LNG - A Generational Opportunity For Tellurian

2023-10-31 15:33:16 ET

Summary

- Tellurian is a development stage LNG and natural gas producer aiming to sell low-cost US natural gas in the international market.

- The company's integrated business model allows it to capture the spread between cheap US natural gas and international prices, providing higher profitability.

- The energy transition and increasing recognition of natural gas as a transition fuel create a growing demand for LNG production, which facilities like Driftwood can fill.

Tellurian Inc. is a development stage LNG and natural gas producer looking to take abundant low-cost US natural gas and sell it into the international market. Tellurian's 27.5 MPTA Driftwood LNG liquefaction facility is the last fully licensed major US LNG project designed to produce LNG this decade. The Driftwood facility benefits from the energy transition's growing commitment to natural gas and capitalizes on the higher margin provided by Tellurian's integrated business model.

Tellurian's model differs from its competitors by capturing the spread between cheap US natural gas $2.971/mmBTU and international prices -- TTF (Euro Benchmark) $15.293/mmBTU and JKM (Asia Benchmark) $17.840/mmBTU -- versus a tolling model which limits profitability to a few dollars per mmcf/d of LNG produced. See HH, TTF and JKM benchmark prices on 10/24/2023 listed below. Tellurian will share this attractive spread with its shareholders and equity partners. By funding its Driftwood liquefaction facility with equity partners, Tellurian shareholders should benefit from its potential $4-5 billion in annual cashflow once Driftwood is operating.

natural gas prices HH TTF JKM (Tellurian Inc daily email)

Executive Chairman Sharif Souki has argued that traditional LNG financing models based on long-term tolling contracts are not sufficiently profitable to meet current development costs and future maintenance costs. Recently reported problems at competitors Venture Global, Freeport LNG, and Next Decade suggest that Souki is right. Off taker delivery problems, deficient maintenance and op ex, and shareholder participation at Venture Global, Freeport LNG and Next Decade suggest the toll road business models with thin margins have created these problems. Tellurian's integrated model better allocates development and operating costs which will lead to off takers receiving their expected cargoes and fewer plant disruptions (e.g. explosions). Consequently, Tellurian's lucrative integrated business model should avoid these industry problems because its funders will be fairly paid for their participation.

The energy transition has evolved from an effort to cancel all fossil fuel production and nuclear energy and replacing those energy sources with wind and solar. Europe had embraced this strategy but found itself in an energy crisis before Russia's invasion of Ukraine. Today, natural gas, LNG, and nuclear are increasingly recognized as transition fuels. They provide a pragmatic balance of energy generation and low carbon emission reduction targeting net zero 2050. Thought leaders like this Japanese think tank concluded recently that $7 trillion in natural gas development will be needed by 2050. This forecast, like Wood Mackenzie's market analyses, suggests that facilities like Driftwood will be needed to fill an LNG production gap in the years ahead.

Tellurian's management team has helped to build 79% of US LNG facilities and is working with Bechtel to construct Driftwood. Furthermore, because liquefaction is a commercially proven technology, the primary challenge to Tellurian is securing the financing of the $14-15 billion Driftwood facility. If Tellurian successfully finances Driftwood in the coming weeks and months, we believe there is a five to ten fold return potential for its shares by first half 2024. Assuming a five times EBITDA multiple on projected annual cash flows of $4-5 billion, when Driftwood is fully operational, Tellurian could trade at a $20-25 billion market capitalization around 2030. Based on Tellurian's $379 million market capitalization, Tellurian's market cap grow fifty-fold.

The Global Economic-Environmental Case for LNG:

Natural gas is the cleanest fossil fuel in terms of carbon emissions. Natural gas emits about one half the carbon which is emitted by coal. In recent years, activist groups have promoted banning all fossil fuels and switching to renewables - primarily solar and wind. Unfortunately, physics has shown that eliminating all fossil fuels and nuclear power will lead to an energy crisis and food shortage. Powerful arguments have suggested that transitioning to renewables is a process that will take decades. Furthermore, policies which seek to accelerate that transition will lead to energy and food crises.

Mark Mills, a world class energy expert provides an entertaining short video highlighting the fallacy of a rapidly deployed renewables only energy strategy. Please watch his video .

Europe, which aggressively adopted a rapid transition to renewables at an unrealistically fast pace found itself in an energy crisis and then Ukraine was attacked by Russia. Russia went on to use energy as a weapon of war. Today energy security has become an important new strategic consideration for energy policy and investment decisions. Once natural gas is liquefied and placed on an LNG ship, that cargo can be easily shipped around the world. This allows energy users to diversify their energy supply sources to reduce carbon emissions and increase energy security.

UN Sustainability Goals' top priorities are ending poverty and ending hunger. Natural gas addresses both of these top UNSDG goals while simultaneously reducing carbon emissions. An energy transition emphasizing natural gas can reduce carbon emissions, provide fertilizer to feed billions and energy to lift the world's poor out of poverty.

EQT Corporation, the largest US natural gas producer, makes the following argument for international LNG. " Unleashing U.S. LNG and replacing international coal with American natural gas is the largest green initiative on the planet and the world's best weapon to address climate change." EQT states that "the emissions reduction impact of an unleashed US LNG scenario is equal to:

- Electrifying every US car

- Powering every home in America with rooftop solar and backup battery packs [and]

- Adding 54,000 industrial scale windmills, doubling US wind capacity."

Furthermore, "By 2030, an unleashed US LNG scenario would reduce international CO2 emissions by an incremental 1.1 billion metric tons per year" and US citizens would be paid for this initiative (tax revenues and an additional $75 billion in royalties 3 , as opposed to paying for it."

The institutional energy market is moving in the direction of greater reliance on natural gas. This week, Bloomberg energy analyst Steven Stapczynski reported that Europe is signing long-term LNG contracts despite political pledges to rapidly reduce carbon emissions. Furthermore, the Biden administration seeks to increase US LNG supplies to Europe and replace dirtier Russian sourced natural gas. The Presidential joint declaration of March 2022 helped to lift Tellurian share prices to $6 per share. Europe did not consummate those import deals in 2022 due to Europe's lack of degasification facilities -- at the time -- and the EU's preference of a hydrogen solution. Today, that thinking may have changed.

For a comprehensive overview of the US shale boom, please watch Peter Zeinan's The First Shale Revolution : Humble Beginnings and then The Second Shale Revolution: Industrial Expansion. The first video describes the early development of the US natural gas business and how it made the US energy independent. This revolution explains how the US turned from an LNG importer to an LNG exporter. From 2000 to 2006, Cheniere Energy shares rose from $1 to $40/share when it initially built a gasification facility to import cheaper international LNG; however, when abundant natural gas was found in US shales with hydraulic fracturing and horizontal drilling, Cheniere found its business model was upside down and its shares declined from $40/share to $1/share. Note the share prices of Cheniere Energy Inc from 2000 to the present.

Cheniere Inc 25 year stock price chart (Yahoo.finance)

{kind=link}

Souki then restructured Cheniere Energy to make it a liquefaction company and Cheniere today is the largest LNG producer in the US. Cheniere's stock rose from $1/share to $183/share. The second video discusses how the US took its shale oil and natural gas and turned it into low-cost power plant fuel for electricity which then broke the US dependency on coal and made the US the leading reducer of carbon emissions on a relative and sustainable basis on the planet! This shale history helps to explain the recent $60 billion acquisition of Pioneer Natural Resources by Exxon Mobil and Chevron Corporation's $53 billion acquisition of Hess Corporation.

History of Tellurian:

This is our ninth article on Tellurian, a spectacularly volatile stock due to its extraordinary upside potential, if Tellurian can successfully finance its Driftwood LNG facility. Our reports are updates of Tellurian's financing history highlighting its successful milestone developments and financing setbacks. Tellurian is led by a joint effort between Charif Souki, who co-founded Cheniere Energy ( LNG ) -- the largest LNG producer in the US, CEO Octavio Simoes, the former President and CEO of Sempra LNG & Midstream, and Martin Houston, Tellurian co-founder and former COO of BG Group plc. Our first article in October 2021 highlighted the exceptional return potential of Tellurian by quantifying Cheniere's 269% and 138% annualized rates of appreciation during Cheniere's funding and construction phases. Our second article in August 2022 covered the company's change to an equity first funding strategy. Our third article predicted that funding was imminent and was published a day before its debt with warrants offering . Our fourth article, October 2022, analyzed the bond offering cancellation, 50% share decline, and revised investment prospects. Our fifth article , February 2023, identified the first commercial sign that Driftwood funding was still possible. Our sixth article highlighted a potential strategic equity prospect through GAIL's "EOI" Expression Of Interest announcement. Our seventh article highlighted a $1 billion sale leaseback LOI that will provide $1 billion in equity/mezzanine capital for TELL. Our eighth article highlighted the binding commitment letter with Blue Owl, for a $1 billion sale leaseback transaction with Driftwood. Today's article discusses Tellurian's unusual price weakness and value opportunity for this asymmetric LNG disruptor.

Tellurian Financing Prospects:

Tellurian's valuation reflects a distressed liquidation value. However, if Tellurian is able to secure additional financing for its upstream business and grow its upstream business to $400mm/year by 2027, Tellurian's upstream business could be worth 3 to 5 times EBITDA multiple or $1.2 billion to $2.0 billion in the next 4 years.

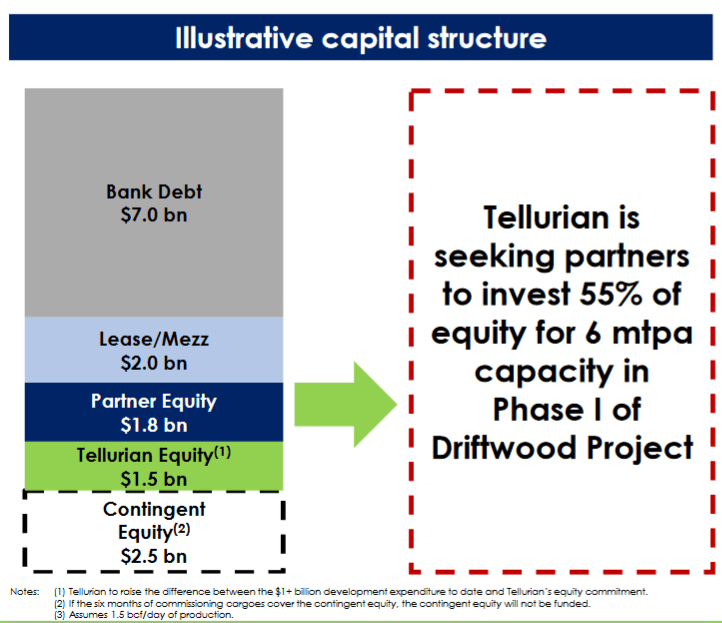

Overwhelmingly, the biggest variable in valuing Tellurian is tied to Driftwood LNG's financing prospects. Below is a diagram of the capital structure that has been proposed by Tellurian to finance Driftwood LNG.

Below each segment of the capital structure is assessed for the risk associated with each component.

Bank Debt $7.0 bn

Project finance is a particular type of long-term financing of infrastructure or industrial projects that is based upon projected cash flows of a project as opposed to the balance sheet of the sponsor. These loans are financed off of a bank's balance sheet. Port Arthur, for example is priced at 2 ¼ over the LIBOR- the London Interbank Offered Rate. Like the fed fund rate, LIBOR is a short term rate. LIBOR, like the fed funds rate, has risen to 5 1/4% following a sharp run up since 2020 and has paused. Unlike 10 and 30 year Treasury rates which have been rising this year, this huge loan should be in the 7 ½% range. The loan will be similar to a credit line for a construction project, where a combination of equity and bank line are drawn down to pay Bechtel's monthly EPC fee. The liquefaction equipment which will be the majority of the $12 billion. These project loans are considered low risk loans. Jamie Dimon CEO, of JP Morgan, would likely lead a syndicate of banks to fund this $7.0 billion bank line. Project finance is an easy spread business for a bank to book where the banks' capital costs lies between its deposit rates, the fed fund rate, or LIBOR rate.

Driftwood capital structure (Tellurian August 2023 Investor Presentation)

{kind=link}

Lease/Mezz $2.0 bn

The lease has been publicly offered by Blue Owl in its sale leaseback agreement for $1 billion. Blue Owl will pay Tellurian $1 billion for ownership of the Driftwood project and site with a 40 year lease at an 8.75% cap rate (rent = $87.5 million/year) with a 3% annual escalator. Blue Owl is a sophisticated publicly traded finance company with Doug Ostrover as Co-CEO . It is intriguing that Ostrover "was a founder of GSO Capital Partners (GSO), Blackstone's alternative credit platform and a Senior Managing Director at Blackstone until 2015." Blackstone was a key private equity funder to Cheniere Energy, Inc. We suspect Ostrover is familiar with or was involved with the debt and or private equity financing of Cheniere Energy, Inc. and may have worked with Souki in the past.

The other $1 billion in mezzanine finance is where we believe the Driftwood project has been held up. In the spring, Souki had said the company had a term sheet out with an equity investor with whom they had worked in the past. We speculate that this could be John Paulson, because John Paulson is a Tellurian shareholder and was involved with financing Cheniere Energy, Inc. I met John Paulson when I worked at Alex Brown in the 1990s. Earlier this spring, in an interview with David Rubenstein, Paulson said he liked asymmetric investment opportunities. Paulson is a Wall Street phenom whose firm made 20 billion dollars buying credit default swaps on sub-prime mortgages during the Great Financial Crisis and may have been the true inspiration for the book and movie "The Big Short" and not Michael Burry another investment genius who also owned credit default swaps on sub-prime mortgages during the GFC. Paulson's investments in credit default swaps were in the billions through various hedge fund vehicles he set up at the time. Burry's investments were much smaller. Paulson could easily be attracted to the potential asymmetric spread between international LNG prices and Henry Hub prices. A private equity convertible stock with an equity upside would be consistent with financing structures used by Cheniere Energy, Inc. in the past and could be attractive to private equity and infrastructure investors.

For a non-strategic equity partner (an entity not interested in owning or handling the LNG like John Paulson) the signing sales purchase agreements (SPAs) would give financial or infrastructure investors a steady tolling fee for risk mitigation, but also the spread between international natural gas prices and domestic prices. On Souki's September 13, 2023, weekly video , Souki stated (4:20 in video) that if the company is able to secure a $2.75/mmcf, they would have about $0.50 to give to infrastructure funds that are now investing in the LNG space. A compelling example of a private equity investment in the LNG space is Warren Buffett's $3.3 billion July investment in Cove Point. Buffett paid about 10 time cash flow for his investment and the Driftwood equity is being offered at about one times cash flow. The obvious difference is that Cove Point is built and currently cash flowing. Driftwood is not. Driftwood should start generating its first LNG revenues in 2027. Until the company begins generating cash flow, investors will be assuming the risk that the project won't be completed and generate cash flow as expected. Actual interest payments can be made in PIK (pay in kind) equity until the company begins to generate cash flow in 2027.

Consequently, we believe that if Tellurian has 11 MPTA in SPAs, they could comfortably secure $1 billion in infrastructure financing for this mezzanine financing. Martin Houston reported on Bloomberg this week that they are working on their portfolio of SPAs .

Partner Equity $1.8 bn

The private equity partners have been the focus of Tellurian, since last September when they pulled the $1 billion 11 1/4% 2027 notes with warrants. The equity partner strategy alternatively focuses on the sale of a share of equity ownership of Driftwood. For strategic partners, Driftwood is an appealing piece of energy infrastructure which will give each equity partner a share of the equity economics of Driftwood LNG. Tellurian is seeking $1.8 billion. The Blue Owl deal required that Tellurian reveal who these entities are to preapprove them and that they have the financial capacity to be "contingent guarantors". We believe several have been preapproved by Blue Owl or they would not have converted their original letter of intent into a binding commitment . The profile of an equity partner, strategic equity partner or contingent guarantor is a substantial entity capable of paying its share of rent, mortgage, and operating expenses for decades. Logical partner prospects include Shell plc, Saudi Aramco, Tokyo Gas Co. Ltd, as well as European, Korean, or Indian energy companies or utilities who want access to low-cost high quality US LNG.

Tellurian Equity $1.5bn

Tellurian itself is an equity owner of the Driftwood project and has invested $1 billion in the project and will continue to fund its construction. Its share -- inflation adjusted -- is estimated at $1.5 billion. That funding piece is assured as one billion is already invested.

Contingent Equity $2.5bn

Contingent equity is what Tellurian will invest into the Driftwood LNG project from commissioning cargoes. Commissioning cargoes are the first (approximately six months) of cargoes from a new facility while the sponsor is testing its equipment and output to assure that it meets specifications. Tellurian has committed six months of commissioning cargo proceeds to the project. This is one area where significant controversy, regarding Venture Global, has arisen. Venture Global built a huge low-cost prefabricated facility and sold its off taker fees at very low prices. However, when the commissioning cargoes were set to end and Venture Global was to send their customers their LNG, the company -- Venture Global -- argued that those cargoes were theirs due to there being equipment issues. According to Reuters "U.S. liquefied natural gas ((LNG)) company Venture Global LNG sold over 200 LNG cargoes worth about $18.2 billion since its first export plant started operations in March 2022, according to vessel data and Reuters gas price calculations.

Those shipments have become a flashpoint for gas buyers and marketers who insist they should have received some of the supplies under long-term contracts for Venture Global's Calcasieu Pass export plant in Louisiana. There have been at least three contract arbitration cases brought this year." Tellurian has said it will be fully transparent in its financial model and contracts implying that in working with their team, long-term off takers will get the cargoes when they expect them. We believe Tellurian has had the time to study this problem and the Freeport LNG explosion and shape a financing model which will be more reliable in the future.

We believe that Tellurian has been speaking with counterparties for each of these funding stack. While contracts have not been finalized, we believe the management has shown contract terms with each counter party. We believe with the completion of their off take portfolio with SPAs as an option, they will be able to fine tune prices to secure the best terms for the company and its shareholders.

Tellurian's Attractive Shares Valuation:

We value Tellurian's shares by separately analyzing its upstream E&P business and its downstream Driftwood LNG facility. Tellurian's upstream natural gas business generates 200mmBCF/day of natural gas on 31,000 acres of land in the Haynesville and should generate $100mm in EBITDA this year according to Charif Souki on September 19th, 2023. Cash flow multiples for gassy E&Ps run in the 3-5 times area. Due to Tellurian's 31,000 acre Haynesville property ownership, the value of its pipelines, and LNG value add prospects, we think a 5x 2023 EBITDA multiple on its upstream business is fair value. However, conservatively valuing the cash flow at three times, we conservatively value their upstream business at $300mm.

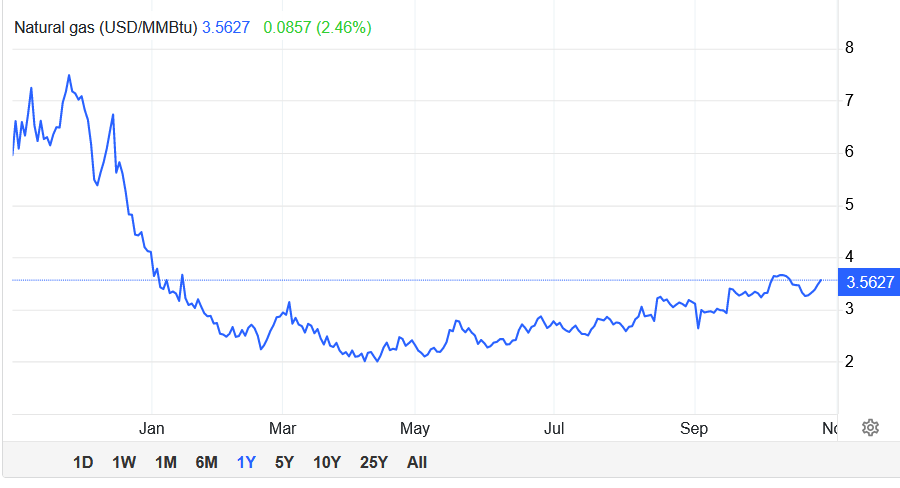

Natural gas prices are firming and up 2.36% today, 6.63% this month, and -40.17% year to date in the table below as of October 27th, 2023.

Henry hub prices day month and ytd (Tradingeconomics.com)

{kind=link}

As a result of Russia's invasion of Ukraine in 2022 natural gas prices spiked to $10/mmBtu which prompted a rapid expansion of US natural gas production that ultimately led to a collapse in natural gas prices back to $2/mmBtu. Today, natural gas well counts are declining, and natural gas prices are reversing upward as shown in the chart below. Furthermore, as LNG capacity ramps in the years ahead, natural gas prices should firm further helping Tellurian's upstream cash flows. Tellurian's natural gas production break-even is $1.8 to $2.0/mmBtu. Consequently, Tellurian's operating leverage is significant. Continued strength in natural gas explains the decline in operating profitability from 2022 into the first half of 2023.

Chart of Henry Hub nat gas benchmark (Tradingeconomics.com)

{kind=link}

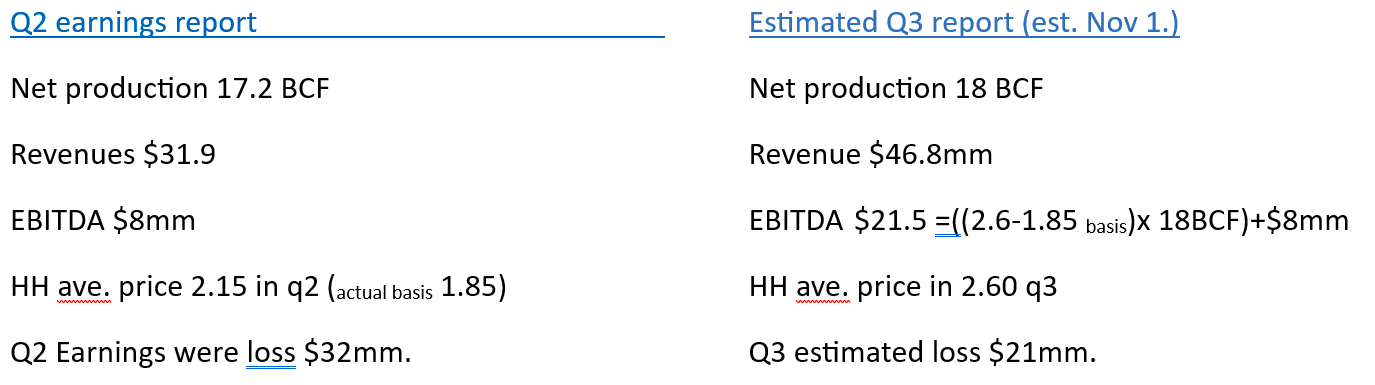

Tellurian's upstream business will need to scale significantly to produce the needed feed stock for Phase 1 of its 27.5 MPTA Driftwood facility. Tellurian plans to double its production from 200mmcf/day to 400mmcf/day and the company stated it plans to do a financing before year end to fund this additional production according to Souki's September 19th video. This will be a private transaction and the counter party might split upstream or midstream cashflows and or get liquefaction rights with Driftwood LNG. Logical equity partners are public and private natural gas E&Ps like those which have expressed an interest in selling their natural gas internationally. Potential upstream funders include EQT Corporation (EQT), Chesapeake Energy Corporation (CHK), Rockcliff Energy , Comstock Resources, Inc. (CRK), Devon Energy Corporation (DVN), Antero Resources Inc. (AR), Range Resources Corporation (RRC), and Southwestern Energy Company (SWN). Earnings are expected to be released November 1st, 2023, and with those latest cashflow numbers, a transaction could be negotiated by year end.

Tellurian's second quarter's earnings were poor due to low natural gas prices, low volumes, and drilling expenses. The third quarter should be much better as the company stopped drilling, natural gas prices are rising and production volumes are growing. With those improved cash flows, Tellurian should be able to continue funding Driftwood construction until they complete their financing. Below are our rough estimates of the company's financials for Q3.

estimated TELL q3 earnings vs q2 (Income Growth Advisors, LLC)

{kind=link}

The newly restructured convertible cash covenant was reduced to $50 million. See Note 17 10-Q August 8, 2023 . The company will have $107mm-50mm=$57mm in cash to draw down and an ATM to draw on to cover out estimated $20 million quarterly cash burn.

Valuing Driftwood LNG

Without the facility being fully constructed and without financing, we conservatively value Driftwood at $100 million. Driftwood is the last large fully licensed LNG project expected to produce LNG this decade. This $100 million resale estimate is "10 cents on the dollar" despite Tellurian having invested over $1 billion. Once financing progress is announced, such as an SPA or binding letter of intent, Driftwood's valuation would increase immediately.

If Tellurian secures the $14.5-15 billion for construction, then the value of Driftwood should jump as the public market risk-adjusts future cash flows of $4-5 billion a year. From a market capitalization of $400 million to $20 billion in 2031, the annualized equity return is approximately 63%. Consequently, Tellurian's abnormally high volatility is directly related to its financing prospects.

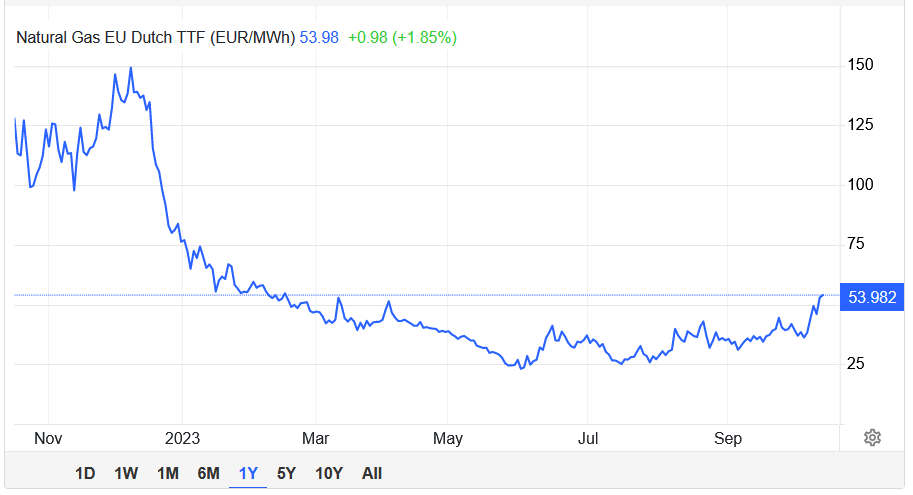

The giant opportunity for Tellurian is to sell its LNG abroad. The European TTF index chart below shows that prices are firming. LNG prices are also improving for the Asian JKM. Higher international prices should stoke interest in signing LNG deals with Tellurian.

TTF Dutch natural gas benchmark price (Tradingeconomics.com)

{kind=link}

The conversion for Euros/MWh to $/mmBtu is 0.31. TTF $53.982EUR/MWh x .31 = $16.73/mmBtu.

Based on Tellurian's proposed pricing structure with a third party buyer ( SPA ) at Henry Hub + 15%= 2.97 x 1.15= $3.642 plus transfer fee of $2.75/mmBtu = $6.39 LNG cost. The TTF is $16.73/mmBtu which is a $10/mmBtu spread.

See Tellurian's Driftwood model emailed daily below:

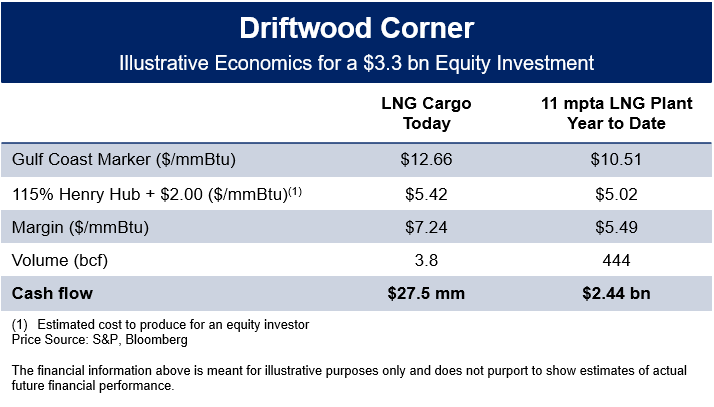

Tellurian shows a Gulf Coast Marker a metric Platts uses to reflect the "daily export value of LNG traded free on board (FOB) from the US Gulf Coast." This gives an indication of what the profitability of the Driftwood plant would be for this year to date and based on prices this year and tabulated daily.

illustration of Driftwood plant economics (Tellurian daily email 10.26.2023)

{kind=link}

The Box diagram above shows that the entire 11 MTPA through October 24th, would have generated $2.44 billion in cash flow. Annualizing that cash flow number equals $3.34 billion for all 11 MTPA. Tellurian is offering strategic equity investors 55% of Driftwood for a 55% share of its cash flow. Consequently, the strategic funders or contingent guarantors should earn $1.834 billion in CF for 2023 according to the illustration above and on investment of $1.8 billion. This prospectively illustrates a very attractive one times cash flow return.

Tellurian which has or will invest $1.5 billion should get $1.5 bn in cash flow prospectively based on this illustration based on prices year to date. Both Tellurian and its strategic partners are getting paid out at one times cash flow. We believe there are interested funders "Contingent Guarantors" who have been preapproved by Blue Owl. These could be Shell, Saudi Aramco, or Tokyo Gas based on their scale and interest in LNG.

So when funded, the Driftwood facility could be valued at $3.34 billion based on adjusted year to date cash flow example. Consequently, we believe a $100 million valuation for Driftwood is a conservative valuation.

Combine Tellurian's conservative $300mm upstream value plus Driftwood's $100mm valuation, Tellurian's conservative market capitalization is $400 million. $400 million/583 million shares = $0.686/share. Positive news on earnings, the FERC permit extension, and or an SPA could lead to prices around $1.70 when Blue Owl's financing was first announced and they signed a binding commitment letter July 18th.

A Rare Investment Opportunity:

Compelling investment opportunities are typically contrarian investments. For example, when selling, the shrewd investor sells when everyone is buying and ideally in a state of "irrational exuberance." Nobel Laureate Robert Shiller wrote his brilliant and exquisitely timed book Irrational Exuberance in March of 2000-the tech bubble peak. Alternatively, buying when others are selling, panicked, or completely disparaged also makes sense. Severe negative sentiment often occurs when a security is priced at low or distressed valuation levels. Many owners of Tellurian are discouraged with its shares down 90% from when it peaked in May of 2022, following the Russian invasion of Ukraine. Furthermore, since July, Tellurian shares have declined 62% from $1.71/share to $0.65/share. This was caused by weak second quarter earnings, Gunvor's SPA cancellation, and the FERC construction permit extension overreaction.

On the positive side on September 4th, Baker Hughes agreed to supply eight key refrigerant compression packages for Phase 1 for 2027 production. To deliver Driftwood on schedule, maintaining long lead time orders "in the queue" is critical to avoiding delays in construction and maintaining cash flow forecasts. Compressors and refrigeration units are in great demand and this Baker Hughes agreement keeps Tellurian on schedule even though the company's financing has not been completed. Additionally, Blue Owl pre-approved Tellurian's equity partners as "contingent guarantors" by signing its binding commitment letter, but closing expectations slipped from H2 2023 to H1 2024.

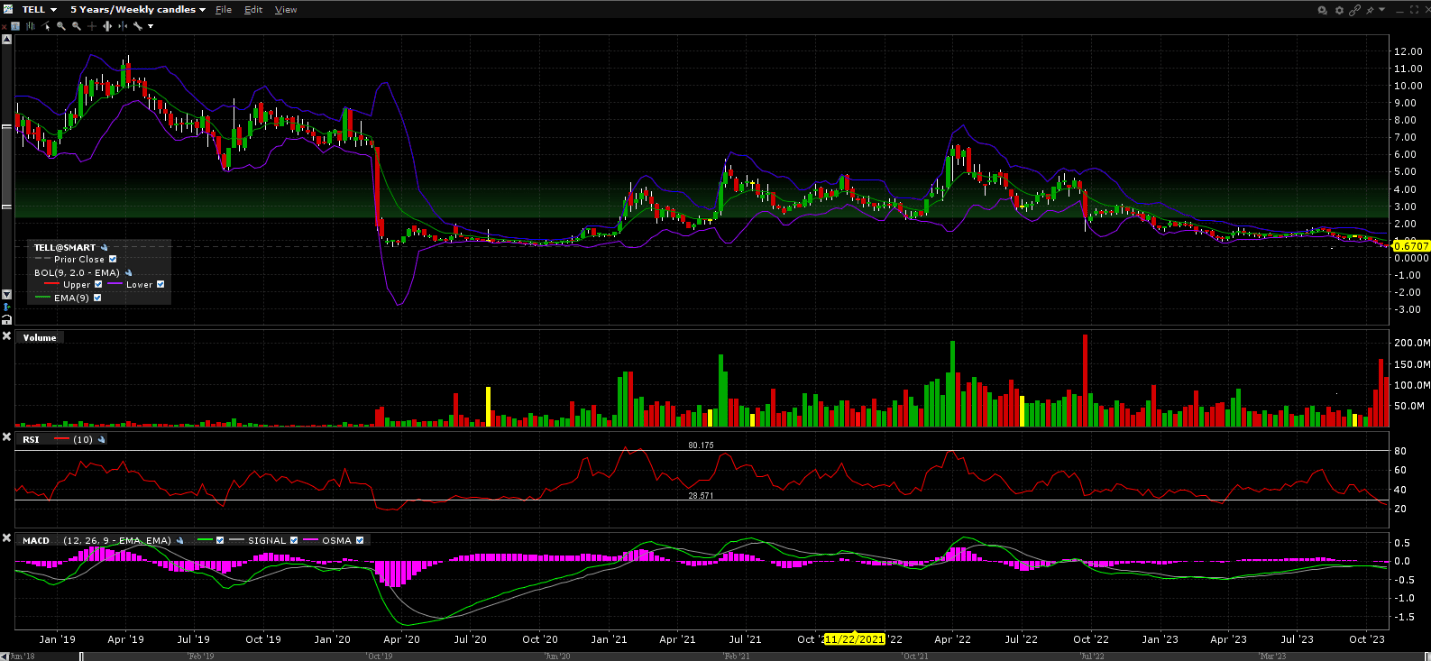

The chart below shows how Tellurian rallied from its nadir, below a dollar, and during the COVID 2020 market crash to over $6/share in the wake of the Russian invasion of Ukraine. Its share reversion back to below one dollar, despite development at the Driftwood LNG site, suggests despondent sentiment. The recent weeks' jump in volume from about five million shares a day to 25 million shares a day suggests major turnover in shareholder ownership. The spike in volume may be the handiwork of the shorts working to cover their 85 million share short position by scaring the longs into selling. We would not be surprised if new shareholders emerge and seek to gain control of Tellurian not unlike Carl Icahn's activist investment into Cheniere Energy Inc. in 2015, when Icahn famously ousted Souki just as Cheniere Energy was poised to begin producing LNG.

five year chart of Tellurian stock (IBKR traderworkstation)

{kind=link}

Last September, Tellurian withdrew its billion dollar offering and Tellurian announced that it intended to work with strategic equity partners whose businesses made those equity partners natural LNG off takers or natural gas feed stock providers. Partnering with strategic partners created mutually beneficial commercial relationships and not simply financial investors seeking attractive returns by investing in Driftwood. With these key strategic equity partners, Tellurian would finance the Driftwood project. Consequently, with the strategic equity partner model, subsequent SPAs cancellation were no longer essential since Tellurian planned to work with its equity partners who were natural off takers, feed stock providers, and or symbiotic business partners.

The SPA agreement is the traditional complement to the long-term tolling contract model that the Tellurian model seeks to out-mode. This September, with its contingent guarantors approved and liquefaction fees rising, Souki declared that if Tellurian could get HH x 115% plus $2.75/mmBtu, they could attract infrastructure funding. On September 13th, Souki announced that the company was going to reintroduce standard SPA offtake agreements. If Driftwood can sell liquefaction for $2.75/mmBtu, Souki said the company would have a $0.50 spread to attract infrastructure and private equity funding after $2.20 in operating, pipeline and interest costs per mmBtu.

On October 6th, the LNG Journal reported that Poten and Partners , an institutional natural gas research publication, reported that off takers are now looking at paying liquefaction fees between $2.60/mmBtu and $2.80/mmBtu. "Poten ship brokers heard that some developers are actively trying to market US LNG for about $2.60 to $2.80 liquefaction fee 'and we see some customers buying even at that prices,' he pointed out. This is largely because contracts linked to Henry Hub prices are still relatively cheap, compared to Brent-linked contracts."

This credible third party report showed us the market now trading at the levels which are sufficient to attract private equity to invest in LNG facilities like Driftwood. Souki can now sell LNG to strategic equity partners and or private equity firms at levels. Additionally, a combination of tolling and equity participation can now be offered with the SPA they are now securing. This should now allow Tellurian to finance Driftwood LNG.

The Poten article also described the US LNG market this year "Three substantial FIDs already took place in the United States in 2023 so far, all of them "junky projects," Poten's global head of business intelligence Jason Feer said." This confirmed Souki's assessment of the LNG market and that Tellurian's competition is offering "junky projects". This Poten report gives us comfort that Tellurian is in a position to finalize Driftwood financing.

Who are these private equity partners? BlackRock and Blackstone are two prominent and likely funders of LNG projects. Warren Buffett's Berkshire Hathaway recently invested in $3.3 billion in Cove Point at 10x EBITDA. Cove Point is a fully developed LNG facility owned by Dominion, but that compares to the 1 times EBITDA multiple that Tellurian is offering strategic equity partners to invest directly in its Driftwood facility.

Because the cash flows from Driftwood are not expected until 2027, a significant discount to future flows is reflected in the stock price. However, historically, when the financing prospects for Driftwood have appeared likely, Tellurian's shares have rallied sharply and sometimes ten-fold. This potential ten-fold return potential why Tellurian is so attractive to investors.

Co-Founder Martin Houston said this week that the company is putting together our portfolio of buyers (off takers) as we speak. Furthermore, if we see a cold winter, we could see the $25/mmBTU or higher in one or both the European benchmark TTF or the Asian benchmark JKM.

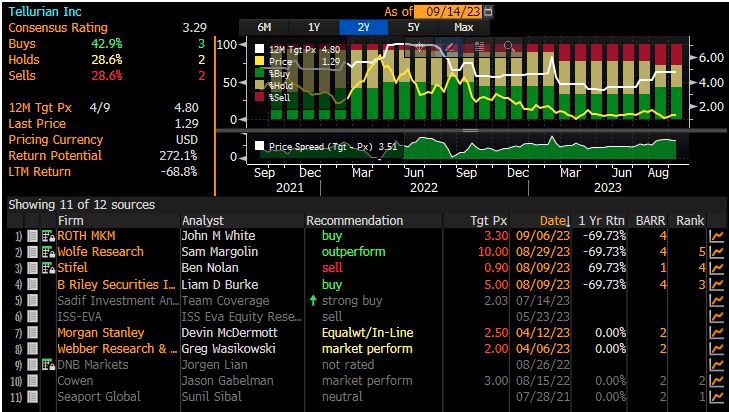

We are not alone in recognizing Tellurian's significant upside potential. Wolfe Research's Sam Margolin put out a research report with a $10/share price target.

Wall Street Analyst coverage list for Tellurian (Bloomberg)

{kind=link}

Conclusion:

Tellurian is an exciting investment opportunity due to its attractive valuation and extraordinary upside potential, if the company successfully finances its Driftwood LNG project. Tellurian shares are conservatively valued at $0.68/share or three times expected cash flow of $100 million for 2023 plus "ten cents on the dollar" for the $1 billion Tellurian has invested to date in Driftwood LNG - the last large fully permitted LNG facility to produce LNG this decade in the United States. While not without risk, Tellurian, if it successfully finances Driftwood LNG, could see its market capitalization rapidly rise to a valuation of $4-5 billion, based on forecast future annual cash flows of $4-5 billion in the 2030s. Due to the unique asymmetric upside opportunity versus downside risk, we believe Tellurian is a generational investment opportunity.

Tellurian has attracted some of Wall Street's smartest hedge fund investors like Paulson & Company and Shaw, D.E. & Co., Inc. as well as some of Wall Street's largest institutional investors including Vanguard Group Inc. with 41,110,453 shares, Blackrock Inc. with 24,623,898 shares, and State Street Corporation with 24,924,075 shares. Tellurian's management has built 79% of US LNG export capacity and has great contacts which could prove critical in pulling together Driftwood's capital structure.

The stock market today is largely driven by quantitative models used by institutions and those models frequently rank momentum as a top algorithmic input. Furthermore, the last four decades has watched Wall Street being made readily accessible to Main Street with low-cost online trading. Legions of retail investors look to online and social media forums for investment advice and this phenomenon has manifested itself in the " meme stock craze" in 2021 where stock valuations reached irrational valuations. With the volatility surrounding Tellurian, we believe that its 90% decline since 2022 has been compounded by institutional momentum trading and social media.

While Tellurian's cash flow dropped sharply due to the decline in natural gas prices from 2022 to 2023, neither momentum rankings nor social media commentary are designed to capture technical funding and valuation factors. Tellurian seeks to pioneer its integrated business model and shift the industry away from it historic SPA and toll road business model. Consequently, the declining importance of SPAs to Tellurian's financing success has been lost on the majority of investors, in our opinion. Likewise, most online commentary over the last month may have overstated a routine permit extension with FERC as a consequential delay. Herein lies the unique opportunity with Tellurian. Momentum investing works until it doesn't.

Now that a conservative valuation case can be made for Tellurian's shares, we believe panicked retail and momentum investors have sold their shares to sophisticated institutional shareholders educated in valuation analysis, project finance, and LNG contracts, manufacturing, and trade know how. Two sophisticated investors who have those skill sets are Warren Buffett and Carl Icahn. Buffett might pass on buying into Tellurian at this early stage, but Carl Icahn famously seized control of Cheniere Energy Inc., when Cheniere was poised to begin operations after Charif Souki had successfully converted Cheniere's operations from gasification to liquefaction.

Human nature is a constant in the market. Ben Graham famously wrote that in the short-term the market is a voting machine but in the long-term it is a weighing machine. While social media buzzes about a permitting delay and Tellurian's decline, Charif Souki was the keynote speaker for the International Energy Forum on Thursday in Riyadh, Saudi Arabia. Natural gas prices and geopolitical risks are rising. With Poten ship brokers saying deals are getting done at the levels Souki said can bring in private equity and infrastructure investors, we believe that Tellurian's asymmetric return profile is a timely generational investment return opportunity.

Whether you invest or not, following Tellurian may be a captivating corporate saga that may well provide extraordinary returns for intrepid investors.

Tyson Halsey, CFA and his clients own Tellurian, Inc. shares. Halsey is also President of Optima Process Systems Inc. and energy startup.

For further details see:

A Generational Opportunity For Tellurian