MPW - A Fleeting Opportunity To Upgrade Your Dividend Portfolio Quality

2023-11-04 08:45:00 ET

Summary

- Dividend investors have a chance to upgrade their portfolios with high-quality dividend growth stocks at bargain prices.

- The recent drop in long-term interest rates and rebounding of high-quality dividend growth stocks mean that this buying opportunity may be fleeting.

- I explain my "quality at a reasonable price" strategy and provide examples of both a low-quality stock I sold this year and several high-quality dividend stocks I recently bought.

The market has given dividend investors a fantastic opportunity to upgrade the quality of their portfolios.

Many high-quality dividend growth stocks that rarely ever go on discount are on offer today at what I consider bargain prices, but this opportunity may very well be fleeting.

After the Fed's continued pause (and expectations for that pause to stick this time), as well as Friday's softer-than-expected jobs report, long-term interest rates are dropping like a rock and high-quality dividend growth stocks are rebounding sharply.

Take, for example, the Schwab U.S. Dividend Equity ET ( SCHD ) and the WisdomTree U.S. Quality Dividend Growth ETF ( DGRW ), both of which explicitly utilize quality metrics in their stock-picking methodologies, which have surged over 5% each in the last several trading days:

Admittedly, the low- to middling-quality companies are discounted, too.

But in my view, going as high up the quality ladder as I can go while still paying reasonable prices is what best accomplishes my ultimate financial goal of generating a steadily compounding passive income stream with as few interruptions or setbacks as possible.

My investment strategy, put simply, goes like this:

- Buy high-quality companies

- that pay a growing dividend

- at a discount to fair value (and thus an attractive dividend yield )

- and wait patiently as they compound over time .

I try not to reach for yield.

I try to buy and hold and not to overtrade.

And I try to thoroughly understand what I'm invested in so as to distinguish between high-quality and low-quality.

In what follows, I want to give my personal definition of a quality business. Then I'll answer the inevitable questions: "Why buy now?" "Isn't it still too early?" "Or is it too late?" Finally, I'll give some examples of high-quality dividend stocks I bought recently on the dip.

What Is "Quality?"

I like to throw around the word "quality," and it's a word that sounds really nice. But what exactly does "quality" mean when it comes to investing?

Here are what I view to be some of the most important characteristics of a high-quality company :

- Provides essential goods and/or services to its customers

- Tangible and/or intangible competitive advantages

- Pricing power and unit volume growth (or for REITs: rent growth and portfolio expansion)

- Strong market positioning in a secular growth trend

- High and sustained returns on invested capital (well in excess of cost of capital)

- A strong balance sheet that remains resilient across the full economic cycle

- A skilled and shareholder-aligned management with a solid track record

- A safe and growing dividend

To modify Warren Buffett's phase, my desire is to own "wonderful dividend growth companies purchased at fair prices rather than fair dividend growth companies purchased at wonderful prices."

I've realized this year that I'm not a value investor. I'm a quality investor.

That sounds a bit pretentious, so let me quickly add that value and quality investing are both legitimate strategies that can work well. But a quality-minded investor likely won't thrive at or enjoy value investing, and a value-minded investor likely won't thrive at or enjoy quality investing.

And, of course, value investing doesn't necessarily mean ignoring quality, nor does quality investing mean ignoring value.

I'd label my strategy "quality at a reasonable price" ("QARP"). And that QARP strategy is in service to the larger strategy of dividend growth investing ("DGI").

At the beginning of 2023, I owned a few dividend stocks that I gradually realized were lower in quality.

The most notable example was Medical Properties Trust ( MPW ), a BB-rated REIT that owns hospitals mostly purchased from and leased to private equity-backed operators. MPW began 2023 with net debt to EBITDA well over 7x, having gorged on low-cost debt during the decade of low interest rates from 2012-2022.

Meanwhile, COVID-19 took an already shaky situation for MPW's generally weaker tenant-operators and made it much worse, exacerbating the hospital labor shortage and pushing increasingly more procedures to outpatient facilities.

And now, MPW's plan to deal with huge upcoming debt maturities is to sell billions of dollars worth of real estate in the coming years to deleverage. Higher interest rates seems to have destroyed MPW's business model.

Thus, the REIT fails on one of the quality points cited above:

- A strong balance sheet that remains resilient across the full economic cycle

Every economic cycle has a period of higher interest rates. If a company's balance sheet works great in a period of low interest rates but terrible in a period of high interest rates, then it doesn't have a strong balance sheet.

Risk must always be assessed in terms of cycles , not by looking at the present situation only.

Fortunately, I realized that MPW didn't qualify as "quality" by my definition early in the year, and I sold it at over $13 -- a big loss that could have been much bigger, including a dividend cut, if I'd held on.

I think MPW's growth model is broken at this point and could only work again if interest rates return to very low levels.

Lesson learned. In the future, whether interest rates are high or low, I want to own quality businesses with financial management practices that work in any monetary environment.

Why Buy Now?

The pushback I've received on every article pitching dividend stocks and/or REITs as good buys in recent months has been more or less the same: "It's too soon. The Fed is still raising rates. Wait for the recession. Wait for the Fed to cut." In other words, " wait for some 'all-clear' signal ."

I don't believe the next bull market in dividend stocks will begin with an "all-clear" klaxon sounding off. Nobody is going to ring the bells in the town chapel to let us all know it's safe to come out of hiding. It's not going to be announced by Jay Powell on CNBC as he reads from a script in a practiced monotone voice, glasses perched on the tip of his nose.

The new bull market in dividend stocks may have just begun.

Here's my line of reasoning:

- Most dividend stocks have sold off primarily because interest rates have gone up.

- Interest rates have gone up primarily because of the Fed's monetary tightening actions.

- The Fed has tightened monetary policy because of their view that the economy is too strong and inflation is too high.

- But recently, the economy has weakened and inflation fallen by a sufficient amount to cause the Fed to pause rate hikes, probably permanently.

- The economy will continue to weaken, likely into a recession, and inflation will likely continue falling until the CPI and core PCE rates blow right through the Fed's 2% target, probably sometime in 2024.

- The Fed will probably begin to cut the Fed Funds Rate sometime in the first half of 2024.

- The market's pricing in of near-future rate cuts is causing dividend stocks to rise.

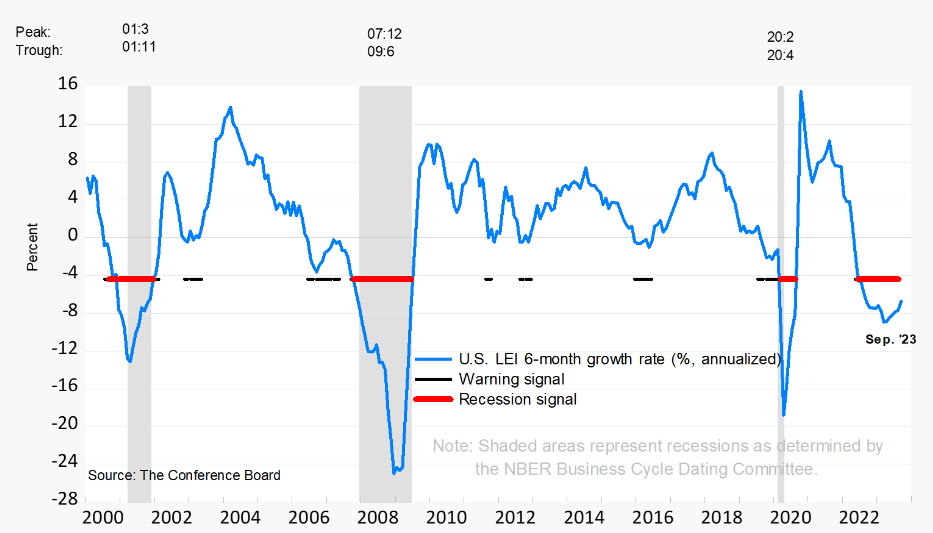

On the point about economic weakening likely leading to a coming recession, simply look at the leading economic indicators, which have been negative for over a year now:

{kind=link}

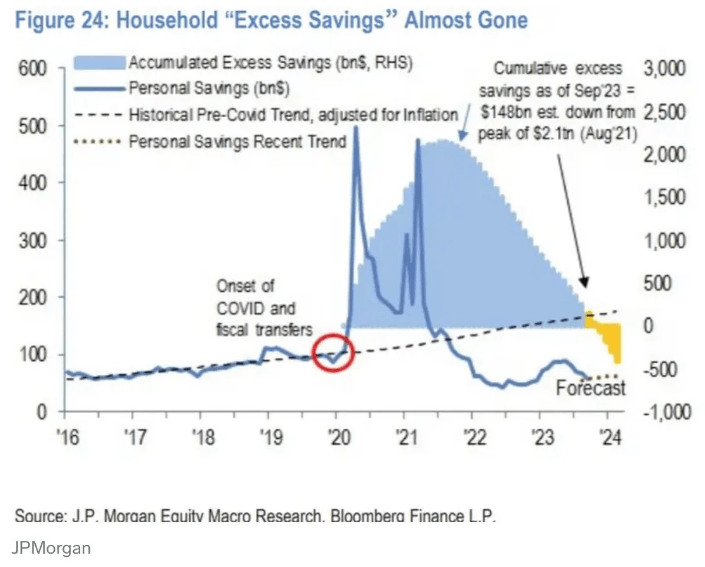

Negative LEIs have historically been a very accurate predictor of recessions. Usually, it doesn't take this long for recessions to show up after the LEIs turn negative, but there has been a critical factor making this time different: excess savings built up during the pandemic.

During COVID-19, unprecedented levels of fiscal stimulus and helicopter money led to a massive buildup of household savings, which then proceeded to fuel an economic expansion and inflationary surge from 2021 through the first half of 2023.

{kind=link}

As of September, those excess savings had been drawn down to 7% of their peak level. At the average monthly drawdown rate of $78 billion, JP Morgan's data presented above shows that 100% of pandemic-era excess savings should be depleted by sometime this month (November 2023).

Combine this with falling wage growth, soaring interest costs on personal debt, and the fact that the percentage of Americans living paycheck to paycheck is slowly growing into the 60% territory, and it looks doubtful to me that economic growth and/or inflation is going to be revived anytime soon.

Recession looks more likely than growth resurgence.

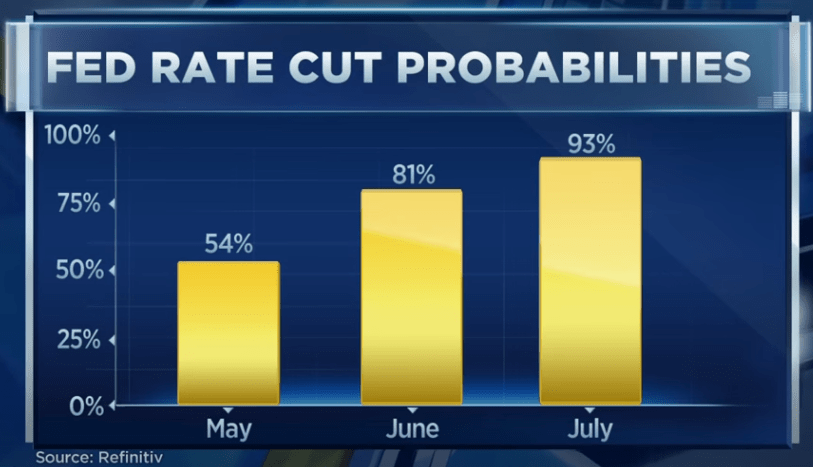

Hence the rising Fed rate cut probabilities being priced into futures markets for the first half of 2024:

{kind=link}

Over 50% probability of a Fed rate cut by May 2024 seems about right to me, given the weakening economic data.

And what should we expect from dividend stocks in the 6 months following the beginning of rate cuts? Historically speaking, we should expect about a 2.5 percentage point outperformance over the market.

Goldman Sachs

(Note that this chart refers to Dividend Aristocrats, which are the generally high-quality stocks that have raised their dividends for at least 25 consecutive years, but dividend stocks more broadly will likely follow the same pattern.)

But it potentially gets even better than that.

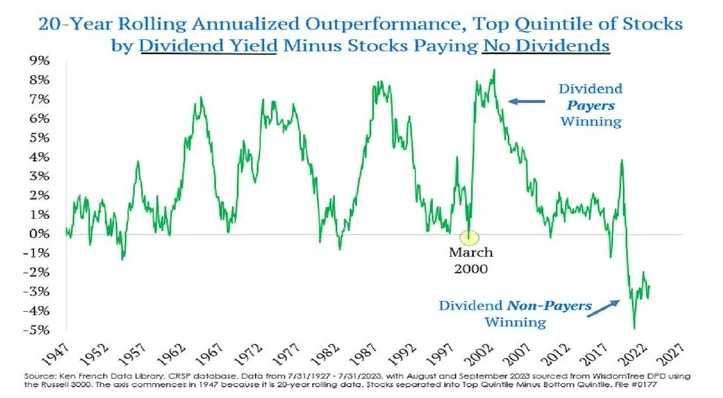

On a 20-year rolling basis, high dividend yielding stocks are near their greatest level of underperformance against non-dividend payers going all the way back to the 1940s.

{kind=link}

If this trend reverses and the market's appreciation of dividends increases going forward (which strikes me as likely, given aging demographics and the need for supplemental retirement income), then dividend stocks could be in for a sustained period of outperformance.

Let's go back to the original question: why buy now?

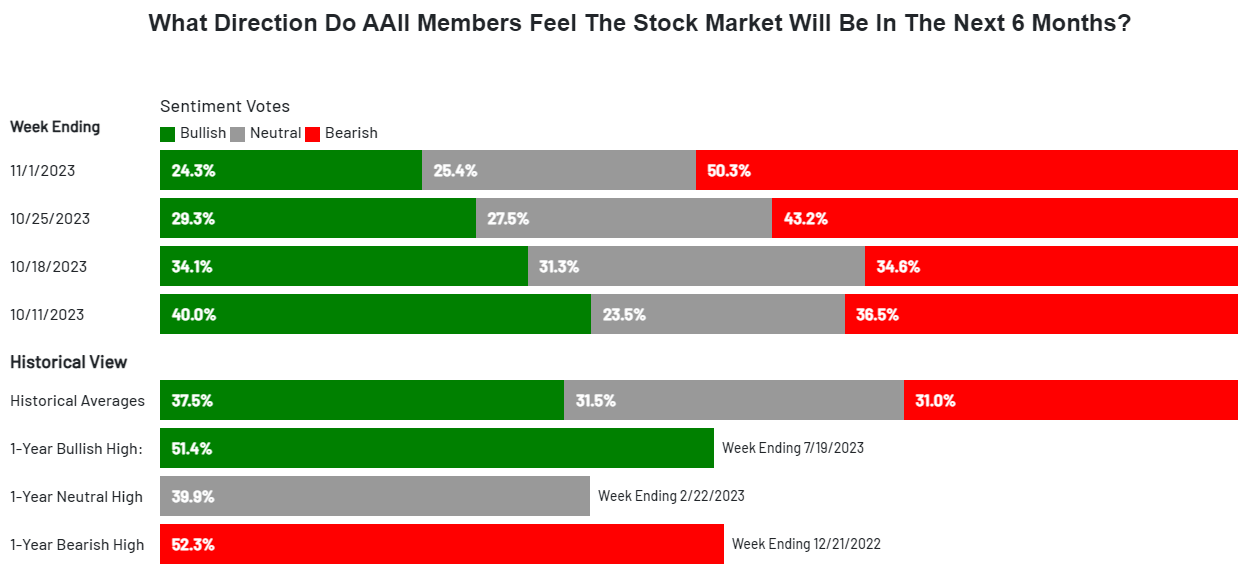

To be honest, the better time to buy was last week. Investor sentiment as measured by the AAII Investor Sentiment Survey was dropping like a rock.

{kind=link}

Though I wouldn't extrapolate this into a hard and fast rule, it generally seems like a good idea to buy when the investor community is mostly bearish.

As I wrote in last weekend's missive, titled " Use This Bear Market As A Passive Income Accelerator ":

The current bear market is a dream come true for any dividend investor still in the accumulation phase of their journey, and also for those retirees who are able to reinvest a portion of their passive income.

The reason for this is that the discounts to fair value for many stocks have grown way bigger, and thus their dividend yields have risen to much more attractive levels.

Since dividend stocks have rebounded from last week's levels, their yields are lower and their discounts to fair value have been reduced.

That said, if the above narrative proves accurate -- if we do see a mild recession soon, which causes interest rates (including the Fed Funds Rate) to drop, which lowers the cost of debt for and increases the income appeal of dividend stocks -- then this may be just the beginning of a new, sustained bull market in dividend stocks.

I'm glad I put every available dollar to work in dividend stocks in October. As I wrote in mid-October in " Buy REITs Before Everyone Else Does ":

I would argue that income-oriented investors and dividend growth investors have a rare opportunity right now to buy ahead of the crowd.

Sure enough, just as soon as interest rates and interest rate expectations began declining, the crowd began piling back into dividend stocks.

High-Quality Dividend Stocks I'm Buying

In addition to buying more shares of SCHD and DGRW recently, I also opened new positions in three high-quality dividend stocks.

Ingredion ( INGR )

As the name implies, INGR sells processed ingredients like starches, sweeteners, and proteins to food producers. I really like INGR's strong market positioning in specialty ingredients like stevia, a naturally calorie-free sweetener that doesn't come with the issues of other artificial sweeteners like Aspartame or Sucralose, as well as pea protein, which is showing up in more and more packaged food items as well as vegan products.

INGR has very low debt, a 24-year record of no dividend cuts (and 12 consecutive years of dividend increases), and a disciplined, focused management team.

You can buy INGR today at a 3.25% yield and an 11x P/E ratio, which is below its 5-year average of 13x.

Chevron ( CVX )

CVX is the best of the best among the integrated energy supermajors, in my opinion. I love the Hess acquisition, and the selloff following Q3 earnings results was a great time to buy back in at a 4%+ dividend yield.

CVX was already a free cash flow gusher, and the Hess acquisition is only expected to increase its FCF going forward. This FCF will be the fuel for future dividend increases and share buybacks, which positions CVX well to continue its 35-year dividend growth record. By the way, CVX boasts an enviable record of 111 years of paying a dividend with zero cuts.

This high-quality company is built like a battleship, and its P/E ratio of ~10x is below its 5-year average of 13x.

Diageo ( DEO )

This perpetually expensive but ultra-high quality alcohol producer sorta-kinda went on sale recently. It's currently offered at a 19x P/E ratio, compared to its historically average 23x, and its dividend yield of 2.5% is higher than its 5-year average of 2.1%.

Warren Buffett bought DEO in Q1 2023 in the $170s. I bought in the low $150s. That makes me feel good, but I only own a very small position so far.

DEO may not be the fastest grower, but it's a reliable grower with a 25-year dividend growth streak.

Everything about this company strikes me as being high-quality and long-term-oriented. Consider, for example, the moat around its highly trusted brands and the natural scarcity around assets that require aging for many years, sometimes decades.

DEO has a strong balance sheet, ample pricing power, growing market share, and recession resistance.

Bottom Line

The market is giving us an opportunity to upgrade our portfolio quality with rare discounts in top-tier dividend stocks. I would surmise that this buying opportunity won't last much longer.

If there are high-quality companies on your watchlist that you've wanted to own for a long time but never gotten the chance to buy at an attractive price, I'd suggest taking a look at that watchlist.

For further details see:

A Fleeting Opportunity To Upgrade Your Dividend Portfolio Quality