FRC - A Look At First Republic Bank's Death Spiral

2023-04-27 07:50:42 ET

Summary

- Shares of First Republic Bank have come under renewed pressure as concerns weigh over the company's ability to survive.

- Deposits plunged over the past quarter, and the company looks forced to consider significant asset sales.

- Whether the company survives and how much value remains will be determined by what kind of haircut it experiences while selling these assets.

April 25th proved to be a terribly painful day for shareholders of First Republic Bank ( FRC ). After the company announced financial results covering the first quarter of its 2023 fiscal year, shares of the business plunged, closing down 49.4% for the day before plunging another 29.8% on April 26th. At first glance, this reaction, much akin to a death spiral, by the market may seem peculiar. Yes, revenue and profits fell year over year. But not anywhere near enough to warrant such downside. On top of this, loans outstanding increased and the company's book value per share rose as well. But when you dig deeper into the picture, you come to understand the dilemma that the company is now facing thanks to panic in the banking sector. In truth, there is some probability that the company may not survive its current circumstances. But with regulatory support in place, it does make for a very interesting binary prospect for investors to consider.

The good, the bad, and the ugly

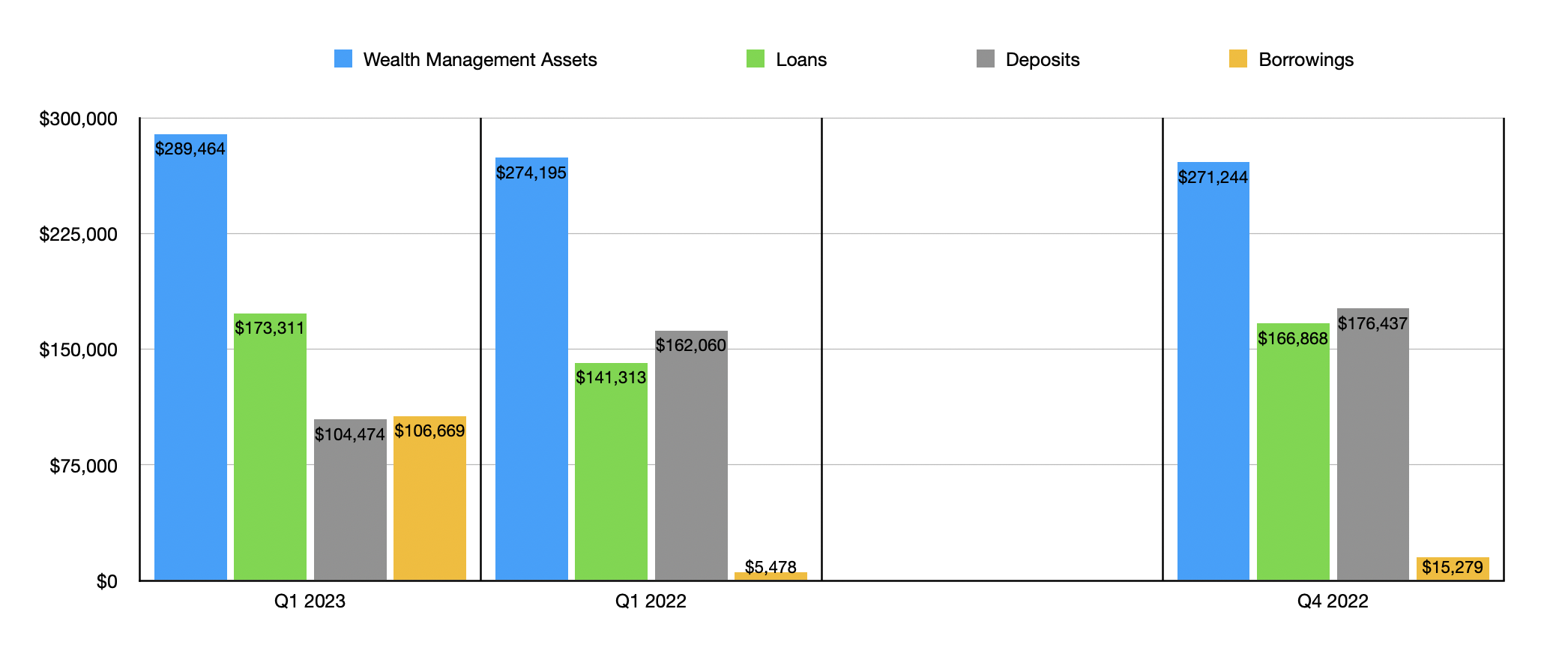

When I write articles like this, I like to try and look at the good and the bad. But the fact of the matter is that there is very little good in the financial data that management reported on April 25th. The good really does center around a couple of important metrics. For instance, the value of loans that the company has outstanding totaled $173.31 billion. That's up from the $166.86 billion that the company had only one quarter earlier, and it's up nicely compared to the $141.31 billion reported the same time last year.

{kind=link}

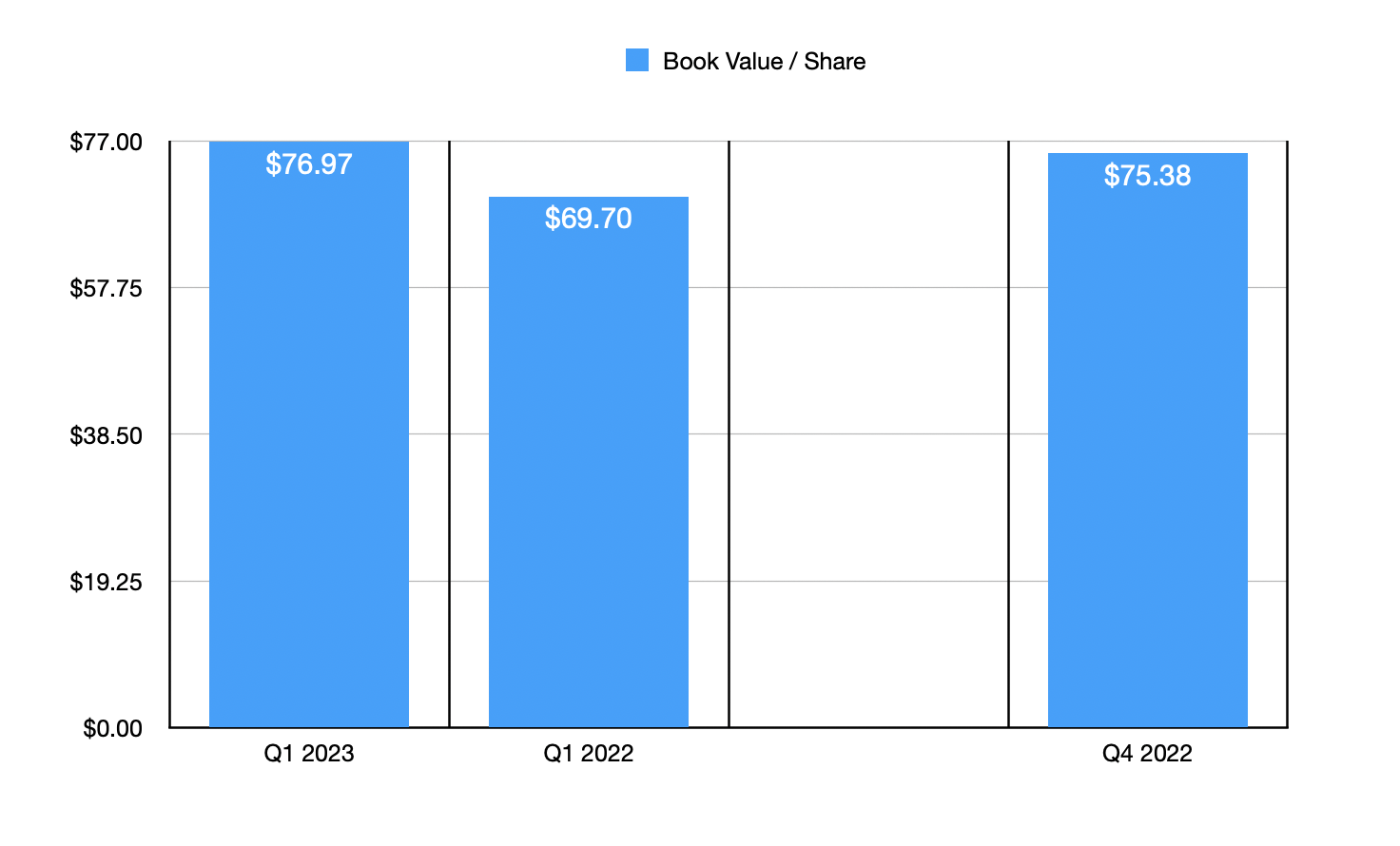

In addition to this, the company enjoyed an increase in its book value. This number grew from $69.70 per share in the first quarter of 2022 to $75.38 per share by the end of last year. By the end of the first quarter of this year, that number had grown further to $76.97. Lastly, wealth management assets for the company actually ticked up nicely, hitting $289.46 billion by the end of the quarter. That number was $271.24 billion at the end of 2022 and totaled $274.95 billion in the first quarter of 2022. This does show some strength in the face of what is otherwise a pool of weakness.

{kind=link}

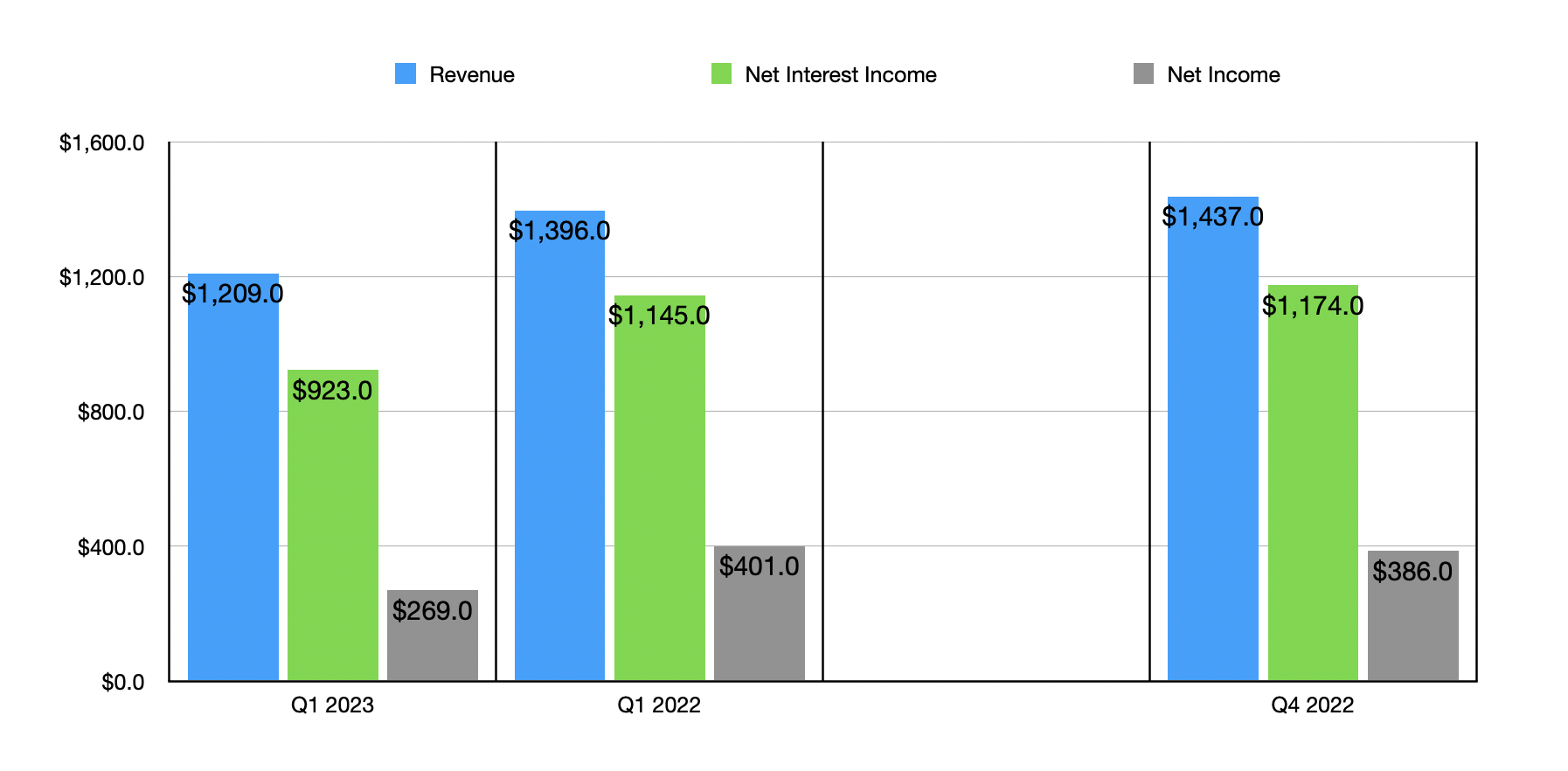

Outside of those couple of metrics, the rest of the data reported by management can be grouped into two separate categories. The first would be the bad, while the second would be the ugly. On the bad side of things, you have the fact that revenue for the enterprise did fall materially year over year. For the first quarter of 2023, revenue was $1.21 billion. That's down from the nearly $1.40 billion that the company reported only one year earlier. More than 100% of this decline came from a drop in the net interest income that the company reported. This number fell from $1.15 billion in the first quarter of 2022 to $923 million the same time this year. I'll get to that topic a bit more later.

{kind=link}

This drop in revenue brought with it a rather sizable decline in profits. Net income for the latest quarter was $269 million, which translated to earnings per share of $1.23. By comparison, at the same time one year earlier, profits were $401 million, or $2 per share. The decline of revenue, particularly of the high margin net interest income, was responsible for this pain. But this is where the picture starts to turn ugly. A decline in revenue and profits across the board is never great to see. But when you factor in the rising loans, wealth management assets, and book value, it seems farfetched that the company's stock price would take such a beating.

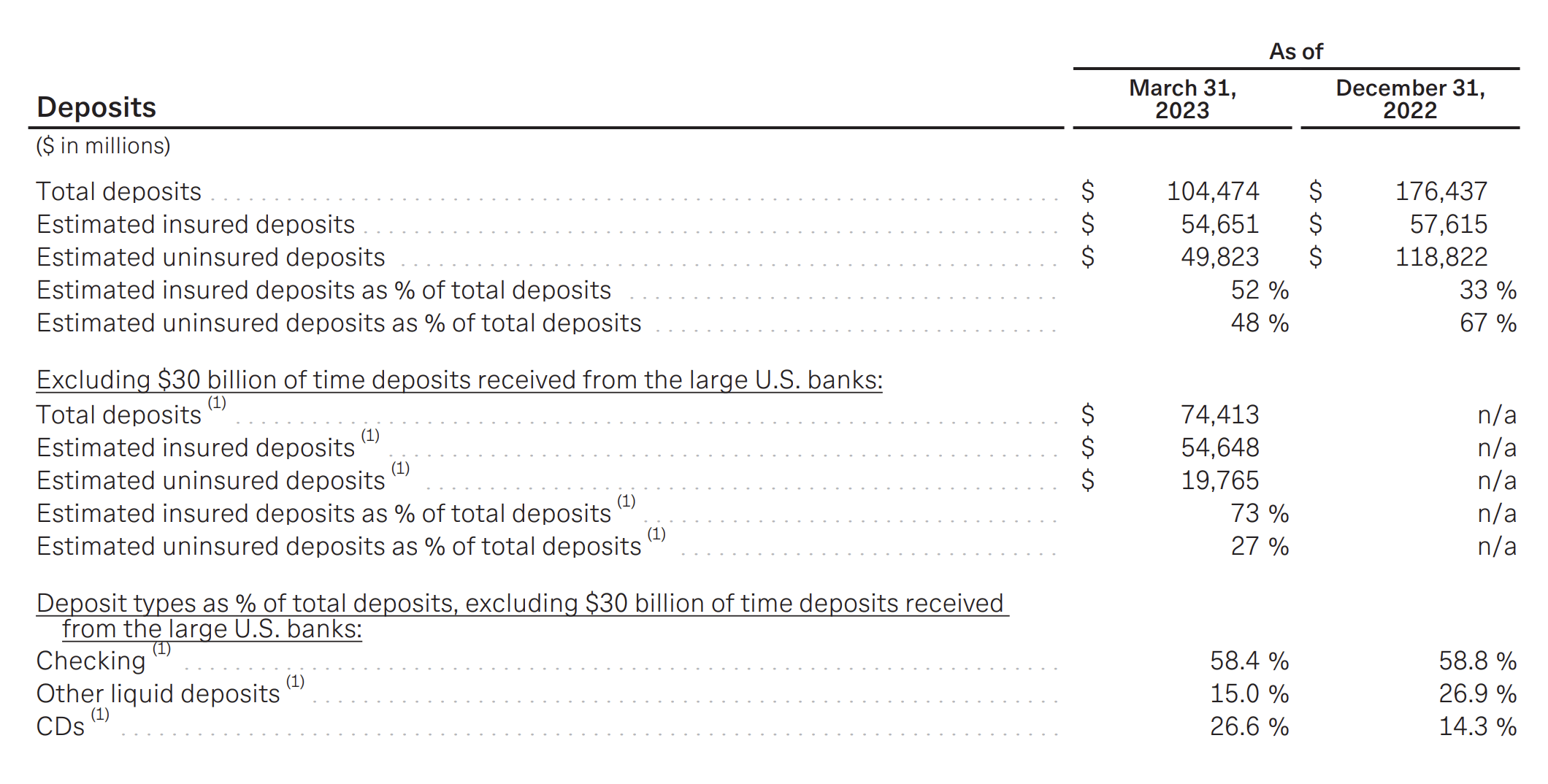

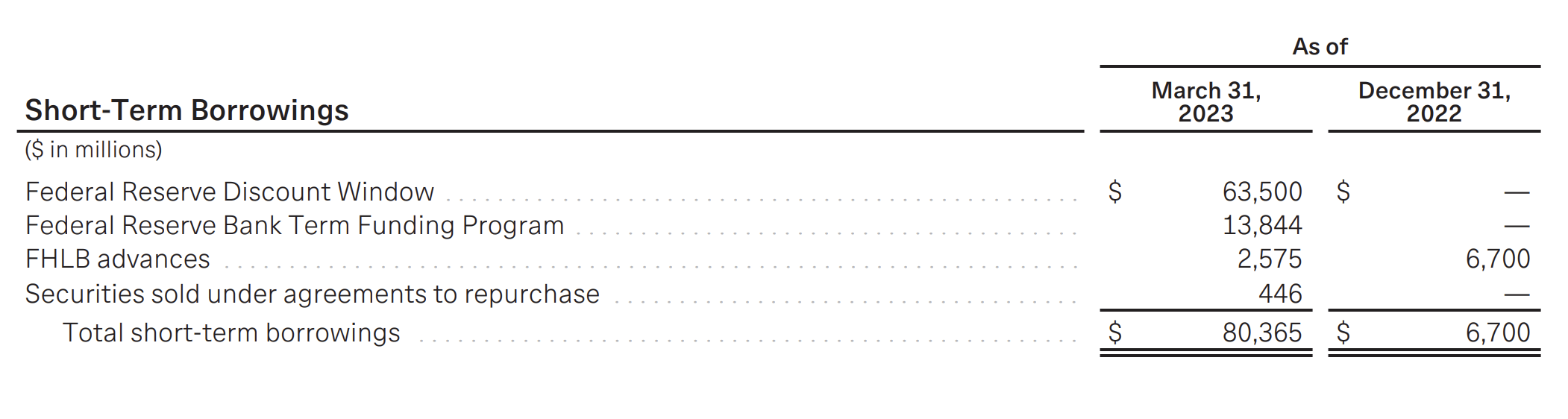

The pain, then, really boils down to how the assets and liabilities on the company's books have changed over the past quarter. Although total assets for the company grew from $206.10 billion at the end of last year to $218.58 billion at the end of the most recent quarter, actual deposits for the company plunged, falling from $176.44 billion at the end of last year to $106.67 billion by the end of the first quarter. That's a decline of 39.5%, or $69.8 billion. How can deposits fall by so much and yet overall assets increase? The answer boils down to support that the company has received from outside sources. By the end of the most recent quarter, the company had short-term borrowings from various federal sources totaling $80.37 billion. This compares to just $6.70 billion in borrowings that the company had one quarter earlier. The largest chunk, $63.50 billion, comes from the Federal Reserve Discount Window, with the rest coming from the Federal Reserve Bank Term Funding Program, FHLB advances, and Parities sold under agreements to repurchase.

{kind=link}

There are two problems that come with these borrowings. First and foremost, they are, by nature, short term. At some point, the company needs to raise the capital needed to repay these amounts. This can take on the form of new deposits coming in. It can take the form of the company selling off certain assets. Or it can take on other forms or a combination of forms. One option would be for the company to try and raise longer term capital or equity capital. But in this environment and in these circumstances, the probability of that is next to zero. At the end of the day, the company is almost certain to have to sell off assets. In fact, management said that they are exploring asset sales of up to $100 billion. This would mean that many of the loans on its books will need to be divested of, depriving shareholders of a future revenue stream.

{kind=link}

As to the final outcome of this, it ultimately depends on what kind of haircut, if any, the company needs to take on these assets. The fact that it does have support from regulators and other market participants means that, in theory, it might be able to sell off assets and experience little to no write-off. But we won't have any idea until management actually follows through with the process. We do know that the company doesn't have a great deal of wiggle room on this front. After all, the book value of equity for the enterprise currently stands at $17.99 billion. Selling off $100 billion of assets at, say, a 5% write down, would wipe out nearly 28% of the company's book value.

Even if the company was in a position to keep the borrowings that are on its books, the end result would be significantly more pain for shareholders in the long run. For the first quarter of this year, the effective yield that the company generated on all interest earning assets was 3.66%. That was up from 3.51% reported only one quarter earlier. And it compared favorably to the 2.78% experienced the first quarter of last year. However, the interest rate spread for the company was only 0.93% compared to the 2.59% reported one year earlier. These numbers were based on a weighted average of all assets and liabilities throughout the quarter. But as the quarter neared its end, high-cost borrowings became more plentiful on the company's books. According to one estimate I made, even keeping its balance sheet as it was at the end of the most recent quarter and assuming that all applicable interest rates apply, the company would actually see its effective net interest income drop to around $393 million per quarter as opposed to the $923 million actually experienced during the quarter. That would easily wipe out any profits that the company is generating.

To make matters worse, the deposit situation for the company actually looks worse than it does at first glance. As I reported in a prior article , the company received $30 billion in uninsured deposits from a consortium of the largest banks in the country. Those are only available to it for a period of time. Without factoring in these deposits, the total deposits at the bank would have fallen by $102.02 billion over the course of one quarter. The good news, I suppose, is that only about 27% of these deposits, excluding the $30 billion I mentioned, are still classified as uninsured. That does limit how much additional outflow the company could realistically expect should the market panic again.

Takeaway

At this point in time, I am treating First Republic Bank as an incredibly binary situation. In theory, if management can sell off roughly $100 billion in assets in order to cover its borrowings, and do so without taking a massive haircut on them, it could very well survive this downturn in decent shape. Yes, revenue and profits moving forward would be substantially lower than they were previously. But the company would still be trading at a significant discount to its book value per share. It likely would take years in order for the enterprise to get back up to the size that it was previously as well. If that is even something that's possible at all. But upside in this scenario could still be attractive. To prepare for this, management has already started planning a 20% to 25% workforce reduction. But what ultimately will matter most will be the haircut on asset sales if there is one.

Generally, I encourage investors to stay away from binary opportunities when it comes to funds that are important for their future. But I'm not necessarily against allocating a speculative piece of a portfolio that you can afford to lose toward such an outcome. That is what I did just before earnings came out for the company by buying some July 2024 call options. But the amount allocated was less than 1.5% of my overall portfolio. As for what you should do, I believe the answer should come back to what you believe management, regulators, and other parties can achieve in terms of the aforementioned asset sales. Because at the end of the day, that would determine the fate of the enterprise.

For further details see:

A Look At First Republic Bank's Death Spiral