T - A Lousy Tape Demands A Shopping List

2023-10-04 12:47:31 ET

Summary

- Down markets spawn the next set of winners.

- When the tape is lousy, creating a shopping list of stocks to buy is a lot more constructive than tracking portfolio drawdown.

- The article provides a short list of six stocks I believe warrant further due diligence: including Bank of America, Alaska Air Group, Dominion Energy, Realty Income, AT&T, and Skyworks Solutions.

- Each stock includes a three-point investment thesis, several key metrics, recent management commentary, my remarks, and a FAST graph valuation chart.

- I look forward to your opinions and additional data points in the comment section.

The Current Tape Stinks

Market averages are getting pounded. Seems like one of those times when stocks seem to go down every day. There's nowhere to hide.

Fed tightening cycles have the propensity to bring out the worst in the equities market.

Sell everything? No.

Unlike 2008, there is no systemic risk to the U.S. financial apparatus in my view.

No, there's plenty of fear and handwringing, but in reality, the underlying issue is just garden-variety Fed tightening and resultant interest rates. Beneath those fears are a looming recession due to the Fed keeping short rates "higher for longer," thereby scuttling the economy: no "soft landing."

I don't know when the current tightening cycle will end, nor the outcome of short rates on long rates and the economy. Frankly, that doesn't much matter to my investing strategy, anyway. I don't believe it possible to time the market consistently, and I don't try.

During times like this, I prefer to create a shopping list.

Why?

First, it's a lot more productive than sitting around worrying about your portfolio balance.

Second, tight money and higher interest rates are not "forever" conditions. Therefore, it's not too early to do some constructive back-and-filling and / or selective accumulation of specific stocks.

A shopping list is a short list of tickers that one would like to consider buying as prices fall. (You know, as prices fall, stocks do get cheaper).

It is important to be patient, then buy only in increments. No one can know for sure when the bottom is in. However, armed with an investment thesis, adequate due diligence, and at long-term outlook, there's often good money to be made.

My Shopping List

I offer readers my personal Quick Six short list, including a three-point investment thesis and FAST Graph for each stock. I already own shares in all these companies but believe now is the time to slowly accumulate more.

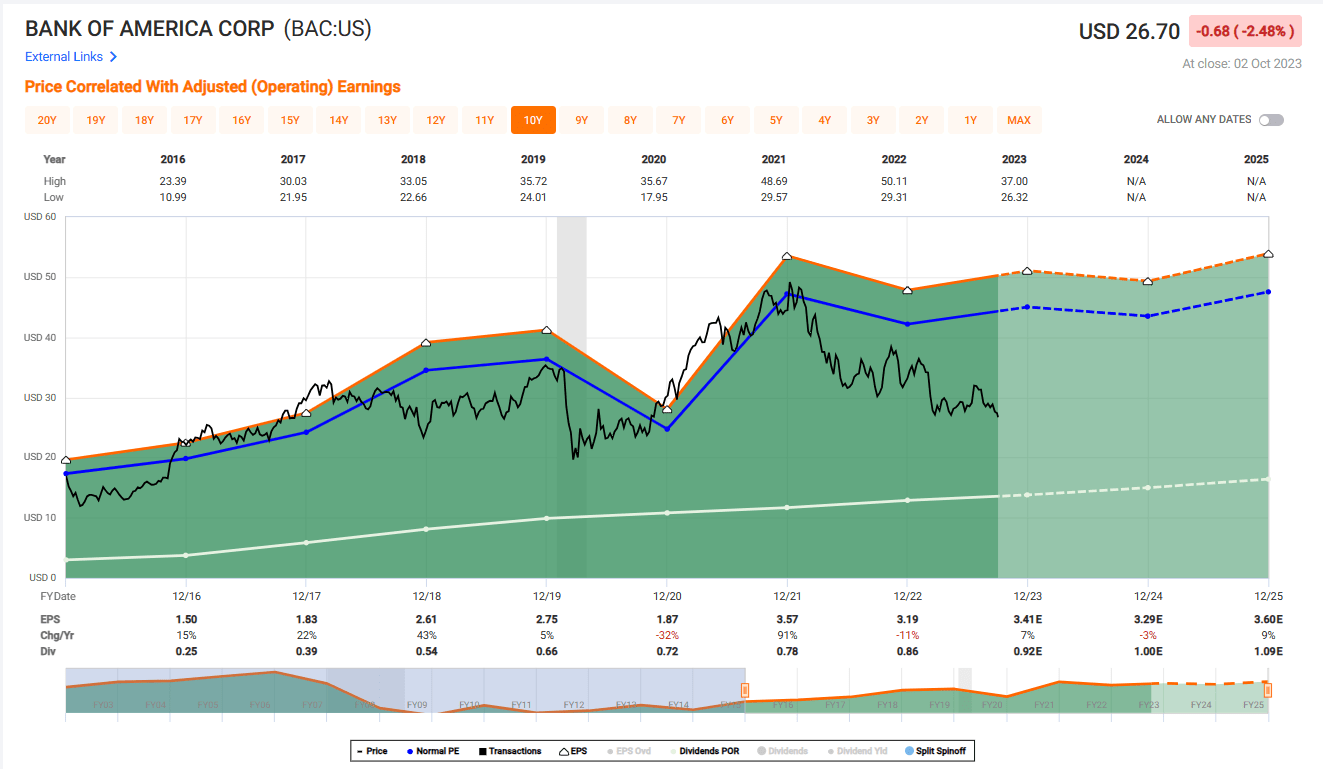

Bank of America

Bank of America ( BAC ) is one of the largest banking institutions in the world.

S&P Credit Rating: A-

Trailing P/E: 7.4x

Forward P/E: 7.9x

Dividend Yield: 3.71%

Investment Thesis

-

Well-managed, diversified, TBTF bank

-

Historically, banks are one of the first industry sectors to turn around after economic contractions

-

Stock is cheap on P/E and P/B

Recent Management Commentary

CFO Alastair Borthwick at Bank of America Corporation Securities 28th Annual Financials CEO Conference -- 9/20/23

Well, I think simply, our bank has four of the great banking franchises of the United States and of the world. Our wealth franchise is excellent. Our consumer bank is world leading. We have a world-leading investment banking practice and sales & trading practice. Those four franchises individually are hard to create. Putting all four together is very, very, very difficult today. And for long-term holders, I think we're on sale relatively.

My commentary

One of my largest single positions, I don't mind when BAC shares "come in." Bank of America is well-managed, well-capitalized, and maintains strong asset quality. Based upon a 13x P/E or 1.2x P/B, I value common shares between $40 and $43. I like the current 3.7% dividend yield, too. The historical P/E is 13.2x. Primary risks include a deep, protracted recession and / or enactment of proposals for materially higher regulatory capital requirements.

{kind=link}

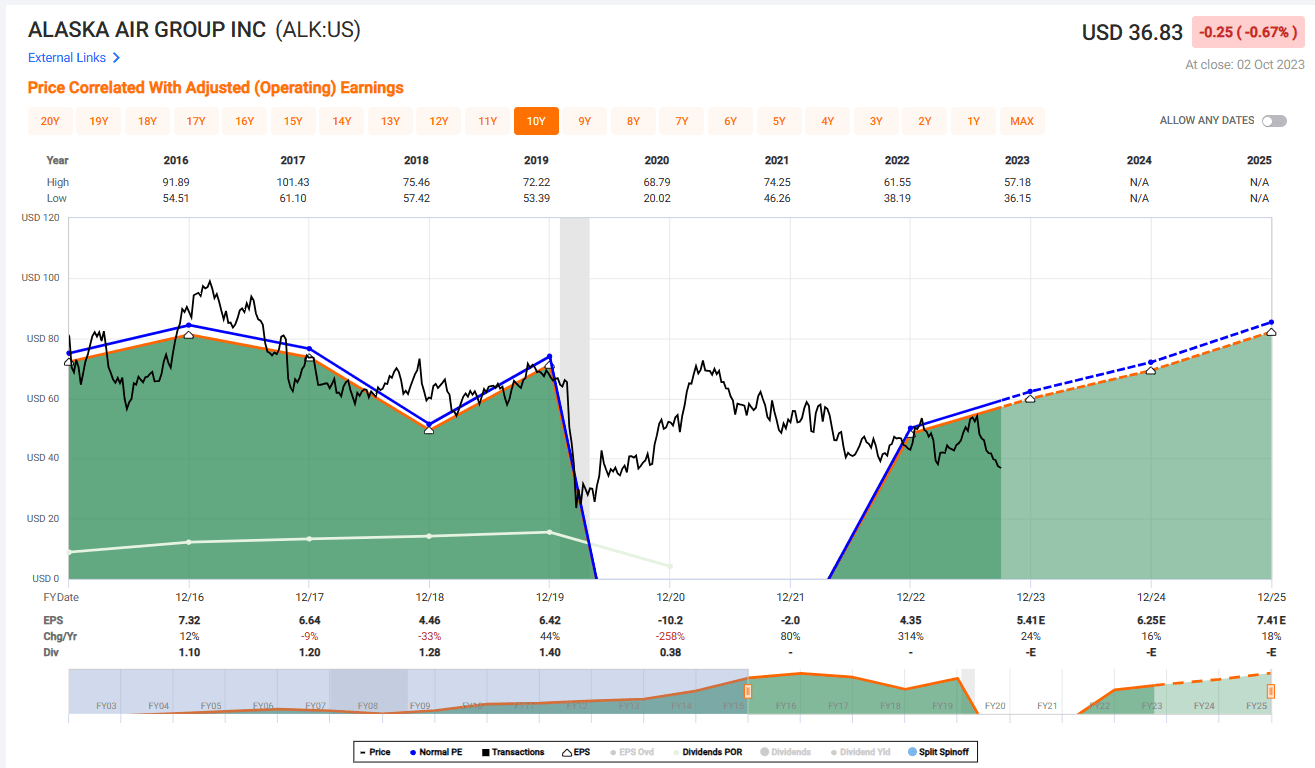

Alaska Air Group

Alaska Air Group ( ALK ) is the sixth largest commercial passenger airline in the United States.

S&P Credit Rating: BB

Trailing P/E: 6.1x

Forward P/E: 5.7x

Dividend Yield: nil

Investment Thesis

-

Solid balance sheet; net debt near zero and best pre-tax margins in the industry

-

Combines a low-cost business model, excellent customer service, and strong management

-

Current valuation reflects excessive multiple compression. Mr. Market is too pessimistic.

Recent Management Commentary

Updated management guidance -- 9/6/23

The carrier said it expects Q3 revenue to be up 1% to 2% vs. +0% to +3% prior range and capacity to rise 13% vs. the prior forecast for +10% to +13%.

Alaska Air said operations continue to perform at an exceptionally high level and throughout the peak summer period. The completion rate was noted to have reached record levels during July and August. ALK also highlighted that it executed a market wage rate adjustment for pilots, effective September 1, as part of the agreement originally reached in October of last year. Inclusive of that impact, ALK revised its Q3 CASMex guide to the better end of the range of down 1% to 2%.

My Commentary

Alaska Air stock has fallen precipitously: it's been down for eleven straight weeks, sitting near a three-year low.

Nonetheless, as late as a month ago, management had not called out a significant downturn in the business. Guidance was tightened. Investors appear to be in panic mode. Indeed, given the nature of Alaska Air's passenger airline business, there is risk: primarily, escalating fuel costs and a business model that caters to leisure air passengers. However, I believe the risk / reward is asymmetric at these levels. Applying an 11x P/E to 2024 EPS, my FVE is $65 to $70. The historical P/E is 11.5x.

{kind=link}

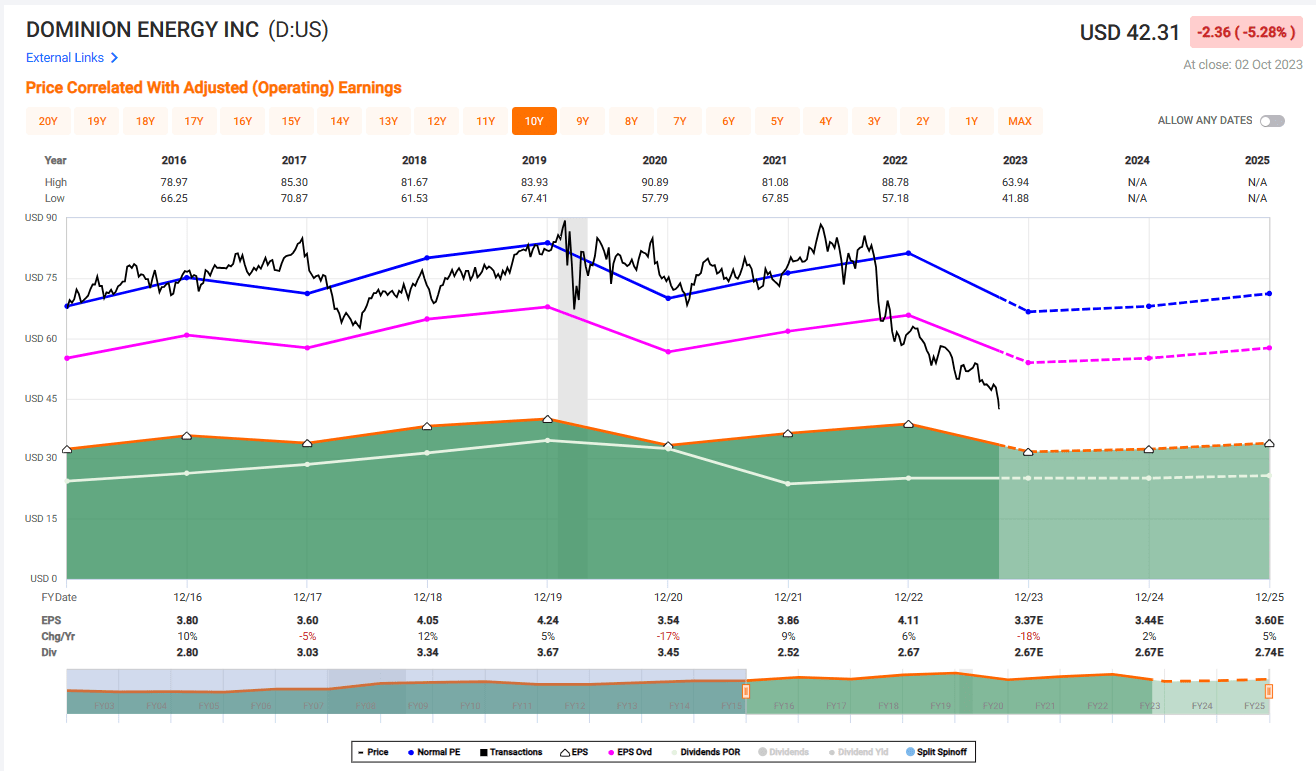

Dominion Energy

Dominion ( D ) is producer and distributor of regulated electric power operating primarily in Virginia, North Carolina, and South Carolina.

S&P Credit Rating: BBB+

Trailing P/E: 11.9x

Forward P/E: 12.3x

Dividend Yield: 6.31%

Investment Thesis

-

New business model is a forward catalyst

-

Operations are located in one of the best growth regions in the U.S.

-

Recent utility sector selloff is overdone; particularly Dominion Energy

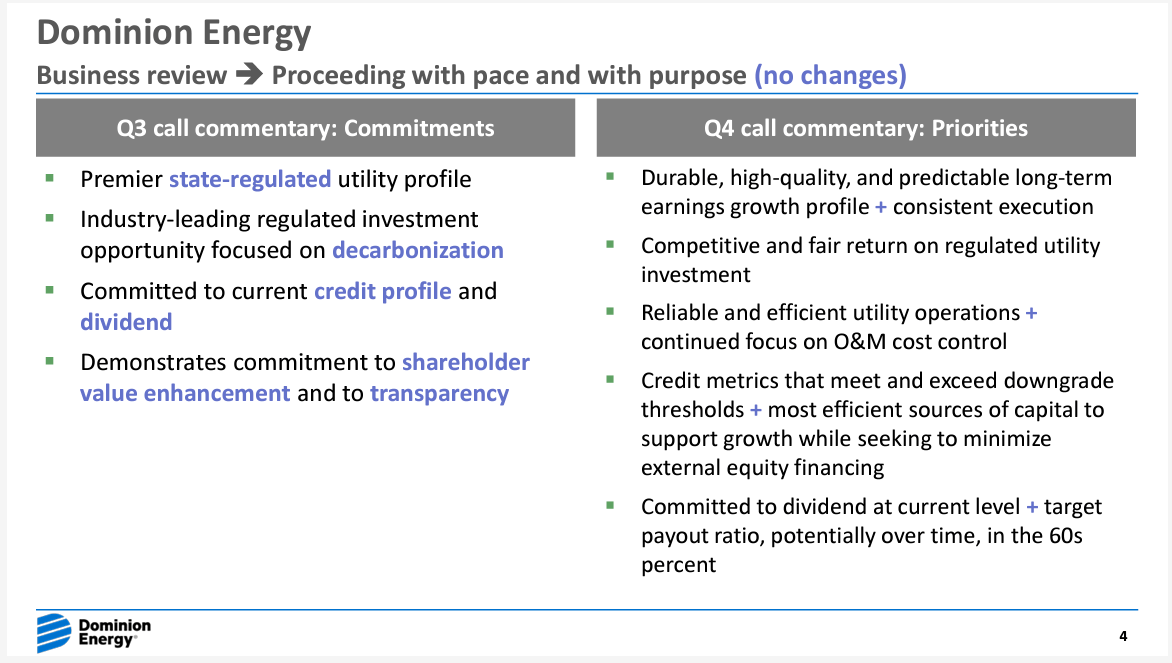

Recent Management Commentary

The company is engaging in a "top-to-bottom" business / strategy review. The following slide from the August 3, 2023 quarterly earnings presentation highlights the general themes:

{kind=link}

My Commentary

Despite being a regulated utility, Dominion Energy may be my most controversial pick. In recent weeks, utility stocks have been obliterated and Dominion is no exception. Interest rate fears, including their impact upon refinancing costs and dividend yields versus T-bonds are pressuring the entire sector. Adding to the uncertainty, Dominion management is embarking upon a company overhaul: selling natural gas assets to raise cash and strengthen the balance sheet, focusing upon regulated electric power, reducing the company' footprint, and undertaking construction of a large U.S. offshore windfarm. Based upon a 16x P/E, I contend Dominion common shares are worth ~$55 each. I recommend buying in small increments until management provides a much-anticipated 4Q business update, including the go-forward status of the dividend.

{kind=link}

Note: The pink line on the chart represents a 16x P/E ratio. This is about 4 turns less than the current 19.8x historical average. (The blue line)

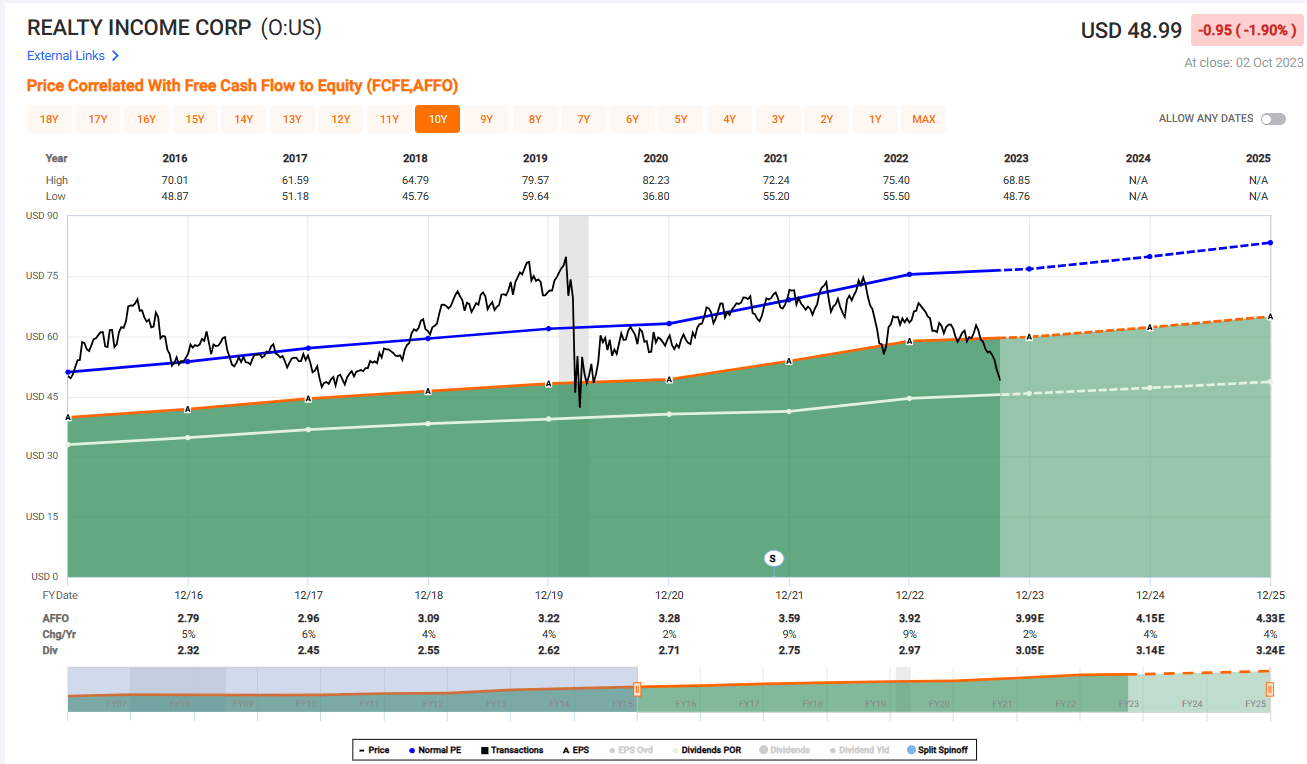

Realty Income

Realty Income Corporation ( O ) is a real estate investment trust. The Company is engaged in acquiring and managing single-unit freestanding commercial properties under triple-net long-term lease agreements.

S&P Credit Rating: A-

Trailing P/AFFO: 12.2x

Dividend Yield: 6.28%

Investment Thesis

-

Excellent management

-

Steady, safe, increasing dividends built upon a 3N real estate leasing model

-

Historically low valuation / high dividend yield

Recent Management Commentary

President and CEO Sumit Roy at Realty Income Corporation Q2 2023 Earnings Call Transcript -- 8/3/23

Delivering stable and consistent growth is foundational to our mission at Realty Income. Underlying this growth, our team continues to source and invest in high-quality properties at accretive spreads to our cost of capital while partnering with our clients who are leaders in nondiscretionary, low-price point and service-oriented industries. Partnering with industry leaders across over 13,000 properties in a diversified real estate portfolio offers us durability of cash flows that results in the predictable nature of our revenues, earnings and dividend payments.

Our investment activities remain robust as we continue to demonstrate that size and scale are unique advantages in the sale-leaseback and portfolio transaction markets. Cap rates in our acquisitions appear to have stabilized after a meaningful adjustment period to a higher interest rate environment.

My Commentary

Rarely do we find premier companies trading at such compelling valuations. Over the past year or so, Realty Income stock has fallen 35 percent. Meanwhile, the dividend yield is the highest in at least ten years. Realty Income is a Dividend Aristocrat .

Realty's triple-net lease structure, diversification, defensive-business lessees, outstanding balance sheet, and previous track record through the cycle, indicate rising rates are not a major risk. Currently, some REITs are rightly under pressure. Realty Income is not an ordinary REIT. Risks include a full-on real estate collapse and / or long-term skyrocketing interest rates. Based upon 17x AFFO and recent management guidance, I place a target price of $65 to $69 on the shares. The historical P/AFFO is 19.3x.

For an excellent perspective on Realty Income, I encourage you to read a recent S.A. article by fellow-contributor Brad Thomas. The link to that article is found here .

{kind=link}

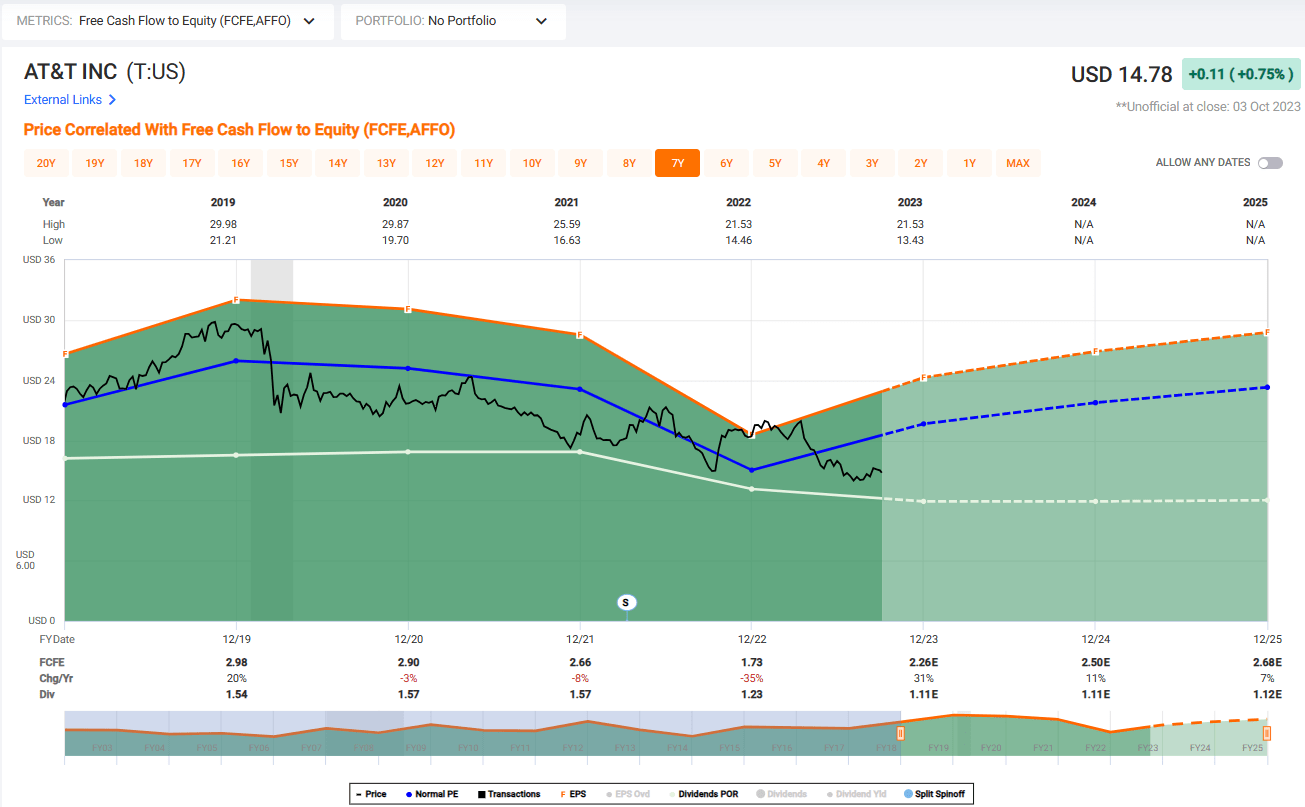

AT&T Inc

AT&T ( T ) is an integrated telecommunications company.

S&P Credit Rating: BBB

Trailing P/E: 6.0x

Forward P/E: 5.9x

Dividend Yield: 7.51%

Investment Thesis

-

Changed management

-

Excellent free cash flow

-

Mis-aligned investor sentiment

Recent Management Commentary

CFO Pascal Desroches at Bank of America Securities Media, Communications and Entertainment Conference -- 9/14/23

Look, first -- remember, the first half of the year, you had a peak level of device spend, we had peak levels of capital and we had our annual compensation. If you normalize for those items, you can really get a sense for why we are so confident about the back part of the year. We said at the very start of the year, first quarter was going to be the lowest followed by second quarter, followed by third quarter, and fourth quarter. It is playing out exactly as we thought. [Reference to management's 2023 guidance to generate $16 billion free cash flow.]

Here's what we have said, and we've been very clear about. We expect over time to get to a mid-teen's capital intensity. That's what we've said. And John has been very clear about that, that we are at peak levels in 2022 and 2023, that we will -- as we exit 2023, you will begin to see moderation in our cash and with the goal of getting to mid-teens.

My Commentary

In recent times, AT&T has turned over most of its senior management, a majority of the board of directors, and re-tooled the corporate strategy. Yet, some investors cling to the notion AT&T is the same company as it was under ex-CEO Randall Stephenson. It's not. AT&T is now focused upon wireless telecommunication service / equipment, and ethernet-based fiber services. The streamlined company has the propensity to generate significant, sustainable cash flow. Free cash flow should improve further as beginning in 2024 the company enters a period of moderating capital requirements. The dividend and current 7.5% yield are secure. Risks include a telecommunications price war. Based upon a modest 9x P/FCF ratio, my Fair Value Estimate is $20 to $22. The historical P/FCF is 8.7x.

{kind=link}

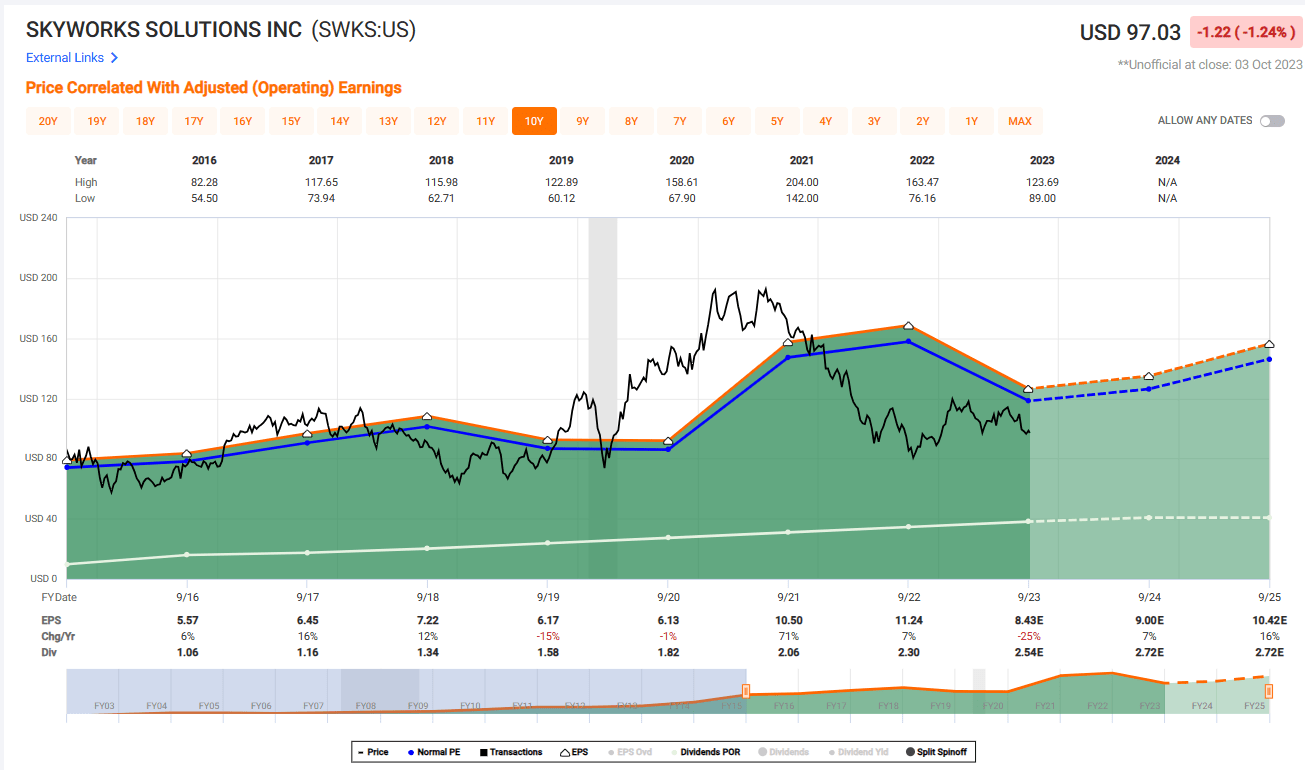

Skyworks Solutions Inc

Skyworks Solutions, Inc. ( SWKS ) is engaged in designing, manufacturing, and marketing analog semiconductor products, including intellectual property. The Company's largest customer is Apple, Inc. ( AAPL )

S&P Credit Rating: --

Trailing P/E: 10.4x

Forward P/E: 10.8x

Dividend Yield: 2.80%

Investment Thesis

-

Strong, experienced management

-

The semiconductor industry has a long runway; Skyworks is a niche player with a durable relationship with Apple

-

The stock offers GARP (growth at reasonable price) and is an outstanding dividend growth company (over the past five years, 15% average annualized increase)

Recent Management Commentary

CEO Liam Griffin at Skyworks Solutions, Inc. Q3 2023 Earnings Call -- 08/07/23

In mobile and IoT, we secured 5G content for Android smartphones across all tiers.

Across infrastructure and industrial, we enabled 5G small cell deployments with a top North American operator and ramped timing solutions for AI data centers at a leading cloud provider.

In automotive, we continue to post double-digit year-over-year revenue growth while capturing design for telematics applications across a broad range of manufacturers.

Additionally, several disruptive market trends are now unleashing new meaningful growth opportunities for Skyworks. For example, generative AI is proliferating on a global scale with rapid adoption, sparking exponential growth in the amount of data accessed from the network edge to the cloud. In turn, this will further drive complexity in wireless infrastructure networks as AI will require higher throughput, more secure connections, lower latency and improved power management.

Skyworks is uniquely positioned to benefit from these trends with our advanced integrated solutions, supporting wireless infrastructure, cellular connectivity for mobile devices as well as other leading wireless protocols used in billions of IoT products.

My Commentary

This mid-cap stock is one of my favorite "sleepers." This chip company doesn't get the attention of some peers; however, management is very good at cash generation. Skyworks is one of a small subset of corporations that consistently generate more cash flow than earnings. The company is an industry leader within its niche and enjoys high margins. The balance sheet is outstanding: net debt to equity is just 16 percent. Risks include a loss of primary client Apple (comprising about 64% of Skyworks' revenue), and / or a sustained, deep recession. The loss of Apple's business is unlikely in my opinion. The stock is inexpensive: based upon 14x EPS, my current target price is $126 to $130. The historical P/E is 14.0x.

{kind=link}

Conclusion

Bad markets spawn future winners. When the tape reads rough, get to working on a shopping list.

This article highlights six candidates I believe warrant further due diligence and evaluation.

Accumulate stocks slowly and incrementally. Keep a sharp eye on future developments. Review and update the investment thesis, as necessary, after subsequent earnings releases.

Focus upon value, not price.

I look forward to your comments and opinions in the comment section.

Please do your own careful due diligence before making any investment decision. This article is not a recommendation to buy or sell any stock. Good luck with all your 2023 investments.

For further details see:

A Lousy Tape Demands A Shopping List