JXN - A New Era Approaches For AIG

2023-10-04 13:23:52 ET

Summary

- Insurance companies are poised to benefit from a new secular tailwind of higher interest rates.

- Property & Casualty insurers have large, short duration bond portfolios that will cause them to experience the fastest increases in investment income.

- AIG is poised for a massive long-term breakout due to industry leading underwriting performance, share repurchases as it divests Corebridge, and growing investment income.

The Bottom of the Cycle

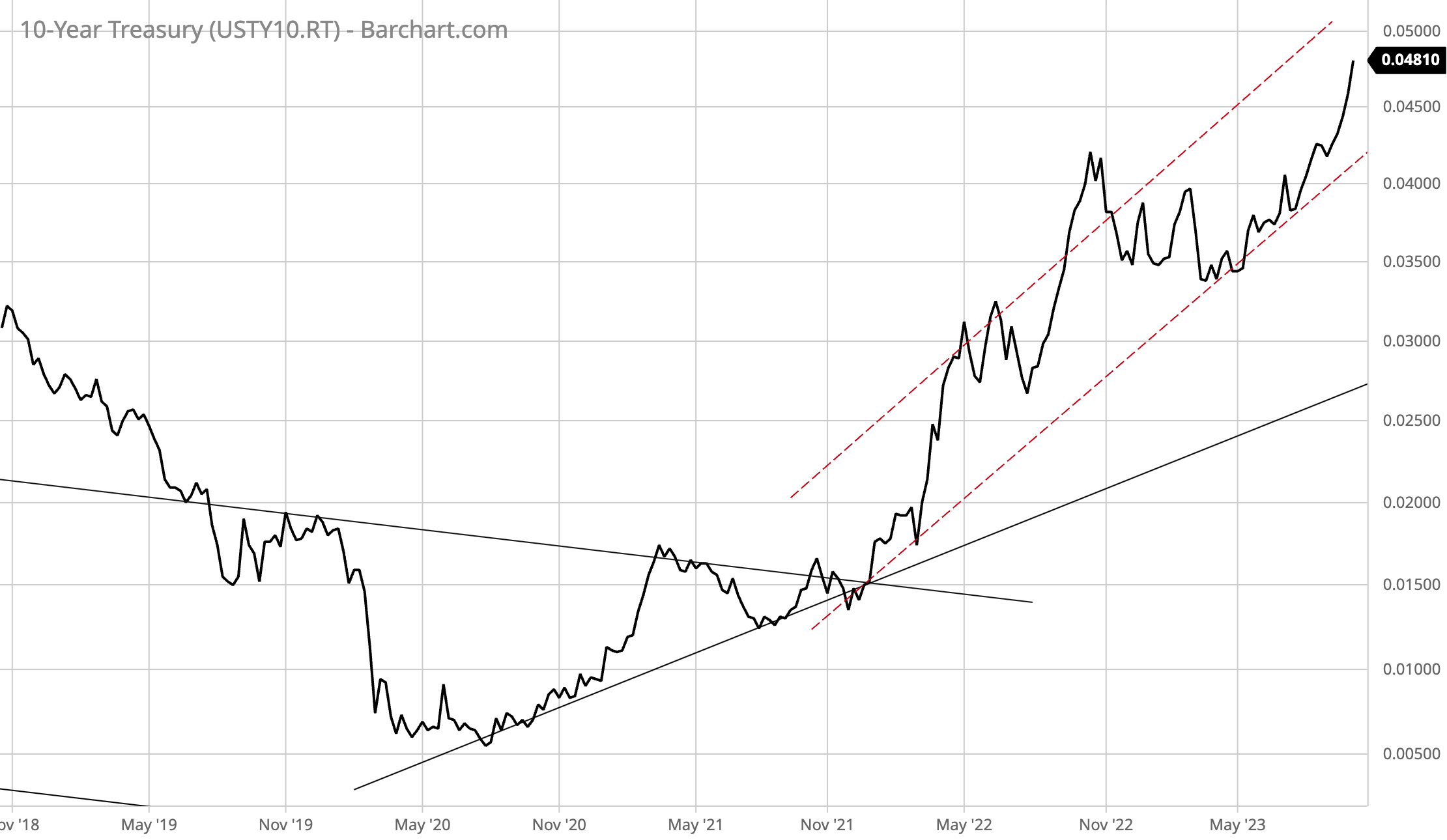

Let us start with the tailwind. Here is a weekly chart of the 10-Year U.S. Treasury yield:

{kind=link}

By my estimation, the U.S. Treasury still has to sell over $750 billion of net new debt this year. As you can see in the above quarterly chart, the 10-year U.S. Treasury yield is exploding higher (the U.S. Treasury bond market is crashing).

Every once and a while, a vision of an investment opportunity unfolds before me. This is happening now in life insurance and annuities companies which look poised to see earnings growth from higher interest rates—potentially a multi-decade, secular trend of higher interest rates—as they experience strong investment income growth from the reinvestment of maturities and new proceeds in their large bond portfolios.

A discovery that I recently made is that the insurance industry, in typical corporate herd fashion, mostly ditched their life insurance and annuity businesses right at the worst possible time—at the very bottom of the long-term, secular cycle. Prudential ( PRU ) spun-off Jackson Financial ( JXN ), MetLife ( MET ) spun-off Brighthouse Financial ( BHF ). American International Group ( AIG ) spun-off a minority stake in Corebridge Financial ( CRBG ) and has made public its plans to divest the rest of its stake in the near future.

There are 2 key points that I must make here before continuing on.

First, life and annuity insurance companies are not banks. They have long-term assets (bonds) and long-term liabilities (insurance liabilities) whereas banks have long-term assets (bonds and loans) and short-term liabilities (deposits). In a rising interest rate environment, like we are seeing this year, a bank can be forced to sell its bonds at a loss if it is losing deposits. This is not case for life and annuity insurance companies. Their long-term bond portfolios will decline when interest rates rise, however, they tend to hedge these to protect their capital. The key point is that life and annuity insurance companies usually do not have to liquidate their bonds at a loss.

Insurance company stock prices were drug down earlier this year as banks brought down the Financials sector and this has helped create even more value in insurance shares generally. This could happen again, however, as I highlighted in the intro, I expect the major move happening on the longer end of the bond curve to generally benefit insurance companies going forward.

Second, Property & Casualty (P&C) insurers, such as Progressive ( PGR ) and AIG have shorter duration bond portfolios than life insurance and annuity companies. This means that P&Cs should generally experience faster increases in investment income in the current environment as short-term interest rates have climbed much higher (5% to 5.5%).

To summarize this section, insurance companies are in the early phase of a secular tailwind.

AIG

As I was researching insurance stocks, I came across the following monthly chart of AIG:

{kind=link}

Given what it is going on at AIG, which I will get into momentarily, this chart is sort of a beautiful masterpiece for the long-term investor. I’m going to go out on a limb and predict that a game-changing, long-term breakout is coming soon. AIG, one of the poster children of disaster from the Global Financial Crisis, is ready to rise from the ashes after years of cleaning up its underwriting and being buffeted by the secular headwind of lower interest rates. New Chairman and CEO, Peter Zaffino, highlighted this in the 2022 Annual Report :

Having fundamentally changed every part of the company and delivered exceptional performance on our underwriting and operational priorities, we have a renewed sense of purpose and strong momentum.

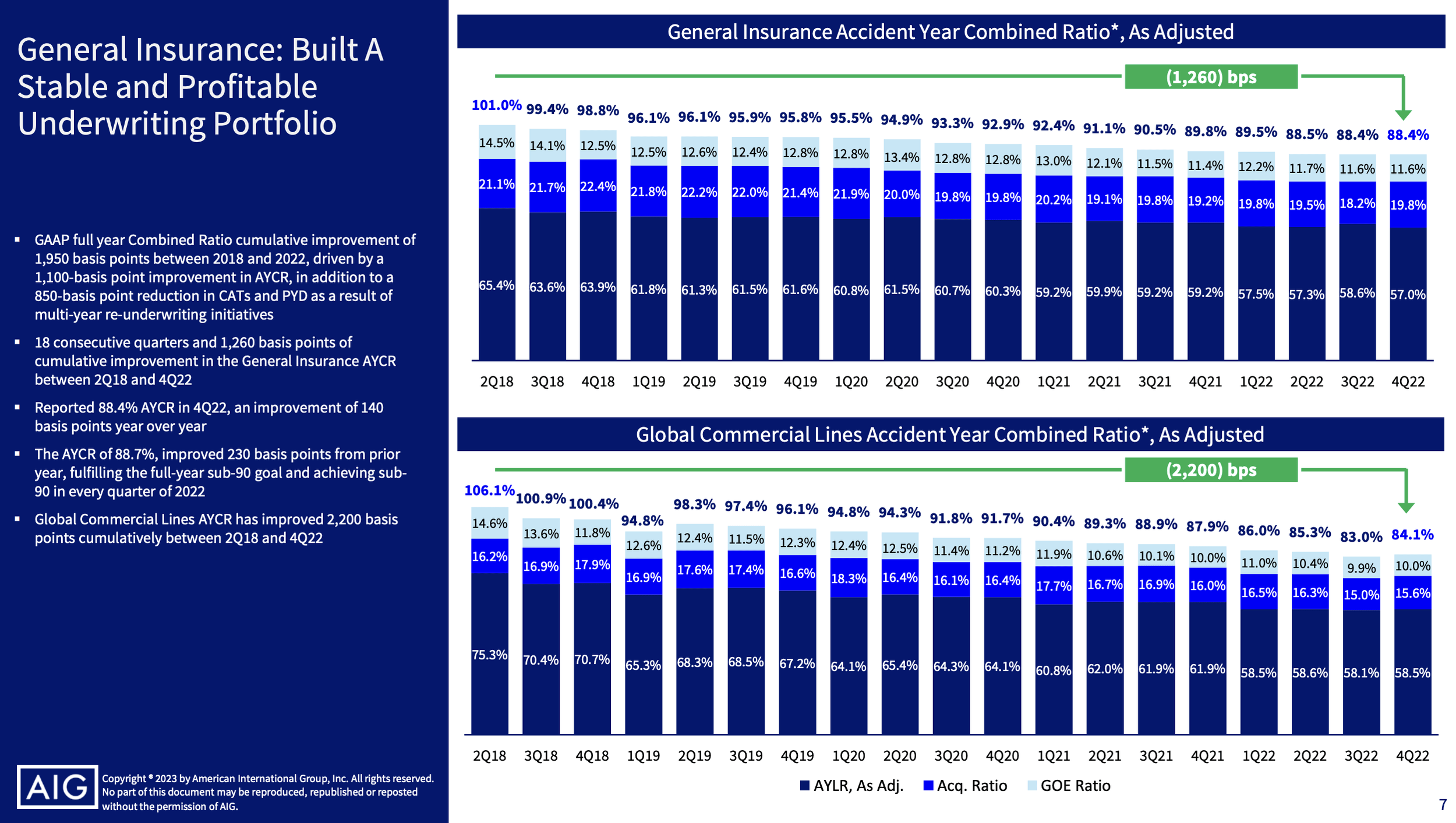

The core advancement at AIG has been its underwriting strength as the company showed in the following slide during its Q4 2022 Earnings Presentation :

AIG Q4 2022 Earnings Presentation

{kind=link}

AIG has gone from a loss making combined ratio 5 years ago to industry leadership this year.

The “Combined Ratio” for an insurance company is the combination of its (1) loss ratio (dark blue above), (2) acquisition ratio (bright blue above), and (3) general operating ratio (turquoise above). What is left over is the company’s underwriting income. AIG’s Property & Casualty segment, General Insurance, finished 2022 with an 88.4% combined ratio. Internationally, it was lower at 84.1%. About half of the General Insurance segments premiums come from outside the U.S. In 2023, the segment is on pace for about an 87% combined ratio which would give it almost $4 billion of underwriting income.

AIG is now on pace with 2022 P&C industry leader Chubb ( CB ) which had a combined ratio of 87.6%. The orange line on the following graphic shows the 10-year combined ratio range of AIG’s global peer group:

Chubb Q4 2022 Earnings Presentation

{kind=link}

The 10-year peer group average was 97.4%. At 87%, AIG is now essentially an industry leader.

Improved underwriting is catalyst #1 for AIG.

Catalyst #2 is the company divesting its stake in Corebridge Financial to focus exclusively on P&C, globally. This is why I have only focused on AIG’s General Insurance underwriting segment above. This is where the company is headed. This is what is ultimately going to drive earnings.

AIG’s market cap is $43 billion. The company’s board recently authorized a $7.5 billion share repurchase plan. They have done so because the plan is to fully divest the Life and Retirement segment and mostly use those proceeds to lower its outstanding share count. These share repurchases will be enormous tailwind for the stock.

Rising interest rates is catalyst #3. As 2025 approaches, AIG’s net investment income (from its General Insurance segment) could rise to $4+ billion, approaching its underwriting income, giving it total pre-tax income of more than $8 billion.

Strategic Conclusion

The AIG that emerges from this transaction will be lean, focused, and more profitable with a short-duration investment portfolio that is poised to increasingly throw off more income.

I estimate that AIG is trading for about 5.6 times the earnings it will have in a year or two after divesting Life & Retirement and subsequently lowering its share count. Assuming a target multiple of 11 times earnings (which Chubb also currently trades for), I arrive at a target price of about $102 per share which is roughly 73% upside over the next 18 to 30 months.

For further details see:

A New Era Approaches For AIG