GNRC - A Fragile Grid And Mega-Trends - Generac Is A Buy

2023-09-11 11:59:27 ET

Summary

- Generac Holdings is a company benefiting from mega-trends including the evolution of the energy grid and the impact of climate change.

- The aging infrastructure of the American energy grid is under stress due to the rapid transition to renewables, creating opportunities for Generac.

- Despite short-term challenges, Generac remains attractively valued and has the potential for significant long-term growth.

Introduction

In this article, I want to take a detour. After an almost countless number of dividend and macro-related articles, we'll discuss a fascinating company benefiting from a very troublesome trend.

That company is Generac Holdings ( GNRC ) . Headquartered in the beautiful state of Wisconsin, the company is a prominent energy technology solutions player specializing in backup and primary power generation systems for residential and commercial/industrial (C&I) applications.

| USD in Million | 2021 | Weight | 2022 | Weight |

|---|---|---|---|---|

| Residential Products | ||||

| 2,457 | ||||

| 65.7 % | ||||

| 2,912 | ||||

| 63.8 % | ||||

| Commercial & Industrial Products | ||||

| 999 | ||||

| 26.7 % | ||||

| 1,261 | ||||

| 27.6 % | ||||

| Other | ||||

| 281 | ||||

| 7.5 % | ||||

| 392 | ||||

| 8.6 % |

The company also offers solar and battery storage solutions, smart home energy management devices, advanced power grid software platforms, and engine- and battery-powered tools and equipment.

In recent years, Generac has evolved its business model by investing in growing markets like residential clean energy storage, solar module-level power electronics, and energy monitoring & management devices.

These distributed energy resources can be integrated into virtual power plants within grid services programs.

{kind=link}

Generac Holdings

Before this introduction gets too long, the reason I put GNRC on my watchlist is that it not only benefits from a number of mega-trends , but it also benefits from increasing stress on the American energy grid, which could provide catalysts capable of pushing this undervalued stock much higher.

So, without further ado, let's get to it!

Mega-Trends (Including One That Worries Me)

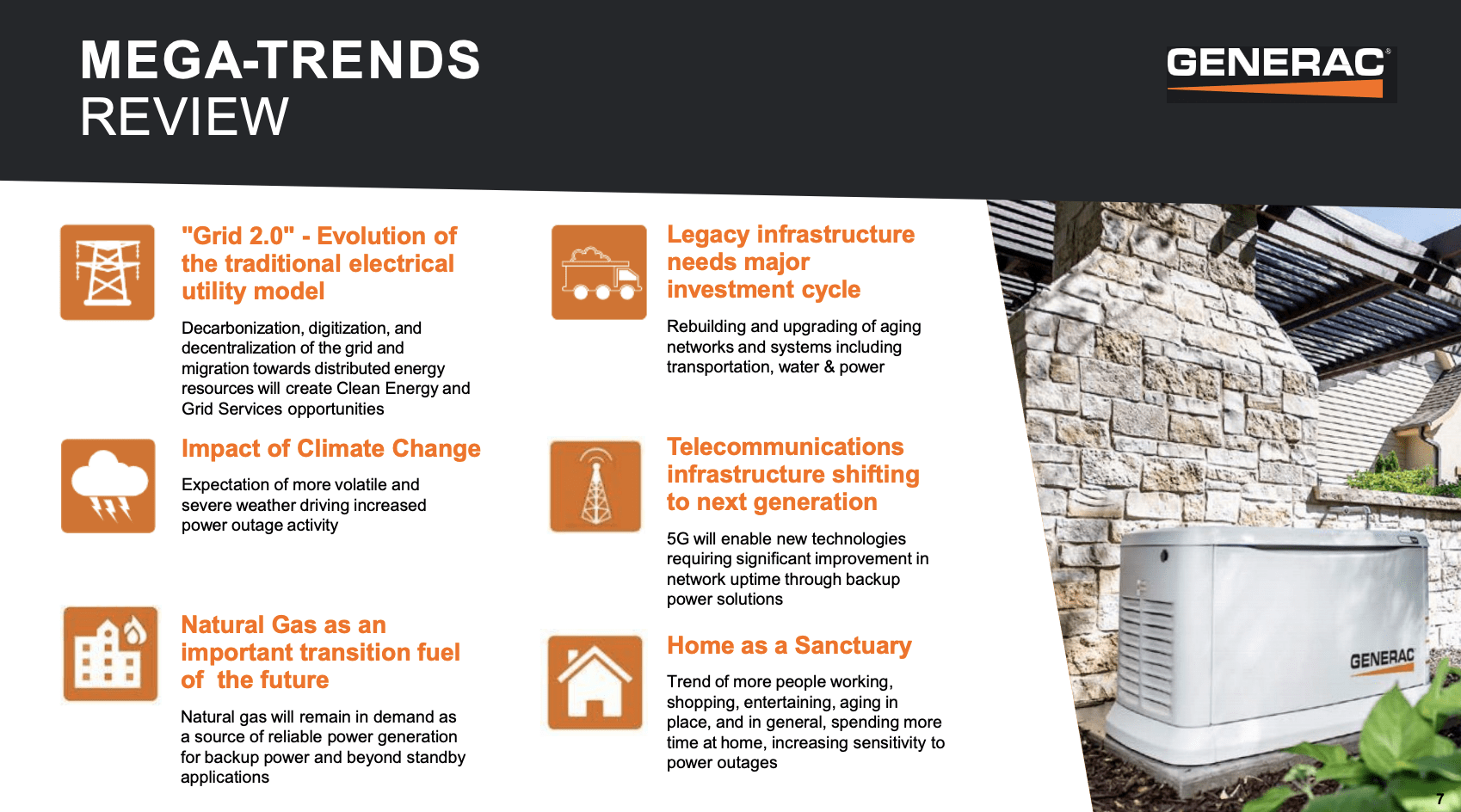

Generac believes it benefits from a number of long-term tailwinds. It calls these tailwinds mega-trends.

{kind=link}

Generac Holdings

- Grid 2.0: This trend reflects the evolution of the traditional electrical utility model towards decentralized, digitized, and decarbonized grids. It results from the increasing adoption of renewable energy and the electrification of various aspects of society's energy consumption, driving demand for clean energy and grid services solutions.

- Impact of Climate Change: More volatile and severe weather patterns are expected to lead to increased power outages, while global regulations accelerate investments in renewables.

- Transition Fuel: Natural gas remains in demand as a cleaner, reliable power generation source, especially for backup power and applications beyond standby use, compared to diesel fuel.

- Legacy Infrastructure Investment: Aging and underinvested infrastructure networks require substantial rebuilding and upgrading, spanning transportation, water, and power systems.

- Next-Generation Telecommunications Infrastructure: The shift to 5G architecture comes with the need for backup power solutions to enhance network uptime, supporting new technologies.

- Home as a Sanctuary: Growing trends of working, shopping, and spending more time at home, combined with the electrification of daily life, have increased awareness of the need for backup power due to power outages' impact on productivity and functionality.

While personal views may differ, I believe that all of these mega-trends are standing on fertile ground.

However, one of these trends is more important than the others: legacy infrastructure investment.

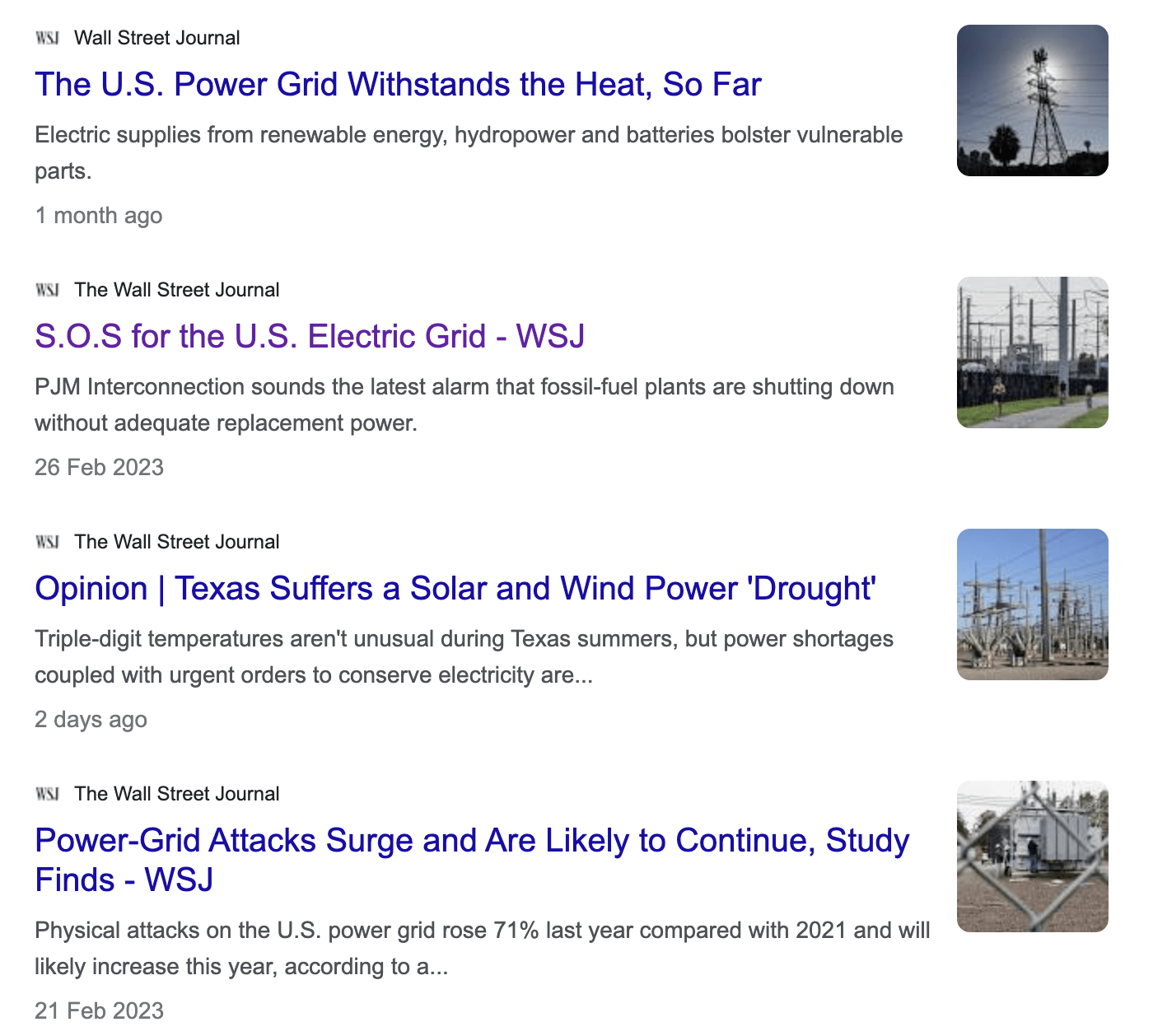

Below are some Wall Street Journal headlines from this year that support the company's case.

{kind=link}

Google News

In February, the Wall Street Journal wrote that the U.S. electric grid is facing significant challenges due to the rapid transition to renewable energy sources.

It highlighted a report from PJM Interconnection, one of the nation's largest grid operators, which raises concerns about the stability of the grid as fossil-fuel power plants retire faster than renewable sources are developed, potentially leading to energy shortages and blackouts.

PJM traditionally maintains a surplus of power thanks to its extensive fossil-fuel fleet, which it shares with neighboring grids. However, PJM anticipates a significant reduction in its power reserves as coal and natural gas plants retire.

The report estimated that 40,000 megawatts of power generation, equivalent to powering 30 million households, are at risk of retiring by 2030, accounting for about 21% of PJM's current generation capacity.

Furthermore, the report underscored the increasing demand for electric power, driven by data center growth and government initiatives to electrify vehicles and heating.

Unfortunately, renewables cannot consistently provide power 24/7, which raises concerns about the reliability of the grid as coal and gas plants are phased out.

ScottMadden Management Consultants

This is what the Bear Traps Report wrote in a bullish report on the company:

The rising rate of power outages has motivated more households and businesses to acquire generators as a backup for power. Businesses cannot afford to be out of power for any time, let alone multiple weeks, as has occurred on the East Coast during some of the hurricanes, and California. Many households also do not want to be without power for more than a few minutes.

I agree with this, which is the reason I'm writing this article.

I'm not predicting a full-blown implosion of the grid. However, I do expect an increasing number of power outages, forcing people to be better prepared.

ScottMadden Management Consultants

I also expect the company's other mega-trends to provide long-term demand growth.

Hence, and in light of these benefits, it helps that GNRC shares are attractively valued. We're not buying into a high-flying startup here but a proven giant in the industry.

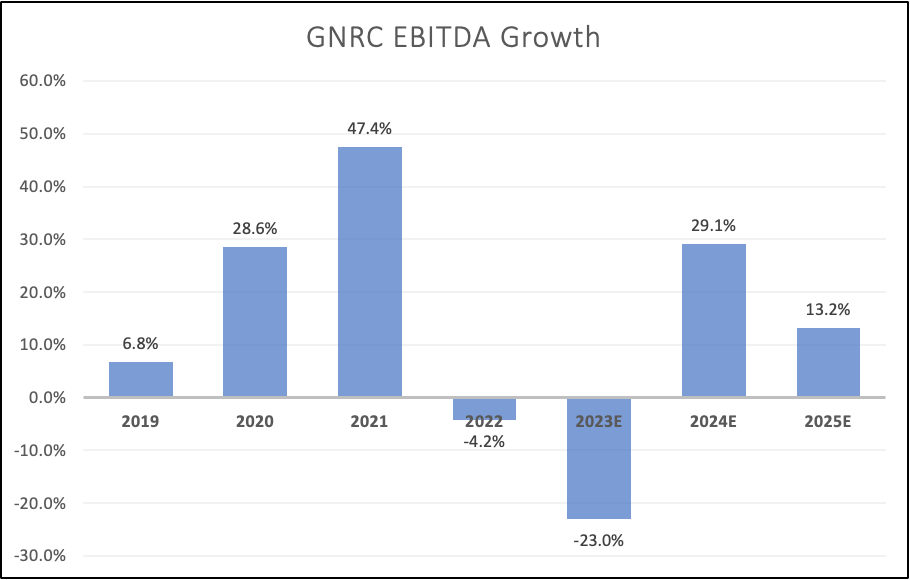

2023 Is Tough, But The Trend Is Up

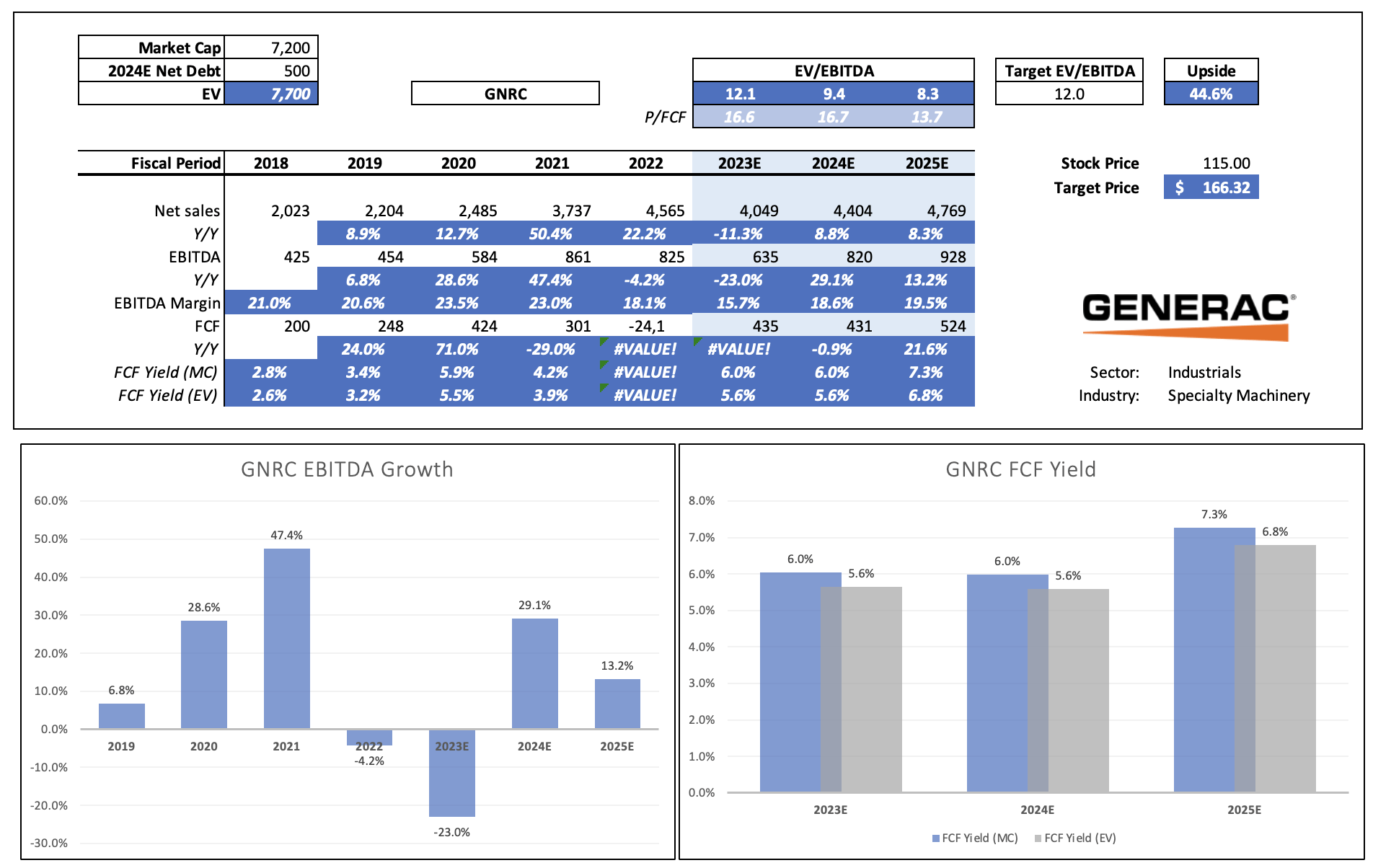

After accelerating annual EBITDA growth rates between 2019 and 2021, the company isn't doing so well right now. EBITDA declined by 4.2% in 2022, and analysts expect the company to see a 23% EBITDA decline in 2023.

{kind=link}

Leo Nelissen (Based on analyst estimates)

In the second quarter, the company reported that residential product sales dropped by 44% compared to the previous year, mainly because the prior year had benefited from significant backlog reduction for home standby generators.

Field inventory for home standby generators remained high, and clean energy product shipments also declined year-over-year. Despite a strong sequential growth in home standby shipments, year-over-year numbers were significantly down. The field inventory normalization process is expected to extend further into the second half of this year.

Furthermore, the good news is that consumer interest in home standby generators remained strong, with home consultations and sales leads maintaining levels significantly higher than in 2019.

The number of residential dealers also grew, reaching approximately 8,700, an increase of 500 dealers from the previous year. The company is focused on expanding installation capacity and increasing dealer count while streamlining the installation process and raising category awareness.

The good news continues, as global C&I product sales grew by 24% year-over-year. This makes it an all-time quarterly record.

Domestic C&I product sales were strong, including shipments to key customers for applications beyond traditional emergency standby projects and industrial distributors.

Unfortunately, the company's overall sales decreased, resulting in a lower adjusted EBITDA before deducting non-controlling interest. The adjusted EBITDA was $137 million, which accounts for 13.6% of net sales.

This is a notable decline from 2022's adjusted EBITDA of $271 million, which represented 21% of net sales. The decrease in EBITDA margin was primarily caused by higher operating expenses as a percentage of sales and lower gross margins.

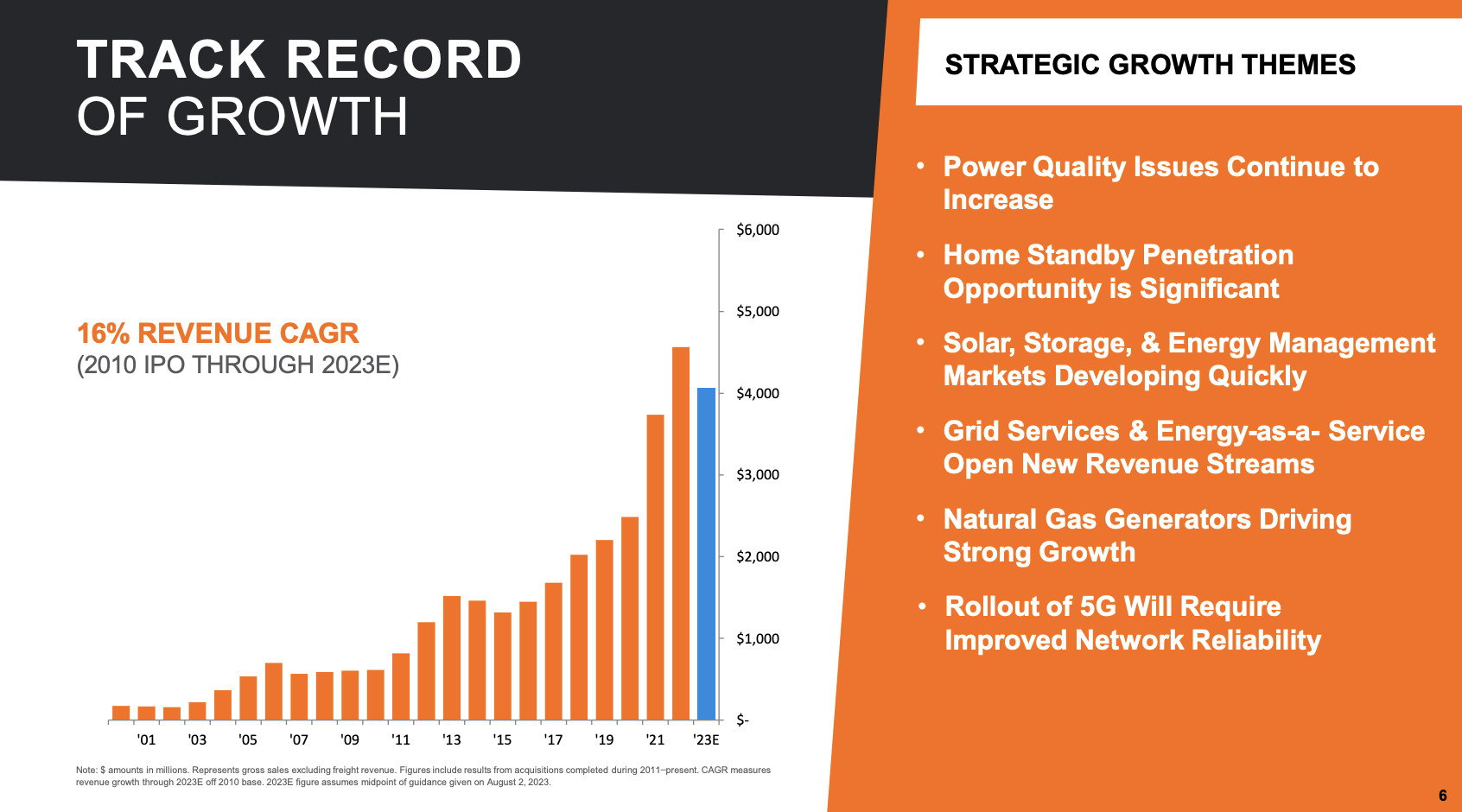

Using the company's own numbers, this is expected to be the first year with lower revenues since 2015. Since its 2010 IPO, revenues have grown by 16% per year.

{kind=link}

Generac Holdings

With regard to balance sheet health, the total debt outstanding at the end of the quarter was $1.62 billion, with a gross debt leverage ratio of 2.8x.

The company expects this ratio to moderate in the second half of the year as LTM EBITDA increases.

Outlook & Valuation

Despite seeing strong demand, the company downgraded its full-year outlook due to a softer consumer spending environment for home improvement, impacting residential product sales, particularly shipments of home standby generators.

In other words, macroeconomic challenges are offsetting the company's secular tailwinds.

- Residential product sales for the full year 2023 are now expected to decline in the mid-20% range, compared to the previous expectation of a decline in the high teens range.

- Overall, net sales for the full year 2023 are now expected to decline between 10% and 12%, including a 2% net favorable impact from acquisitions and foreign currency.

Having said that, analysts are upbeat about GNRC's future. Both 2024 and 2025 are expected to see strong growth, potentially resulting in more than $900 million in annual EBITDA. Free cash flow is expected to rise to more than $520 million, which would imply a free cash flow yield of more than 7% in 2025E.

{kind=link}

Leo Nelissen (Based on analyst estimates)

Prior to the pandemic, GNRC traded at 12x EBITDA.

A consistent valuation close to that number would imply that GNRC is roughly 45% undervalued.

This would give the company a stock price target of $166. The current consensus price target is $141.

Based on this context, I believe that the potential upside is higher in case grid stability turns out to be weaker than expected. Any surprises like large blackouts or related hurricanes can cause (temporary) spikes.

I consider GNRC to be a wild card. It's an interesting long-term play on secular tailwinds and I think it's undervalued. It's a company that might do very well in light of longer-term grid challenges.

I may open a small trade in this stock over the next few weeks.

Takeaway

Generac Holdings is a captivating company poised to benefit from a number of mega-trends, including the evolution of the energy grid, the impact of climate change, and the need for reliable backup power. While the company faces short-term challenges, it remains attractively valued.

The critical factor to watch is the aging infrastructure of the American energy grid, which is under stress due to the rapid transition to renewables. This trend, along with GNRC's other major growth drivers, may lead to significant long-term growth.

Though 2023 may be a challenging year for GNRC, analysts anticipate a promising future, with potential annual EBITDA exceeding $900 million by 2025. The stock's current undervaluation suggests room for growth.

While GNRC is a wildcard investment, it offers an intriguing prospect for those looking to capitalize on long-term grid challenges.

For further details see:

A Fragile Grid And Mega-Trends - Generac Is A Buy