OR - A Reality Check For Victoria Gold

2023-09-25 03:45:52 ET

Summary

- We check in on Victoria Gold's updated technical report for the Eagle Gold mine and the latest quarterly results.

- The acquisitions of Brewery Creek and Raven drilling are positive developments for the company.

- It remains to be seen if there is a case for long-term value creation for shareholders.

- Nevertheless, there is a bull case to be made for a shorter time frame.

Following its failed run at ATAC Resources earlier this year, Victoria Gold ( OTCPK:VITFF ) VGCX:CA announced the acquisition of the Brewery Creek property in the Yukon on September 14 in what's probably fairly described as a distressed sale. Unfortunately, the market only took a passing interest in this deal and swiftly re-focused on its bearish sentiment about the company -- a sentiment we predicated in this article back in January.

The Brewery Creek acquisition was not the only noteworthy news item about Victoria Gold during the time since said article. The company also released an updated technical report on its Eagle mine, published exploration results for the emerging Raven deposit, and reported operational and financial results for two quarters. Plenty of material to weigh and update our view of this gold miner; and perhaps even ponder a change of sentiment.

Let's start with our updated charts after the Q2 results.

Operational And Financial Performance

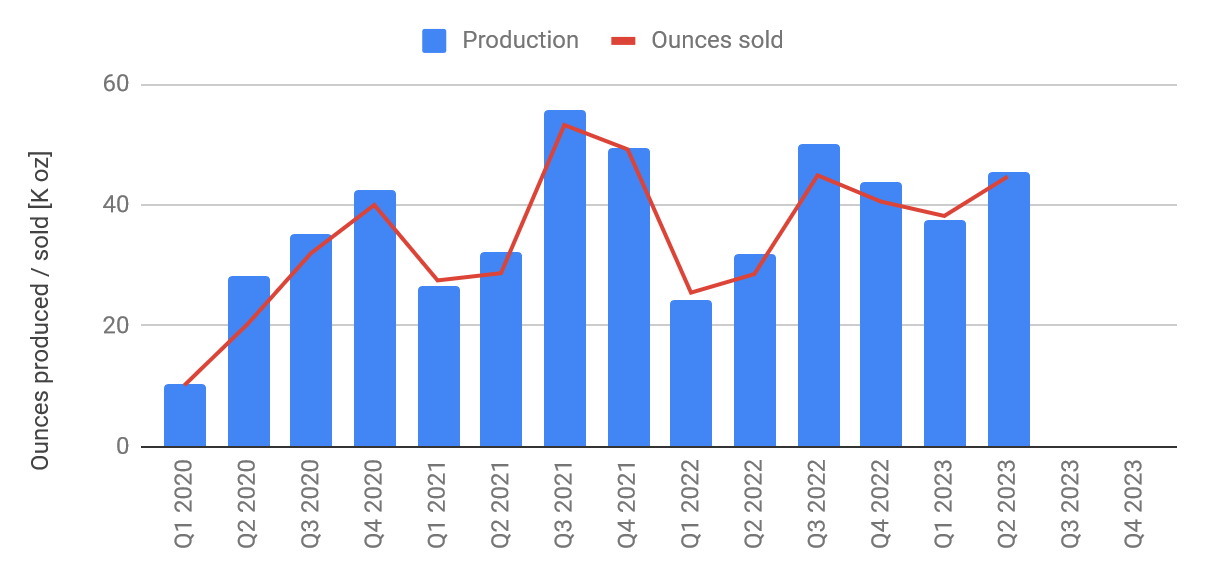

Mine performance at Victoria Gold's Eagle mine is ticking along as could be expected in the first two quarters of the year. This is a cold climate heap leach operation, and hence production is heavily weighted towards the second half of the year. The company has kept winter down time at the mine to a minimum this year and Q1 stacking rates exceeded the corresponding quarters of previous years.

{kind=link}

Mine operations (company filings, author's work)

Gold output has also held up well, thanks to the strong performance at the mine during winter and leaching kinetics that seem to show less sensitivity to the cold season than originally predicted. The typical dip in gold production during Q1 and Q2 is barely visible this year.

{kind=link}

Gold production (company filings, author's work)

Normally, this would bode well for the stronger quarters of this year but unfortunately, the East McQuesten wildfire caused disruptions this summer and the company has already flagged total annual production at the low end of the guided range of 160-180Koz, and all-in sustaining costs near the high end of the guided range of US$1,350-1,550/oz.

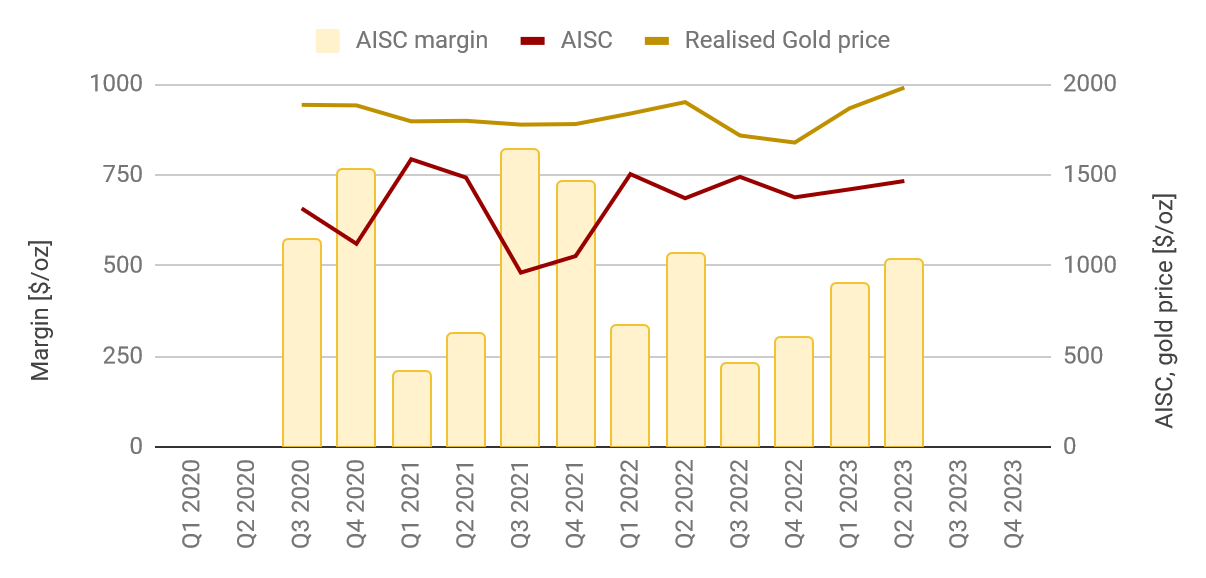

Nevertheless, margins have been trending up again, printing roughly $500/oz in Q2.

{kind=link}

Margins (company filings, author's work)

These margins also found their way into the next chart showing free cash flow generated at the Eagle Gold mine. In fact, Q2 was the best quarter in this regard during the mine's operating history so far.

{kind=link}

Free cash flow (company filings, author's work)

Unfortunately, only a small portion of the cash flow generated during the first two quarters of this year has found its way to the balance sheet. Interest payments, the settlement of call options that had formed part of the construction financing, and funds for near-mine exploration have all taken their toll. And while we note an increase in working capital, we also note practically no reduction of the total debt load so far this year. In fact, after tickling the $200M line at the end of 2021 total debt (red line in the chart below) has trended up again and printed $264M at the end of Q2.

{kind=link}

Balance sheet (company filings, author's work)

A Quiet Farewell To Project 250

Victoria Gold filed an updated technical report for the Eagle mine in April which made for interesting reading material on a recent rainy weekend. This report provided plenty of detail, and it was good to see that the real-life experience from operating the mine had translated into the adjustment of several input parameters for the economic model of the mine.

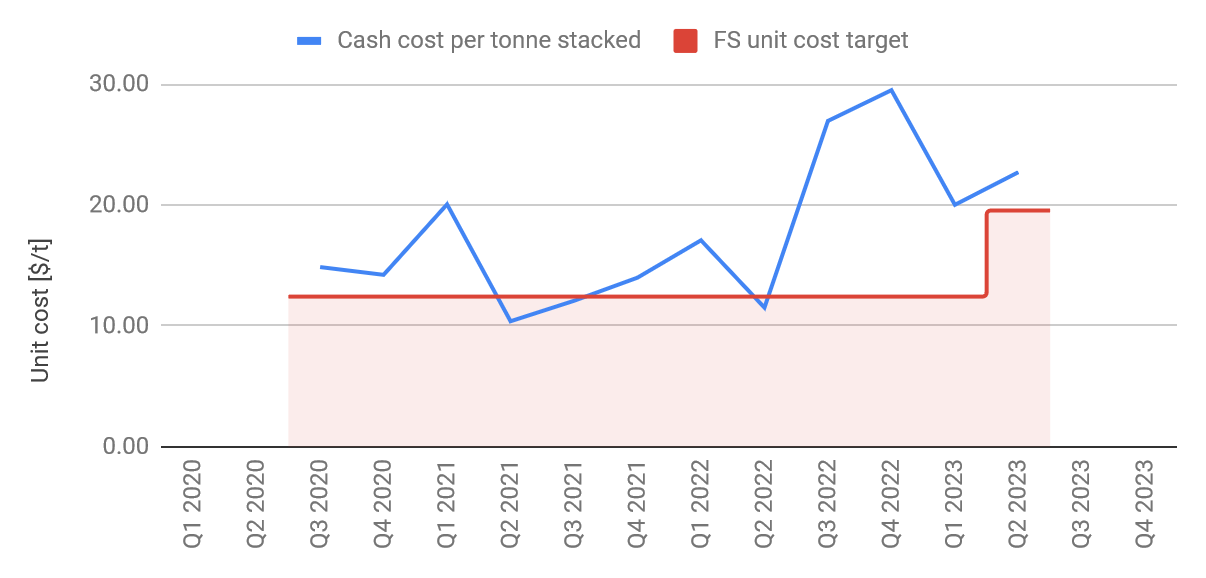

One such parameter that we have followed closely is the unit cash cost per tonne stacked. This is a central number in the cost accounting for any bulk mining heap leach operation, and we have always found it unfortunate that the company does not spell this metric out in its quarterly MD&A documents. Nevertheless, this unit cost can be back-calculated from other reported items, and the chart below shows how Victoria Gold only managed to achieve the feasibility assumption twice on a quarterly basis during three years of operations. This unit cost assumption was increased to $19.55/tonne stacked in the latest technical report, a 57% increase and a much more realistic assumption judging from past experience. We note that actual unit costs already exceeded this new assumption for the past four quarters, and it will be interesting to see if Victoria Gold will manage to live up to its latest expectations.

And talking of costs, we note that the updated technical report calculates average all-in sustaining costs for the remaining mine life to $1.114/oz. This seems like a very ambitious goal, and just like the unit cost discussed above, it has only been achieved in two quarters in three years of operations so far; and that was before the recent inflationary pressures that have driven cost increases throughout the industry.

{kind=link}

Unit costs (company filings, author's work)

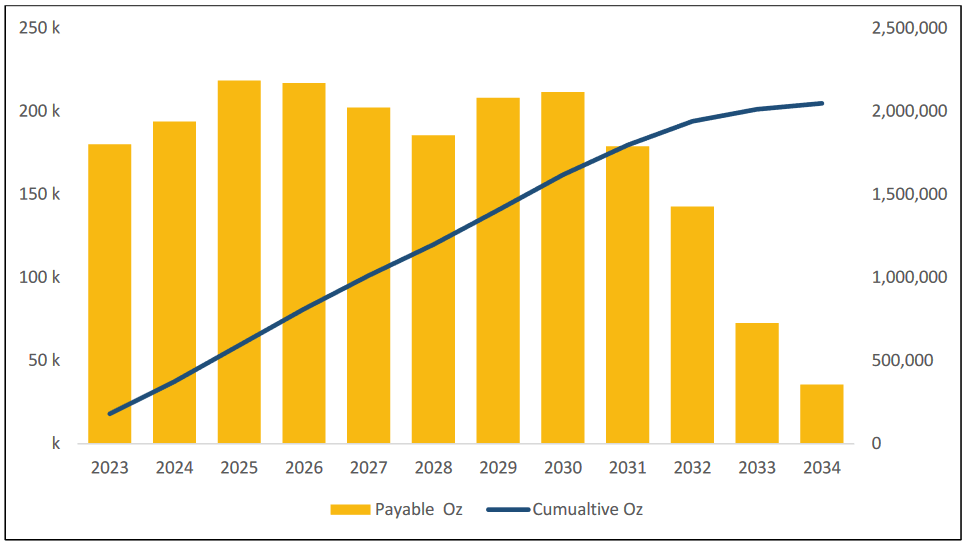

The second takeaway from said rainy weekend concerns the updated mine plan, keeping in mind the frequent promises of the so-called "Project 250" which was supposed to take annual production to 250Koz by 2023 by virtue of optimisation and de-bottlenecking of the existing operation. It seems that these grand plans have been quietly buried, and replaced by a mine plan that will try to achieve sustainable production of around 200Koz for the foreseeable future. The chart below illustrates annual gold output according to the latest mine plan.

{kind=link}

Annual and cumulative gold production, Eagle gold mine. (Technical report, filed April 2023)

The dip in 2028 may look benign in the chart above, but it leads to a very pronounced dip in the cash flow profile. It will be the main topic to be addressed in future iterations of this report, and bringing additional resources into the mine plan to flatten this dip looks like a high priority to us.

Taking all these and plenty more inputs at face value, the NPV(5%) computes to C$954M after tax, or $707.6M in the US denomination.

Exploration Success At Raven

Victoria Gold has invested significantly into near-mine exploration, testing several targets and releasing a maiden resource for the Raven deposit in September last year.

{kind=link}

Maiden Raven resource (September 15, 2022, news release)

The Raven deposit clearly was the focus of the 2023 summer exploration efforts with over 13,200m drilled and results for 16 out of the 39 holes were released on September 14. This latest data set is already pointing towards significant resource growth, and also seems to confirm a higher-grade zone which was identified last year around drill hole NG22-155C.

Clearly, this emerging discovery is good news for Victoria Gold and there is a high likelihood that the Raven deposit will add to the mine life of operations on the Dublin Gulch project. However, before we get too enthusiastic it's important to note, that mineralization has been described as " long intervals of gold mineralization [...] hosted within granodiorite lithologies punctuated by intervals of high grade massive sulphide veins ". Victoria Gold has not released any results of metallurgical studies for the Raven deposit, but it's probably a fair assumption that this ore will not be amenable to treatment on the existing heap leach infrastructure, and the company will have to invest in a mill to process ore from the Raven deposit. Consequently, the Raven deposit will most likely not serve as the means to flatten the 2028 dip in the production profile mentioned above.

Brewery Creek Acquisition

September 14 was a big day for Victoria Gold as the company not only released the above-mentioned drill results, but also the acquisition of the Brewery Creek project located about 55 km to the East of Dawson City in the Yukon. This acquisition makes sense from a broad geographical point of view as Victoria Gold already knows how to operate in the Yukon, although it's difficult to see too many direct synergies given the distances between the two sites.

A small heap leach operation produced gold at Brewery Creek in the 1990s, and subsequent owners of the project have defined a NI 43-101 compliant resource of just over 1M indicated ounces, plus a similar amount in the inferred category at Brewery Creek.

{kind=link}

Brewery Creek location map (Google maps, author's annotation)

Victoria Gold is purchasing the Brewery Creek project from Sabre Gold Mines ( OTCQB:SGLDF ), and for Sabre investors this deal probably raises some question marks. Sabre evolved from a 2021 business combination of Arizona Gold and Golden Predator. Shares traded around C$1 at the time, and investors were assured , the deal would create " a diversified near-term gold producer in North America ". Two years on, and the share price has dropped to 13 cents. Production at any of Sabre's projects is still a pipe dream, and Brewery Creek is changing hands for C$13.5M, after Sabre has invested a total of C$18.9M in the project.

Circling back to Victoria Gold now, we note that regardless of the merits of the Brewery Creek project, near-term benefits might lie elsewhere. To quote from the September 14 news release:

Golden Predator has reported non-capital losses of $44 million. Victoria expects certain tax-related synergies to be associated with the Transaction.

Overall, this looks like a distressed sale to us and we view this transaction as a net-positive for Victoria Gold, adding some incremental near-term value and some long-term optionality for a very reasonable price.

Valuation

Victoria Gold was trading for C$6.23 at the time of writing, translating into a C$414.5M market capitalization. Adding C$236.8M in net debt to the tally we compute an enterprise value of C$651.4M, or $483.1M in the US denomination.

Discounting all future optionality the market is putting a valuation of just 0.68xNAV on the Eagle Gold mine -- that is if we use the economic analysis from the latest technical report as a yard stick. This is a valuation deserving of a feasibility stage development project, and not that of a fully operational and cash flow generating mine.

Summary & Investment Thesis

We said in the introduction to this piece that we would ponder a change of sentiment regarding Victoria Gold's investment proposition in the light of a host of new data points. And ponder we did, arriving at two ways to look at the investment proposition offered by Victoria Gold's common shares.

- One could place a bet on Victoria Gold delivering on the operational and financial performance laid out in the technical report, and using this cash flow to pay down the debt and repair the balance sheet. All going to plan, this would see Victoria Gold debt free by the end of 2029 (already accounting for the lull in cash flow generation in 2028). A share price in the C$-double-digits would be a reasonable target in this case.

- Alternatively, one could extrapolate from the previous three years of operation. And in this scenario we would see a gold mining company with an asset that will most likely produce gold well beyond the current 12 year mine life; but we also see limited probability for this company to generate cash flow beyond the requirements to service its debt, after paying for the royalties to Osisko Gold Royalties ( OR ) and Franco Nevada ( FNV ).

We are leaning towards scenario 2 here, until we start seeing evidence of scenario 1 whereby Victoria Gold would be operating the Eagle mine to the specifications laid out in the latest report, and do so reliably. And to be clear, this will require substantial improvements over this year's performance which is currently set to achieve the lower end of the guidance. The technical report forecasts 20% higher gold production in 2024 when compared to the guided production for 2023, and at all-in sustaining costs 20% lower than this year. Sound like a steep task? We certainly think so.

And as we continue to view Victoria Gold as a vehicle to generate wealth primarily for its lenders and royalty holders, we can't help but circle back to our initial piece on Victoria Gold which we wrote back in March 2018, titled " Sell Victoria Gold After The Construction Financing ". The points raised five years ago still seem to be holding true to this day: the financing conditions of 2018 are still serving the financiers well, but they stand in the way of shareholders participation in the value created at the Eagle gold mine. Even the financiers themselves seem to have agreed to this thesis: Osisko sold its shareholdings to co-financier Orion Mine Financing in 2019, and Orion sold its stake to Coeur Mining ( CDE ) effectively dis-aligning the financiers from the shareholder. And by the way, Coeur sold down this stake in the course of 2022 thus ending all speculation of Coeur adding the Eagle mine to its porfolio. No other miner has stepped up since then to the best of our knowledge.

As it stands we see only speculative opportunities in the common shares of Victoria Gold. The share price tends to serve up speculative spikes as could be seen intermittently in the years since our initial post, but at the end of the day, reality checks in, and the share price is cut back to size. And for those ticking to a shorter time frame, the second half of this year might be a good point in time for such a speculative punt on a repeat of last year's winter season. We can't really see too much downside from the current market valuation of 0.68xNAV, the stronger half of the year has just started, and a repeat of last year's winter performance should get the market excited about Victoria Gold again.

In summary, we see little reason to invest in Victoria Gold with a long-term view; and we see an argument to place a speculative punt for some short-term gains.

For further details see:

A Reality Check For Victoria Gold