distribution that has never been cut. The fund was managed for many years by Scott Minerd, who passed away suddenly from a heart attack at age 63 in December 2022. Nevertheless, the remaining fund managers have carried on the tradition of paying a steady monthly distribution of $0.1821, which was most recently declared July 4, and represents an annual yield of 13.75%.

The fund NAV appears to be stabilizing and distributions appear to be made up of mostly long-term capital gains for the last several months rather than ROC, which had investors concerned about a potential dividend cut. The fund trades at a premium of about 28% which is slightly above the 1-year average, and it does not appear that it will trade at a discount any time soon. You could wait for another market crash to initiate a new position, but that may not happen for a while given the improving US economy.

{kind=link}

RA

Another high yield fund that holds mostly fixed income and other "real assets" and trades at a premium to NAV includes RA. I last wrote about RA in February of this year. At the time, I explained that the types of assets that RA holds are good for a slow growth economy with inflationary pressures. I mentioned that the fund appears well positioned to offer defensive income holdings that yield 14% based on a monthly distribution of $0.199, most recently declared on July 3.

While the fund currently trades at a premium of about 14%, that is just slightly above the 52-week average of 11%. The fund's inception date was December 2016, and it has paid the same monthly distribution since it began, even throughout the 2020 Covid pandemic. This is the primary reason why investors are willing to pay a premium for a high yield income fund that pays a steady monthly distribution.

{kind=link}

Similar to GOF, there is a fair amount of ROC included in the distributions from RA, however, for those holding these funds in a taxable account that is another benefit to consider as ROC can reduce the cost basis of your holdings.

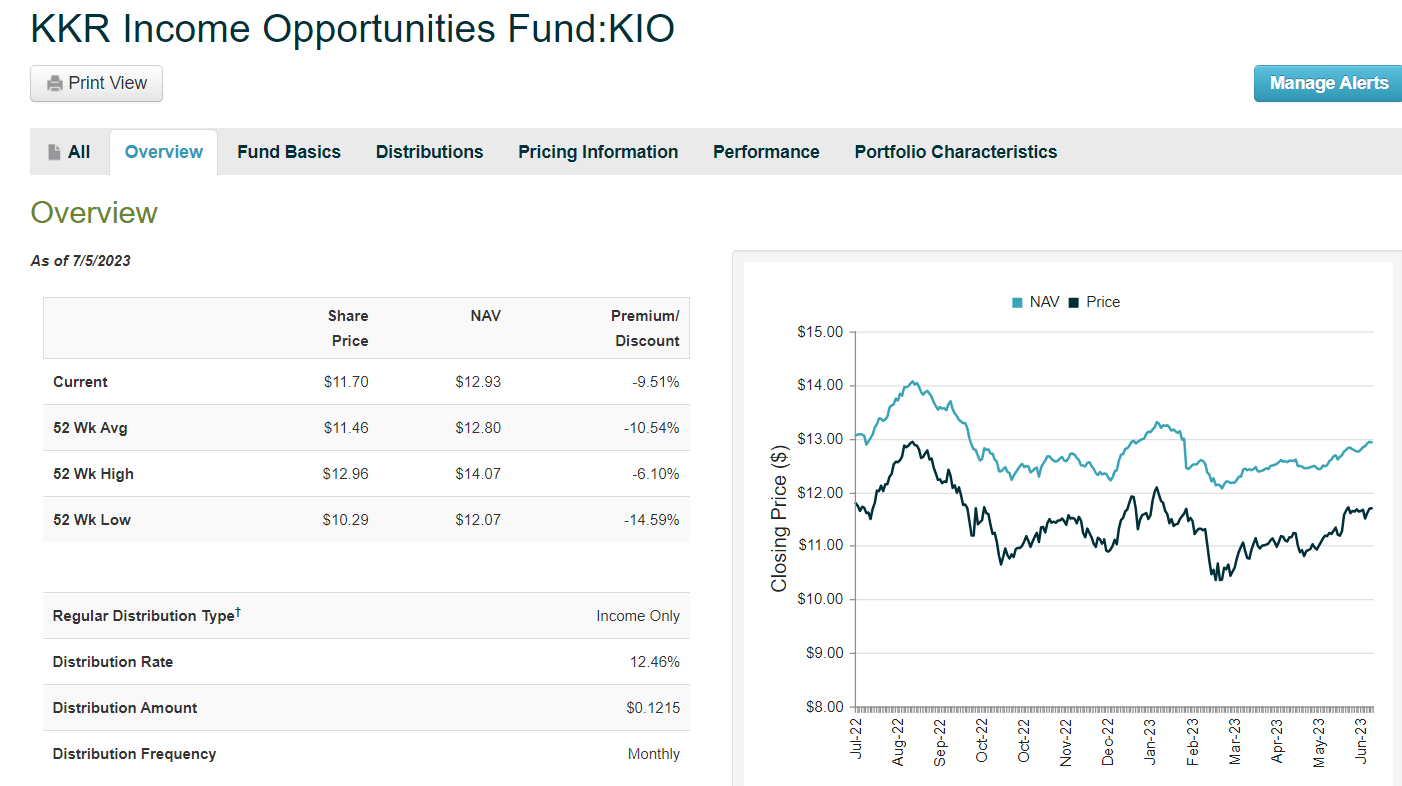

KIO

Back in January of this year I mentioned how KIO was shaping up to be a good opportunity to invest in fixed income to generate high yield income in 2023. At the time it was trading at a -11% discount to NAV and offered an annual yield of 12.5% based on a recently raised monthly distribution. Since that time, KIO completed a rights offering which reduced the NAV by issuing more shares, however, they have continued to pay the increased distribution of $0.1215 per month and declared 3 more months out on April 18 for the May, June, and July distributions. The fund currently trades at a discount of -9.5% and the annual yield at current prices is about 12.5%. The NAV has been increasing and is nearly back to its pre-RO level.

{kind=link}

Midstream Assets Benefit from Inflation

Another high yield CEF to consider is one that holds midstream energy assets such as MLPs or pipeline companies. A recent report from an analyst with Citi states that we are entering a new period of elevated capital returns from midstream companies.

The analyst said three key factors have made this excess cash flow shift possible: Shale growth has slowed and become more ratable, which in turn has moderated capital spending; midstream companies have spent the last three years de-levering and have largely achieved leverage targets, which releases capital back to equity holders; and companies are able to maintain growth rates due to brownfield expansions which are highly capital efficient.

SRV

The NXG Cushing Midstream Energy Fund ( SRV ) is one that I like a lot and wrote about twice this year - first in April when it was yielding 16%, and then again in May when I further explained how the steadily increasing cash flows from midstream companies could support the high yield distribution. When I first covered it, I rated the fund a Strong Buy and received lots of comments about the risks of such a high yield distribution from a fund that invests in companies that typically generate 7 to 8% yields. Yet the fund has strongly outperformed the S&P 500 in the past few months even as the market turned bullish in the second quarter.

Seeking Alpha

While the fund now trades at a slight premium of about 1% above NAV, the yield has declined to 14% but still offers a good opportunity for income investors to take advantage of the increasing cash flows from midstream assets.

Final 3 High Yielders to Consider

In no particular order I wanted to briefly mention 3 additional options for generating income that exceeds 12% annually based on monthly distributions. Those 3 include RYLD, XFLT, and FSCO.

RYLD

One of the Global X funds that invests in a nontraditional equity asset class that uses option strategies to generate income based on covered calls is the Global X Russell 2000 Covered Call ETF (RYLD). For a good discussion of why RYLD should perform well during a recession (that many are still predicting is coming), see this recent article .

The dividend is paid monthly but is variable based on the options premiums collected so it is difficult to state an annual yield going forward. Over the TTM period, the dividends paid have exceeded 19%. With reduced volatility in the market, that level of distribution may not be feasible going forward, although the outlook for small cap stocks outperforming in the second half of the year may help to generate strong premiums from covered calls.

{kind=link}

XFLT

Another alternative investment vehicle is the XAI Octagon Floating Rate & Alternative Income Term Trust (XFLT). Structured as a CEF, the XFLT fund offers investors a forward yield exceeding 15% after raising the monthly distribution in May from $0.073 to $0.085. Several other authors have recently covered XFLT including analysts Rida Morwa and Treading Softly, and you can read their thoughts about buying this fund at a discount here .

Although the fund currently trades at a slight premium to NAV of about 4%, the discount comes from fund managers buying leveraged loans that trade at a discount to par due to fear in the market of increasing loan defaults. That means that XFLT can generate even more income from cash flows by buying loans for less than the value at maturity, further increasing the yield generated from the payments on those loans.

FSCO

Another relatively new high yield holding for my portfolio is FS Credit Opportunities (FSCO). This fund just went public in November 2022 although it was initially formed in 2013 by Franklin Square Capital Partners. The fund uses a dynamic credit strategy investing across private and public markets. At a -25% discount to NAV the fund recently raised the dividend by more than 15% on July 3 and now yields over 14% with a $0.057 per share monthly dividend.

The fund went public using a direct listing approach (as opposed to an IPO) which involved selling a third of the shares in November, with another third offered in March, and the final third in May. The specifics of the direct listing and what it means for investors was described in this article from Alpha Gen Capital in March in which he recommended to Buy FSCO. The unlocking of the shares helped to keep the discount wide so now that all shares are publicly listed the discount is likely to start narrowing. You can see that pattern unfolding on CEFConnect with the price beginning to approach the NAV, which is also rising.

{kind=link}

I just started an initial position in FSCO and plan to watch it closely and possibly add to my position on dips when the market offers additional buying opportunities.

Baker's Dozen - Special Mention

Although I have now covered my 12 picks for income investors that offer 12% or higher yields, I cannot help myself but to suggest one more for those of you who just love to enjoy increasing income with rising interest rates. There are several floating rate funds that invest in senior loans and offer increasing dividends as interest rates continue to rise. One in particular that gets very little coverage on SA and which has raised the dividend now for the 8th time in just over a year is Pioneer Floating Rate fund (PHD).

I last covered PHD in December 2022 when I wrote about how the fund traded at a discount of -11% and was paying an annual yield of 11.5% at the time after the 5th dividend raise in 2022. Since then, the fund has raised the dividend 3 more times and now offers a forward yield exceeding 12.4% while trading at an even deeper discount of -13.3%. I feel that PHD is an undiscovered gem of an income holding that is likely to catch up to its peers in terms of price appreciation while continuing to offer delightful monthly income from senior secured floating rate loans and corporate bonds.

Have your cake and eat it too with these high yielding income picks. Despite what the broader market does, you can collect monthly income and grow your future river of cash by reinvesting and compounding your income holdings at lower prices when the market drops to generate even more cash in the future. That is the crux of my income compounder approach. Best wishes and happy investing!

For further details see:

A Dozen Income Picks Yielding 12% Or More