LGND - A New Ligand Is Taking Shape

Summary

- Ligand's spinoff of OmniAb has rightsized Ligand as it faces revenue challenges.

- Ligand's management changes should be productive for it.

- Several key catalysts are poised to enhance its portfolio to address expected revenue reductions.

My inaugural Ligand (LGND) article , 12/2020's "Ligand: Scalable Growth" served as my introduction to this innovative and attractive company. I started out as a fan and continued until my most recent 12/2021, " Ligand: Green Shoots And A Hidden Treasure - A Spinoff Bonus For The New Year".

Today, 12/29/2022, its OmniAb ( OABI ) spinoff is complete, as I recently reported in a separate OmniAb report . In this article, I issue a sanguine assessment for Ligand, albeit it will soon face a significant revenue falloff as COVID abates,

Now a smaller, more focused company, Ligand has completed its OmniAb spinoff.

Ligand announced completion of its OmniAb spinoff in an 11/01/2022 release . It was structured as a tax free deal, accordingly its logistics were complex as described in the release. In its Q3, 2022 earnings call (the "Call"), Ligand's then CEO Higgins described the substance of the deal impacting Ligand shareholders as:

- While retaining their same share ownership in Ligand, after the split Ligand's shareholders received 4.9 shares in OmniAb;

- roughly half of Ligand's workforce of 150 people will leave.

As promised during the Call, Ligand reported a specific employee count of 79 in its 12/13/2022 Investor & Analyst Day presentation (the "Presentation") slide 5.

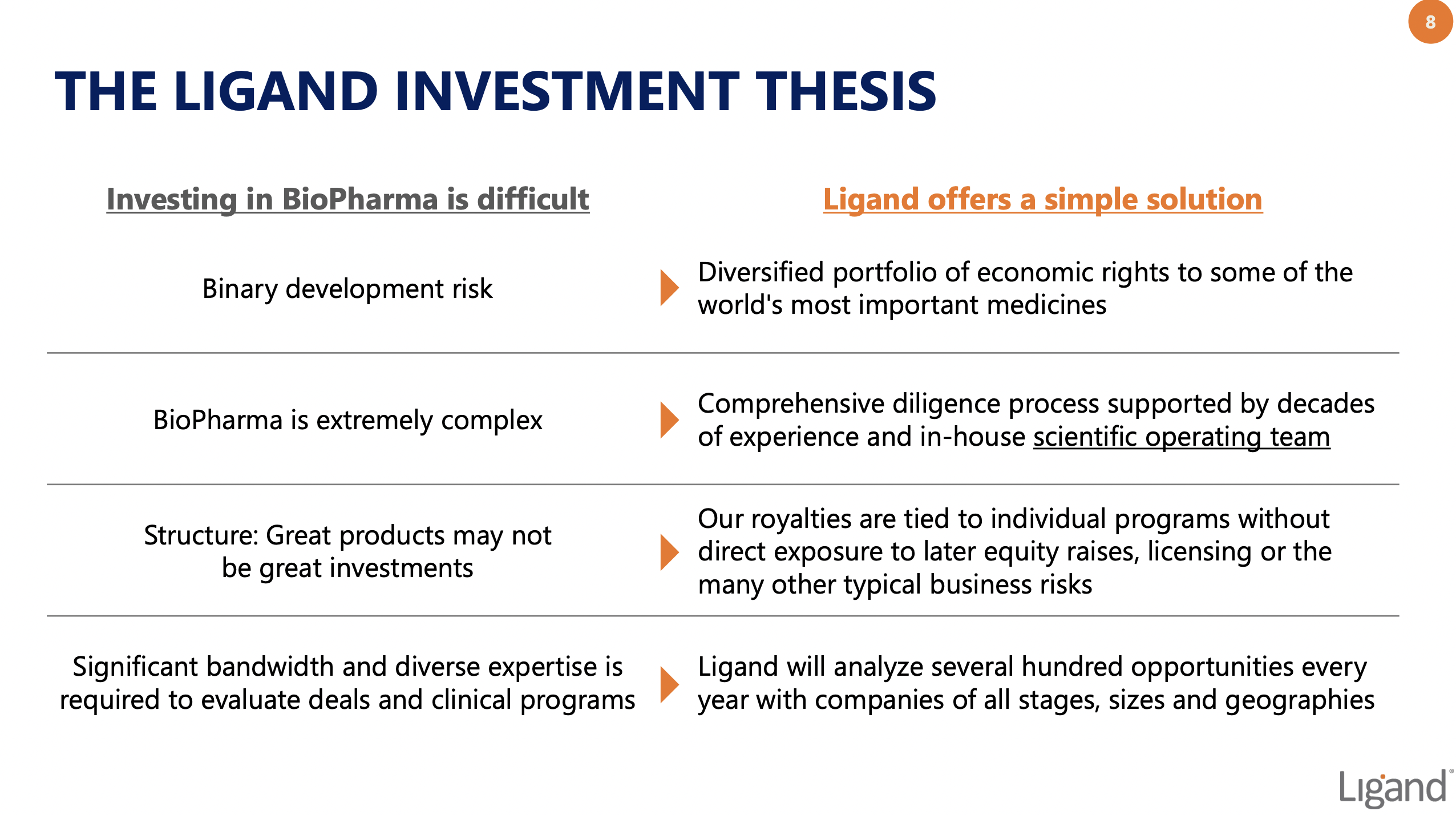

Presentation Slide 11 described the Ligand investment thesis as follows:

{kind=link}

One of Ligands great attractions is the ability to participate, albeit at a reduced level, in the drug development experience of dozens of the world's most productive pharmas. Ligand and its investors enjoy multiple shots on goal.

Ligand's business model allows it to benefit from successful therapies without having any direct participation in the expense of clinical trials. As described in more detail below, its deal team evaluates hundreds of opportunities every year, only selecting the few that its long experience has shown to have the most potential.

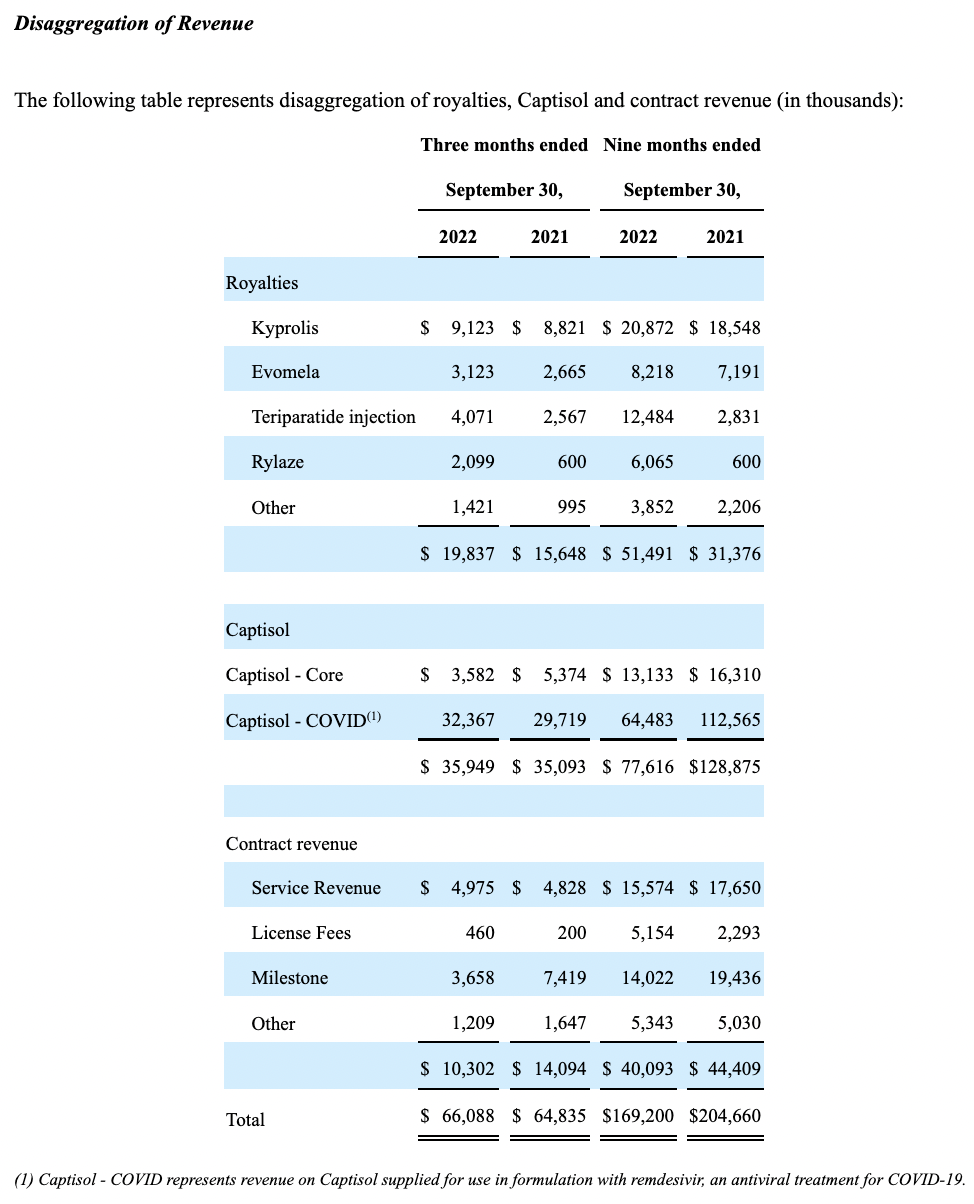

This thesis translates into today's Ligand with its disaggregated revenues as shown by the table excerpted below from its Q3, 2022 10-Q:

{kind=link}

The important medicines which are partially enabled by Ligand technology and which return the most revenue to Ligand include Kyprolis , Evomela, Teriparatide injection , Rylaze, and Remdesivir. Captisol, a solubilizing agent, is Ligand's most productive asset.

It was a big pandemic winner thanks to Ligand's propitious deal with Gilead ( GILD ) to supply Captisol as a key ingredient in Gilead's COVID-19 therapeutic remdesivir. This deal is so lucrative that it merits its own, by far the largest line item, on Ligand's disaggregated revenue graphic above as "Captisol-COVID".

Ligand has been quite open about its expectations for Captisol-COVID revenues to tail off as the pandemic winds down. This has proven difficult to predict. In any case, while responding to a question during the Call, then Ligand CEO Higgins advised that Captisol-COVID should run down to nil revenues during upcoming quarters.

Beyond its role in remdesivir, Captisol is used in sundry other therapies reflected as Captisol. Unfortunately, Captisol-core revenues are far smaller than Captisol-COVID revenues.

Ligand has reshuffled its C-Suite.

The CEO role is crucial for a company's success. To all appearances, Ligand has operated successfully in recent years. It has carved out a nice niche in the biopharma world where it fulfills an important role as reflected by disaggregated revenues set out above. Its share performance however has been uninspiring as reflected by it comparison to the S&P 500 below:

{kind=link}

By my estimation, its C-Suite executives were a bit too highly appreciated; its Compensation table (p. 66) in its most recent Proxy valued its four top executives' 2021 compensation packages at an aggregate >$24 million. As I write on 12/29/2022 of these four, only Matthew Korenberg, then CFO and now President, is still with Ligand.

Ligand announced CEO Higgins' abrupt departure for no reason given on Monday 12/05/2022. The release was short on explanation. It did provide the following Higgins encomium:

...When the Board recruited John as CEO in 2006, Ligand was operating at a significant net loss and had fewer than 10 royalty assets. With great vision, speed and effectiveness, John implemented a new royalty-based business model, acquired new technologies, and positioned the company for significant growth and profitability. Today Ligand has nearly 150 partnered drugs and drug candidates in various stages of commercialization and development. Following Ligand's recent spinout of OmniAb, and its related drug discovery and enabling technologies, we look forward to further strengthening the portfolio through a focus on underserved life science royalty opportunities. With this transition, we are pleased Mr. Higgins will continue to serve as chairman of OmniAb and remain engaged with that company.

The release was optimistic that Ligand's newly appointed CEO Todd C. Davis would provide a seamless and orderly transition. Davis has an ideal background to serve as Ligand's CEO. He joined Ligand as a director in 2007. He has long experience in royalty deals and in structuring a variety of relevant financings.

As I assess the situation, he makes an excellent choice to serve as Ligand's new CEO.

Replacing any falloff on Captisol-COVID revenues will be a steep challenge.

Ligand's big challenge derives from its outsized Captisol-COVID revenues, which made up roughly half of its overall revenues in Q3 of both 2022 and 2021.

For nine month revenues in 2021 and 2022 the percentage is trending better, ~38% for nine months in 2022 down from ~55% in 2021. The difference in percentage is the result of a drop of nine month Captisol-COVID revenues from $112,565 to $64,483. Nice gains in 9-month royalties from Teriparatide injection and Rylaze also contributed to reducing the Captisol-COVID percentage.

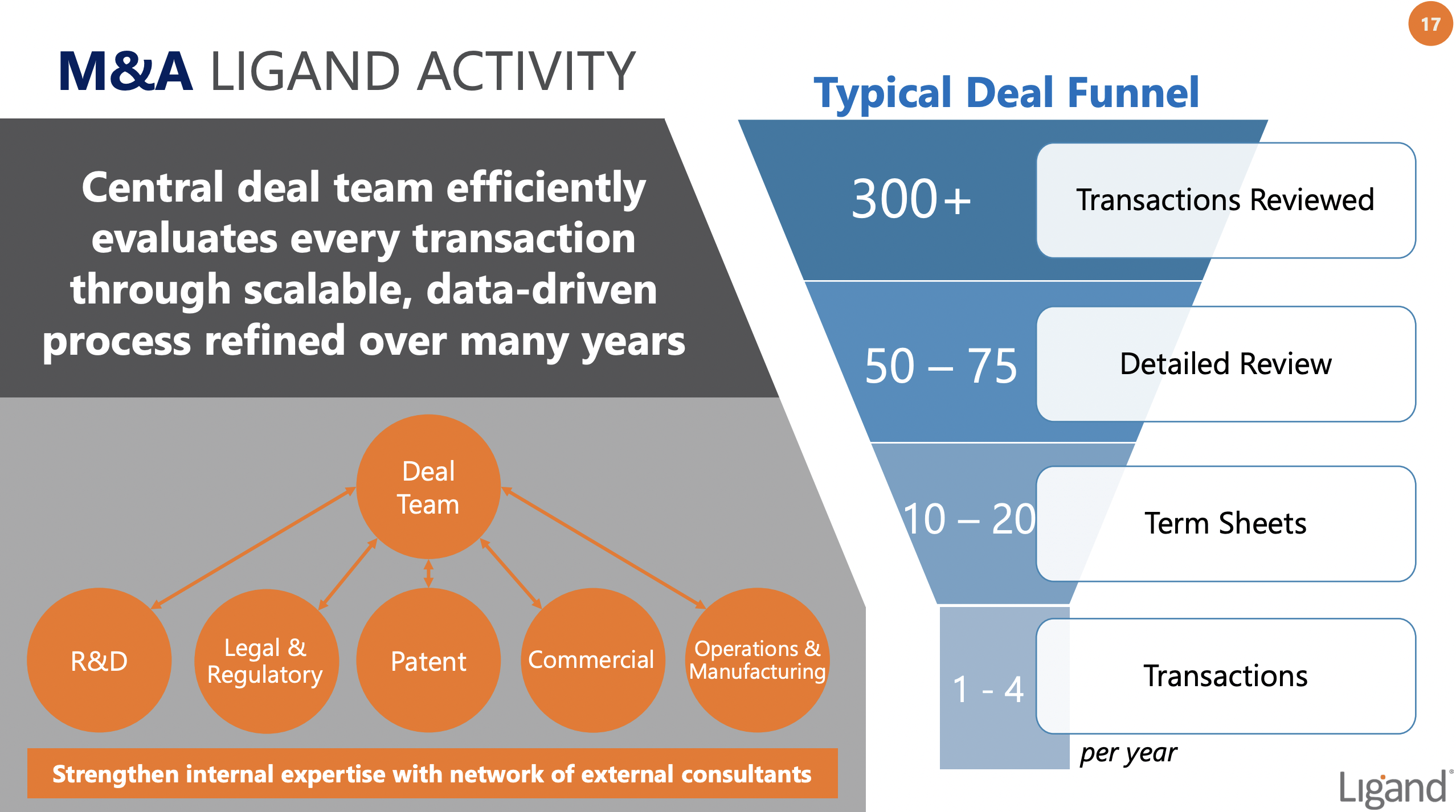

Deals are an important element of Ligand's growth strategy. It has taken deal making beyond an art form, mechanizing the process. It has built deals into its corporate culture, typically reviewing 300 opportunities a year with its experienced central deal team:

{kind=link}

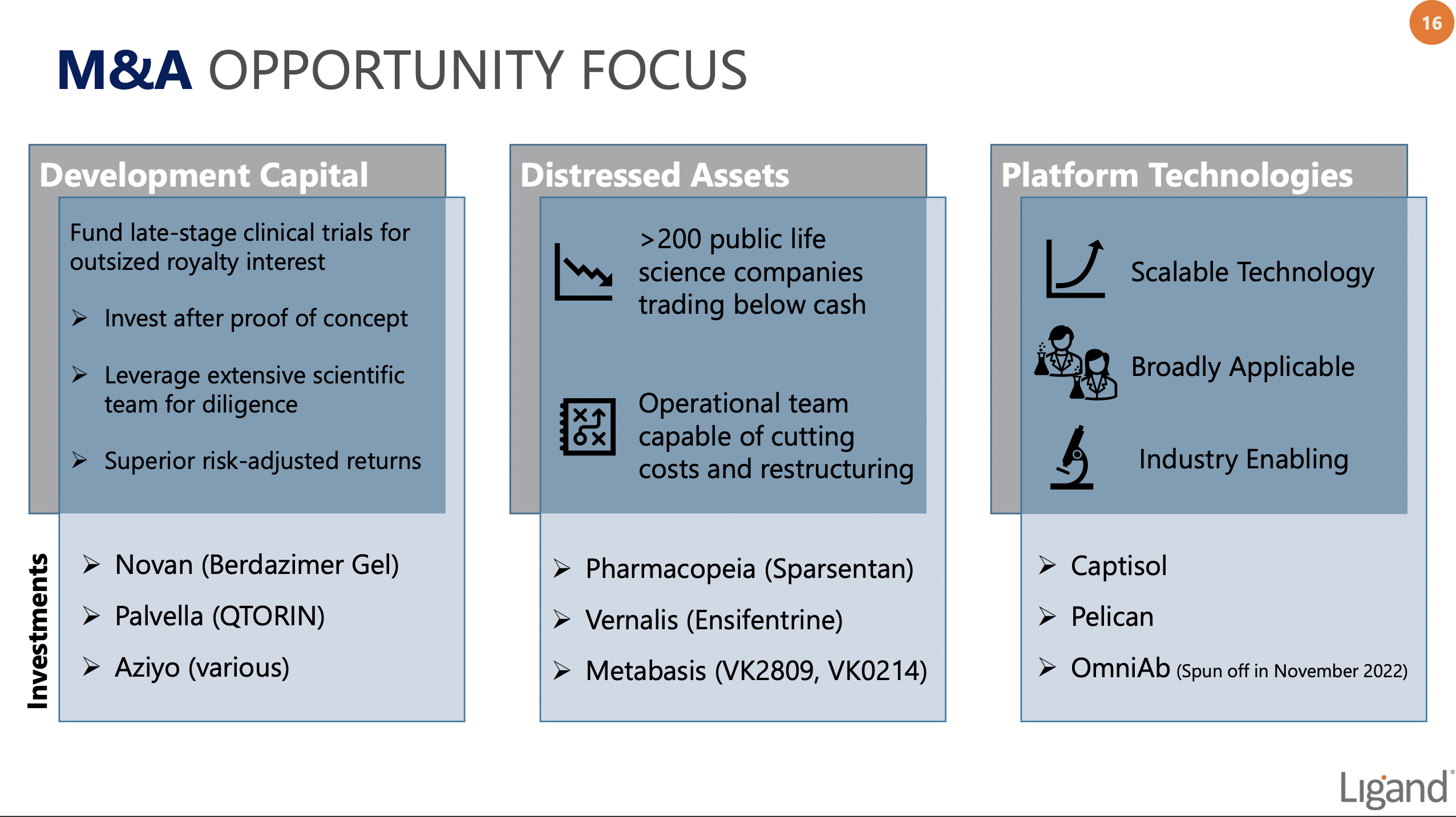

The 300+ deals it looks at then get winnowed down through stages to a handful that actually go forward. Presentation slide 16 shows the three types of deal that it typically finds productive, listing examples of its previous deals

{kind=link}

Ligand's efficient deal making has generated a partnered pipeline including 6 approved programs, many of which are included in its disaggregated income above. Its three most significant partnered programs still in trial stage include:

- Sparsentan, its lead therapy in development for IgA Nephropathy partnered with Travere Therapeutics, in line for 2023 FDA approval with analyst consensus 2027 royalty revenue of ~$60 million,

- Ensifentrine, a Phase 3, first-in-class candidate for the maintenance treatment of COPD, partnered with Verona Pharma ( VRNA ) with planned 2023 FDA submittal and analyst consensus 2028 royalty revenue of ~$10 million,

- Berdazimer Gel, developed by Novan as a topical treatment for molluscum and acne vulgaris with near term FDA NDA expected, and analyst consensus 2028 royalty revenue of ~$17 million.

Ligand's above listed revenue potentials are contingent on FDA approvals. However its royalty based model protects it from the expenses associated with developing these therapies.

Conclusion

Ligand's 2023 Revenue Guidance of $118 - $122 million consists of:

- Royalties - $72-76 million, of which Amgen's Kyprolis contributes 45%;

- Material Sales - $21 million primarily Captisol for commercial use - Core Captisol sales expected to return to pre-COVID levels;

- Contract Payments - $25 million, $10 million of which is from a diversity of payments with more than 15 programs contributing to projected contract revenue guidance in 2023; more speculative is the $15 million milestone contract payment for Sparsentan if FDA approved.

Ligand is guiding for 2023 core operating expenses to drop to $46 million split evenly between R&D and G&A. In addition to 2023 guided revenues, Ligand is benefitting without any added cost in the ripening of its partnered therapies. It is standing in line for tens of millions in new revenues as discussed above just from the three highlighted programs. This is the great attraction of Ligand.

Ligand's revenue guidance is not without risk. Its guided royalties are concentrated with a high percentage reliant on Kyprolis. As noted, its contract revenue guidance includes $15 million dependent on Sparsentan approval.

Ligand expects to be solidly profitable in 2023, despite its upcoming loss of Captisol revenues. Currently, (12/29/2023) trading at a market cap of $1.12 billion, Ligand is a solid hold. It is an interesting stock with unusual future growth potential as partnered assets mature over time. Accordingly, consider it as a candidate for acquisition on pullbacks.

For further details see:

A New Ligand Is Taking Shape