QVMS - A New Year Begins With Renewed Recession Worries

Summary

- Last year was one best forgotten when it comes to equity returns. While large drops often indicate a rebound in the following year, 2023 is fraught with some early challenges.

- Chief among those challenges is the increasing probability of a recession. This is making investors very cautious.

- I see merit to selective buying in the upcoming months. In the final stages of a recession, stocks tend to move markedly higher. This is something readers won't want to miss.

- However, I would caution against too much optimism. A recession is never "good" for stocks - especially initially. Increasing defensive exposure and names with strong track records is a good start.

Main Thesis & Background

The purpose of this article is to tackle the broad macro-concern of an impending U.S. recession. This was top of mind for most investors in 2022, and that story continues into 2023 as well. Just because we turned the page on the calendar doesn't mean the primary risks from last year go away. On the contrary, recession risks are likely even more top of mind since the expectation is we will see a definitive recession in the second half of the year. I say "definitive" because the 2022 recession (where GDP dropped for two consecutive quarters) was argued at length in the media and by market participants. I think the next recession will wind up being less of a debate - even those who don't want to admit it will be forced to do so!

With that prediction on the table, this review will discuss the likelihood of such a recession, why it will occur, and how investors can and should prepare for this event. I will lay out how I will be approaching the new year with my cash on hand (currently about 20% of my portfolio) and where I think some select buying could be advantageous. I would urge readers to be very selective of what and when they buy, but also take comfort in the fact that in the late stages of a recession (and after it) stocks tend to perform very well. That means that if we see a short-lived recession, we hopefully won't have to wait very long to see new positions deliver noteworthy positive returns.

A Recession Appears To Be Very Likely

To begin, let us take a moment to understand why this discussion is even important. Why do we need to worry about a recession? The unfortunate reality is because one is very likely to happen, probably by Q3 in 2023. Last year's recession was hotly contested and a primary reason for why it was short-lived (didn't happen at all) was because of continued state and federal stimulus. This pushed out the timetable and forced the worst of the pain into the future instead of us meeting it head-on in the latter stages of the year.

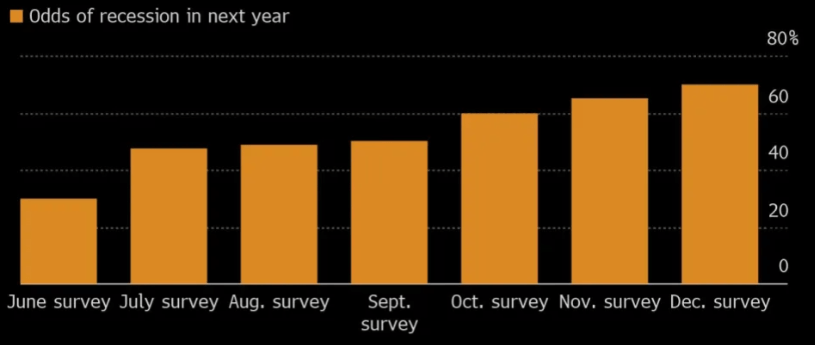

As we push into January, readers should recognize that the majority of economists and market participants now do see a recession happening in 2023. In the middle of last year many were not forecasting such an event to take place. Now, over 60% are, and that percentage has probably risen in the few weeks since the survey was conducted:

Chance of Recession at 70% (Yahoo Finance)

{kind=link}

The consensus (for the time being) is that a recession is a foregone conclusion at this point. Can that change? Of course. But I don't believe it will change and neither does the market. To me this suggests, at the very least, readers need to start thinking now about how they will prepare.

Where Has This Consensus Come From? Many Places, Unfortunately

I will know shift into why this consensus has been building. We have been hearing for a while now that a recession is coming, and I just reiterated that. But that begs the question - why?

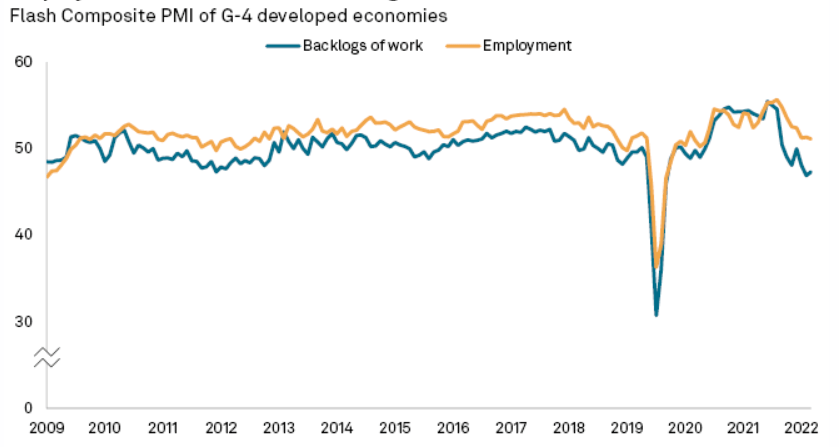

Unfortunately the answer is multi-point. This stems from internal issues within the U.S. as well as global problems that impact the U.S. and other developed economies alike. This is a fundamental point for me - that the economic weakness is not isolated to America. Rather, we are seeing most developed countries contend with inflation, higher interest rates, energy supply issues, and declining business and consumer sentiment. All of these compounding at the same time make the forward outlook look bleak. Further, primary economic signals are declining consistently in major powerhouses like the G-4:

{kind=link}

If major nations on the globe start to see declining business activity at the same time, that is a general precursor to a recession. That has been the short-term trend and I believe Q1 2023 is going to show us more of the same.

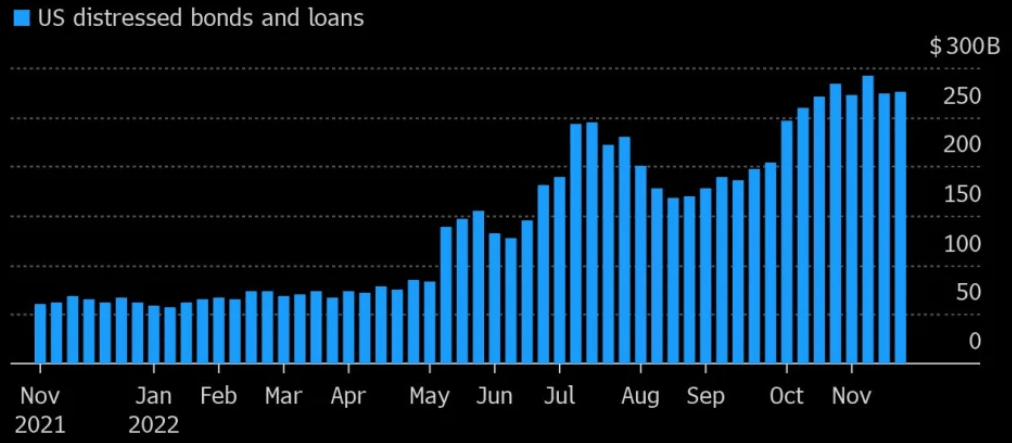

Another worrying trend has been the rise in distressed debt. The total level of U.S. debt under pressure remained at elevated levels through the end of next year. This means that corporate balance sheets are feeling the pressure from the economic environment and the debt that has been issues is getting closer to falling into default status:

$650 billion of bonds / loans are in distressed territory (Bloomberg)

{kind=link}

This is not meant to be overly alarmist because distressed debt levels have risen before without macro-harm being down. But the flip side is also true - that distressed debt loads front-run debt crises. What will happen this time around remains to be seen, but the general rise of trouble in credit markets is never a comforting signal.

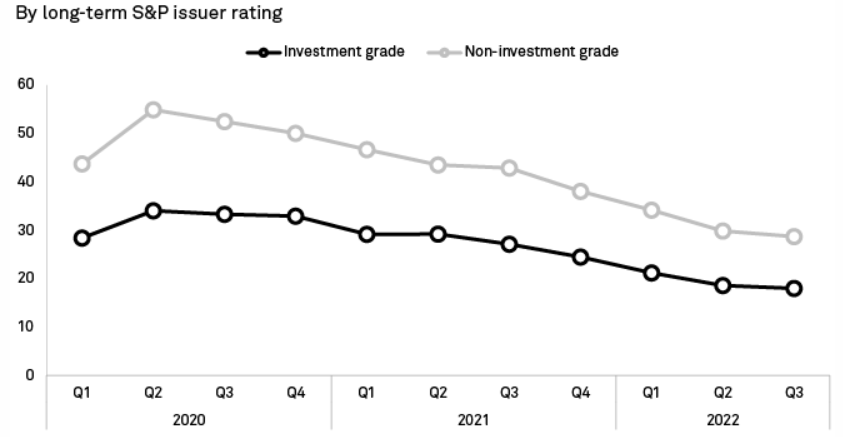

Expanding on the last paragraph, a root cause of the rise in distressed debt burdens is that corporate cash on hand has been on the decline. This is an across the board metric, and explains why distressed debt has risen: if companies don't have cash on hand, that means a higher likelihood of seeing current debt obligations fall into arrears:

Median Cash Ratios For US Companies (%) (St. Louis Fed)

{kind=link}

There are a host of other metrics and signs I could point to, but I believe these are enough to get the message across. Recession risks are rising and justifiably so. This tells me that I need to have a plan in place now.

Should We Worry? Yes, But Not A Lot

Now that I have discussed the likelihood of a recession and the reasons behind it, the next step is how to prepare. A natural move is to begin to reduce equity and/or risk-on exposure. That is a very valid move to make. Unfortunately, getting too creative can be a disservice. Would I be prudent here with new buys? Absolutely. Would I make sure I build my cash reserves (such as sitting on my bi-weekly paychecks rather than plowing them into the market immediately)? Absolutely. But will I be outright selling en masse my positions? Absolutely not.

This comes down to market timing. Selling out now and missing out on further losses is certainly desirable. And the caveat here is that if a readers feels they have too much exposure and won't be able to handle further drops in the market then, yes, selling makes a lot of sense. It is all about risk tolerance. But for those who have a comfortable allotment of cash already (I am at 20% currently), I don't see the immediate need to sell stocks to raise more cash. The reason being is that there is risk in this strategy too. This risk comes down to incorrectly timing the market. If we sell and miss a broad decline, great. But if we sell and miss out on a rebound, that is a painful opportunity cost.

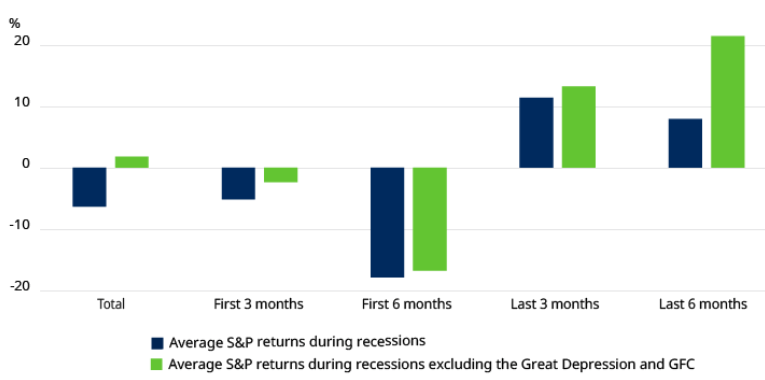

But wait, you say, if a recession is so imminent, why am I talking about a stock rebound? The answer here is because markets often rebound before a recession ends. For support, consider history. At the onset of a recession stocks typically will perform quite poorly. But during the final stages of a recession (i.e. 3-6 months before it officially "ends"), the S&P 500 will typically register double-digit gains:

Average Returns of S&P 500 (Schroders)

{kind=link}

This is where the challenge comes in. It looks likely that if a recession hits those who sold will benefit by missing out on further losses. But timing the re-entry is difficult - most cannot do this with much precision. And if one does miss the appropriate time, that can mean missing out of the gains as well.

My takeaway from this is that oftentimes getting too creative or trading too much can be a disservice. If I sell and miss a 5-10%, only to lag my re-entry and miss the corresponding rebound, it could all be for naught anyway. In lieu of selling off positions, many of which are at a profit which would trigger taxable gains anyway, I will focus on continuing to build up cash through my paycheck (yes, I work for a living) and from dividends. This cash I will use to buy stocks on down days and if a recession dings the broader market. History suggests doing so will work out in the long run.

Be Tactical And Potentially Revisit Old Faithfuls

The good news in 2023 is that investors can get paid to wait out further equity drops. Deposit accounts, certificates of deposit accounts, and other money market options are finally offering reasonable yields. These are ways to earn something with no principal risk. In addition, bond markets are offering historically high yields - so there is merit to moving cash into fixed-income sectors while one waits.

For those with a more risk-on approach, buying stocks can make a lot of sense. Yes, more pain could be on the way, but laddering into broad market funds can work quite well over the long term. Further, there are plenty of defensive names out there that tend to do well during recessionary periods when consumers cut back. Among my top choices (which I own but would also recommend during most recessionary periods) are Walmart ( WMT ), McDonald's ( MCD ), Waste Management ( WM ), and Dollar General ( DG ). I continue to see value in those options, as well as Lowe's ( LOW ) as the housing market takes a breather with elevated interest rates. The logic being as fewer people move / buy homes, home improvement projects rise in demand.

Beyond some of those tradition recession plays I also see some value in less defensive names. One in particular is Microsoft ( MSFT ), which is a household Tech name that is considered a more risk-on, growth play, despite its strong track record over time. Personally, I see it as a more stable, recession proof company due to its history, but investors disagreed in 2022. Over the past year, this stock has dropped over 28% - a move that I believe is unjustifiable:

MSFT's 1-Year Performance (Seeking Alpha)

{kind=link}

Aside from its record of surviving past recession and its usefulness as a dividend play, there is another reason I like MSFT here if I am preparing for a recession.

While MSFT is a diversified company, what I am referring to here is its software business. Known for its gaming consoles (i.e. Xbox), subscription services, and other accessories, MSFT has quite a bit of exposure to the gaming sector. This is especially true as the company continues working towards closing a $68 billion acquisition of publisher Activision Blizzard ( ATVI ).

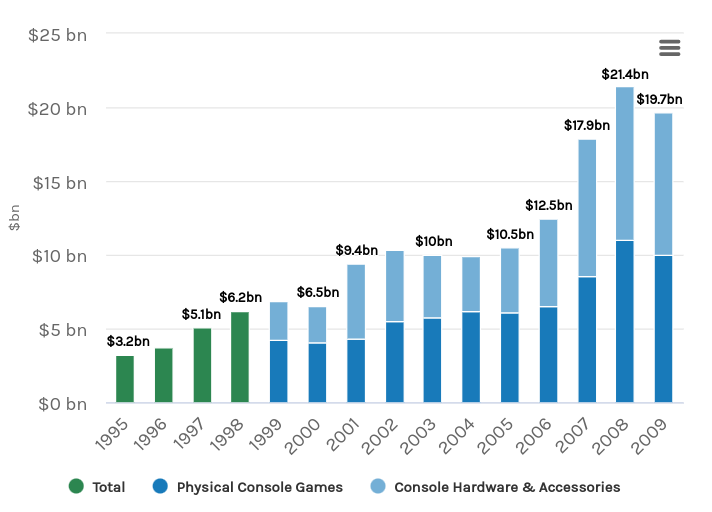

The reason this excites me is that historically consumers have kept spending on video games robust even during recessions. If we look back to the Global Financial Crisis era, we see strong spending figures within this sector in 2008 and 2009, as shown below:

Consumer Spending On Video Games / Consoles (By Year) (Morgan Stanley)

{kind=link}

The point of emphasis here is I like MSFT long term and also as a potential recession beater in 2023. This may seem odd, but the big drawdown the stock saw in 2022 supports the idea that a rebound could be ahead. Given its fundamental business in software is fairly defensive anyway, I view the backstory behind gaming as well as supportive. A similar case could probably be made for search engine champion Google ( GOOG ) (GOOGL). People are going to search the internet and watch clips on YouTube regardless of GDP figures. So there could be some value there as well.

The overall conclusion is that readers should consider some stocks for a recessionary environment that may not seem like traditional "defensive" names, but are likely to hold up well anyway. MSFT in particular is one that I would put into this category.

Bottom-line

The new year hasn't started off great - one session in and we are already in the red for the year (based on the major indices). Concerns over a recession - in the U.S. and globally - continue to plague investor sentiment. The prospect for higher interest rates isn't helping either. This means investors need to make sure they are not currently over-invested. You don't want to have to sell at the worst possible time!

On the other hand, recessions open up some great buying opportunities. Hopefully readers entered the year with comfortable allocations to stocks and bonds, as well as cash on hand. If so, be patient, wait for drawdowns and for a recession to become "official". Once it does, start buying, because the market rebound typically starts before said recession ends. I like defensive names here, as well as Tech plays that seem too beaten down. I also believe bonds are due for a rebound - munis and corporates.

With these thoughts in mind, I want to wish readers a safe and healthy 2023 - I imagine it will be more profitable than last year!

For further details see:

A New Year Begins With Renewed Recession Worries