ETRN - A Few Things To Note If You're Contemplating A Position In Equitrans Midstream

2023-08-22 12:43:36 ET

Summary

- If the MVP comes to fruition, Equitrans Midstream's EBITDA profile could get a 20% uplift.

- ETRN's volatility quotient has ramped up in recent months, and we think this could remain a dominant theme much through this year.

- ETRN's FCF has traditionally covered the flattish dividend bill by around 2.7x, and the presence of a large chunk of stable firm reservation fees helps bring a degree of stability.

- Based on the FY23 numbers, forward valuations look pricey on an EV/EBITDA basis, but given the potential EBITDA growth over the next two years, it is less of an issue.

- Institutions are yet to turn constructive on ETRN, and we are not enthused by the current risk-reward on the standalone chart.

Introduction

Investors fishing for opportunities in the Oil & Gas storage and transportation space have around 60 odd stocks to choose from. Today we'll touch upon one of the stocks in this space - the Pennsylvania based - Equitrans Midstream (ETRN) which only made its debut on the bourses less than five years ago. At the outset, we'd like to state that we're neutral on this stock, but there are some important considerations for those who may be interested in exploring this ticker.

Important Considerations

ETRN's midstream expertise is tapped via three avenues-

- Gathering Services - This segment accounts for close to two-thirds of group revenue and involves the operation of mainly dry gas gathering systems. It's worth noting that ETRN is considered to be one of the largest natural gas gatherers in the US with over 5BcF (Billion Cubic Feet) per day of minimum volume commitments.

- Transmission Systems - This is the other large division accounting for 30% of group revenue and deals with running FERC-regulated pipelines and storage systems.

- Water Network - ETRN also manages a small water pipeline portfolio (4% of group revenue) that supports well completion and produced water handling activities.

Currently, investor interest in ETRN is mainly driven by its strong exposure to the Mountain Valley Pipeline ((MVP)) JV, where it serves as the majority owner (48.3% stake) and the operator of the 303-mile FERC-regulated pipeline. MVP is strategically positioned to transport natural gas from the rich Appalachian basin and fulfil substantial demand in the Southeast and mid-Atlantic US.

This pipeline has been in the works since 2014 and was due to come on board in 2019. But ongoing political, environmental , and litigation challenges have rumbled on for years causing delays in the construction and fruition of this project. On the Q2 call, after the Supreme Court's intervention, ETRN management implied that they were getting close to the finish line and now plan to wrap up construction work by the end of this year, provided there are no more legal or regulatory hassles.

If this comes into operation next year, one could be looking at an initial capacity of 2.0 BcF per day, backed by 20-year-long contract commitments with a variety of shippers. For Q2, management believes that MPV could potentially contribute $220m of fresh EBITDA to the group; given ETRN's group EBITDA run rate last year, you're looking at a potential EBITDA uplift of 20% from this project alone.

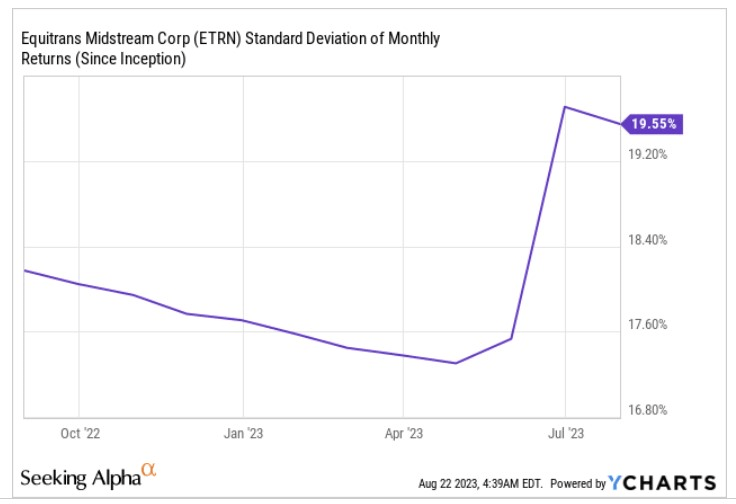

However, getting to the finish line won't be smooth sailing, as various parties continue to make attempts to thwart the project's progress. This also means that ETRN is probably not meant for the faint-hearted as it will be subject to plenty of news-driven volatility. Note that in recent months, the monthly standard deviation quotient of the stock has really ramped up compared to the historical norm.

{kind=link}

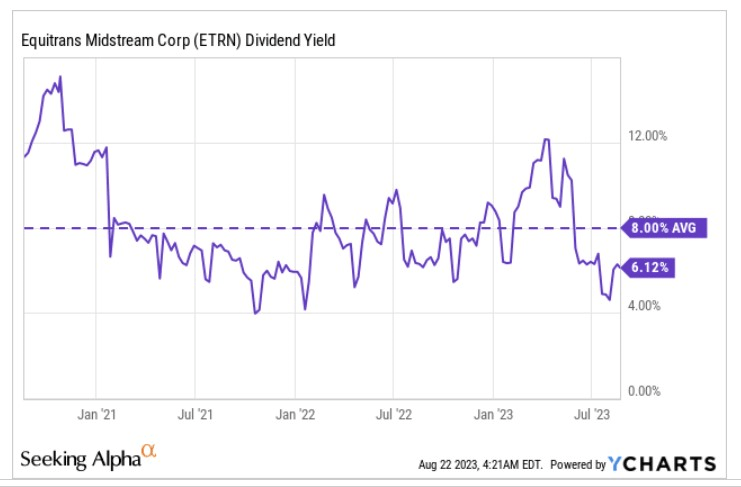

There's also the dividend angle to consider, where ETRN has been paying quarterly dividends since FY19 , although, do note that two-thirds of the usual quarterly payouts were cut in May-2020, and since then the dividend has been maintained at the $0.15 per quarter rate for multiple quarters.

When it comes to the dividend coverage, there are no major reasons to fret. A 15-cent dividend bill, equates to around $65m in quarterly cash payments; as you can see from the image below, with the exception of Q4 last year, ETRN has always managed to generate ample FCF that covers its dividends by an average of 2.7x.

Seeking Alpha

Now looking ahead to H2 and the FY, increased capital commitments primarily related to the MPV project, may likely result in a negative FCF position of -$85m-$135m , which is certainly not ideal. Having said that, over the medium-term ETRN is unlikely to face too many challenges in generating sustainable FCF as well over 70% of the company's operating revenue comes from firm reservation fee contracts which bring a degree of stability to the operating model.

Besides, a flattish dividend across long periods isn't the most eye-catching narrative, and when the stock has already more than doubled this year, the yield angle becomes even less compelling, relative to what you could historically pocket. For context, this was a stock where you could typically lock in 8% yields, now it's almost 200bps lower at a little over 6%.

{kind=link}

Closing Thoughts

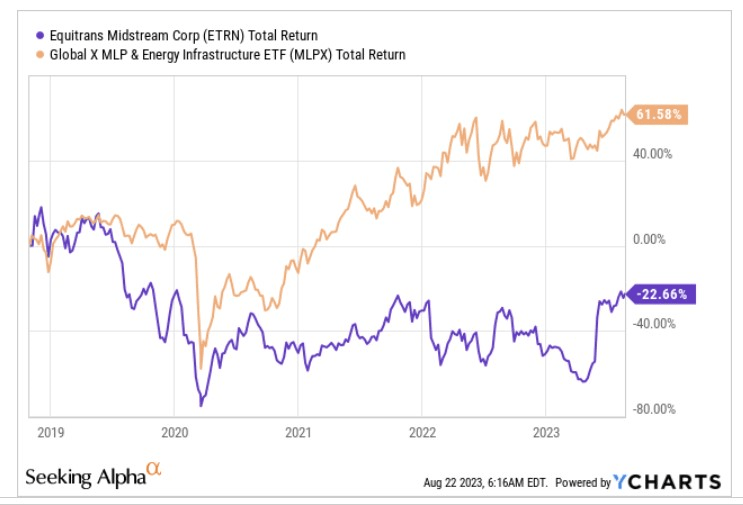

Even though the ETRN stock has enjoyed its time in the sun in 2023, delivering total returns of +56% YTD, it's worth noting that since its listing date back in Nov 2018, it has been a source of wealth erosion for investors. Meanwhile, during this same period, other midstream infrastructure offerings have delivered handsome positive returns of over 60%.

{kind=link}

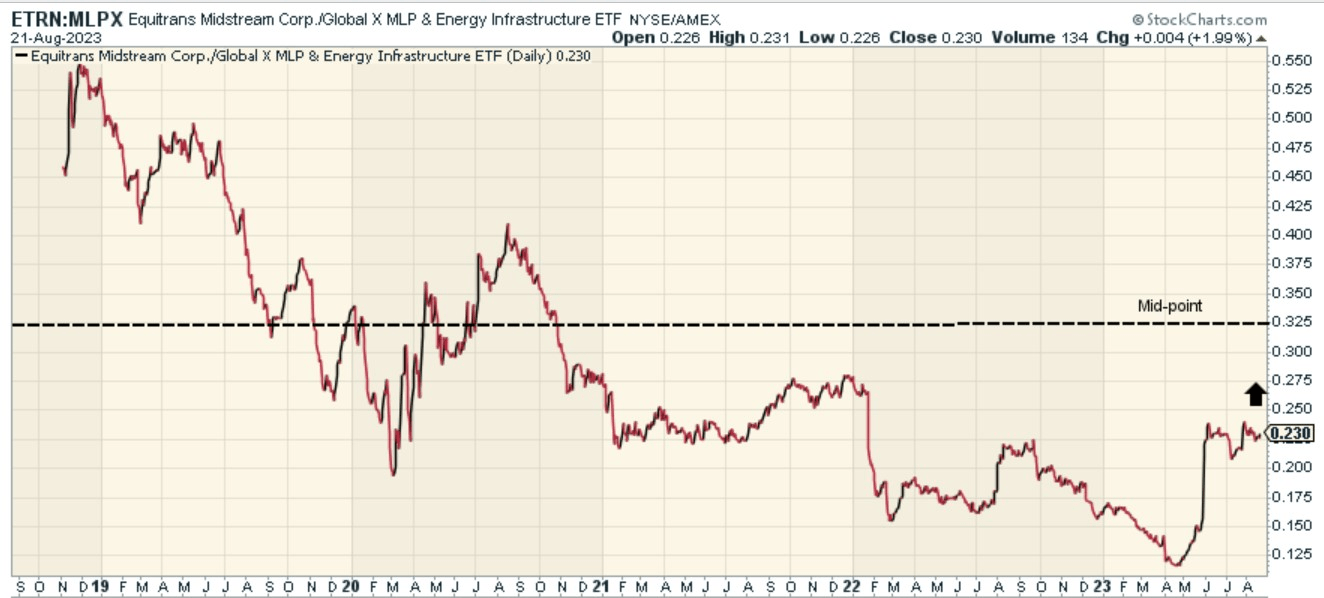

Conversely, the chronic underperformance also means that ETRN is better suited to benefit from mean-reversion momentum in the energy infrastructure space compared to most other alternatives in this space. The image below highlights how, despite a pickup from record lows seen in April this year, the relative strength ratio of ETRN over MLPX is still around 29% off the mid-point of its long-term range.

{kind=link}

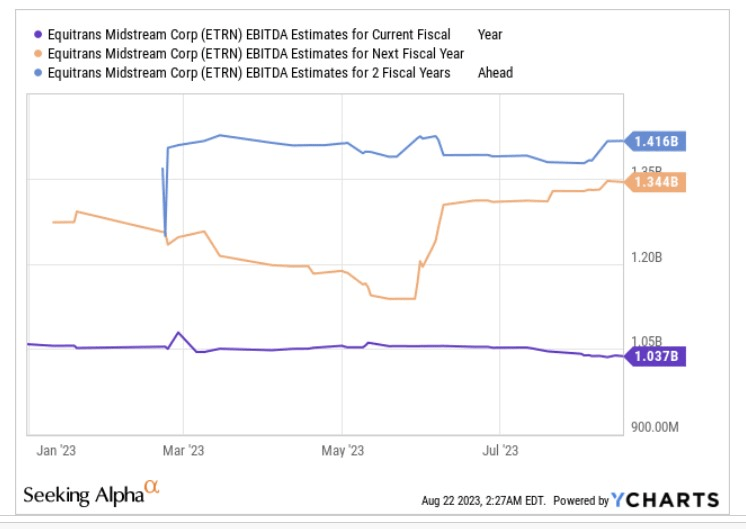

So, are ETRN's forward valuations also compelling enough to warrant some bargain-hunting interest? Well, that depends on whether you're looking at the short or medium-term. On the Q2 call management guided to relatively flat basin volumes for the rest of this year, and so the adjusted EBITDA level that you could likely get by the end of FY23 would be rather unremarkable when you consider ETRN's current EV (Enterprise Value). To be more specific, management guided to an expected FY23 EBITDA range of $1bn-$1.05bn, and consensus is already closer to the higher end of that range at $1.037bn (implying a 3% YoY decline).

{kind=link}

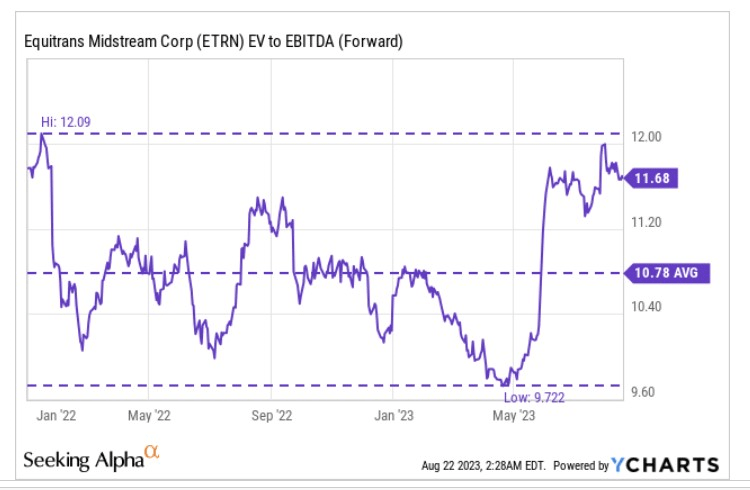

All in all, at 11.7x forward EV/EBITDA, the stock would be trading a lot closer to the peak end of the long-term EV/EBITDA trading range of 9.7-12.1, and also around 8% more than the long-term average which doesn't make it particularly cheap to own.

{kind=link}

However, assuming MVP construction gets wrapped up by year-end and the contractual obligations kick-off from the new year, then that would provide a useful fillip to the company's overall EBITDA growth over the next two years. Consensus currently believes ETRN could generate $1.34bn and $1.42bn of EBITDA over the next two years, representing impressive CAGR growth of 17% over two years. Also, at the FY25 EBITDA runrate, ETRN would be priced at only 8.55x, a lot lower than the trough multiple of 9.72x.

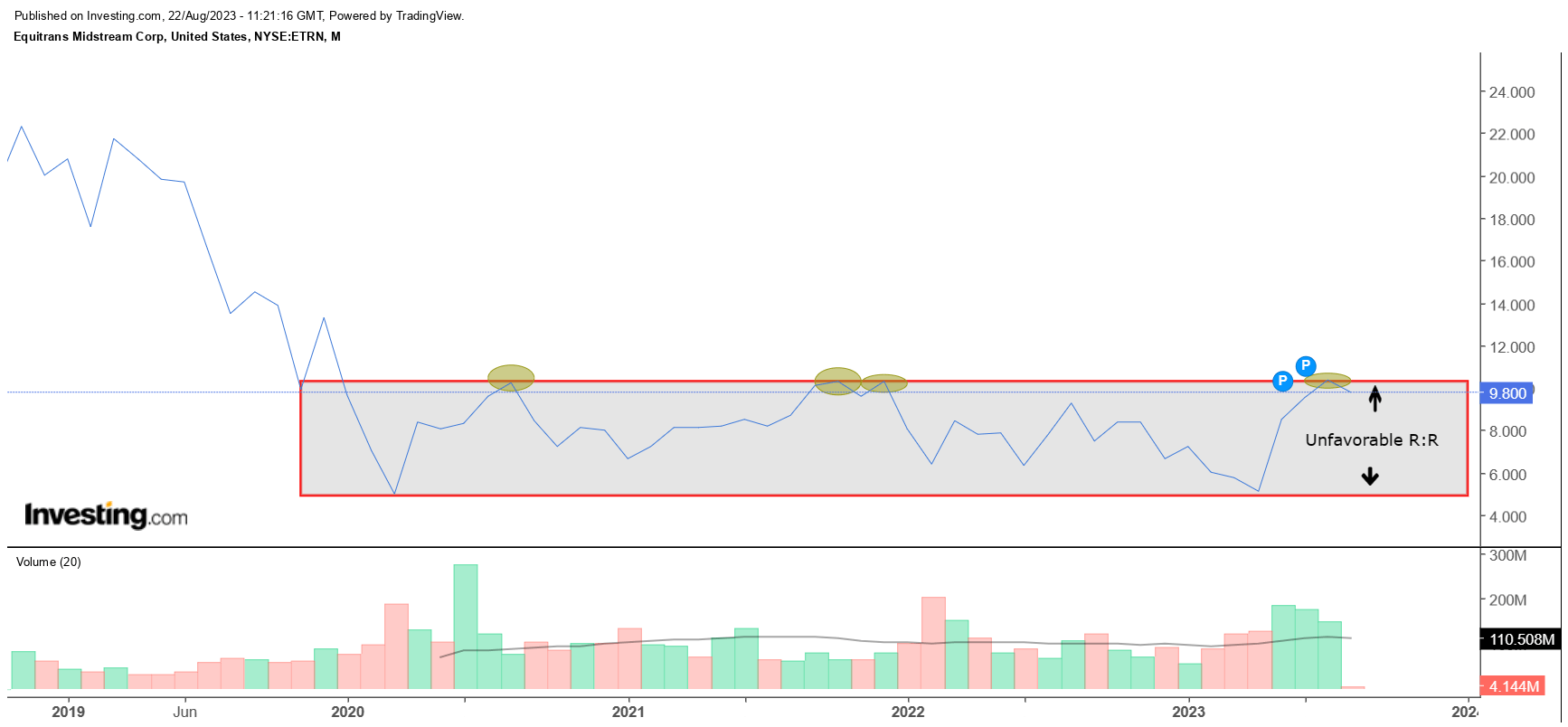

Then, a cursory glance at ETRN's weekly chart will tell you that the risk-reward at the current juncture isn't too ideal. Basically, since 2020, the stock has been chopping along within the range of $3.75-$11.66 and whenever it gets close to these terrains there appears to be a pivot of sorts. Over the last three and a half years, we've seen four separate instances where additional supply tends to come in at around the upper boundary of the range, preventing a breakout.

{kind=link}

At some stage, one may well see a breakout from this range, but we just think that given the pattern of failures at these levels, it would be more prudent to risk capital at this stage and rather pursue this play at the lower end of the range, where the risk-reward is more favorable.

{kind=link}

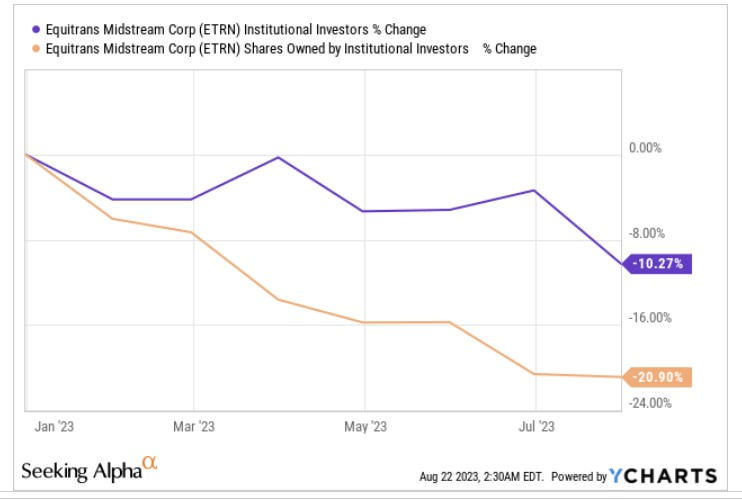

We also think that there's something to be taken from the implication that the institutional cohort hasn't really participated in this year's rally so far. In fact, on a YTD basis, the number of institutions holding the ETRN stock is down by 10%, and the shares owned by them is down by twice as much. Do you want to bet on ETRN when smart money is against it? Your call.

For further details see:

A Few Things To Note If You're Contemplating A Position In Equitrans Midstream