DHC - A Nightmare Deal Between Office Properties Income Trust And Diversified Healthcare Trust

2023-04-12 09:23:52 ET

Summary

- Shares of both Office Properties Income Trust and Diversified Healthcare Trust fell after news broke that the firms were merging.

- This transaction is actually really positive for shareholders of DHC, but it's awful for OPI's investors.

- The stock does look cheap, but the high leverage and problems OPI looks set to inherit make it a risky prospect.

There is a common misconception amongst the investment community that the management teams at companies behave in a fairly rational manner, at least for the most part. But every so often, you see some sort of transaction that just does not make sense. Such is the case regarding the merger that was just announced between Diversified Healthcare Trust ( DHC ) and Office Properties Income Trust ( OPI ). For investors in Diversified Healthcare Trust, the agreement that will see the enterprise essentially absorbed by Office Properties Income Trust is something of a saving grace. But for shareholders of the acquirer, this move should be looked upon very negatively. I would go so far as to say that this transaction justifies a much more bearish outlook for Office Properties Income Trust moving forward, solely because the business materially overpaid for the assets it's picking up.

A look at the deal

On April 11th, news broke that Diversified Healthcare Trust and Office Properties Income Trust had agreed to an all-stock merger. In exchange for each share of Diversified Healthcare Trust that an investor owns, they will receive 0.147 of a share of Office Properties Income Trust. Based on the 30-day average closing price of Diversified Healthcare Trust, this translated initially to a roughly 20% premium for investors. However, shares of the business declined by 3.2% in response to the news. But this drop is nothing compared to the 24.4% plunge that Office Properties Income Trust experienced, with shares closing at $8.73 apiece.

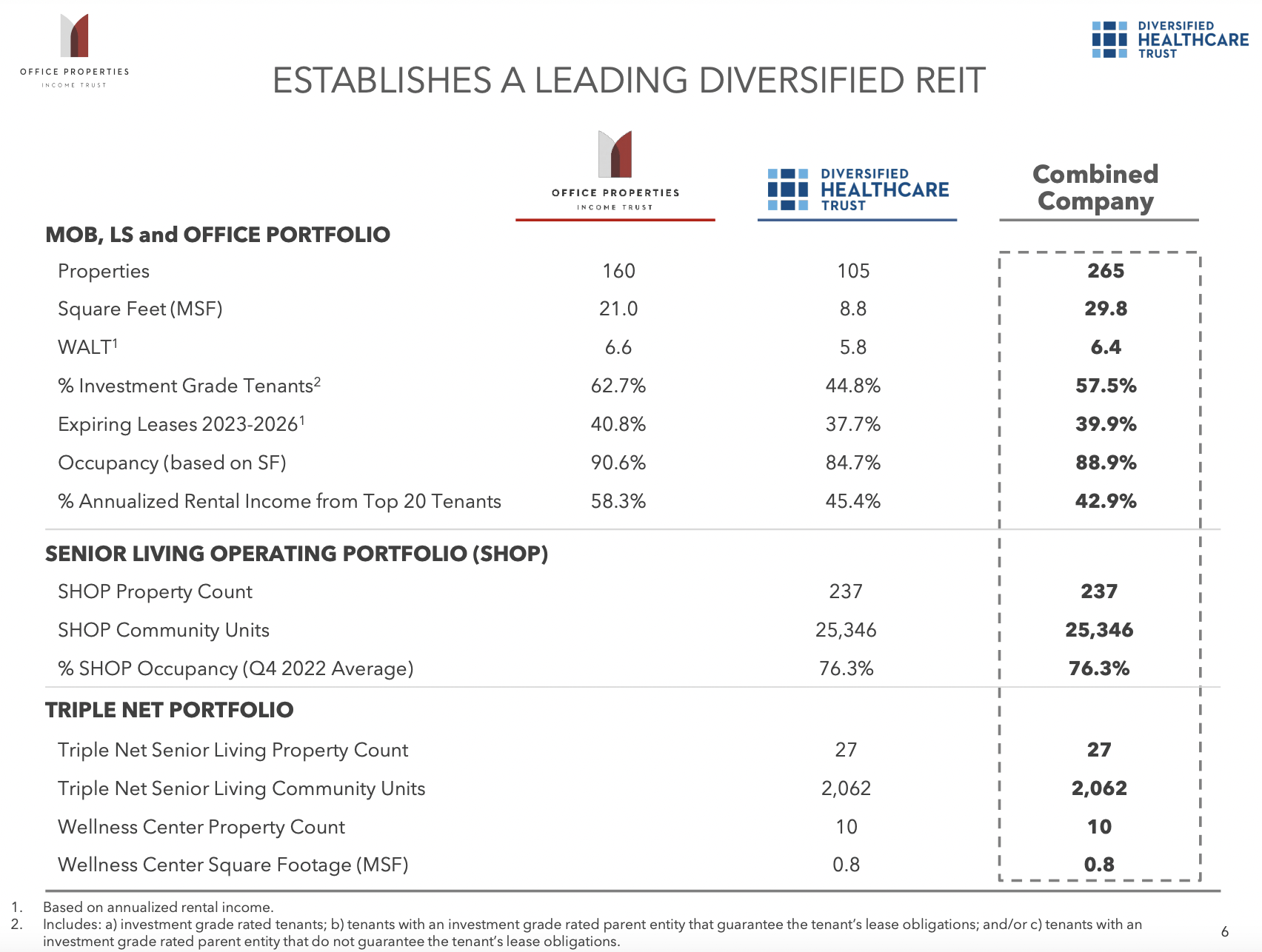

Before we get into why this transaction is bad for investors in Office Properties Income Trust, we should touch on the rationale given by management behind this maneuver. Upon closing of the deal, investors will have exposure to a much larger company than what they had previously. In total, the enterprise will have 529 properties in its portfolio. 160 of these properties currently belong to Office Properties Income Trust, and they all center around medical office buildings, life sciences facilities, and office space. Diversified Healthcare Trust is bringing 105 similar properties (really just office properties) to the table, with an occupancy rate of just 84.7% compared to the 90.6% that the properties owned by Office Properties Income Trust boast.

{kind=link}

On top of this, the combined company will include 237 senior living properties that are managed by a third party. And finally, the transaction will include 27 triple-net leased senior living properties that are not included in the aforementioned managed arrangement. This transaction will result in a rather sizable company that has operations spread throughout 40 different states, as well as in Washington, DC. And approximately 42% of its properties are located in the highly desirable sunbelt region. According to management, the combined enterprise will have 40% of its gross asset values in the senior living space. Office space will comprise 35%, with medical office buildings at 12% and life sciences at 9%.

{kind=link}

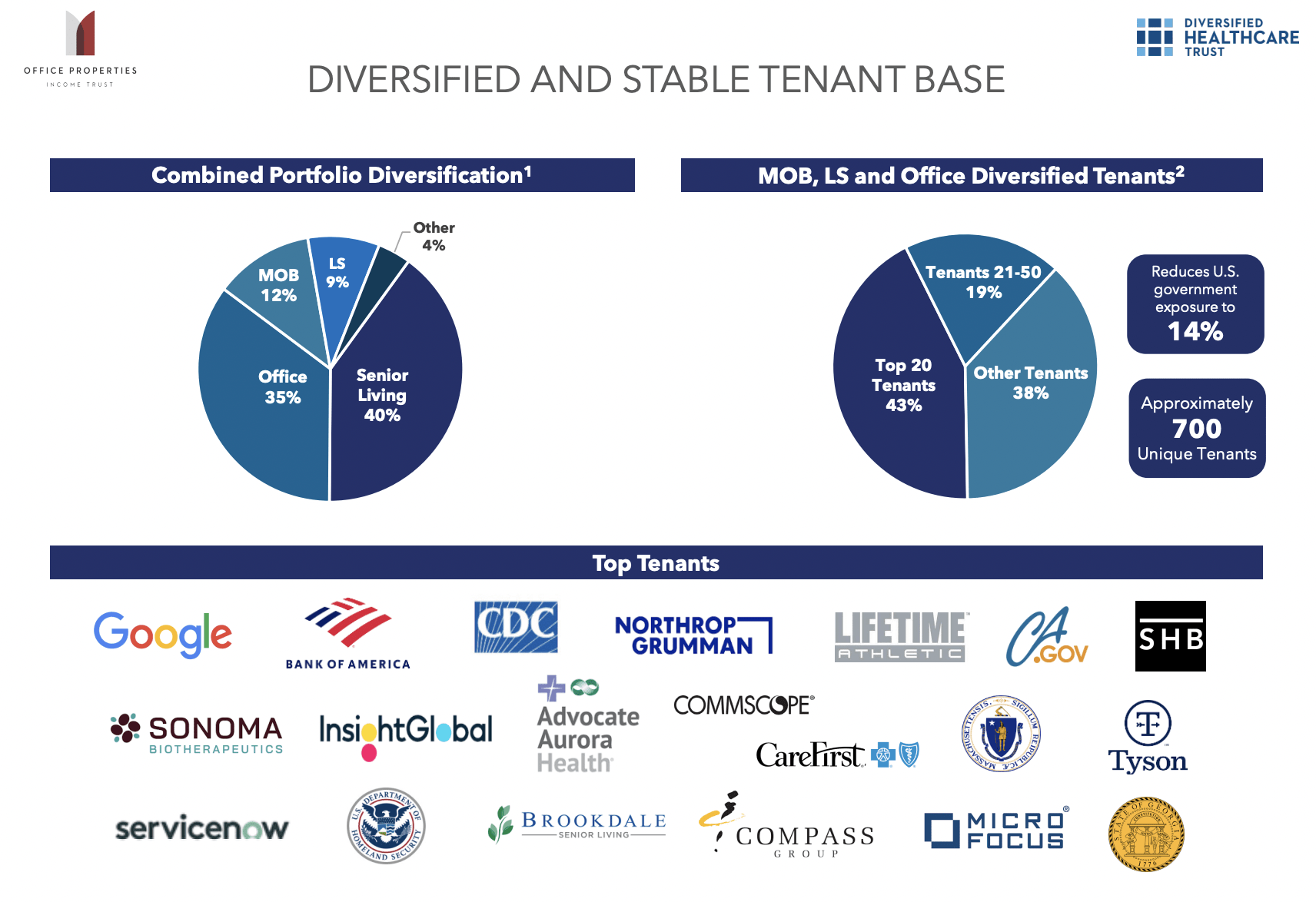

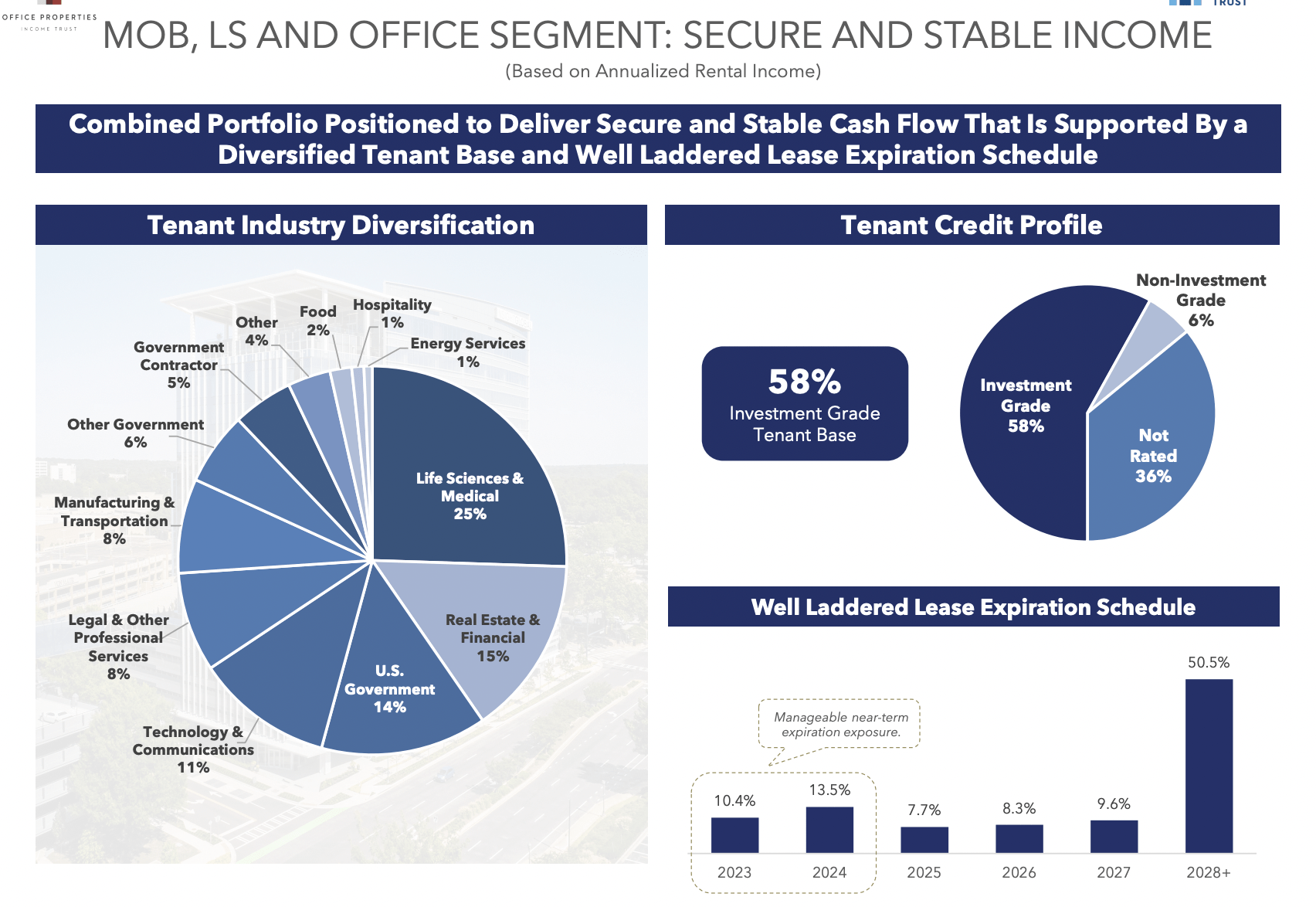

When it comes to specific types of tenants, the largest exposure for the enterprise for the medical office buildings, life sciences, and office segment, will involve life sciences and medical firms at 25%. This is followed up by real estate and financial businesses at 15%. And in third place, we have the U.S. government at 14%. One good thing is that the combined enterprise will still have a rather appealing lease expiration schedule. Between this year and next, only 23.9% of its annual base rent is due to expire. An impressive 50.5% expires in 2028 or later. And when it comes to the senior living properties, management believes that a population that is destined to continue aging will experience heightened demand for these types of services.

{kind=link}

You would expect a transaction of this nature to bring with it significant operating synergies. But this is unlikely to be the case. Or if it is the case, management is being quiet. It is true that RMR Group ( RMR ), which provides management services for Diversified Healthcare Trust, has agreed to waive the exit fee normally charged to a client ending services early. But beyond that, the only synergies mentioned include general and administrative costs of between $2 million and $3 million. Both companies tout this as a win for Diversified Healthcare Trust from a dividend perspective. On an annual basis, shareholders of Diversified Healthcare Trust will receive a distribution of $1.00 per share. At current prices, this translates to a forward yield of 11.3%. While this is a great thing for shareholders of that particular REIT, it does mark a significant haircut from the $2.20 per share previously paid out to investors in Office Properties Income Trust.

{kind=link}

This deal is bad… really bad... for OPI

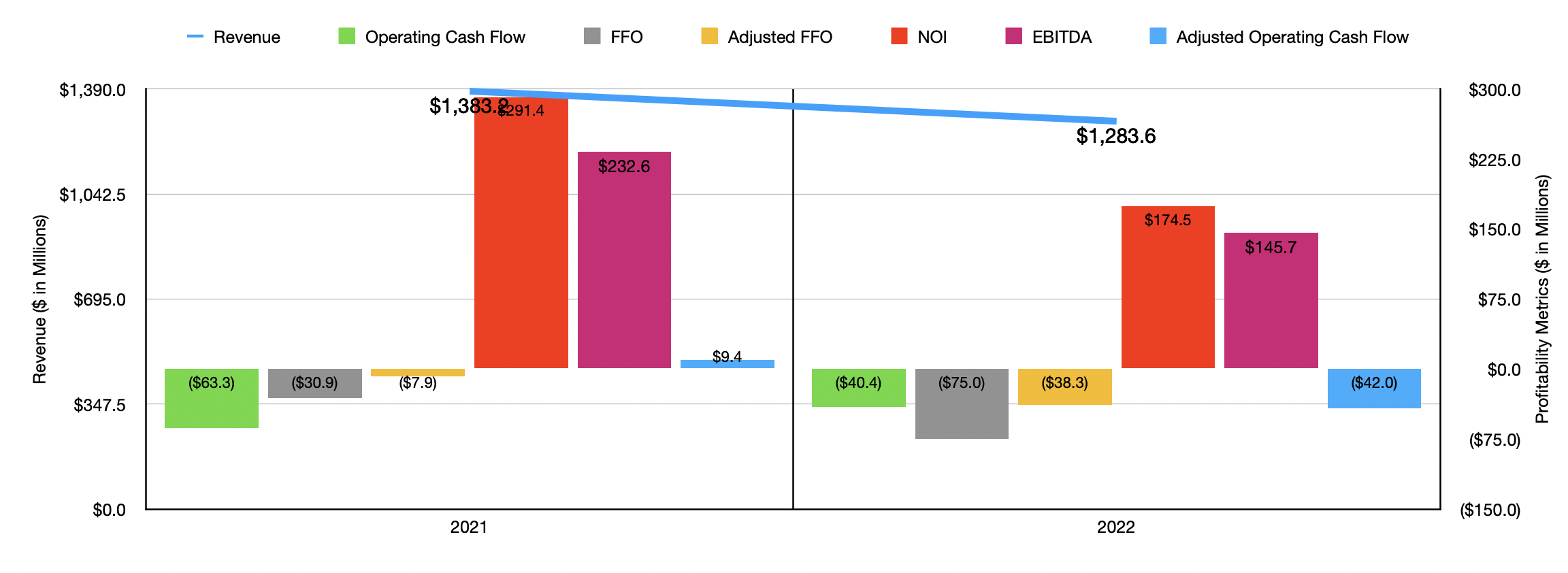

Frankly, for shareholders of Diversified Healthcare Trust, I see this deal as a massive win. To understand why, we need to only look at the recent financial performance achieved by Diversified Healthcare Trust. In 2022, for instance, the business generated revenue of $1.28 billion. That's 7.2% lower than the $1.38 billion reported one year earlier. Even though the company saw its occupancy rate under its senior living properties grow nicely in 2022 compared to 2021, it suffered from a meaningful decline in its office portfolio. Occupancy here plunged from 91.3% to 84.7%. Some of this decline was also driven by a decrease in the number of office properties that the company had in its portfolio. This number dropped from 116 to 105. This, management said, was driven largely by the deconsolidation of 11 medical offices and life science facilities that are currently owned by two unconsolidated joint ventures that the company has an ownership interest in. These factors resulted in revenue associated with the office portfolio of the company plunging from $367.6 million to $222.4 million. In fact, had it not been for this decline, Overall revenue would have grown by 4.5% from 2021 to 2022.

{kind=link}

Bottom line results for the company during this window of time were somewhat mixed. Operating cash flow, for instance, improved from negative $63.3 million to negative $40.4 million. But if we adjust for changes in working capital, we would have seen the metric worsen from $9.4 million to negative $42 million. FFO, or funds from operations, as well as adjusted FFO, also worsened, as the chart above illustrates. The same can also be said of NOI (net operating income) and EBITDA. According to one source , approximately 50% of all office properties across the US are currently empty, with that gaping hole caused by work-from-home that became more popular because of the COVID-19 pandemic. So it shouldn't be surprising to see a company like Diversified Healthcare Trust hit so hard.

{kind=link}

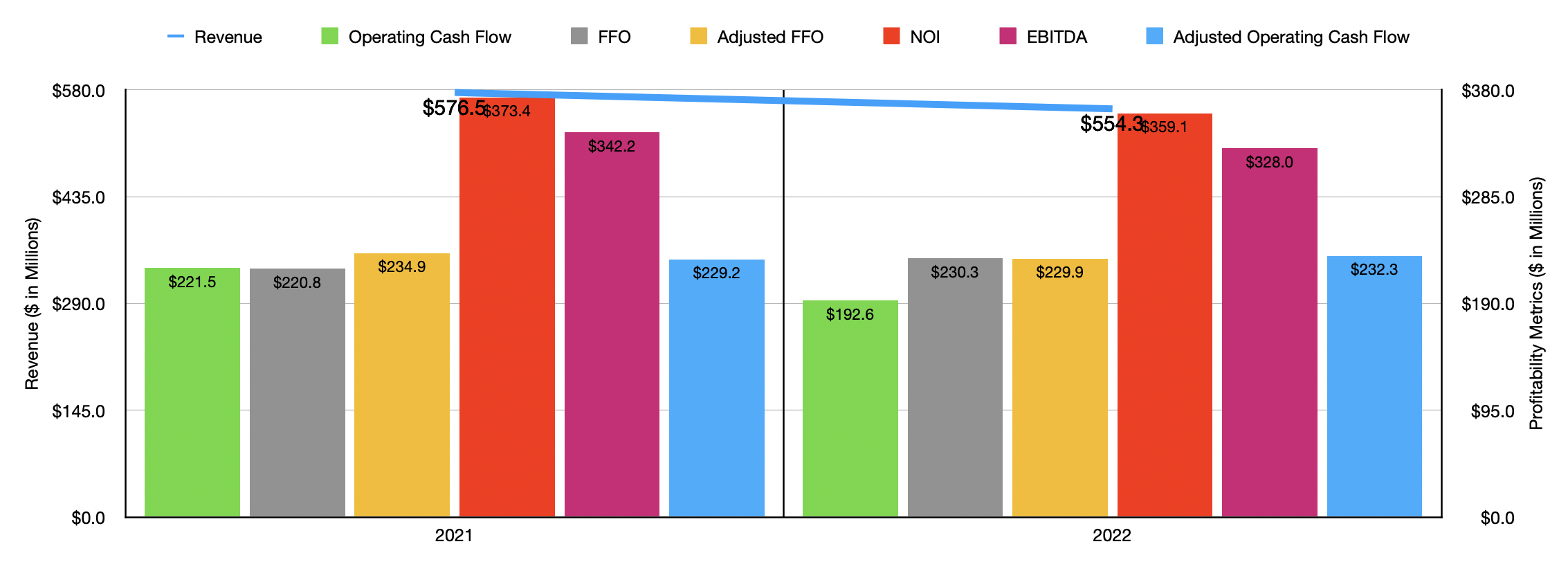

Even though Office Properties Income Trust is considerably smaller, its financial condition is far better. From 2021 to 2022 , the company saw its revenue drop more modestly from $576.5 million to $554.3 million. And from these properties, the company generated significant, though admittedly declining, profits. This much can be seen in the chart above. One motivation for Office Properties Income Trust to move in this direction was likely to diversify itself away from the office category. But they could not have picked a worse firm or worse space to diversify into. Even though Diversified Healthcare Trust saw a worsening in its financial performance when it came to the office properties on its books from 2021 through last year, it's important to keep in mind that those office properties still accounted for 73.4% of the company's NOI. By comparison, the senior living properties were far less profitable, largely because of the third-party management contracts these properties are subjected to.

{kind=link}

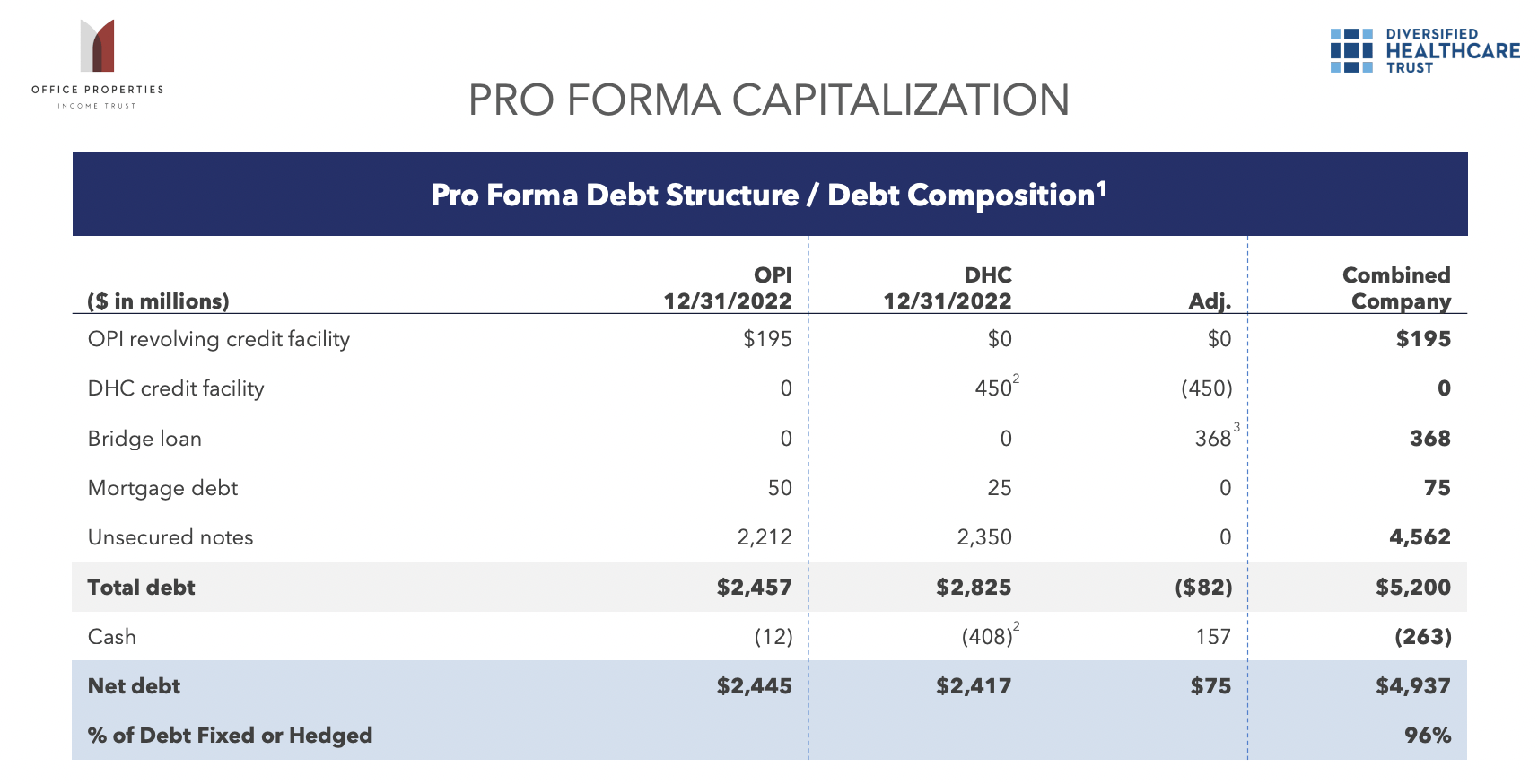

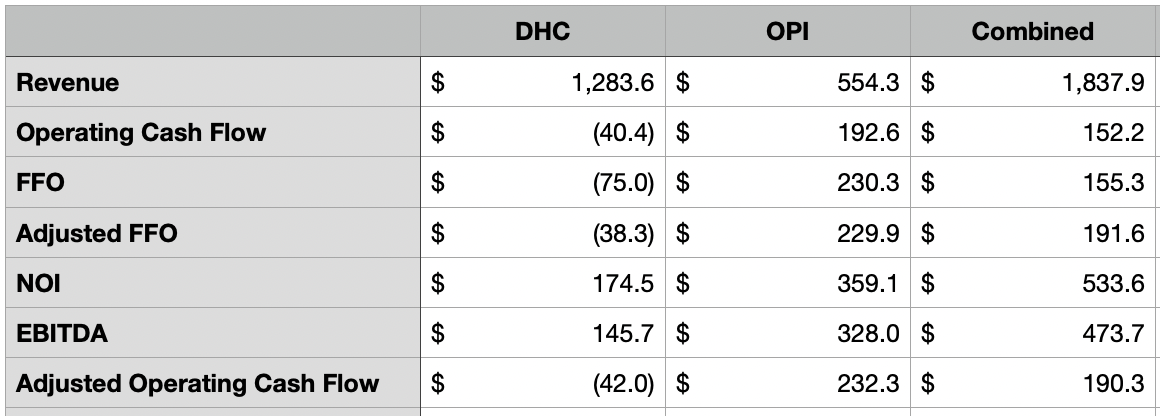

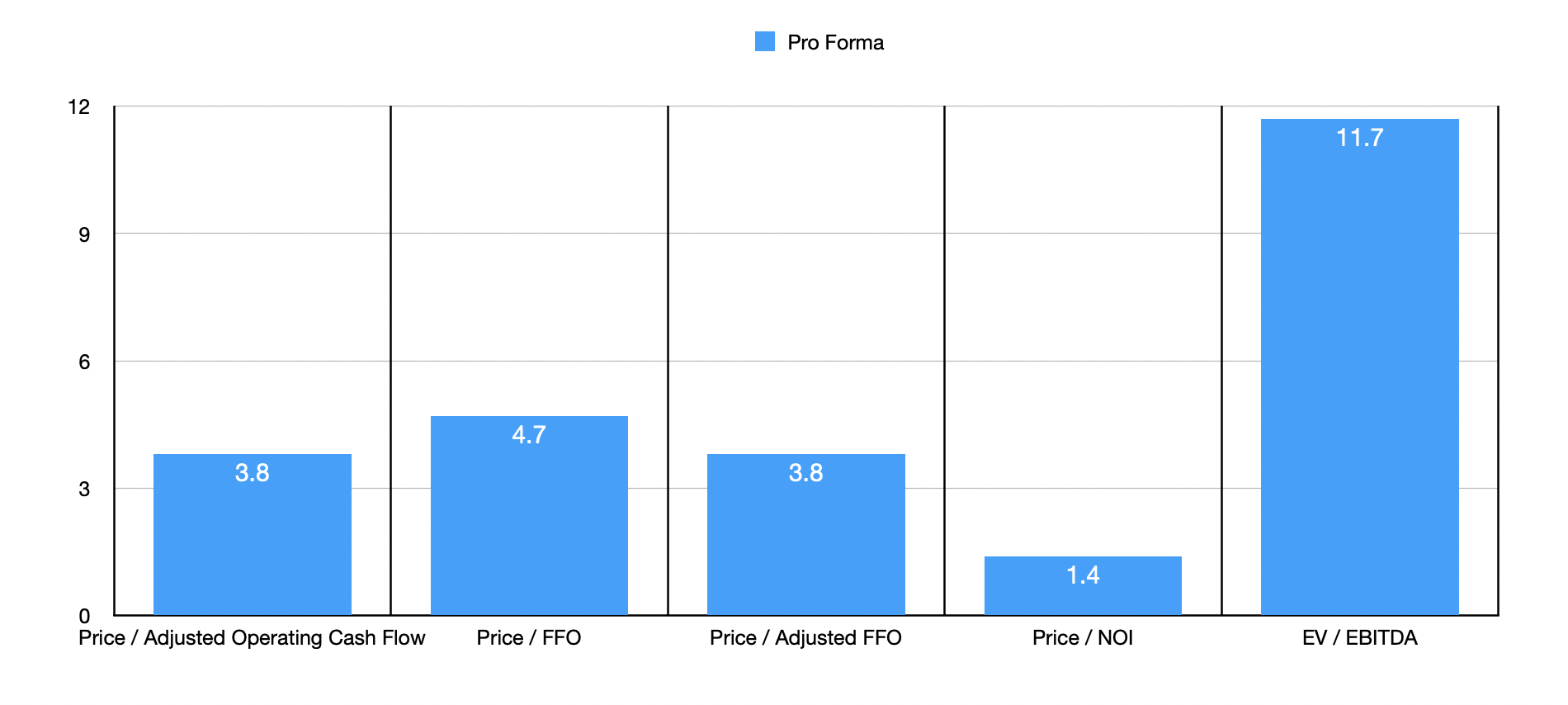

As you can see above, using data from 2022, the actual financial performance of the combined company will be worse on the bottom line, with the exception of when it comes to NOI and EBITDA, than if Office Properties Income Trust remained a standalone enterprise. On top of this, the combined firm will have net debt of $4.94 billion. On a pro forma basis, that translates to a net leverage ratio of 10.4. Management does believe that they can get this number down to 7.0 in the next few years. But that will likely require significant asset sales. Those who are bullish about the transaction may point out that stock and the combined company, given current prices, are quite cheap. This is true, as the table below illustrates. The one exception is the EV to EBITDA multiple, with the stark difference between it and the other metrics highlighting just how problematic debt is. In the event that management can pay the debt down considerably, the upside for shareholders could be tremendous. But we don't have any strong evidence that this can occur.

{kind=link}

Takeaway

Based on the data provided, I must say that I am not a fan of this transaction. At the end of the day, investors in Office Properties Income Trust are paying a massive premium for a business that will, for the most part, worsen its own cash flows. If the company was getting a much larger slice of the overall pie, then this assessment could very well be different. But following the completion of the transaction, investors in Office Properties Income Trust will own only 58% of the combined enterprise. This is in spite of bringing in about 69.2% of the combined firm's EBITDA, 67.3% of its NOI, and more than 100% of its other cash flows. The winner in this arrangement is, without a doubt, Diversified Healthcare Trust because of the greater stability the combined company will have compared to it going things alone. And also because of the robust distribution it will be granted. But because of how I see this entire transaction playing out and what will be left after its completion, I must rate both of these companies bearishly.

For further details see:

A Nightmare Deal Between Office Properties Income Trust And Diversified Healthcare Trust