TELZ - A Pulse At Tellurian Once Again

Summary

- Gunvor extends SPA another month in a row.

- Tellurian targets $6 billion in equity from strategic partners.

- High equity or sponsored deals will define next LNG wave to meet LNG shortfall.

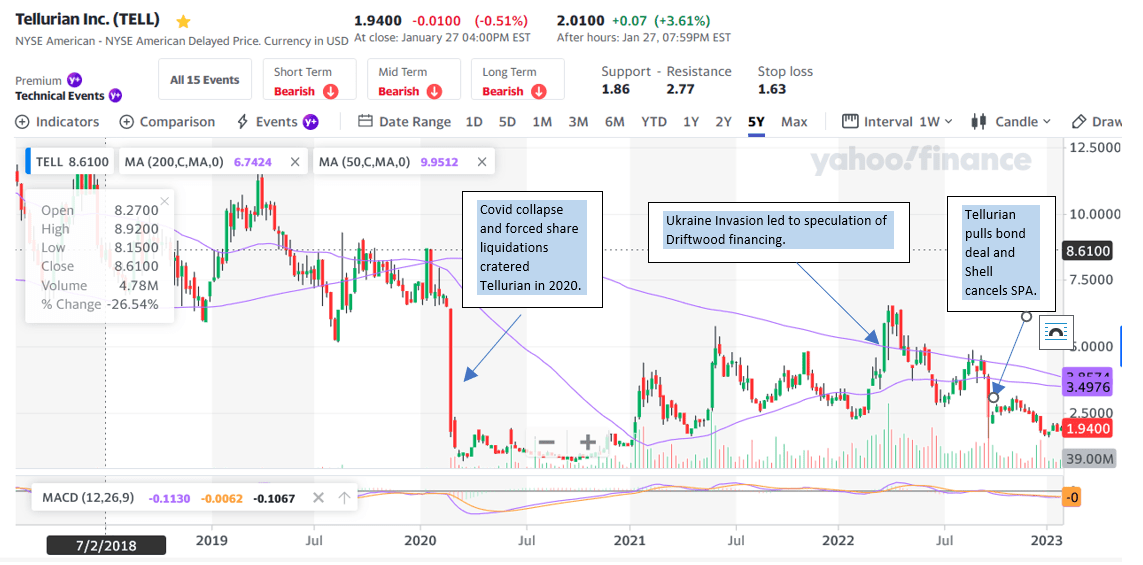

Tellurian Inc., (TELL) the LNG disruptor led by Charif Souki, Martin Houston and Octavio Simoes, collapsed in September following its decision to withdraw its $1 billion high yield bond offering with warrants following Federal Reserve Chairman Jerome Powell's "pain speech" at Jackson Hole, Wyoming, in late August. TELL has experienced heavy speculation from both bulls and bears which has made Tellurian's price moves highly volatile whenever prospects for financing Driftwood rise and fall. The chart below of Tellurian over the last five years show the volatility of TELL stock.

Tellurian stock chart. (Yahoofinance.com and IGA research)

{kind=link}

Friday's announcement that Gunvor extended its SPA (sales purchase agreement) by another month suggests to us that Tellurian might be positioning itself to line up the $6 billion in equity capital which when combined with $8 billion in debt should fully fund Driftwood's Phase one project. Why would Gunvor spend the time and money to extend the SPA for one month unless they see a pathway to funding Driftwood? Nondisclosure agreements also likely allow Gunvor to see nonpublic information.

Background:

Tellurian is a speculative stock that we have written about and recommended based on Charif Souki's experience as a Co-founder and Co-CEO of Cheniere Energy Inc. ( LNG ) and who twice raised significant capital for two Cheniere facilities. The first project was its initial gasification unit in 2006 before abundant US natural gas was discovered. The discovery of massive cheap US natural gas turned the economic logic of the first facility upside down. Souki then reversed Cheniere's business model and Souki successfully helped fund Cheniere's liquefaction facility at Sabine Pass which took cheap US natural gas, liquefied it, and shipped it abroad. Souki was instrumental in making Cheniere the largest pure LNG exporter in the country with a market capitalization of $37.36 billion for Cheniere Energy Inc. and $26.04 billion for Cheniere Energy Partners, L.P. ( CQP ).

What drove Tellurian to below $2 a share in September and year end can be attributable to a range of issues. Specifically, the cancellation of the SPAs with Shell and Vitol in September, the company not having large off take agreements with foreign countries, interest rates having risen so rapidly and or having the high yield window shut in September. However, this report will address the overarching fact that the financing model for large LNG facilities has evolved over time. And today large equity commitments are now needed to finance large liquefaction facilities.

Tellurian has a very experienced team in Charif Souki, Martin Houston, and Octavio Simoes. Their model differs from traditional liquefaction financings since Tellurian seeks to capitalize on the spread between cheap US natural gas and expensive international natural gas. If Tellurian executes on its financing, Tellurian looks to be a home run.

Here is a rough assessment of the value and return profile of Tellurian. Tellurian can be divided into two separate businesses: the upstream business and Driftwood LNG, the liquefaction business.

Their upstream business can be valued as the sum value of their wells, land, pipelines, and the cash flow that can be generated from selling its natural gas. The upstream business is a growing business and TELL intends to own its own natural gas, sell it abroad, and reap the large merchant spread.

Based generally on the analyses I have reviewed including from Morgan Stanley and Dustin Dollar's, at the current depressed natural gas price of $3.00/mmBTU for Henry Hub, TELL should generate about $250mm in EBITDA in 2023. With 653 million shares at $2.00 per share a valuation of $1.3 billion seems fair with little value attributed to the Driftwood facility. This summer, when Henry hub was closer to $6.00, expected EBITDA for 2023 was closer to $400mm. That implied an upstream value of $1.6 billion or about $2.54/share. During the summer, hopes were much higher for Driftwood so a share price range in of $3-5/share was appropriate.

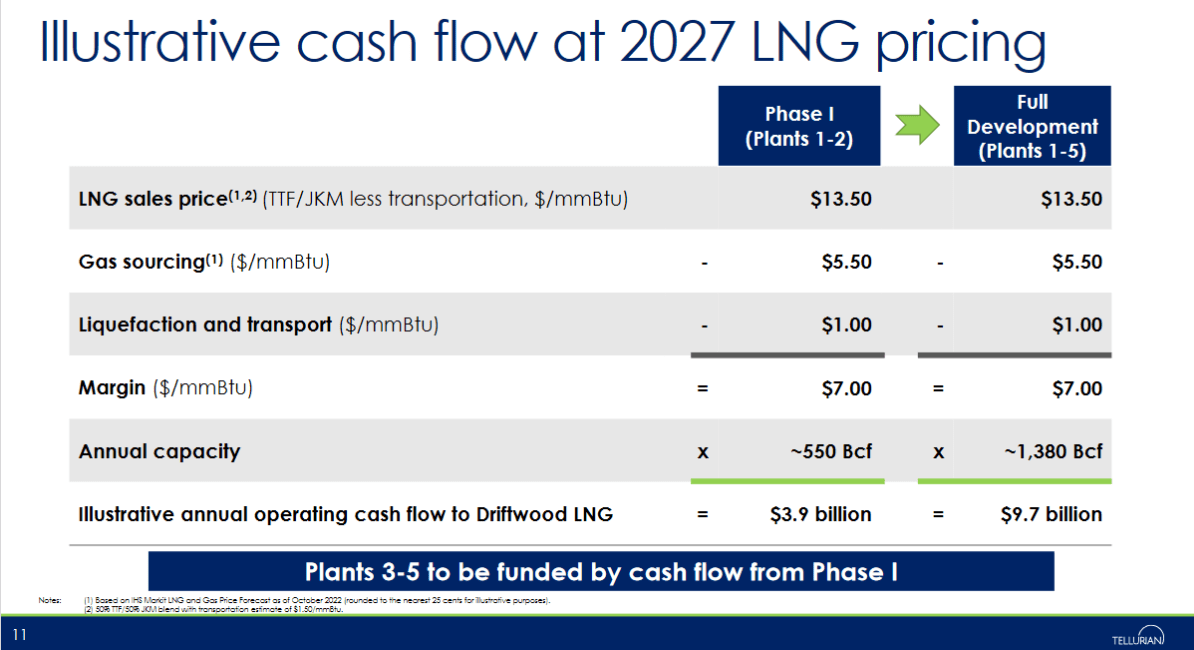

The asymmetric upside or "lottery ticket" in Tellurian's valuation is Driftwood. The slide below from Tellurian's November 2022 corporate presentation shows the company generating $3.9 billion in cash flow/yr with Phase 1 completed and $9.7 billion at full development. Phase 1 should be operating in 2027 and full development around 2029.

The slide below is from Tellurian's investor presentation.

Driftwood estimated cash flows (Tellurian November 2022 corporate presentation.)

{kind=link}

With EBITDA growing from $250 million to $4 billion implies the market capitalization growing from today's $1.2 billion to $16 billion at four times 2027 cash flow. However, the bulk of the cash flows in 2027 and 2028 will be directed to further building the facility in phase 2 from 11 MTPA to 27 MTPA. Consequently, Tellurian becomes a leveraged play on global natural gas prices in 2029 and after. If the large spread remains, Tellurian will be a home run, but getting Driftwood financed is the proverbial fly in the ointment. Tellurian's share price will be highly correlated to the probability of Driftwood Phase 1 getting financed.

A Deep Dive on Financing Driftwood

Jordy Watson, of Watson Project Services, LLC, helped us detail our argument that United States LNG is about to experience a new wave of LNG facilities construction to address a global shortage in LNG. Furthermore, Tellurian's Driftwood is well positioned to be funded as the company seeks $6 billion in equity finance and $8 billion in debt to build Phase 1 (11 MTPA) of Driftwood LNG.

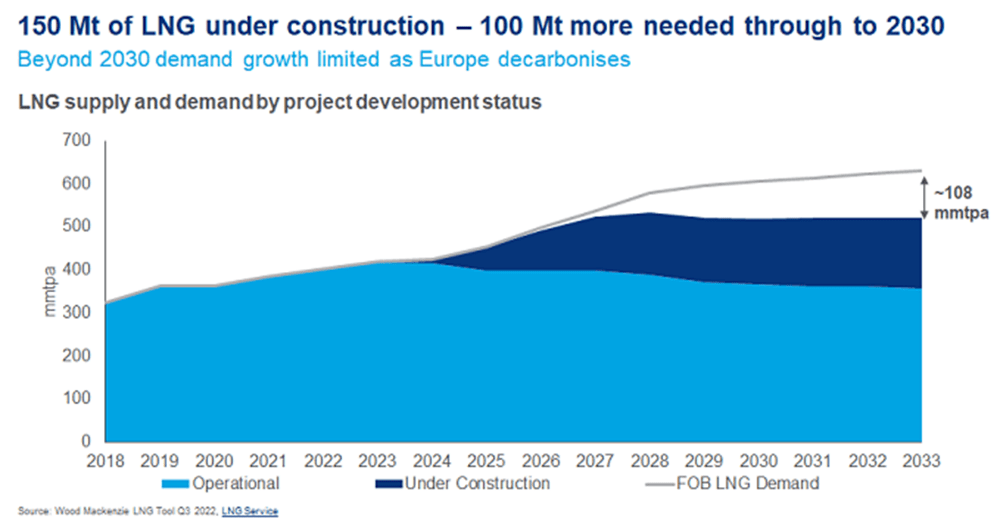

Wood Mackenzie estimates an additional 100 MTPA of LNG is needed through 2030. The chart below shows the needed additional 100 MTPA gap between existing projects, projects under construction, and planned projects -- where Driftwood fits.

Wood Mackensie Long Term LNG forecast (Wood Mackensie December 2022 letter, Simon Flowers)

{kind=link}

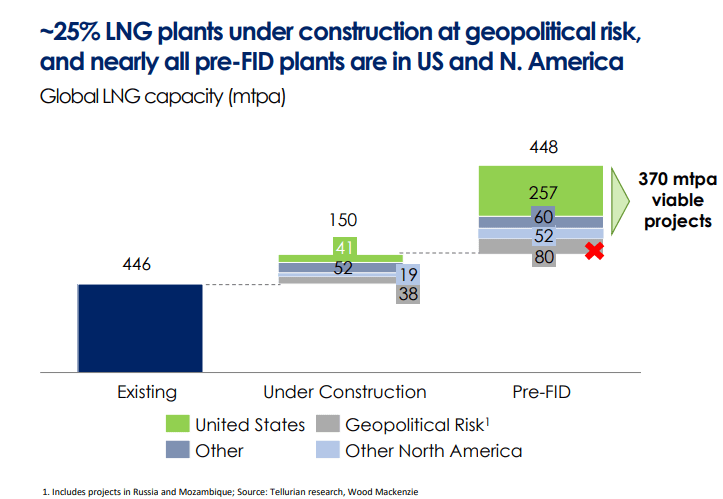

With the invasion of Ukraine by Russia, natural gas became a weapon of war as gas prices spiked 600% and the concept of energy security became an existential priority. According to Tellurian, 38 MTPA of projects under constructions are at geopolitical risk. These projects are principally in Russia but also Mozambique. The Tellurian research chart below suggests that 25% of LNG plants under construction are at risk of not being brought to market as planned, leading to further uncertainty in global markets.

LNG projects at risk (Wood Mackenzie and Tellurian)

{kind=link}

Since there are a limited number of viable pre-FID projects globally, the US will be called upon to provide a disproportionate amount of LNG to world markets. Three major projects which can go some way towards narrowing the supply gap are Tellurian's Driftwood LNG, Next Decade's Rio Grande, and Sempra's Port Arthur with a combined 80 MTPA at full capacity. Highlighting the prospects for a near term LNG investment cycle, Baker Hughes expects to see 65 MTPA - 100 MTPA of LNG projects secure FIDs in 2023, further supporting Tellurian and our belief that these projects are probable this year.

The benefit of the Driftwood project is that it does not have sovereign risk and it is the most advanced pre-FID project in the market. The more Driftwood builds its foundation, the more the project de-risks and the shorter the time to market. Driftwood offers strategic investors (Integrated Oil Companies, domestic E&Ps like Chesapeake Energy Corporation ( CHK ), Southwestern Energy Corporation ( SWN ), Antero Resources Corporation ( AR ), Comstock Resources, Inc. ( CRK ), EQT Corporation ( EQT ) and Devon Energy Corporation ( DVN ), as well as off takers like counterparties from India, Europe and South Korea that wish to access a low-cost integrated LNG project.

We envision strategic partners as those who will benefit from utilizing the Driftwood LNG facility and enhance the equity funding Tellurian seeks. The logic of a US E&P investing in Driftwood - at the project level - allows for it to sell its gas at premium international prices. Many of the afore E&Ps have stated an interest in funding an LNG facility. IOCs can allocate to Driftwood and increase exposure to LNG and capitalize on its decarbonization characteristics. Foreign entities (companies and countries) can address their energy security needs by securing LNG offtake agreements. Furthermore, corporations can enhance their decarbonization goals by securing LNG offtake contracts to facilitate a replacement of coal fired electric power plants with gas fired plants. India is a natural prospect for such an agreement. This video shows Tellurian CEO Octavio Simoes suggesting that Tellurian is working with India's Energy Minister Hardeep Puri on developing such an off take agreement to help India with its enormous growth prospects and its challenging air pollution problem. Building on this, as reported in The Economic Times in October 2022, Indian Oil Corp was in discussions for potential Driftwood equity and offtake.

Evolution of the USLNG Financing Model:

The first wave of LNG liquefaction builds followed Cheniere Energy, Inc. where the company converted its original regasification facility to a liquefaction facility when US fracking established US LNG as the cheapest natural gas in the world.

The second wave of LNG builds was with greenfield projects supported by long term contracts and modest margins to the liquefaction facility owner. With competitors pressing low-cost facilities, margins became so tight that interest from private equity has disappeared since 2019. The absence of private equity to finance liquefaction projects curtailed the available supply of new LNG forcing a reliance on expansion projects and sponsor equity projects. We believe if an evolution of the US LNG financing model doesn't occur, the market will be acutely short for the balance of this decade. It is our view, the current Tellurian model of using strategic equity partners to fund the equity component of greenfield projects is the new sustainable model.

Supporting this view is the partnership between ConocoPhillips and Sempra Infrastructure on Port Arthur LNG Phase 1 , in which ConocoPhillips (COP) will become a 30% equity partner and secured 5 MPTA of LNG over 20 years. Tellurian was early in identifying this model for the next wave of projects. Tellurian's pursuit came at a time when investors believed the markets would stay oversupplied for years and consequently did not want to risk their balance sheets. Now, Tellurian is back with the right model at the right time. The confluence of renewed focus on energy security, a critically undersupplied market, potential partners flush with cash (as demonstrated below), and the decarbonization mandates driving capital investments, positions Tellurian to succeed.

Oil and Gas Majors as Partners have Cash:

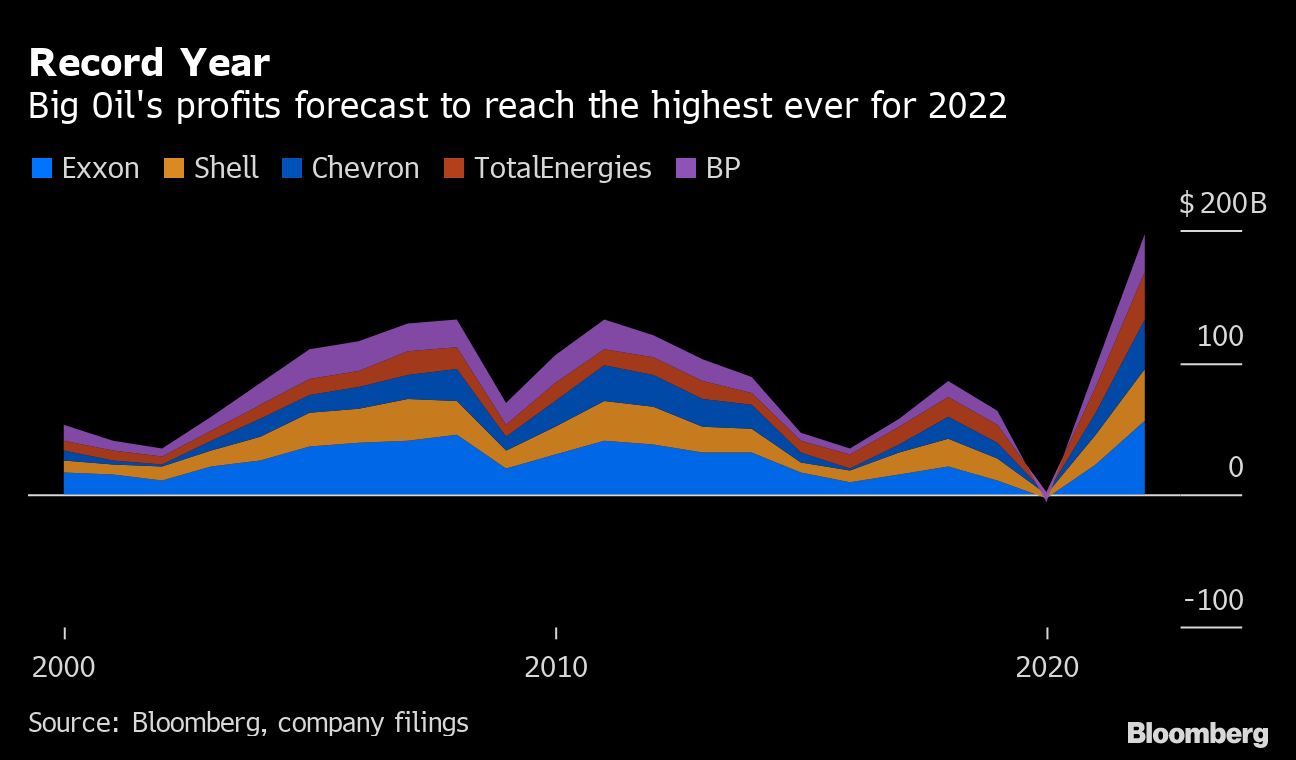

The chart below shows Exxon Mobil Corp. (XOM), Chevron Corp. (CVX), Shell Plc (SHEL), TotalEnergies SE (TTE) and BP Plc (BP) reaped almost $200 billion collectively last year. These companies improve their environmental profile by funding LNG as it is a transition fuel and avoid criticism for returning capital to shareholders.

big oil profits for 2022 (Bloomberg)

{kind=link}

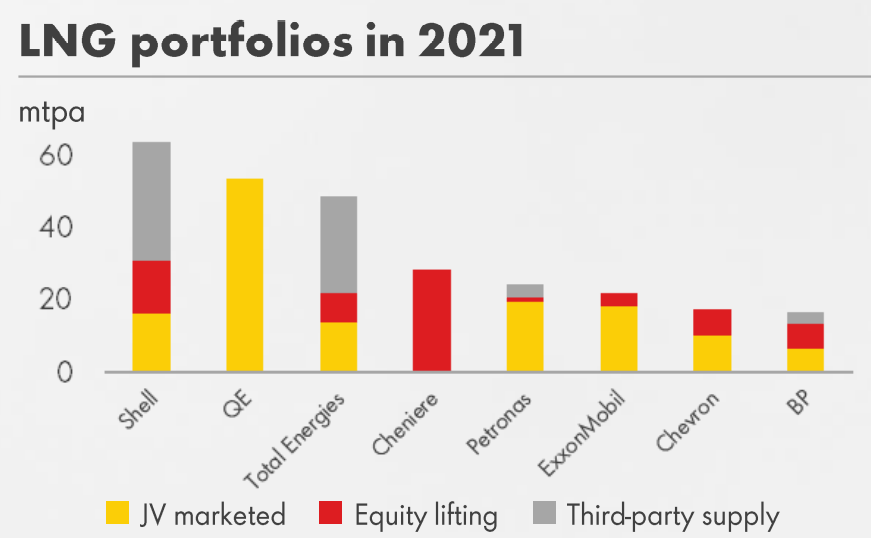

The chart below shows the allocations of LNG in the energy portfolios of eight of the largest operators in the LNG business, many of whom would be interested in Driftwood equity as described earlier. LNG is an energy transition fuel which should enjoy significant capital investment to transition to cheaper and cleaner energy based on cheap US natural gas.

Big oil LNG share of energy assets (Shell annual LNG report)

{kind=link}

Conclusion:

Friday's announcement of Gunvor extending its SPA agreement for another month is compelling evidence in my view that a sophisticated counter-party is maintaining their option to see if Tellurian can secure sufficient funding to reach its conditions precedent of issuing Full Notice to Proceed to Bechtel (FNTP). This suggests that Tellurian is positioning itself to receive enough equity to secure all of its long lead time equipment to build the Driftwood liquefaction facility.

The scenario we see as most probable is some confirmation from India that it will secure a meaningful offtake agreement and provide equity capital to own a portion of Driftwood LNG. With a large equity commitment e.g., $2 billion, Tellurian would likely lock down US E&Ps for another $2 billion, and International Oil Companies and or private equity could combine to give Tellurian the $6 billion in equity capital it seeks. Then the company working with a syndicate of banks will fund about $8 billion in debt. This debt to equity ratio is more conservative than what the company tried in September.

February 6-8, at India Energy Week 2023, Tellurian CEO and President Octavio Simoes will be a keynote speaker. This would be an opportune forum for an update or an announcement regarding Tellurian supplying LNG to India or Indian companies. This could lead to a rapid move in TELL stock much like last spring following the invasion of Ukraine when natural gas prices spiked, and capital flowed to investments which benefit from the structural deficit. As the deficit is expected to persist, now is an opportune time for forward-looking companies or governments to back Driftwood and Tellurian shareholders appear well positioned to reap the benefits of such. While the invasion implied Europe would be a natural buyer of US LNG, Europe demurred on the US LNG option pinning its hopes on a cleaner transition to hydrogen. [We are dubious about Europe's uber green agenda where it prematurely shut nuclear and coal burning plants in anticipation of a flawless transition solely to solar and wind. Sadly, Europe has paid a huge price for its ill-conceived energy policy.] Hopefully, India, South Korea, China, Japan, or some open-minded European countries will back the Driftwood plant.

Both Tyson Halsey, CFA and Jordy Watson are Tellurian shareholders.

For further details see:

A Pulse At Tellurian Once Again