EPRT - A Historic Opportunity To Win Big With REITs

2023-11-18 08:05:00 ET

Summary

- We think that we are about to enter a new bond bull market.

- Bonds are cheap, but REITs are even cheaper.

- We expect an epic REIT market rally. Here's why.

Co-produced by Austin Rogers.

Bond yields for both the corporate and government sectors appear to have peaked and begun a gradual decline:

After the 10-year Treasury yield (US10Y) briefly touched the psychologically important level of 5%, bullish calls on bonds grew louder and more numerous.

In what follows, we explain our view that we are now in a new bond bull market, and why that could be a once-in-decade opportunity for real estate investment trusts ("REITs"), which the market widely perceives as bond proxies.

A New Bond Bull Market Is Born?

Calls to buy bonds appear to be coming from all corners of the market, from those who believe interest rates are going back to low levels and those who think they are simply oversold.

Here's a recent headline from Barron's that has been widely circulated:

{kind=link}

And another bullish call on bonds from Vanguard...

{kind=link}

And another bullish call from The New York Times ...

{kind=link}

Another interesting data point to note is that billionaire Bill Ackman, who famously shorted long-term Treasuries this year, recently closed his short position.

Business Insider via Yahoo Finance

{kind=link}

If the second half of October 2023 turns out to have been the peak in bond yields, Ackman's timing will have turned out to be extraordinarily good.

Finally, we observe that even Howard Marks, who believes that a "sea change" has occurred in markets that will keep interest rates permanently higher, has also become more bullish on bonds.

{kind=link}

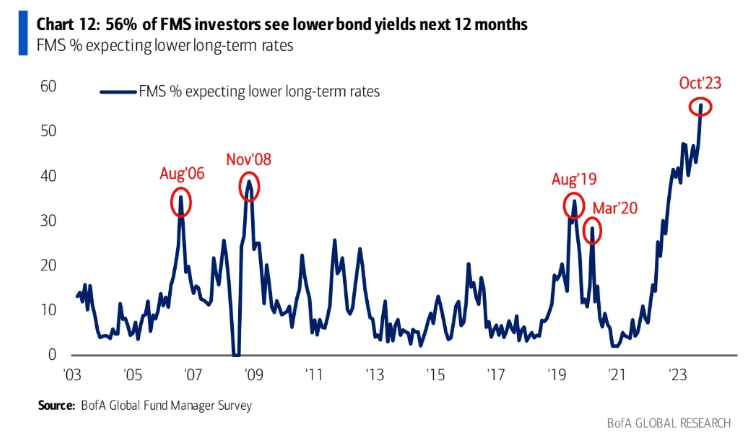

The cumulative bullishness on bonds has led to the highest percentage of global fund managers expecting lower bond yields in the next 12 months than at any time in the last two decades:

{kind=link}

Yes, we are aware of the huge amount of Treasury issuance that will be required in the coming quarters and years, but we believe that U.S. households, investment funds, insurance companies, and so on should be more than capable of absorbing that supply and then some.

Economic growth and inflation are both slowing, which generally results in lower interest rates as investors allocate capital to capture the risk-free real (inflation-adjusted) returns from Treasury bonds.

This logic will be even stronger if the US economy slips into recession sometime in the next few quarters, as we believe it will. For our explanation of this, see " The 2023 Recession Is Still Likely Coming ."

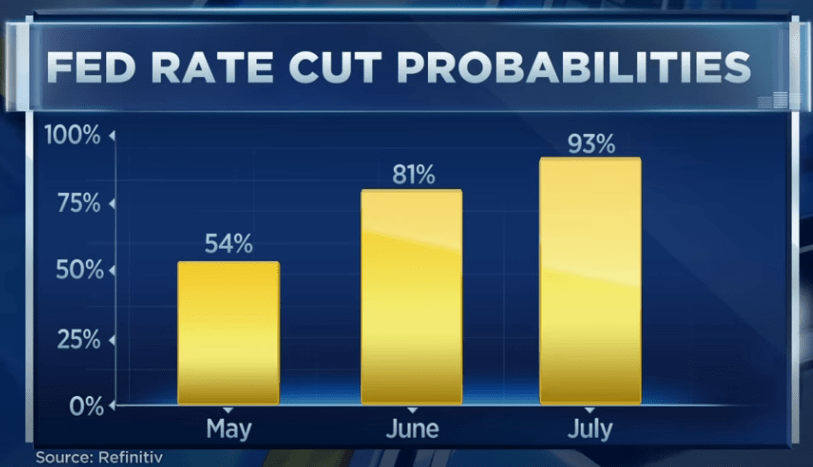

The market seems to be gradually coming to share our view on a likely ensuing recession, as Fed futures are now pricing in an over 80% probability of the Fed cutting the Fed Funds Rate in the first half of 2024.

{kind=link}

If a recession does manifest and the Fed cuts rates, then demand for Treasuries (and probably corporate bonds as well) should soar even higher than it is today, and bond yields should decline markedly.

Bond Bull Market = REIT Bull Market

Does this mean we are about to sell our REITs and buy bonds?

No, of course not.

Since the market treats REITs like bond proxies (even though they are much more than that), we believe REITs should deliver even greater returns than bonds during a bond bull market.

Consider the 12-year period of generally falling interest rates from 2008 through 2020. Even considering the huge REIT selloff during the Great Financial Crisis , REITs ( VNQ ) still pummeled bonds ( AGG ) on a total return basis during this extended period of falling interest rates.

Today, REITs have sold off by nearly 40% already, mainly corresponding to the drop in bond prices and, therefore, the spike in bond yields.

If bond yields fall, then REITs should rebound as income investors begin to seek out yield again.

Consider also that interest rates being where they are have caused investors to drop their allocation to real estate stocks to nearly their lowest levels in the last 15 years:

{kind=link}

If the primary headwind facing REIT prices is high interest rates, both because it creates an alternative for income investors and because it increases borrowing costs, then what will investors do when interest rates come down?

You guessed it: Investors will crowd back into the underweight sector of real estate and REITs.

Net Lease REITs: The Ultimate "Bond Proxy"

If REITs are viewed as bond proxies by the market, then net lease REITs are the "ultimate bond proxy."

We put that in quotes, because we believe net lease REITs are more than simply bond proxies, but we can see why the market is under this impression.

Net lease REITs invest in single-tenant properties with long lease terms, generally 10 years or more, with contractually fixed rent escalations of typically 1-2% per year. The business model of net lease REITs is to consistently invest in properties at yields greater than their cost of capital. This reliance on the capital markets for growth is a big reason why the market views them as bond proxies.

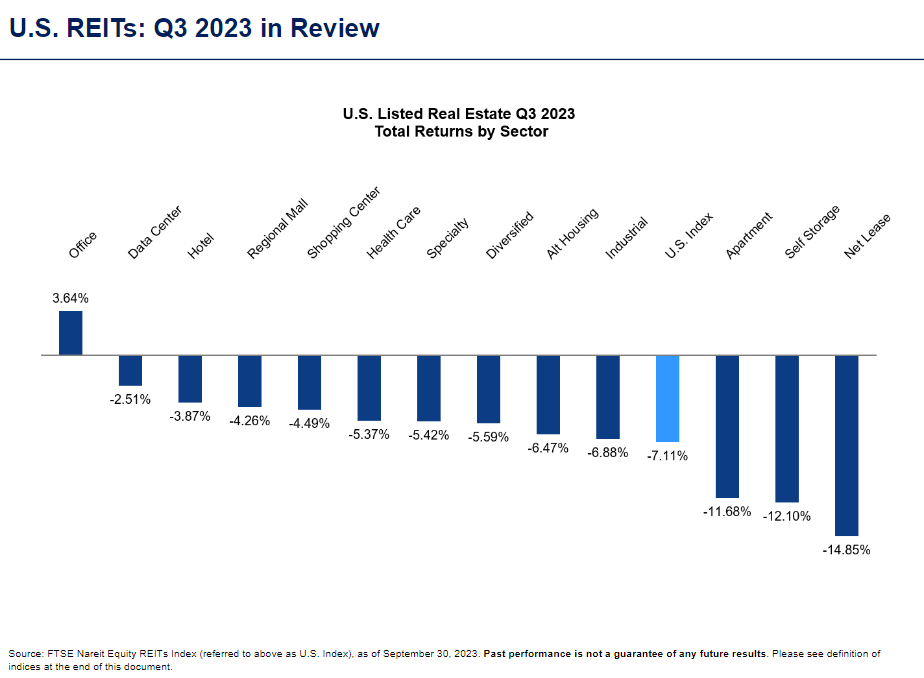

It is also the reason why net lease REITs turned in the worst performance of all real estate sectors in Q3 2023 as interest rates peaked:

{kind=link}

But this is where we believe the market misperceives the level of risk facing net lease REITs.

Some net lease REITs have virtually zero refinancing risk and the ability to grow their cash profits even without tapping into the capital markets.

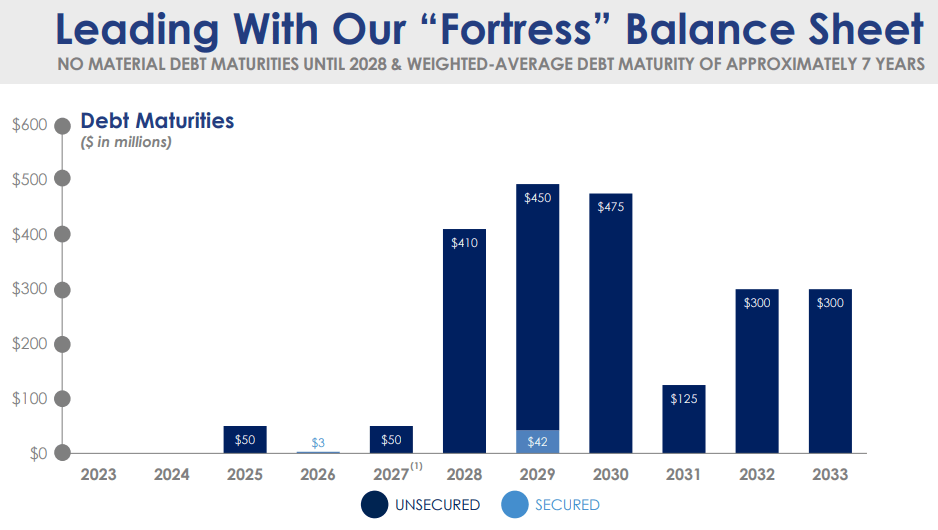

Take, for example, Agree Realty Corporation ( ADC ), which owns single-tenant retail boxes leased to the nation's largest and strongest retailers. Over 2/3rds of ADC's tenant base is investment grade rated, but its average annual rent escalation is only about 1%.

ADC has exceedingly little debt maturing until 2028, positioning it extremely well to weather elevated interest rates for however long they last.

{kind=link}

To quote CEO Joey Agree from the Q3 2023 conference call (emphasis added):

We are in an enviable position for the upcoming year. Our fortress balance sheet has no material debt maturity until 2028, avoiding refinancing headwinds. Simultaneously, our best-in-class portfolio with minimal lease maturities provide stable and growing cash flows. Even in the absence of external growth, this will enable us to deliver AFFO or true cash growth of over 3% next year on a per share basis.

The same is true of several other net lease REITs that prudently took advantage of the ultra-low interest rate era to lengthen their debt maturities.

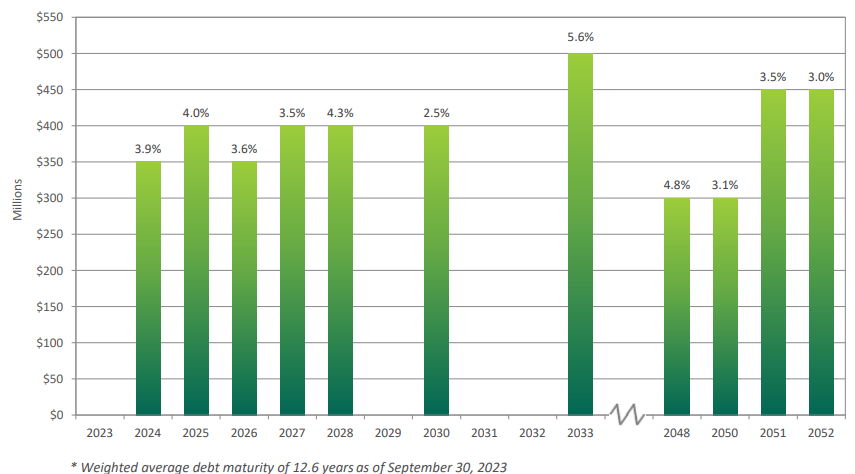

Take, for example, NNN REIT, Inc. ( NNN ), which also owns single-tenant retail properties but focuses instead on well-located and fungible real estate leased to non-investment grade tenants. The REIT's weighted average debt maturity is around 12.5 years, with maturities extending out all the way to 2052.

{kind=link}

To quote CEO Steve Horn from the Q3 2023 conference call (emphasis added):

In a time of prolonged uncertainty like today's macroeconomic conditions NNN's discipline of maintaining a solid balance sheet and reasonable acquisition volume does put NNN in a place to execute the remaining deal flow for 2023, but more importantly, to execute 2024 with limited, if any, needs to access the capital markets.

Even with $350 million of debt maturities in 2024, NNN still expects to grow next year with no need for external growth capital.

The REIT enjoys $188 million in annual free cash flow after dividends that can be deployed into acquisitions. Combining that with NNN's ~1.5% average annual rent escalation, analysts expect NNN to achieve ~3% AFFO per share growth in 2024.

Lastly, consider Essential Properties Realty Trust ( EPRT ), which owns mostly retail and some smaller industrial properties leased to private, middle-market tenants. EPRT has no debt maturities until 2027.

EPRT Q3 2023 Presentation

According to CEO Pete Mavoides on the Q3 2023 conference call (emphasis added):

Combining the reinvestment of our retained cash flow, our strong capital deployment year-to-date, and our healthy rent escalators net of tenant credit assumptions, we estimate our AFFO per share [can] grow nearly 4% in 2024 without requiring any additional external capital.

Like NNN, EPRT enjoys a weighted average rent escalation of about 1.5% and ample free cash flow after dividends, giving the REIT some ability to continue growing next year even if the capital markets don't cooperate.

Bottom Line

To be clear, we believe bond yields will come down meaningfully next year, which should give net lease REITs additional firepower from debt issuance for acquisitive growth.

What we are saying is that even if interest rates remain high and net lease REITs cannot issue accretive equity or debt for growth, they should still be able to grow the bottom line by some amount next year.

And if a new bond bull market is upon us, REITs and especially net lease REITs should rebound powerfully as well. There are a number of REITs that present up to 50% upside potential just to return half-way to their previous peaks.

That's why bond yields peaking and beginning to come down is great news for REITs and we are aggressively accumulating more shares to profit from the recovery.

For further details see:

A Historic Opportunity To Win Big With REITs