ODFL - A Freight Recession Could Finally Allow Us To Buy Old Dominion

2023-05-01 09:00:00 ET

Summary

- In this article, I explain why Old Dominion Freight Line is the best LTL trucking company in North America, thanks to highly efficient operations and a perfect price/quality mix.

- Unfortunately, the company is now hit by economic weakness, as its volumes are declining, driven by deteriorating demand.

- The good news is that potential weakness offers attractive buying opportunities, which I am eager to use to my advantage.

Introduction

Recessions aren't fun - far from it, actually. However, they offer opportunities to patient investors, especially when it comes to stocks that never seem to be cheap. One of these companies is Old Dominion Freight Line ( ODFL ), a stock I have monitored for years. Last year, I finally decided that I wanted to make ODFL a big part of my portfolio, mainly because I expected weak economic growth to pressure the stock and offer buying opportunities.

While ODFL is still not where I want it to be, it is now officially in a freight recession, as it reported a steep volume decline in its first quarter, which comes with a ton of negative news from its industry.

However, the company used its pricing power to offset this weakness and reported another blowout operating ratio.

In this article, I will guide you through the new numbers and explain why and how I'm looking to buy ODFL this year.

So, let's get to it!

ODFL Is The Best (That's A Fact)

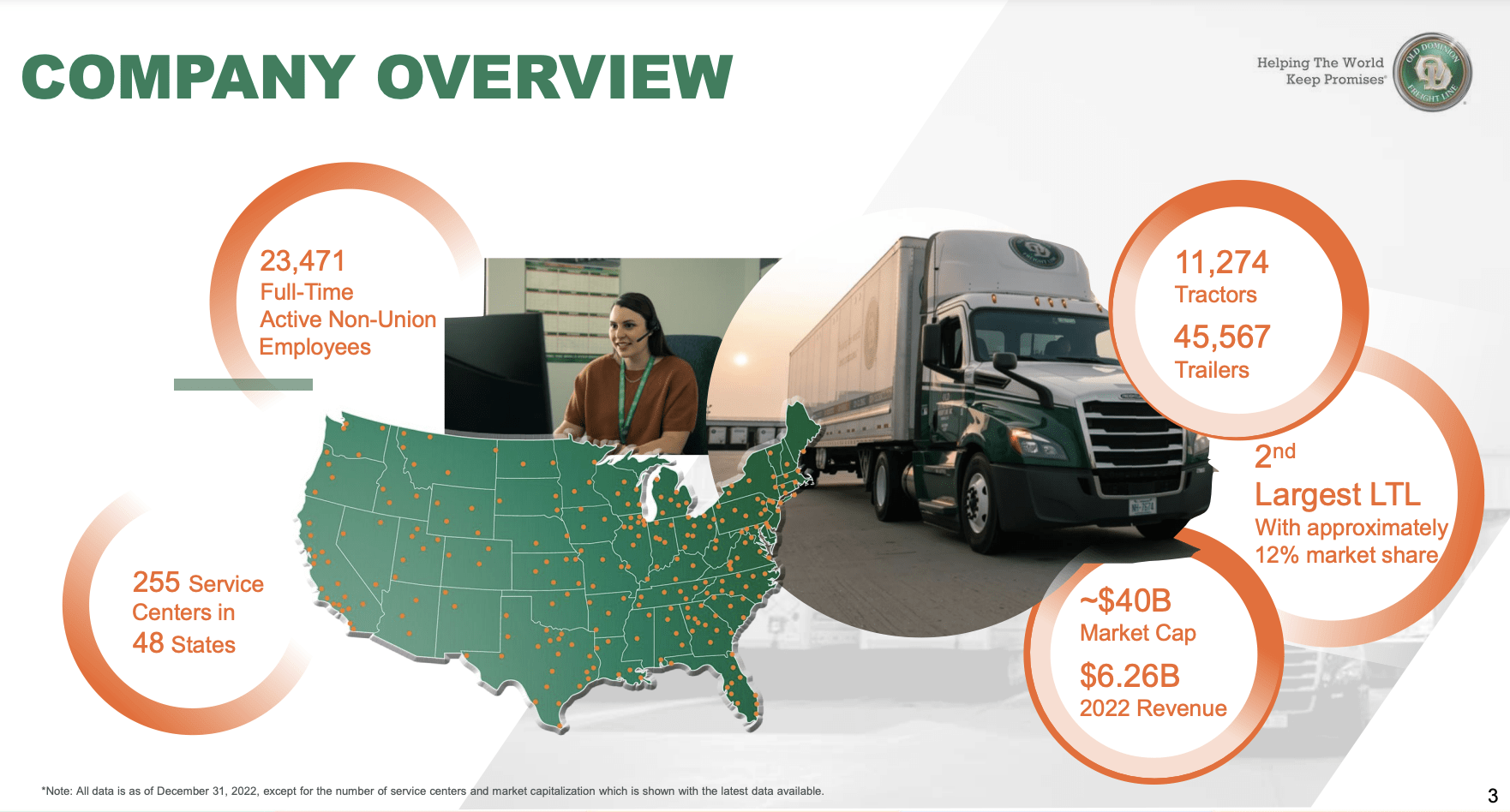

While it's often tricky to tell which company is performing the best in a given industry, it's not difficult in the less-than-truckload industry. North Carolina-based LTL giant ODFL is the most efficient operator in its industry - by a mile.

The company has an operating ratio of just 73.4%, which is slightly higher compared to the prior-year quarter, but a number that continues to blow me away. What this means is that it takes the company just 73.4% of its revenue to maintain its operations. While that might seem like a lot, it's extremely low for a capital-intensive trucking company. Most of its peers would do anything to maintain an operating ratio below 90%.

{kind=link}

What makes ODFL so special is its fast network of service centers and its technology that connects 255 service centers in 48 states to more than 11,000 trucks. Even more important, the company is mainly growing organically, which means it isn't buying competitors to accelerate growth.

According to the company (emphasis added):

Our infrastructure allows us to provide next-day and second-day service through each of our regions covering the continental United States. In addition to numerous service center renovations, expansions, and existing service center relocations, we opened 4, 27 and 37 new service centers over the past one, five and ten years, respectively , for a total of 255 service centers at December 31, 2022. We believe these actions produced increased capacity within our service center network and provide us with opportunities for future growth .

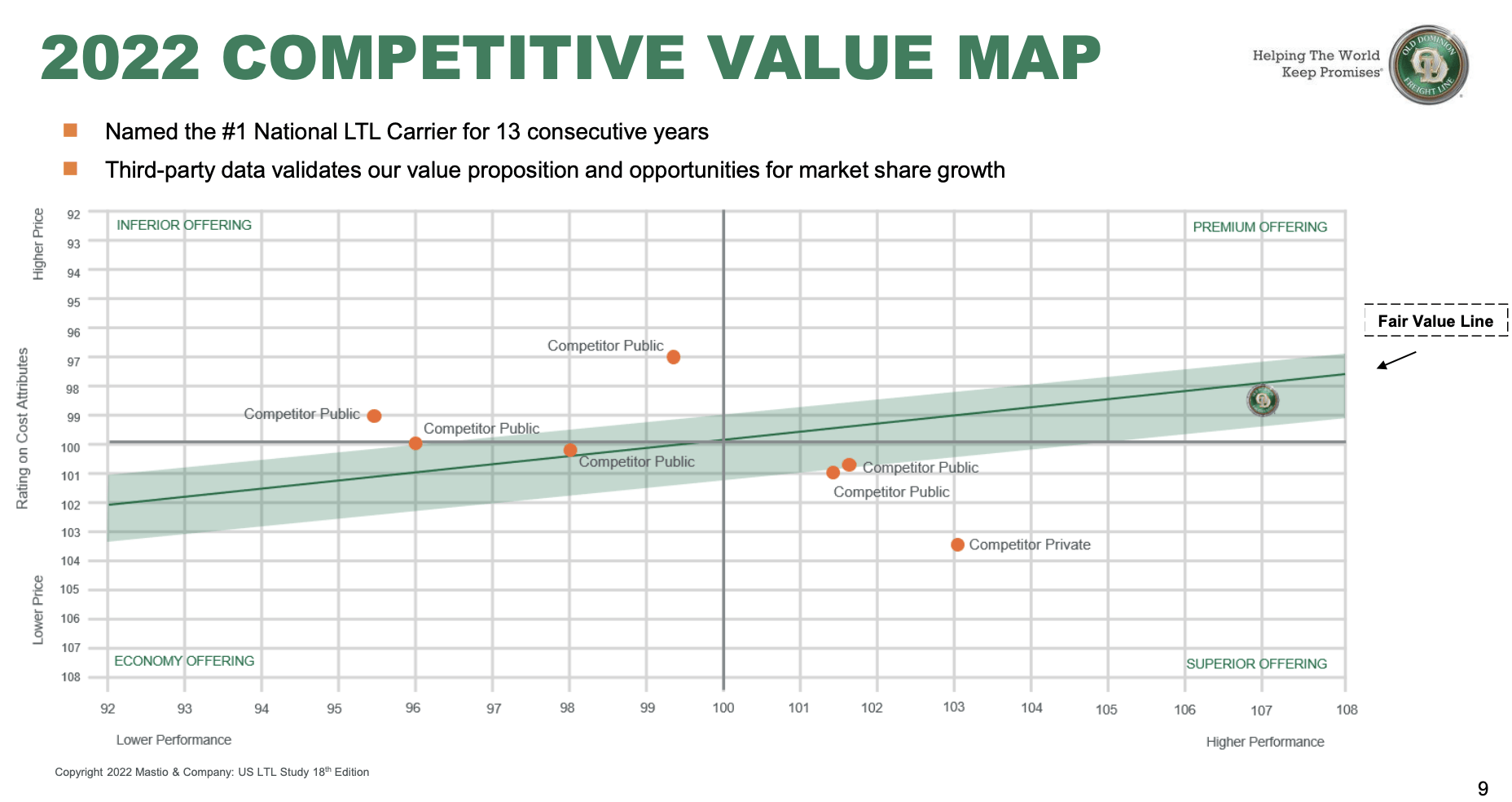

Using the company's own numbers, it looks like the company offers the best performance in the industry (I have heard confirmation from industry insiders) at a price similar to most of its competitors.

{kind=link}

While I do not have all data from peers (we need to trust the company on that), there is a lot of data to back up the company's claims.

- 70% of the company's shipments are next or second day.

- The on-time service has improved from 94% in 2002 to 99% in 2022.

- The cargo claims ratio has declined from 1.5% in 2002 to 0.1% in 2022.

- The company has won the Mastio Quality Award (#1 carrier) for 13 straight years.

As a result, organic growth has been nothing short of impressive. From 2002 to 2022, the company has compounded its revenue by 12.8% per year.

Margins have also grown. While the operating ratio isn't an official metric tracked by data providers like YCharts, we can use the operating margin for that, which has risen from less than 15% in 2013 (which is already impressive) to almost 30% in the first quarter of 2023. This allowed operating income to grow roughly 5x during this period.

Hence, over the past five years, ODFL has returned 265%, beating the S&P 500 by a considerable margin.

This performance has caused me to remain on the sidelines, as I wasn't willing to chase the stock price.

Now, we might get the opportunity to buy, as ODFL's industry is in a bit of trouble, which could trigger a significant drawdown.

Economic Trouble Is Hitting ODFL

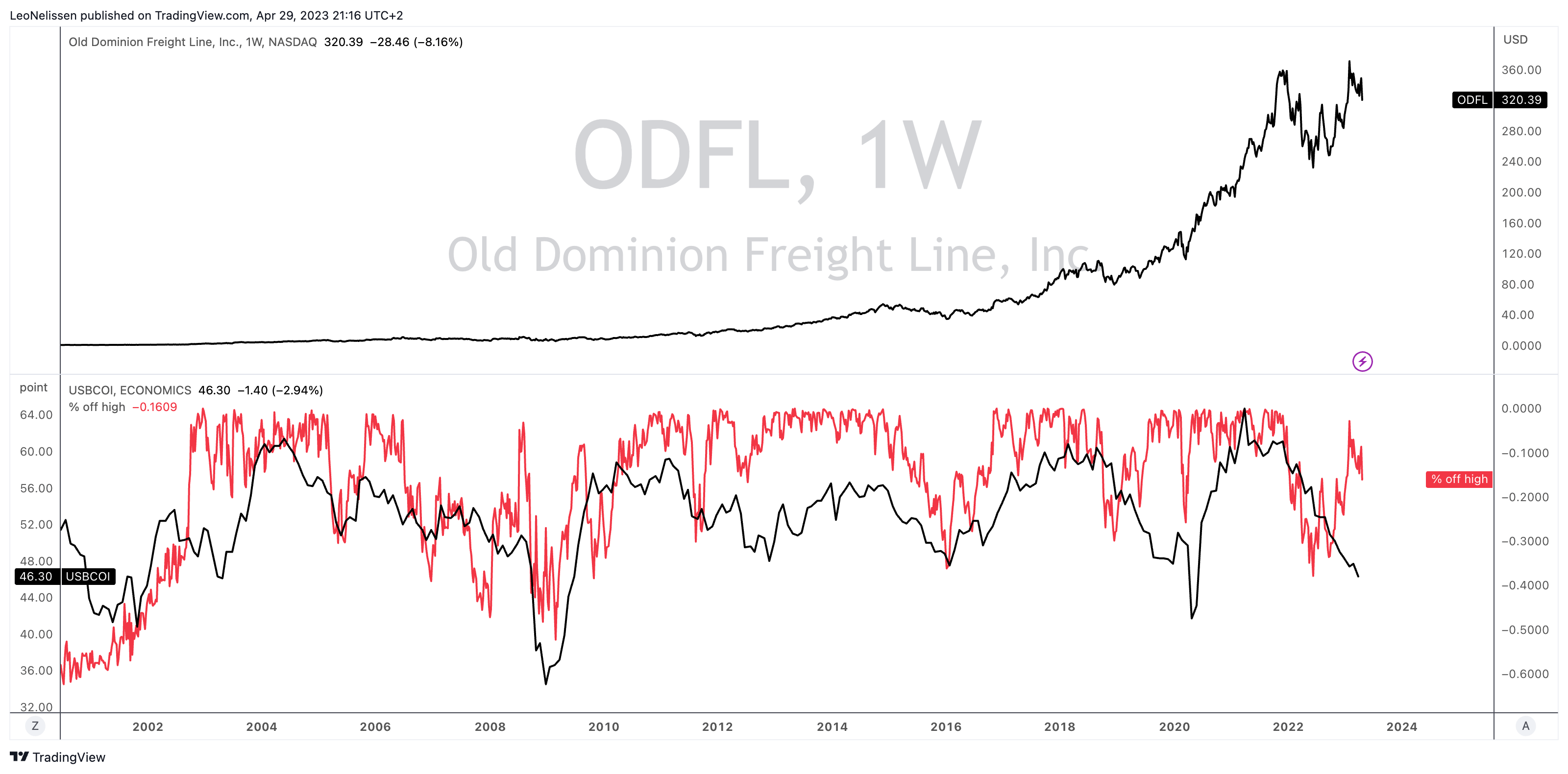

The chart below shows two things. The upper part shows the ODFL stock price. As we already established, its performance has been off the charts in the past few decades.

The lower part of the chart compares the ISM Manufacturing Index (black line) to the distance (in %) ODFL shares are trading below their all-time high. As we can clearly see, the correlation is very high, which makes sense as less-than-truckload demand is highly tied to industrial production. The lower the ISM index, the lower ODFL shares tend to fall.

{kind=link}

Painting with a broad brush, it's fair to say that a sell-off between 25% to 30% offers buying opportunities.

With that in mind, the ISM index is in a rather steep decline, which has been ignored by ODFL. While I would make the case that the company benefited from tremendous pricing power, there is no denying that industry fundamentals are being dragged down.

In early April, FreightWaves CEO Craig Fuller updated his outlook on the industry after warning of a freight recession a year earlier.

{kind=link}

As of the second quarter of 2023, the freight market appears to be worse than the freight recession of 2019. Executives of both carriers and brokers who have spoken to FreightWaves describe the current freight market as being among the most challenging of their careers. SONAR data supports this, with tender rejections on the verge of dropping below 3%, potentially setting the stage for a second trucking bloodbath.

The white line in the chart below displays rejections. Truckers are struggling to get orders, accepting (almost) everything that crosses their paths.

FreightWaves

Several trucking companies have shut down, with one executive blaming the closure on a large, long-term shipper suddenly pulling freight from the company and giving it to another carrier. The low tender rejections have also had an impact on contract rates, as it is unlikely that spot rates will trend up.

According to FreightWaves, the spread between contract and spot rates has widened, indicating that as long as the spread is so wide, shippers will continue to look to the spot market for capacity solutions, and carriers will seek to replace any spot loads with contract rates, even if the contract rates are lower.

FreightWaves

While ODFL is the best player in the market, its recent earnings confirm that demand is weakening.

In its first quarter, the company generated $1.44 billion in revenue, which is $40 million below estimates and 4% below the prior-year quarter result.

As the overview below shows, the company is feeling a softer economy. Tonnage per day declined by 11.9%, it had almost 10% fewer shipments and slightly less efficient operations, as weight per shipment declined by 2.5%.

The decrease in volumes was largely due to some shippers having fewer shipments than normal due to economic headwinds, while others were beginning to emphasize price versus service and choosing lower-priced carriers. However, the company's market share has remained relatively consistent, which is important, as its pricing strategy is important.

FreightWaves

However, the company's pricing remained on point. Revenue per hundredweight increased by 9.2%. Excluding fuel surcharges, that number was still 8.6%.

Furthermore, Old Dominion's first-quarter operating ratio increased to 73.4% due to a slight deterioration in the company's operating metrics. The improvements in the company's direct operating costs did not sufficiently offset the increase in overhead costs as a percentage of revenue. The company's fixed cost categories increased as a percentage of revenue during the quarter due to the deleveraging effect associated with the decrease in revenue as well as the timing and significance of certain expenditures.

Nonetheless, it needs to be said that an operating ratio in the low 70% range is absolutely fantastic.

Moreover, the company said that capacity is not currently an industry issue due to the weakness in industry volumes. ODFL believes this will once again become a critical differentiator for the company when the economy improves. The company believes its consistent long-term investment in service center capacity has been and remains a strategic advantage that supports its long-term market share goals. During this period of revenue decline, ODFL will also maintain a disciplined approach to managing its variable cost and discretionary spending to protect its profitability.

With regard to the outlook, the company anticipates the softer demand environment will continue. However, the company is well-positioned to respond to any acceleration in volumes that might occur if and when the economy improves. The economy will eventually recover, and ODFL is confident that when it does, its team's execution will allow it to achieve further growth and profitability while also increasing its shareholder value.

Valuation

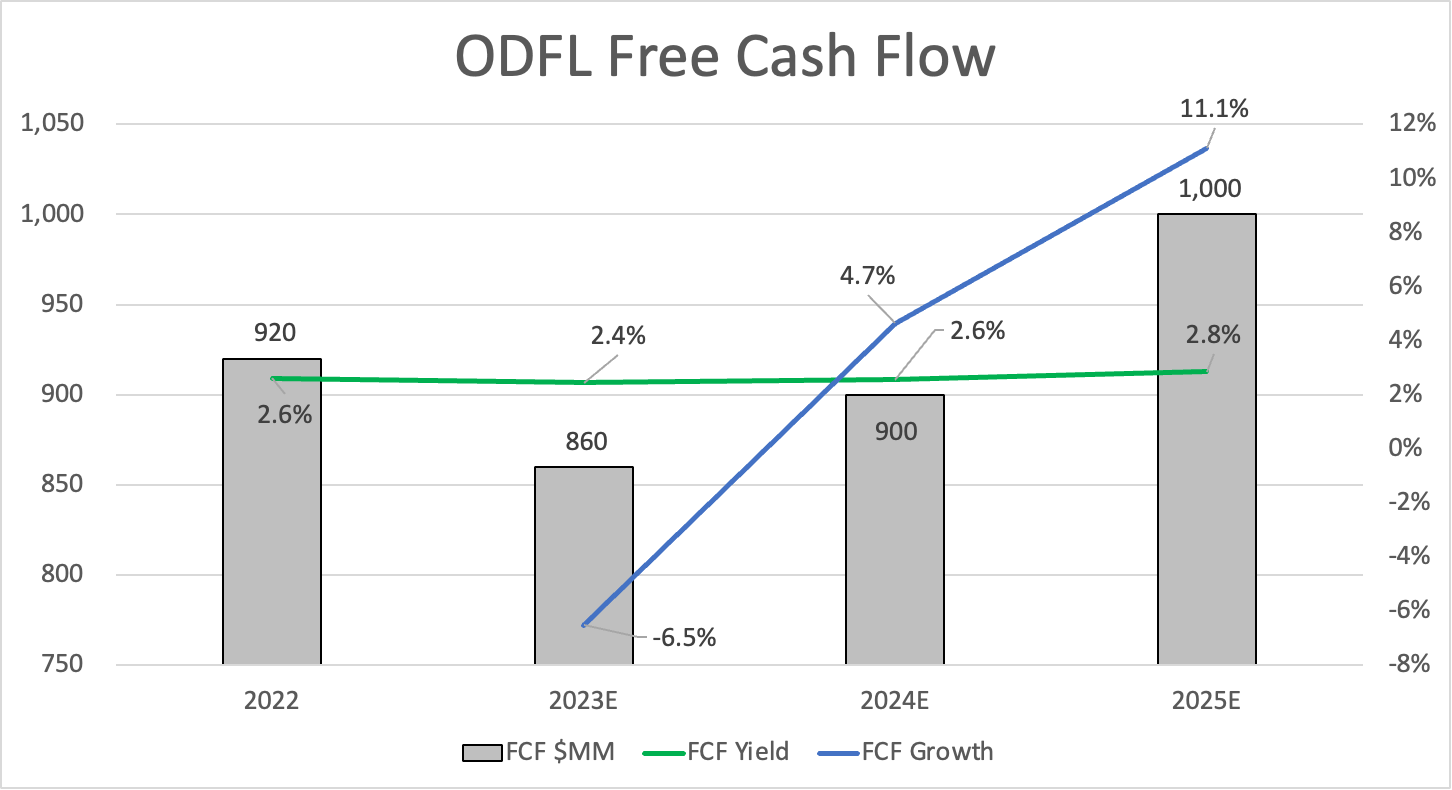

Analysts agree with the company when it comes to the outlook that 2023 will remain challenging. After a blowout performance in 2022, sell-side analysts expect free cash flow to fall by roughly 6.5% this year to $860 million. Next year, free cash flow is expected to grow again (by 4.7%).

{kind=link}

As you may have seen in the chart above, the company's free cash flow yield is below 3%. It is expected to stay below 3% until at least 2025.

This is a very low yield. The company is trading at roughly 40x free cash flow. As a comparison, a lot of railroads are trading close to 20x free cash flow.

The difference is that ODFL is expected to grow fast on a long-term basis.

Recently, Deutsche Bank came out, making the case that ODFL could generate $4 billion in operating profit in 2030 ($1.8 billion in 2022). This could propel the stock price to $600. In this case, the bank excluded any COVID-related benefits.

FINVIZ

I agree with this assessment and believe that the stock could be higher than that.

For now, I still dislike the valuation, as I believe that ODFL has more room to fall. As I said in prior articles , I would be interested in buying ODFL shares if another correction opportunity were to present itself. I'm looking for $280 as a first entry.

However, waiting for more weakness is a tricky game to play, as ODFL is well-positioned to deal with headwinds. It has a terrific balance sheet (almost $2.8 billion in expected net cash (negative net debt) in 2023, strong pricing power, and the ability to use operating efficiencies to somewhat offset volume weakness.

If we weren't in an economic downtrend, I would be a buyer at these levels. However, given my view on macroeconomic conditions, I am willing to wait for better buying prices.

Takeaway

I sometimes joke that a big part of my day consists of watching the ODFL stock price. It's one of the stocks I desperately want to add to my dividend growth portfolio, as its business model goes well with my current rail holdings.

Although I could buy ODFL right now, I believe that investors will get a better opportunity. The freight recession is deepening and impacting ODFL. While ODFL has a superior business model and the ability to use pricing and efficiency to somewhat offset the impact of weaker demand, it is trading at a juicy valuation that could come down if the long-term term growth outlook is impacted.

Hence, if the economy continues to decline for a few more quarters, I am fairly sure investors will get to buy ODFL at a 10% to 20% discount from current prices.

At that point, I will be an eager buyer, as I am convinced that ODFL will continue to be a long-term outperformer.

For further details see:

A Freight Recession Could Finally Allow Us To Buy Old Dominion