AMRK - A-Mark: Highly Profitable Downstream Precious Metals Play With Confined Growth Opportunities

2023-11-24 04:13:24 ET

Summary

- Investors are flocking to precious metals amid macroeconomic and geopolitical unsettlement.

- A position in precious metals has historically been beneficial for astute investors.

- A-Mark Precious Metals provides insulated exposure to the precious metals market and has strong financial performance, but there may be more selective opportunities for capital appreciation elsewhere.

Investment briefing

The case for allocating a section of portfolio risk to precious metals is growing by the day. Investors have once again flocked to the asset class amid a wave of macroeconomic and geopolitical unsettlement.

The role of precious metals in any cross asset portfolio is highly debated. Some recommend up to 2% of net asset value weighted to gold (or a selection of metals). Many portray its inflation hedge properties. Others lip the 'store of value', and 'gold is money, all else is credit' lines. The majority of sophisticated managers hold some weighting for their clients. The point is a position towards precious metals hasn't let the astute investor down.

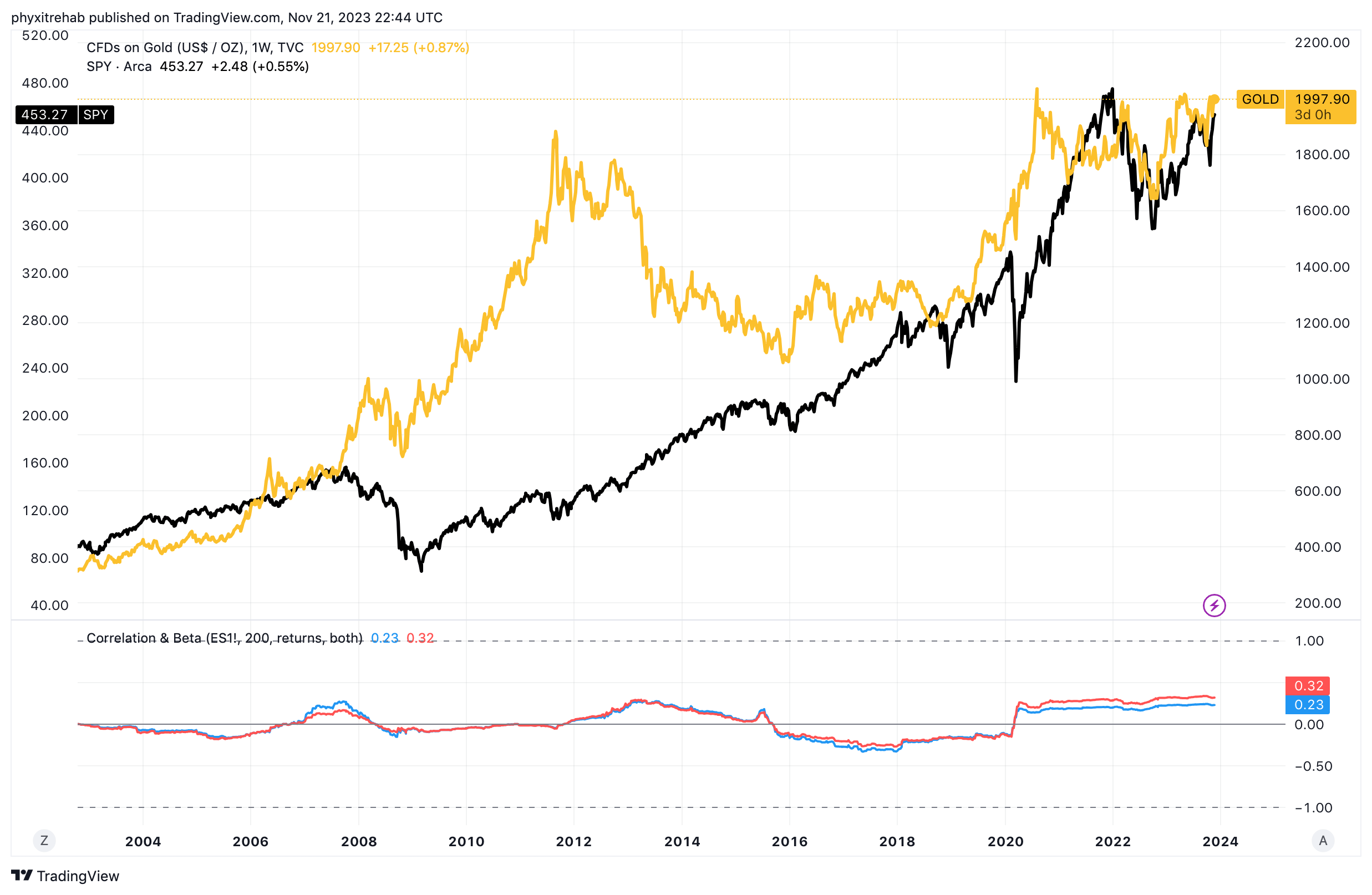

Long-term returns of gold (proxy for precious metals class) dating back to 2003, versus the SPY ( SPY ) are noteworthy (Figure 1). Since 2018, both investment classes have performed reasonably well, with minimal correlation, especially during and after the 'pandemic years'.

Figure 1. Long-term returns + historical beta for gold vs. SPY, 2003-2023

{kind=link}

It then becomes a question of what method of asset ownership one chooses for the exposure. The list to consider:

- Bullion itself

- Custodians who sell directly to you (similar to 1.)

- Precious metals futures/forwards

- Precious metals ETFs (physically backed, trusts)

- Downstream assets - such as listed investment + trading firms, jewellers, commercial suppliers, etc.

- Investment pools

- etc.

Unlike miners + producers, specialized finance + trading operators within the precious metals space are an insulated vehicle to gain or increase exposure on the strategic side.

These firms can unlock value in precious metals in a unique way, extracting cash flow from the transactional value, alongside investment + retail value.

A-Mark Precious Metals ( AMRK ) is one name that provides this insulated exposure for investors.

The company buys and sells investment-grade precious metals (gold, silver, platinum, palladium). It does this on the industrial side, the institutional investor side, and direct to consumer (retail). Its customers include financial institutions, commercial users, bullion dealers, and the general public.

At the current price of 4.8x next year's earnings and 10.5x forward EBIT, no price is being paid to own this high-quality precious metals trading company. Q1 revenues beat Wall Street estimates, and consensus forecasts 9-10% growth in sales in '24-'25. Business returns are exceptionally strong but rely on a high turnover of capital/inventory to remain there. Meanwhile, AMRK is throwing off reasonable sums of cash to its shareholders. The price of gold et al. is also holding value well in a difficult market. Its next direction of travel is crucial to names like AMRK's business model.

Despite a robust set of economics (inc. valuation), there are more selective opportunities to send capital off to work right now in my opinion. The fact that AMRK relies so heavily on capital turns to produce earnings is a red flag for my investment cortex. Any slowdown in the rate of business will cut through earnings given the <2% profit margins. Whilst profitability is high, the route to get there is not so valuable to me as a commodity product. Net-net, based on the balanced factors raised here today, I rate AMRK a hold but am constructive on the name.

Critical facts forming investment thesis

Culminating all of the available data, here is the investment facts pattern, argued below.

Starting with the positives

- Because AMRK holds precious metal bullion as its inventory, it faces price risk on these metals. It turns to the derivatives markets to hedge these away. The company's policy is to hedge the bulk of its inventory position using forward and futures contracts. It then books gains/losses on these as cost of sales. All will have a net cost given what's paid for the hedges in place. The reasons for these risk controls are abundantly clear, observed in Q1 '24.

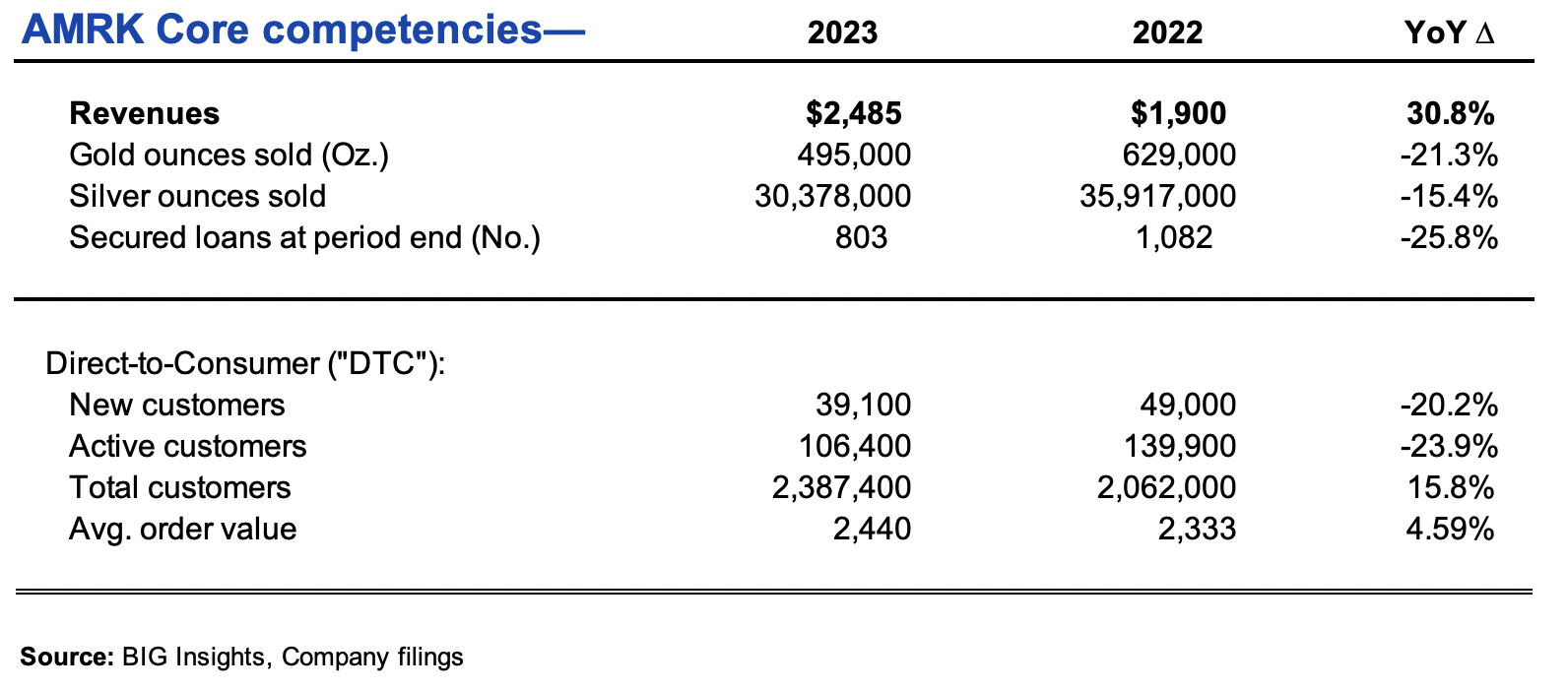

Revenue overview:

Revenues for Q1 '24 came to $2.485Bn, a substantial uptick of $584.3mm or 30.7% from $1.900Bn in 2022:But if you exclude the increase of $660.1mm booked from forward sales, revenues experienced a marginal decrease of $75.8mm or 5% . This is attributed to a reduction in gold and silver ounces sold (Figure 2).

Precious Metal Metrics:

-

Gold:

- Gold ounces sold for Q3 2023 decreased by 134,000 ounces, marking a 21.3% decline from 629,000 ounces in 2022.

- Average selling prices ("ASPs") for gold are in an upward trend, increasing by 10.2% YoY.

-

Silver:

- Silver ounces sold in Q3 2023 decreased by 5,539,000 ounces, a 15.4% decrease from 35,917,000 ounces in 2022.

- ASPs for silver gained by 14.7% during Q1 '24 compared to Q1 last year.

- Alternative statistics are more relevant for AMRK's core competencies than financials, given the price risk above. These are listed for Q1 FY'24 in Figure 2, along with YoY changes.

Figure 2.

{kind=link}

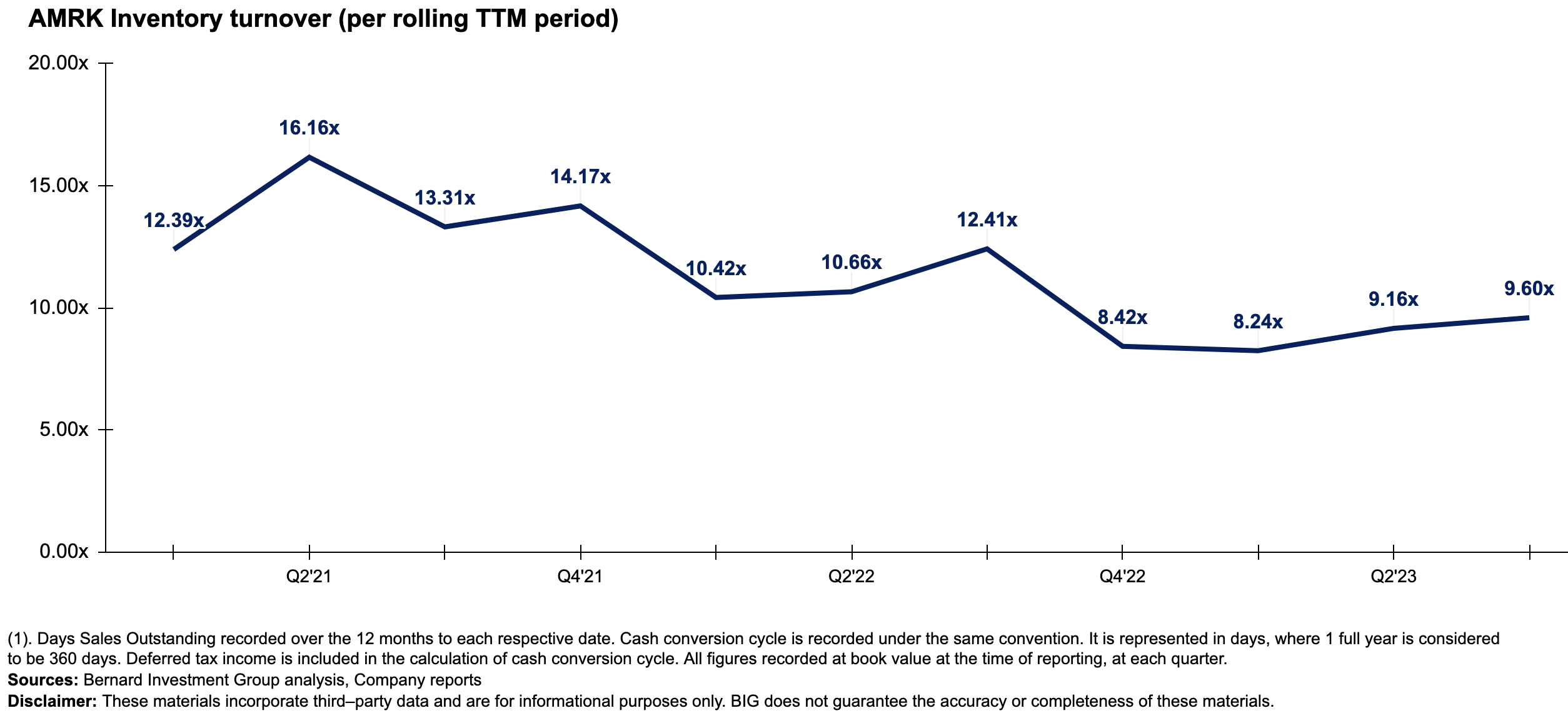

One statistic is inventory turnover. AMRK works through a great deal of bullion, turning over inventory assets >9x in the last 12 months. This is down from highs of 16x in 2021 but above lows last year. This is exceptionally high. Each $1 invested in NWC is therefore recycled back to cash in 37 days, flat with last year.

Figure 2a.

{kind=link}

- AMRK is in a challenging industry, but it is highly profitable. Those in the gold domain face difficulties differentiating between cost and product (it is all gold, prices set by the market). This is blatantly true in the bullion space. The company's business model acting as an intermediary does diversify this to an extent. Still, it is all capital turnover driving the profits for names like AMRK; who has the most productive assets, fastest sales turnover, and so forth. Capital required to run the business is light, and AMRK turns its investments over 12-17x each TTM period. Each $1 investment made to the business' assets returns $12-$17 in sales, a highly successful endeavour if the reinvestment runway is there. Because it can't differentiate on product or cost, post-tax margins are tremendously low, averaging below <2% since 2020. Precisely why it needs to sell ounces at such a high pace. The outcome of AMRK's internal economics is that it routinely produces outsized returns on capital employed in the business. From 2020-Q2 2023, it was a trailing 23-33% but has clamped this back to 17% last period.

Figure 3.

{kind=link}

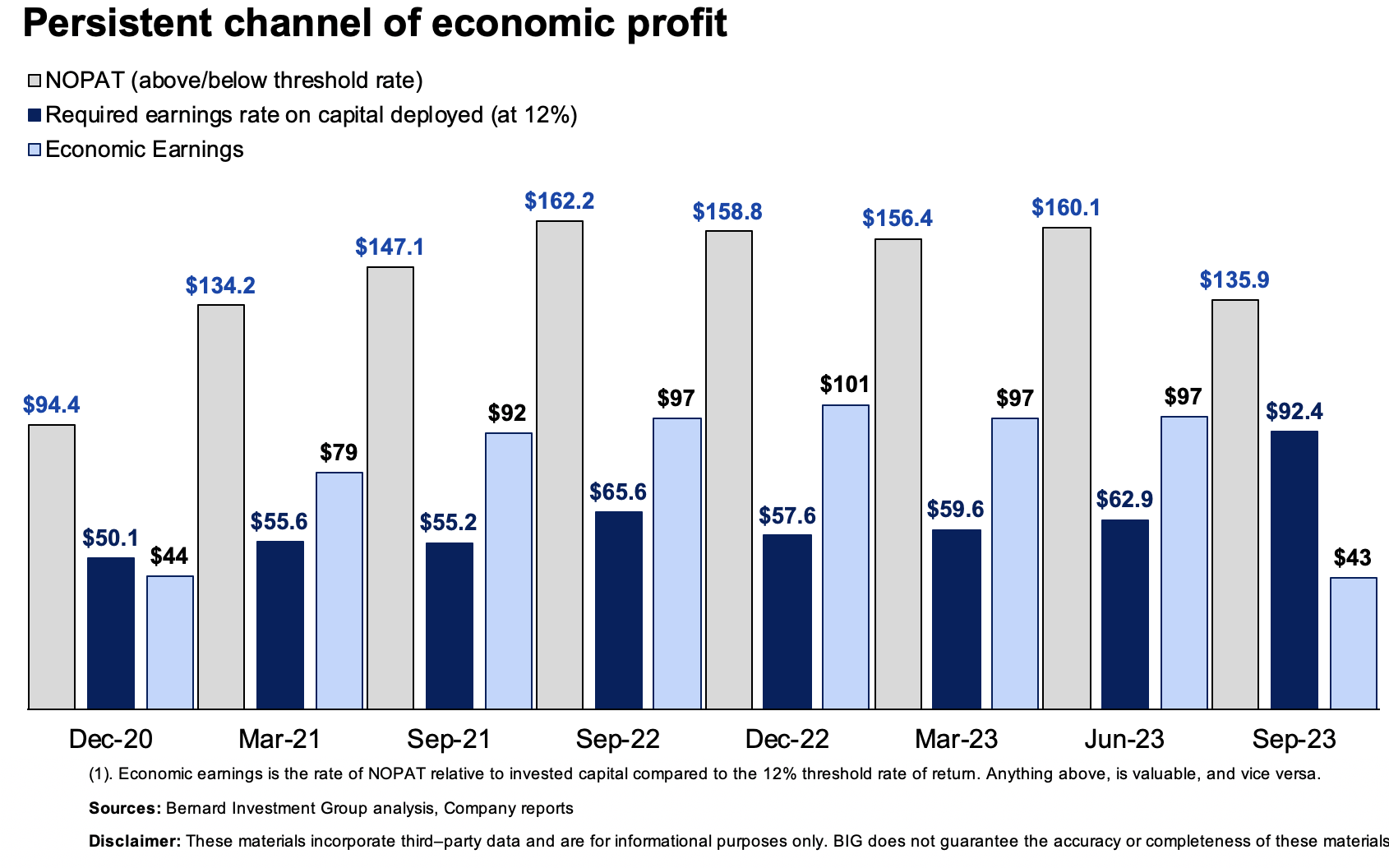

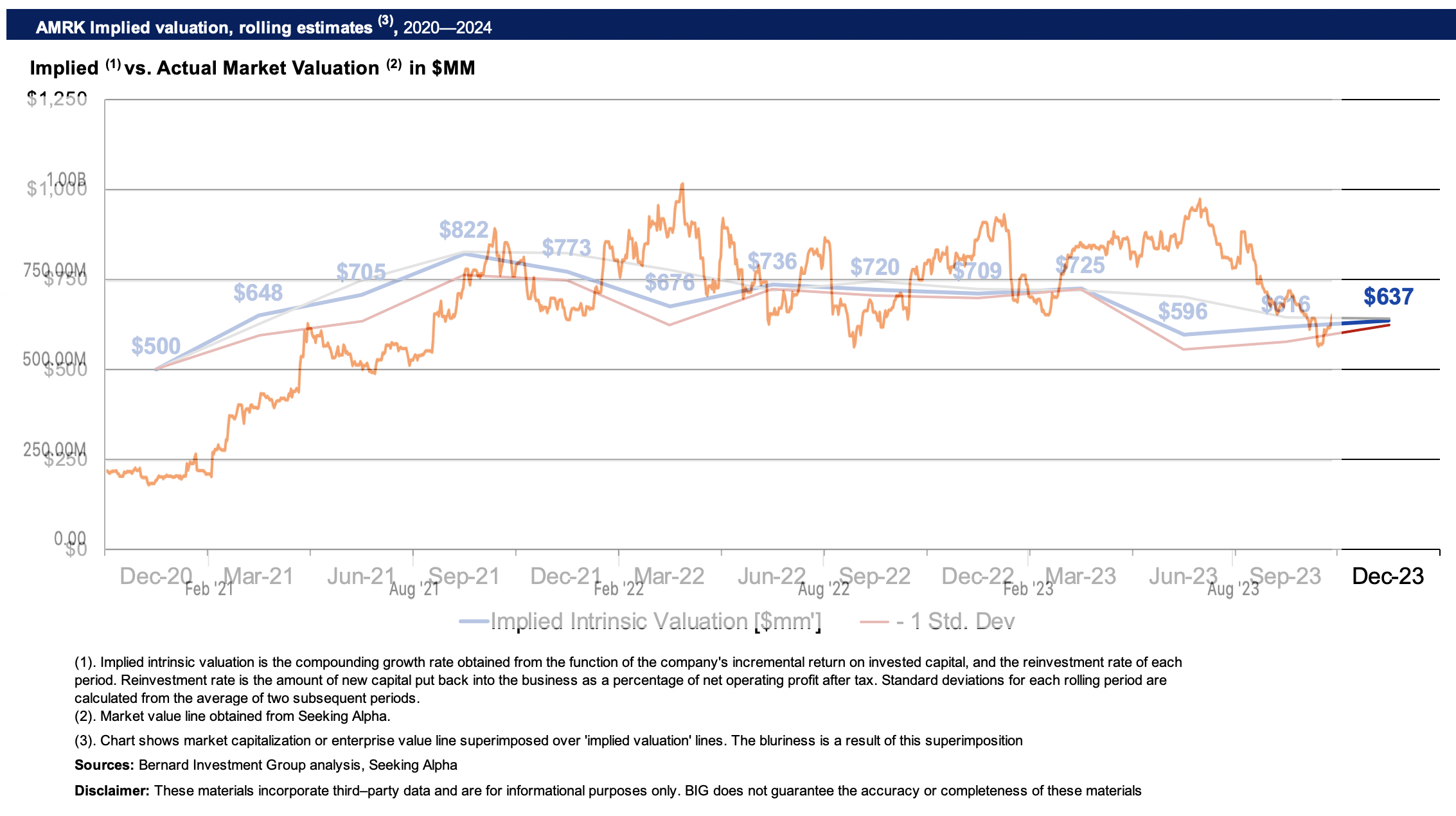

- Value extracted from these business returns is more relevant with context. The company's investments have routinely produced earnings at a rate above long-term market returns (avg. 12% here). As seen in Figure 4, the actual NOPAT (in grey) dwarfs the required NOPAT (dark blue) in regards to what is considered economically valuable (sky blue). AMRK has certainly created economic value for its shareholders since 2020.

Figure 4.

{kind=link}

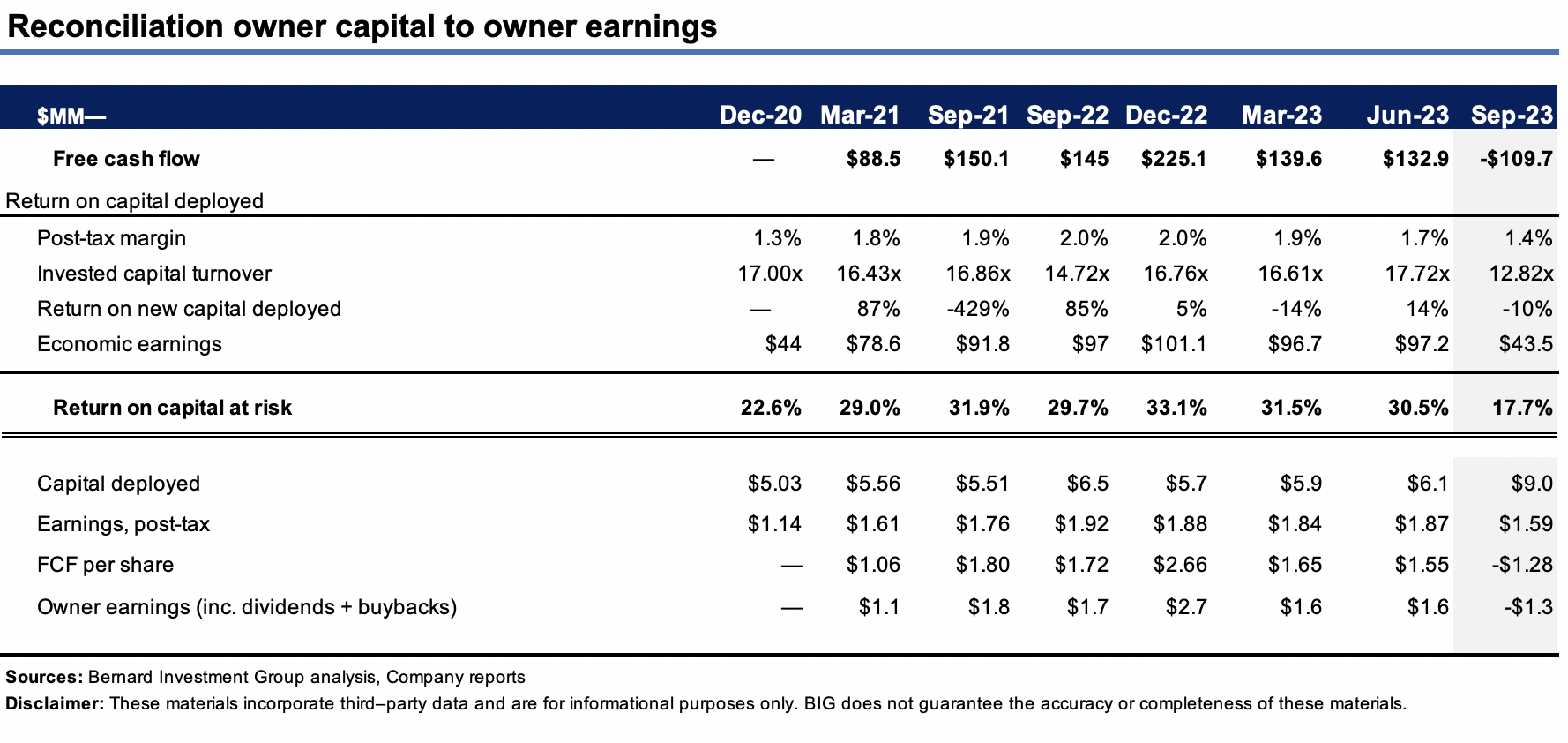

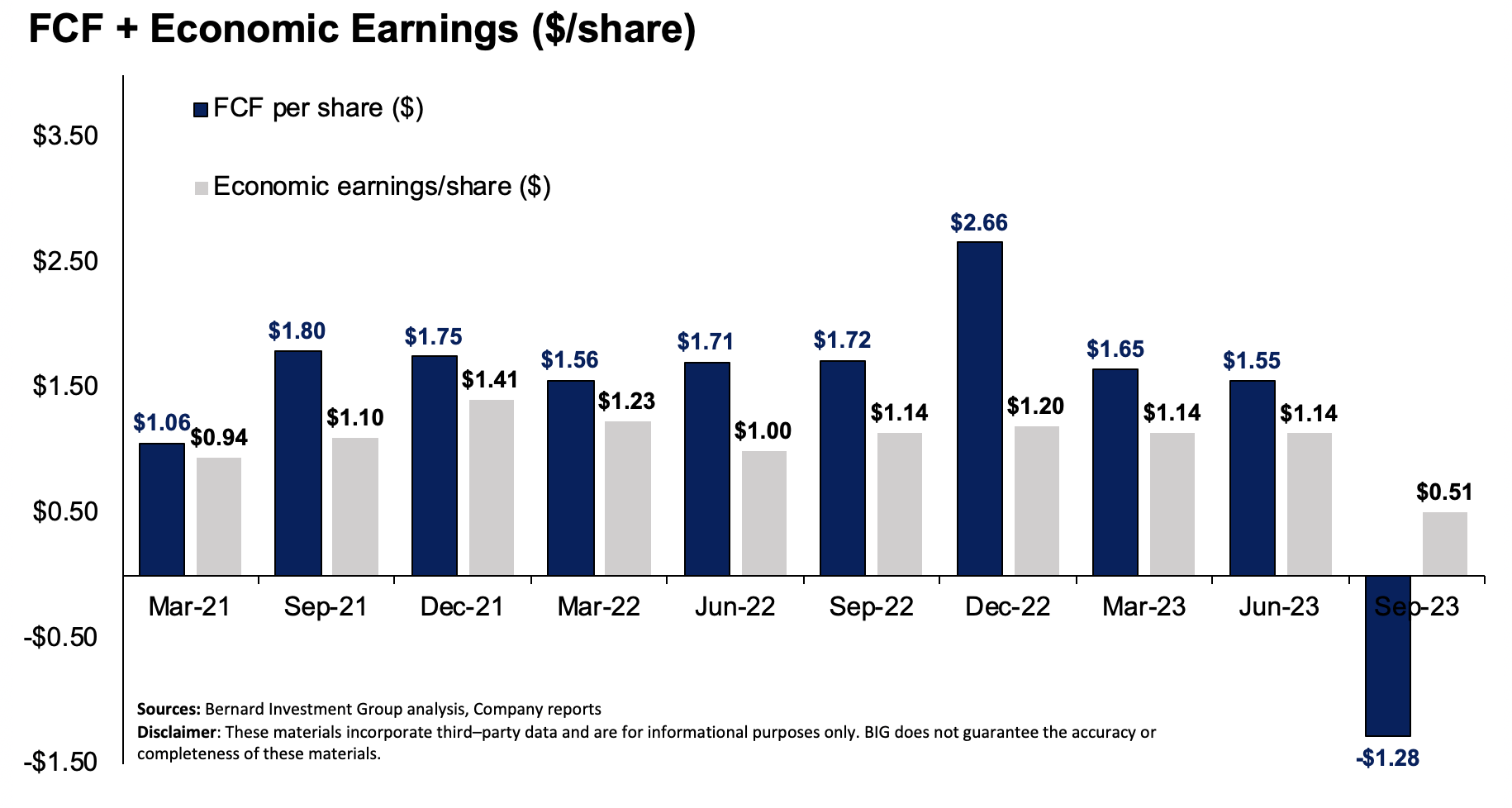

- Extending from the point above, to its credit, AMRK has produced $11.35 per share of economic earnings since 2020. Its share price has increased by ~$16/share in this time. It has also thrown off $14 in FCF per share over this time. With $4/share in dividends paid since Q4 2020, this gets you to $15.35-$18/share in direct value for shareholders. So there is fundamental support underneath AMRK's epic run across 2020-'21. This is a cash-rich company with excellent profit opportunities on its existing capital. We'd expect this from a firm with its roots established back in 1965- high returns on capital, throwing off cash to shareholders in FCF + dividends.

Figure 5.

{kind=link}

Moving to the Challenges

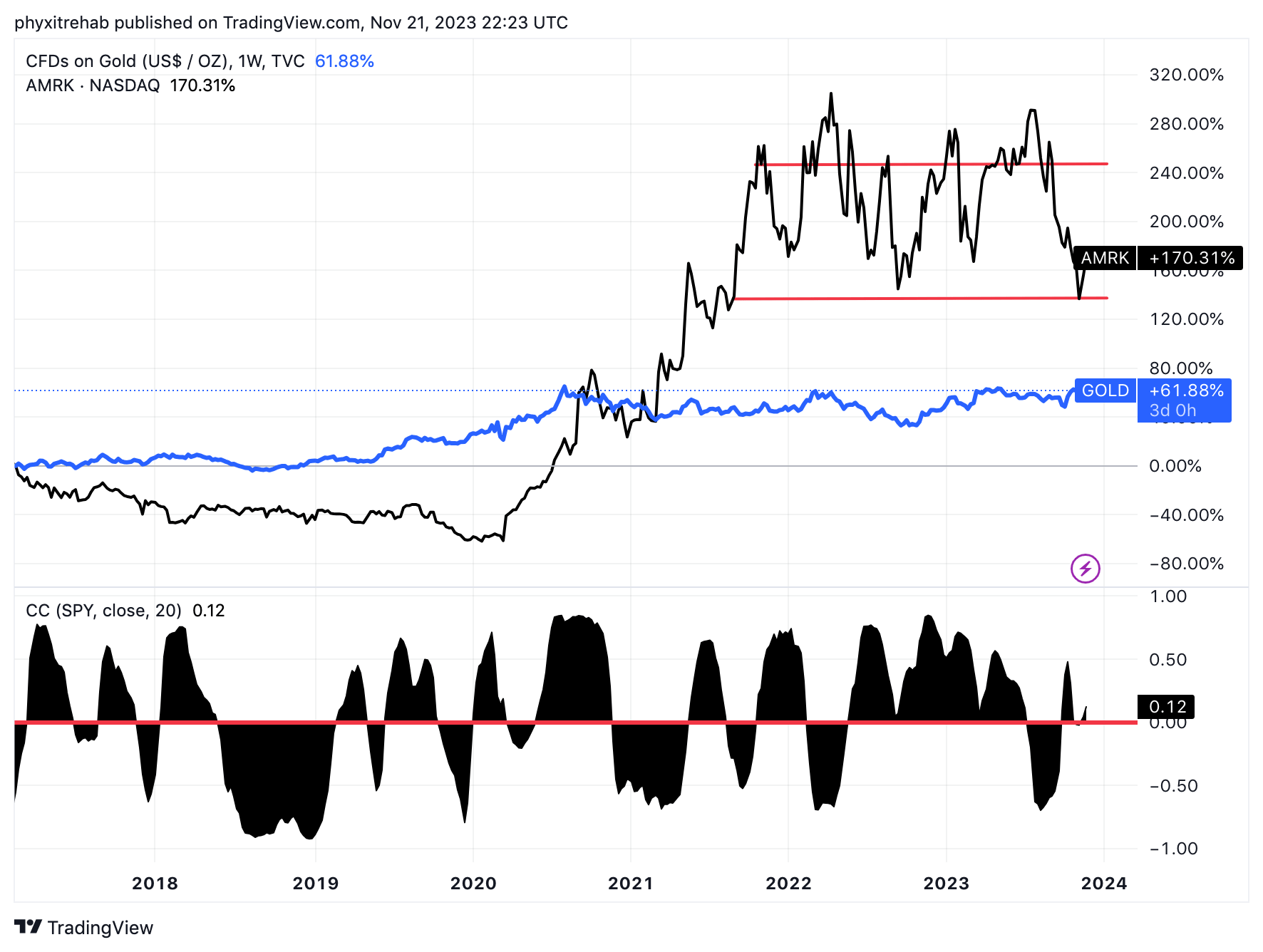

Despite the robust economics, it is hard not to believe AMRK's gargantuan run in early 2020-late 2021 was not beta-driven, at least in part. The firm's low-cost entry to owning yellow metal in an insulated way saw it compound returns at nearly 3x that of spot gold itself since 2018 (Figure 2). Again this proves the notion that alternative means of exposure have payoffs in the right market.

Figure 6.

{kind=link}

There are several negatives that balance the debate, and they are heavy.

One, AMRK's revenues are largely pervious to the underlying metals markets, even more sensitive to profits. Whilst most markets move in cycles, commodities are far more cyclical. This is why analyzing alternative statistics - like ounces sold, which depend on market pricing - is critical for AMRK.

The risk is, what do gold and other precious metals do from here? All other markets move in cycles too. Except, in those markets, there are substitutes. If the cost of filler in medicine increases, a substitute can be developed. Gold, for example, a primary element, has no known substitutes and must be mined. The pricing power is not in the hands of the company, therefore. I am also not in the business of forecasting commodities.

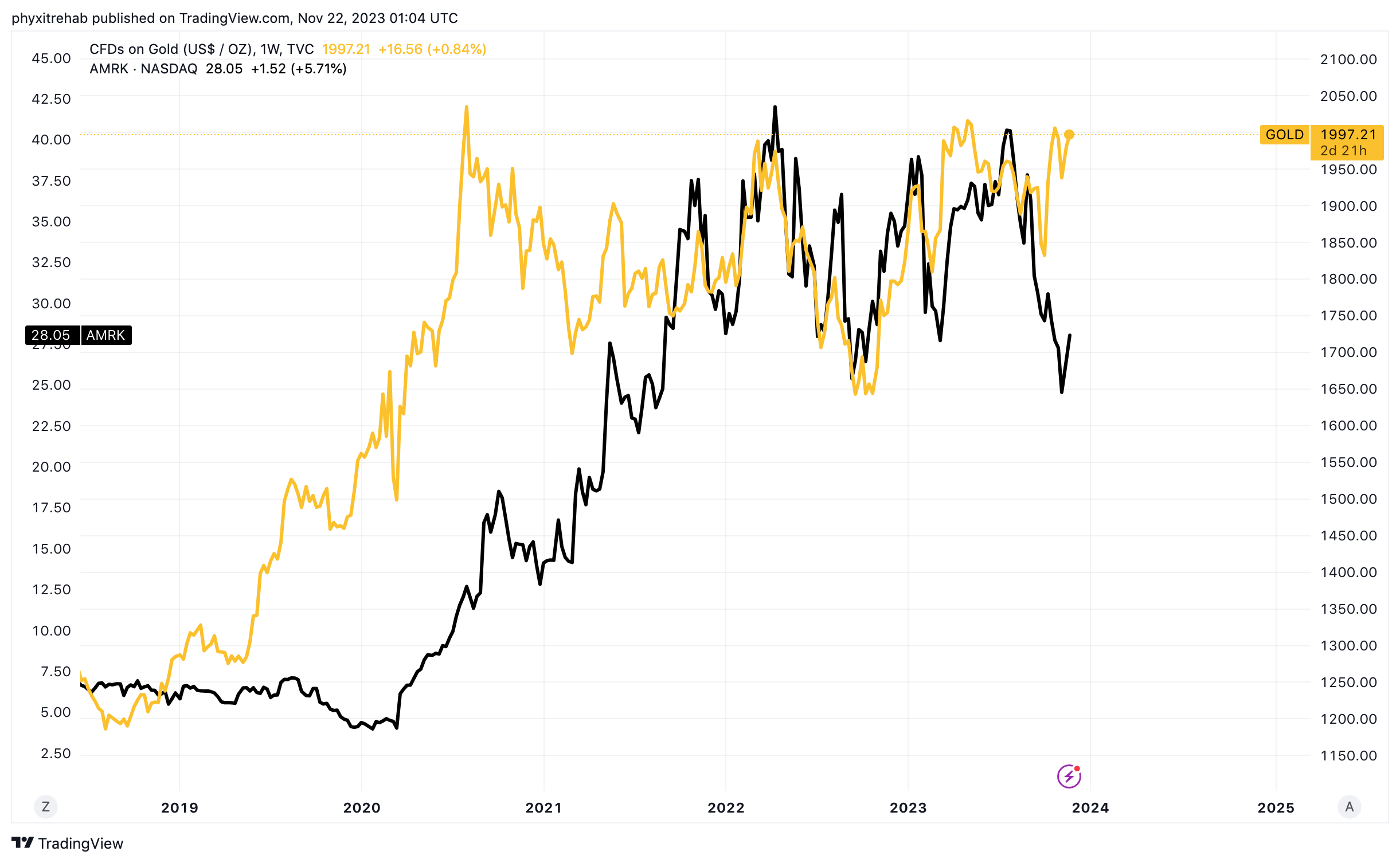

Figure 7. AMRK share price vs. gold spot price, 2019-date

{kind=link}

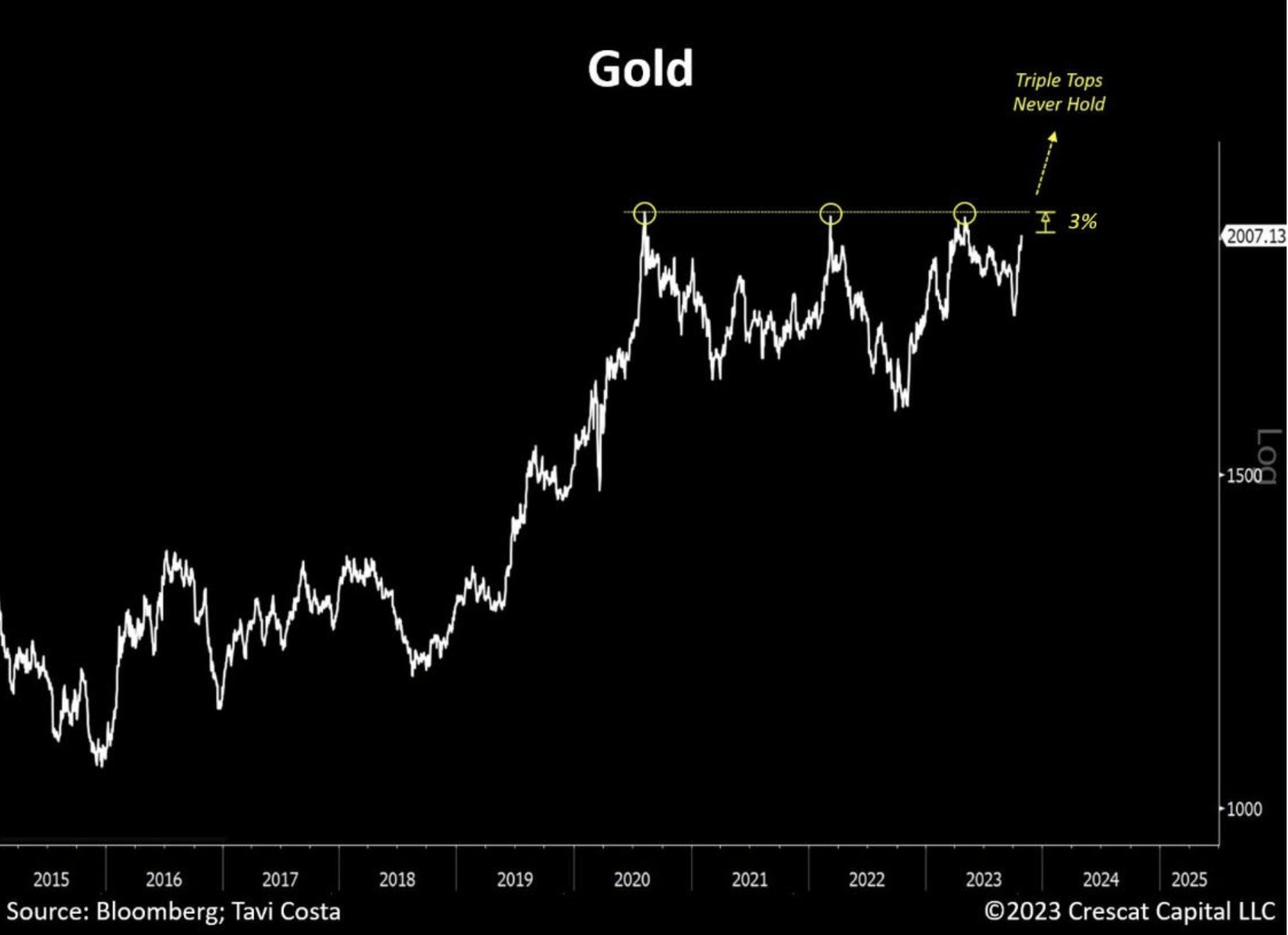

Figure 8. Gold testing triple top

{kind=link}

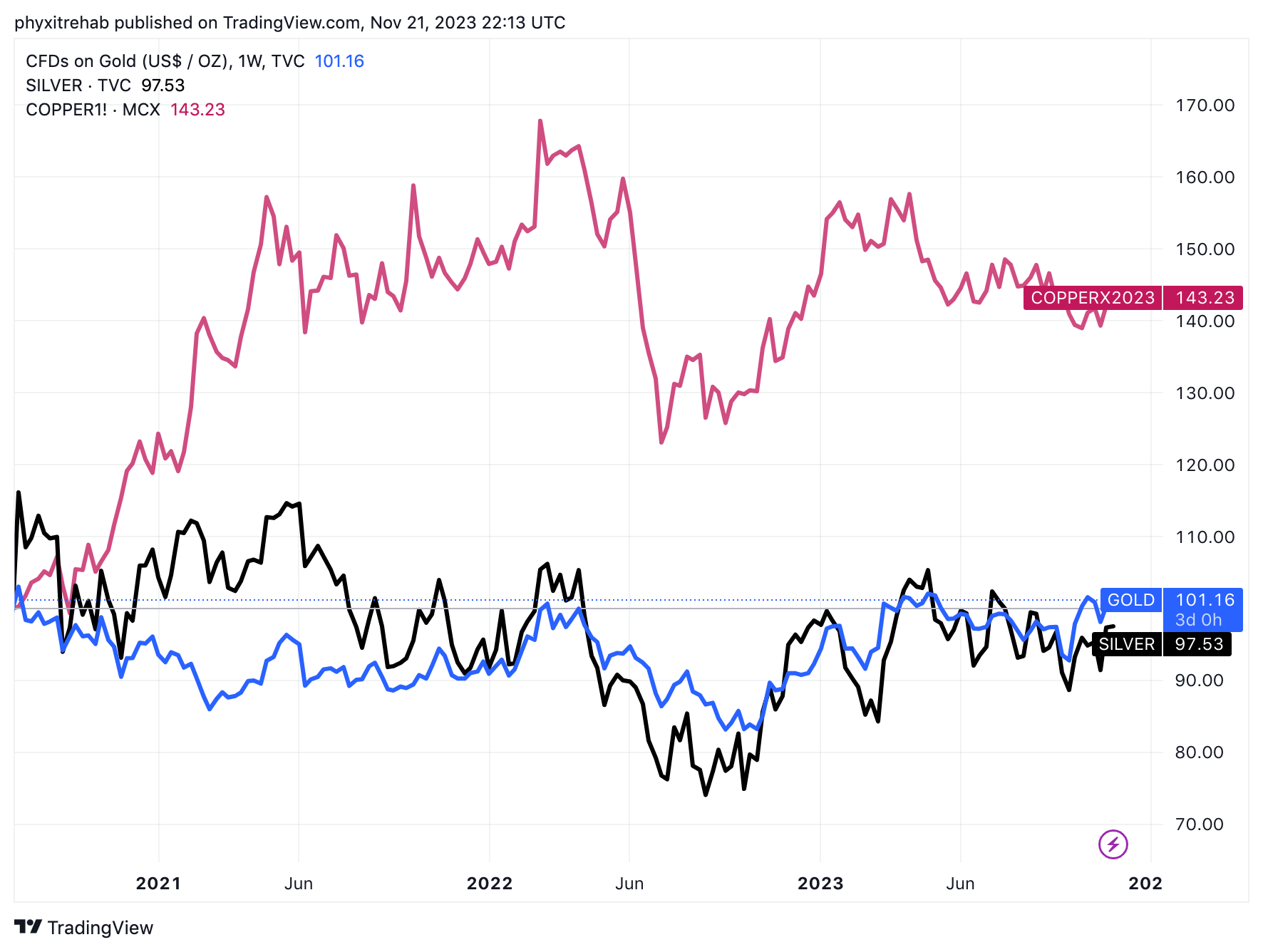

Figure 9. Gold vs. Silver vs. Copper, rebased to 100 (index starts in 2021).

{kind=link}

Two, the firm's profitability, whilst commendably high, relies entirely on turnover of capital. The ratio of sales to assets must remain high, as margins are <5% after tax, as we saw earlier. Any slowdown in business will impact business returns sharply. There is nothing to absorb at the margin.

Critically:

- It had $9/share invested in the business by Q3, increasing commitments by $4/share from 2020.

- Earnings growth from this time was just $0.46/share to $1.59, or 11.5% return on incremental investment.

- This, as sales grew by >70% over this same period.

Herein lies the major hurdle I have when investing in commodity-based businesses. What opportunities are there to grow the business other than buy + sell more gold etc.?

Consider that:

(i). High turnover from capital must be ploughed back into buying more inventory to keep the machine running

(ii). The reinvestment runway to reallocate growth capital is small and relies on customer acquisition

So whilst the profits + cash flows are high, the very nature of the business consumes profits to sustain the company's competitive position. This is a major economic hurdle in my investment distance race.

Valuation

The company sells at near-offensively small multiples of 4.8x forward earnings and 10.5x forward EBIT. Are these statistical discounts, or indicative of this company's intrinsic value?

Using sound economic principles, a few considerations must be made:

- Looking at margins as a source of value, the company's profitability is an eyesore. Compared to the assets and earnings in the business, it is a standout. Avg. 23.5% return on capital employed, 22% trailing ROE - these are clear indications of a company creating value off assets employed to run.

- AMRK also sells at 1.08x book value. You would buy the company today at (1.08 x $581.7 = $628mm), its ROE would be 22% (130/581.7 = 0.22). At these fair multiples, the investor ROE is also ~21% (120 / 628 = 21%). There is value in these compressed multiples.

Going beyond profitability and examining growth, cracks start to appear in the valuation fault line. Compounding the firm's intrinsic value at the function of its ROIC and reinvestment rate suggests the market has been a good judge of fair value these past few years.

In my judgement, AMRK is therefore fairly priced at its current levels. This is because (1) the company cannot recycle surplus capital into new growth avenues to compound value, (2) The undifferentiated offering relies heavily on rate of capital turnover vs. margins or business strength, and (3) The reinvestment runway for business growth is small and confined to expanding its marketplace.

Figure 10.

{kind=link}

In short

In summary, AMRK presents multiple inflection points within the investment debate. However, the facts pattern supports a hold for the company. Critical analysis reveals why:

- AMRK enjoys exceptionally high profits relative to assets employed in the business.

- However, the nature of its industry means opportunities to reinvest surplus capital are small and confined.

- Hence the ability to create additional value/compound intrinsic value over the long term is equally as confined.

I do not feel the company is overvalued. There is fundamental data supporting its rise in market value from 2020. But there is no such clarity as I write. Net-net, rate hold.

For further details see:

A-Mark: Highly Profitable Downstream Precious Metals Play With Confined Growth Opportunities