RRC - A Path To A 20% Distribution Yield: Why I'm So Bullish On Range Resources

2023-09-27 16:43:49 ET

Summary

- Range Resources Corporation is a standout natural gas investment with strong production growth potential, deep reserves, and low breakeven prices.

- The company has a disciplined financial approach, including prudent debt reduction and conservative hedging strategies.

- While the natural gas market is volatile and risky, Range Resources has the potential to offer significant returns if gas prices trend upward.

Introduction

On September 25, I wrote an article titled 18% Yield Potential At $100 Oil: Why Canadian Natural ( CNQ ) Is My Favorite Oil Play . As bullish as that article title was, it was in no way clickbait, as North America is home to some truly impressive energy companies with the capability and plans to reward shareholders handsomely when energy prices are elevated.

After getting a lot of questions, I will dedicate this article to one of my favorite natural gas plays, the Range Resources Corporation ( RRC ) .

In addition to Antero Resources ( AR ) and Tourmaline Oil ( TOU:CA ), I believe Range Resources is one of the best natural gas stocks money can buy. Not only because I'm bullish on natural gas, but because its characteristics are truly special.

The company has deep reserves, very low breakeven prices, a healthy balance sheet , and the ability to reward investors with massive buybacks and dividends down the road.

However, be aware that natural gas stocks tend to be more volatile than oil-focused investments. My natural gas investments are part of my trading portfolio, not of my long-term investing portfolios. The exposure is also lower.

I am not saying that because I don't fully stand behind what I will tell you in this article. I'm saying this because elevated volatility can be an issue. Steep rallies often come with temporary setbacks. On top of that, the general bull case for natural gas is a bit weaker than for oil, as supply growth is stronger.

Having said that, I believe there's tremendous value in Range Resources and that prudent investors can double their capital if natural gas continues its uptrend.

So, let's get to the details!

Range Resources Is Truly Special

Range Resources is an operator in the Marcellus Basin, which is located in the beautiful Appalachia. It's also the reason why I often go with a header picture of that region whenever I cover an Appalachian-based energy company.

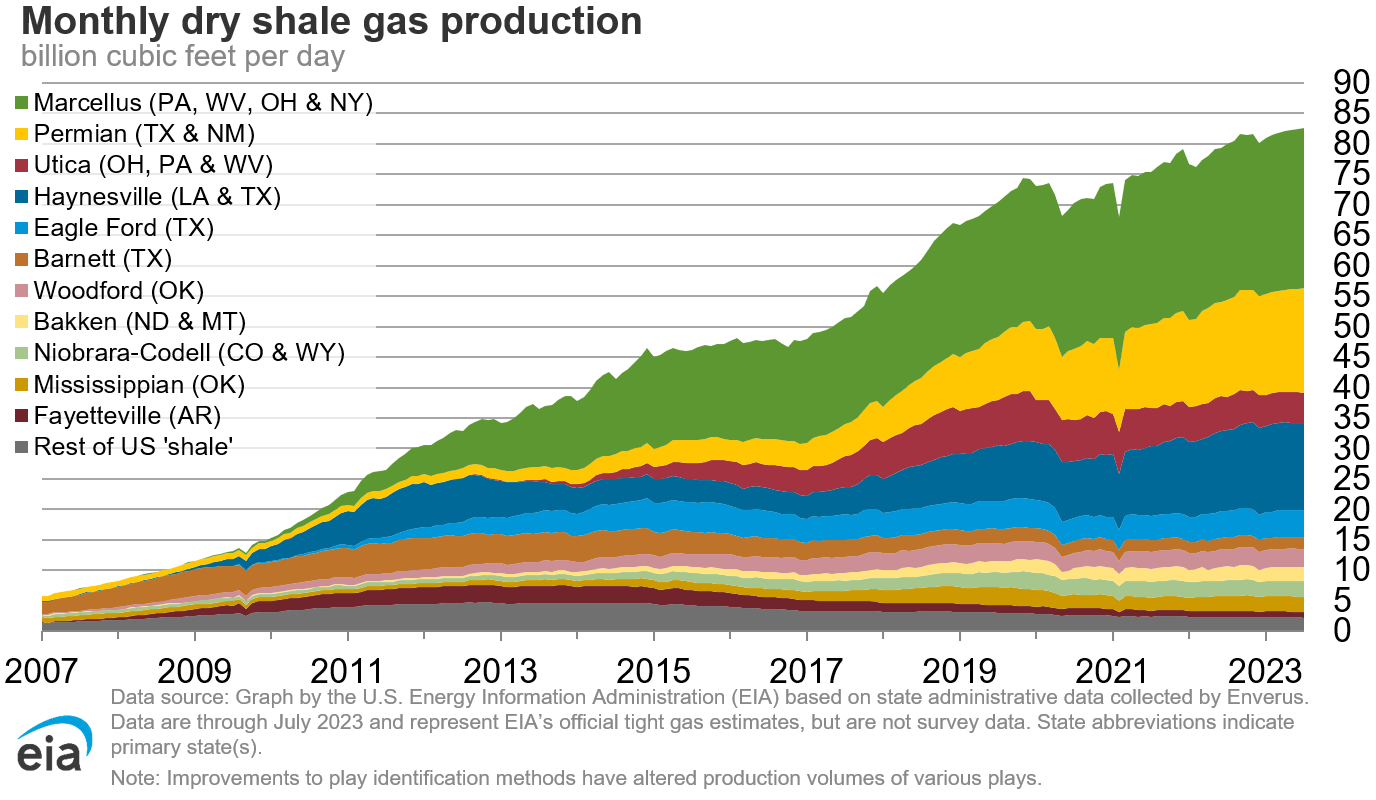

During the years of the Great Financial Crisis, the Marcellus wasn't a factor in global energy markets. At least not in natural gas.

Back in 2009, the U.S. produced roughly 10 billion cubic feet of dry shale gas per day. Now, that number is close to 85 billion cubic feet per day. The biggest player is the Marcellus basin.

Energy Information Administration

{kind=link}

Range Resources, with a current market cap of $7.7 billion, produces a big chunk of this total output.

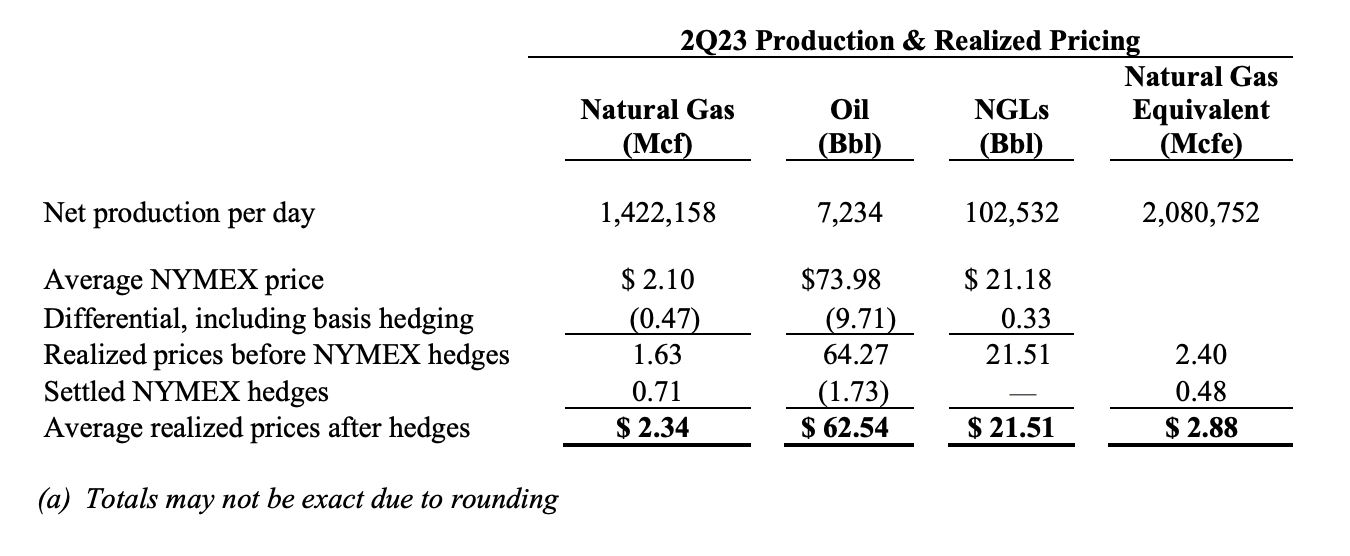

In Q2 2023, the company's net daily production averaged 2.08 billion cubic feet equivalent. 67% of this was natural gas. The remainder was natural gas liquids (103 thousand barrels) and oil (7 thousand barrels).

{kind=link}

In its second-quarter earnings call , the company noted that it plans for additional production growth.

The company's production strategy is expected to drive a significant sequential growth of approximately 30 to 50 million cubic feet a day in the third quarter, ultimately aiming for an end-of-year production level of approximately 2.2 BCF equivalent per day.

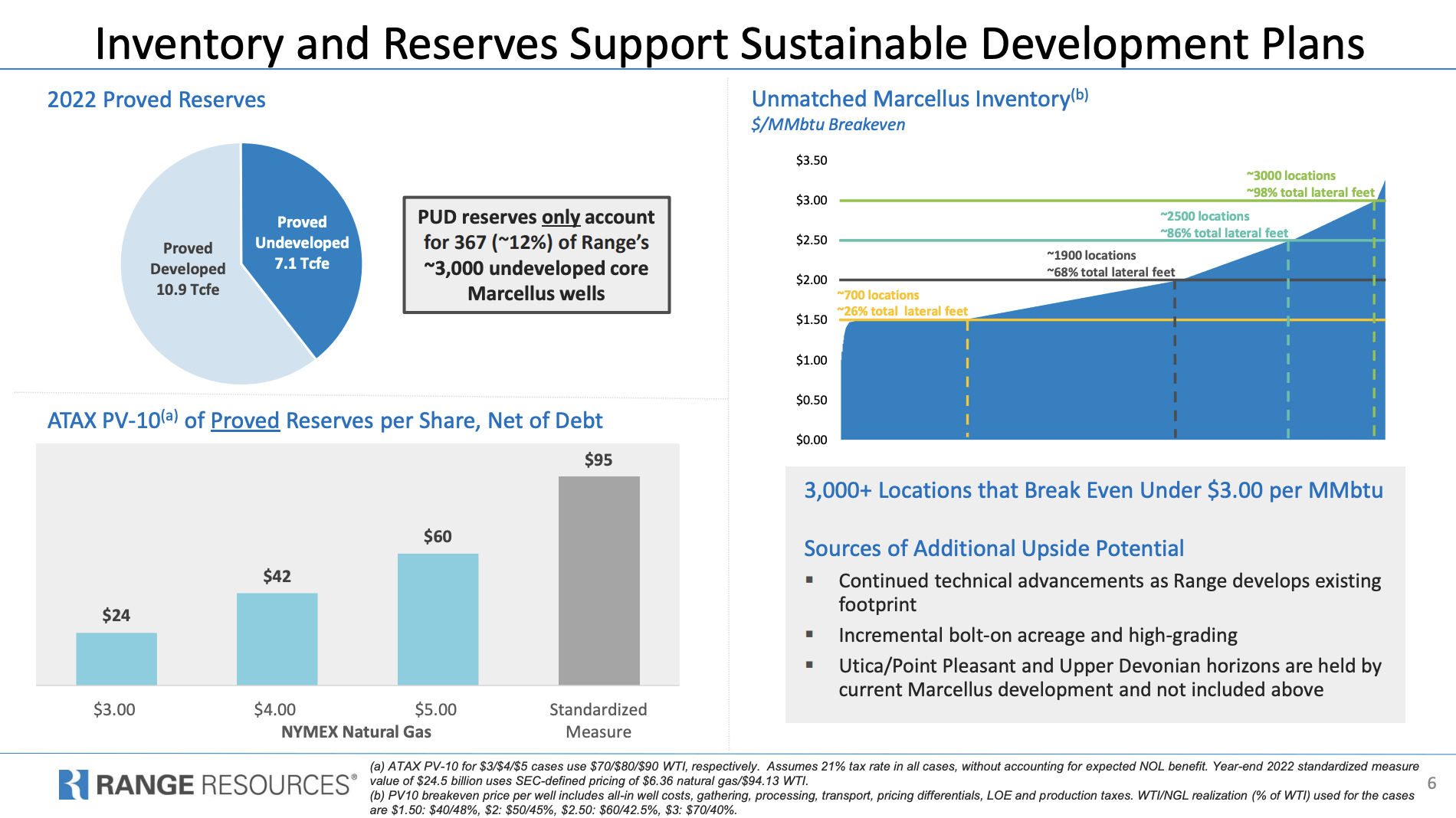

High production numbers are great but a small part of the thesis. Even more important is that the company has very deep inventories with very low breakeven prices.

The company has an almost unmatched inventory of 30 years' worth of production. It has 3,000 undeveloped drilling locations that are breakeven below $3.00 MMBtu, which is extremely low.

Almost two-thirds of its undeveloped drilling locations are breakeven below $2.00 MMBtu!

{kind=link}

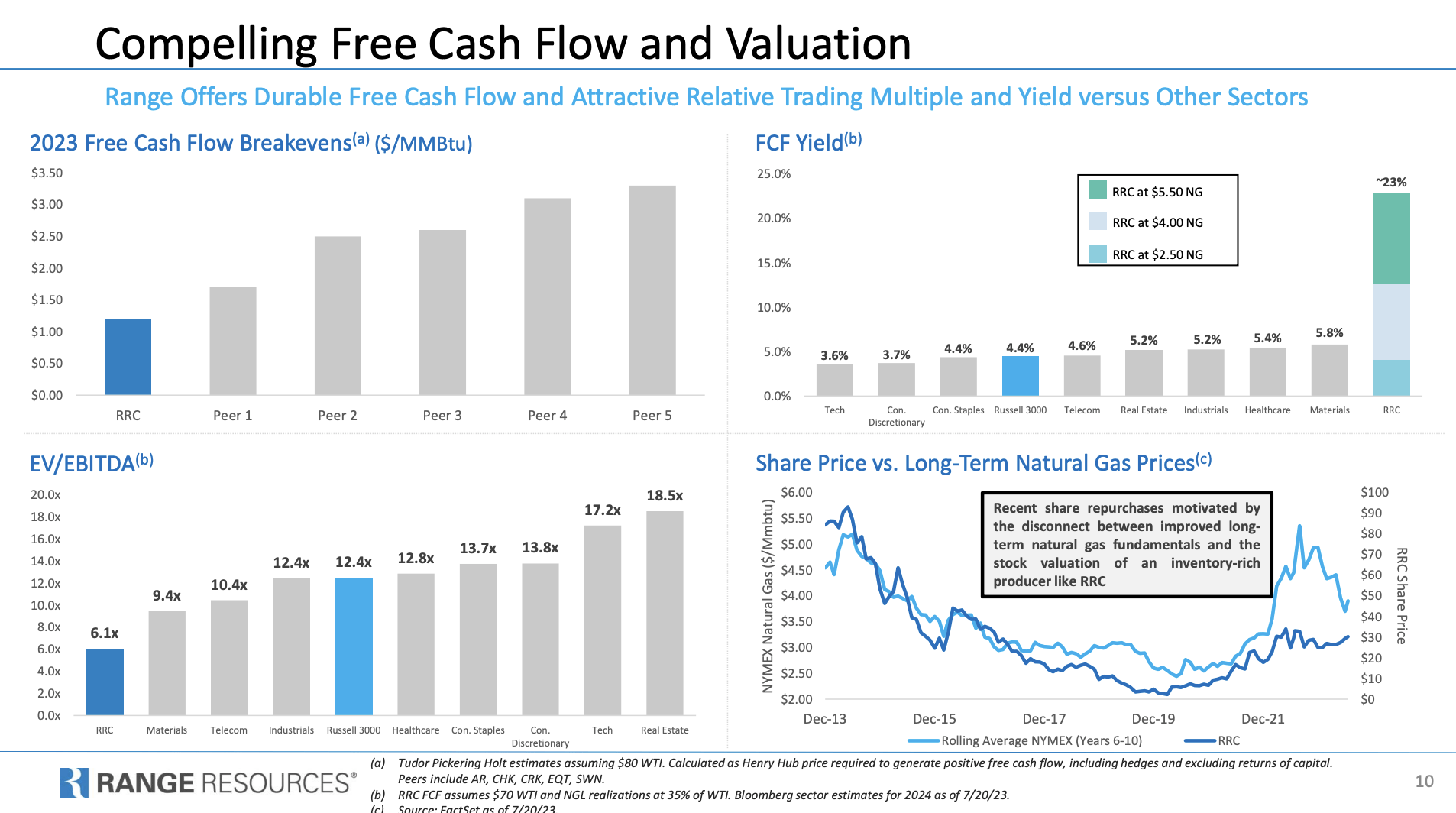

Even better, the company is the most efficient gas producer among its American peers. Looking at the chart below, we see that the company's free cash flow breakeven is slightly above $1.00 MMBtu.

{kind=link}

Not only does this mean that RRC turns into a cash cow at elevated natural gas prices, but it also means that it can still drill profitably when others are forced to reduce output to protect their balance sheets.

This comes with a huge margin of safety. For example, if natural gas prices decline, peers will start cutting output, lowering supply. That tends to stabilize prices before RRC gets into trouble.

Right now, we're once again in a period of decline rigs, as unprofitable producers are cutting output.

On a side note, half of the company's gas is transported to the Gulf Coast. Half of these volumes are turned into LNG for exports. I expect that number to rise dramatically over the next few years, allowing RRC to benefit from better pricing and longer-term contracts.

Going back to its operations, a part of its efficient operations is its advanced drilling process. In the second-quarter earnings call, the company emphasized the continuous improvements by its drilling teams, setting new records and achieving program milestones.

Notable achievements included drilling longer lateral wells, displaying increased lateral length by 5%, and achieving the longest laterals in the program's history, nearing 22,000 feet.

The average daily lateral footage drilled also surged by 42% compared to the 2022 full-year average, showing promising prospects for future development programs.

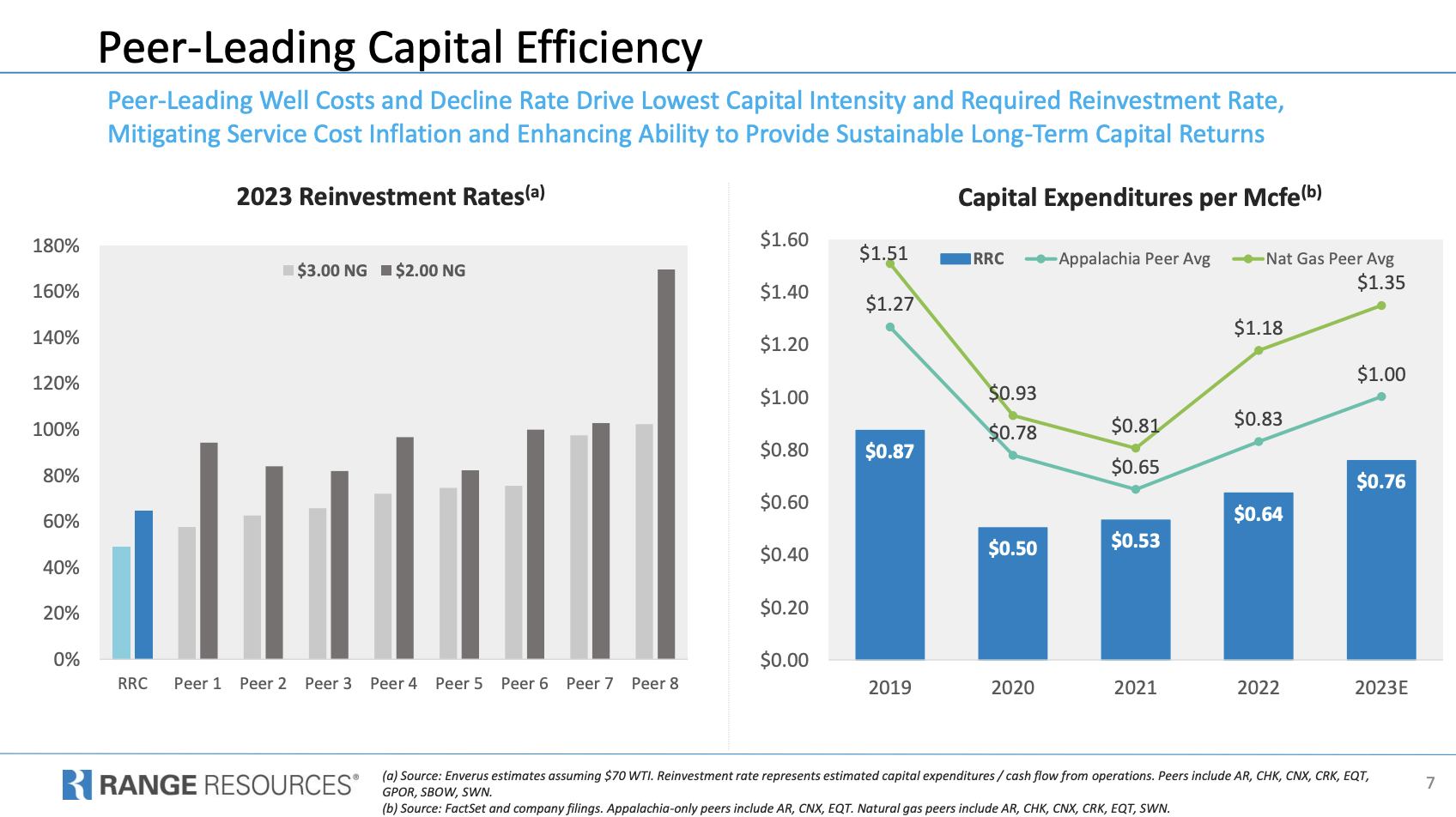

Related to the aforementioned comments and numbers, it is no surprise that the company has much lower capital spending per Mcfe.

{kind=link}

Thanks to these numbers, investors are increasingly benefiting from two major tailwinds.

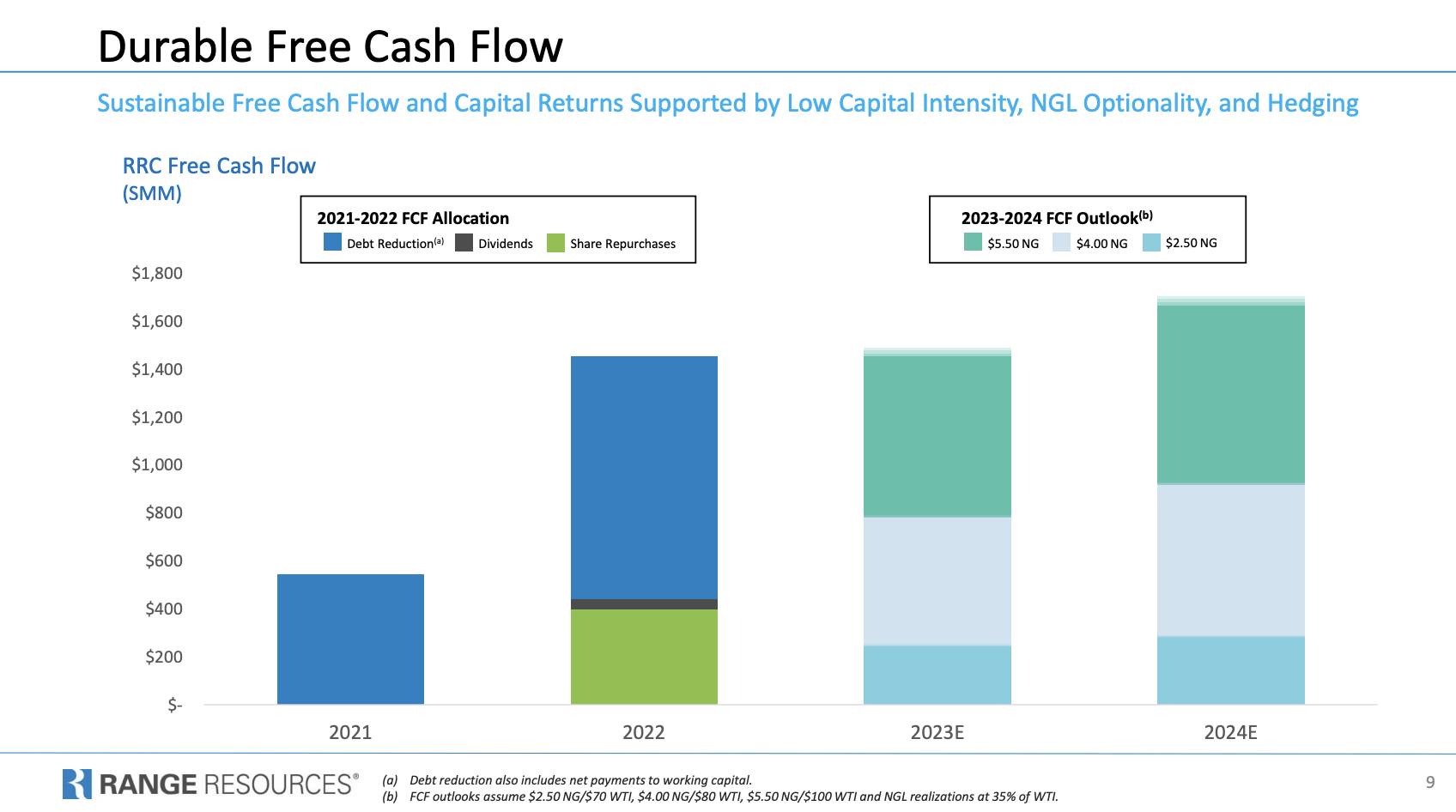

- In 2024, the company is capable of generating close to $1.8 billion in annual free cash flow at $5.50 MMBtu (Henry Hub). This translates to 23% of its market cap! The slide below with the Durable Free Cash Flow header displays these numbers.

- Thanks to an increasingly healthy balance sheet, most of this cash will end up in investors' pockets.

In 2021, when commodity prices were still subdued, the company spent all of its free cash flow on debt reduction. Last year, it generated more than $1.4 billion in free cash flow. Most of it went to debt reduction.

As a result, the company has just $1.6 billion in net debt, which is a mere $100 million above its target.

Next year, the company is expected to end up with $1.2 billion in net debt, which would translate to less than 1x EBITDA. Please bear in mind that analysts assume no major buybacks (they almost never do).

It is very likely that RRC will refrain from further lowering its debt after it hits its target, which is what I expect and one of the reasons why I like this stock so much.

Also, approximately 50% of the company's natural gas for the remainder of 2023 is hedged, with an average floor price of $3.42. For the year 2024, a similar strategy is in effect, hedging around 50% of natural gas at an average floor price of $3.70. This is achieved through a combination of swaps and collars, allowing for potential upside to approximately $5.50.

Additionally, the company initiated a modest hedge position for the year 2025, targeting an average price of $4.12 for natural gas.

{kind=link}

This is what the company said in its 2Q23 earnings call (emphasis added):

So as we start to think about what this future looks like, we think that there will be a greater appreciation for range of share value. We'll have that ability to return that value to shareholders, either through expansion of the dividend in the future, additional share repurchases or either further debt reduction based upon the ability to throw off free cash flow through these cycles in the future , while maybe some of the other either peers or other basins have a difficult time doing so.

The current dividend yield is 1%, which is nothing to write home about.

However, if energy prices rise, the company is in a great position to reward investors with double-digit distribution yields consisting of both dividends and buybacks.

Valuation & Outlook

Putting a valuation on a commodity-driven stock is always tricky. After all, energy prices have a massive impact on earnings in the case of RRC and its peers.

With regard to the natural gas outlook, the company is bullish.

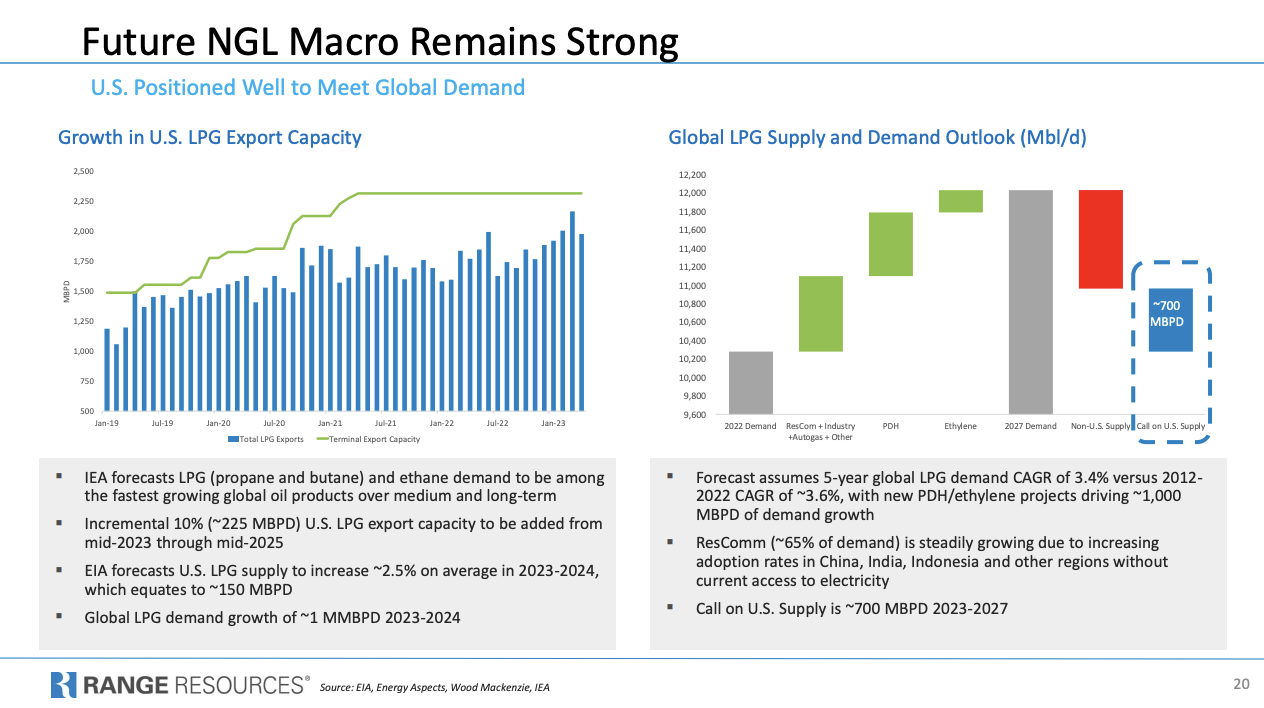

Historically low prices observed in the second quarter are expected to improve later in the year, driven by robust LPG exports from the U.S.

The growth in exports, in conjunction with moderating supply growth, is anticipated to restore storage levels to balance later in the year.

During its earnings call, the company also highlighted the positive trends in ethane prices and strong demand, positioning the company well to capture both international and domestic opportunities, supporting their NGL guidance range for the year.

{kind=link}

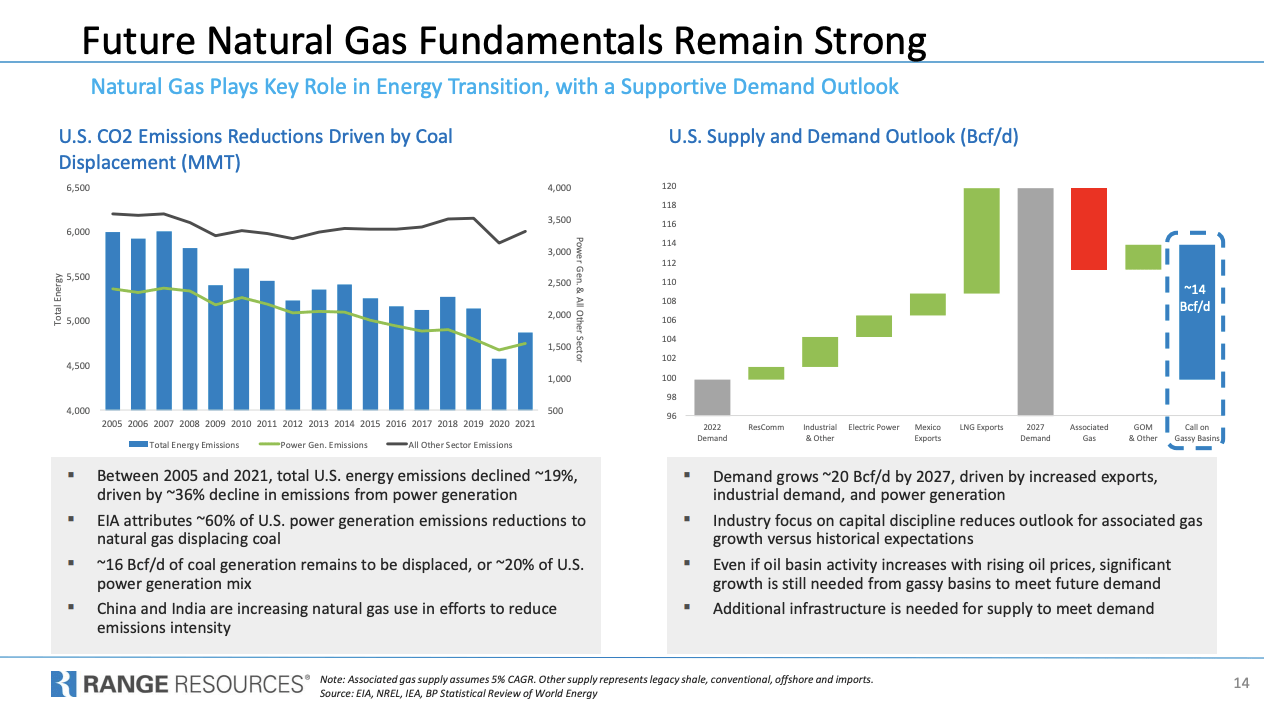

On top of that, the company sees a longer-term divergence between demand and supply growth, driven by massive LNG export capacity expansions and a shift from coal to natural gas - among other reasons.

{kind=link}

Once economic growth rebounds, I expect this trend to be amplified.

Given that the company has a 23% free cash flow yield at $5.50 Henry Hub, I believe that the stock has the potential to double once we reach these gas prices.

I do not expect that to happen over the next few months. However, on a longer-term basis, I'm very bullish on natural gas and expect long-term elevated prices to support aggressive buybacks, further debt reduction, and related improvements that pave the way for a long-term (albeit volatile) uptrend.

If I didn't own AR shares, I would be a buyer of RRC at these levels.

However, as I said in the introduction, RRC and its peers are volatile. Be aware of these risks and always do your own due diligence.

Takeaway

Range Resources Corporation stands out as a prime natural gas investment.

RRC shows remarkable production growth potential with deep reserves and low breakeven prices, making it a standout in the natural gas sector.

Its disciplined financial approach, highlighted by prudent debt reduction and conservative hedging strategies, adds to its attractiveness to investors.

Although we're dealing with a very volatile and risky market, I firmly believe that RRC has the potential to offer significant returns, especially if gas prices trend upward in the future.

However, it's crucial to conduct thorough research and consider the risks involved before making investment decisions in this dynamic sector.

I am mainly buying oil-focused stocks and will add to my smaller natural gas trades on weakness.

For further details see:

A Path To A >20% Distribution Yield: Why I'm So Bullish On Range Resources