RDN - A Resilient Housing Market Makes Radian Attractive

2023-10-09 16:58:07 ET

Summary

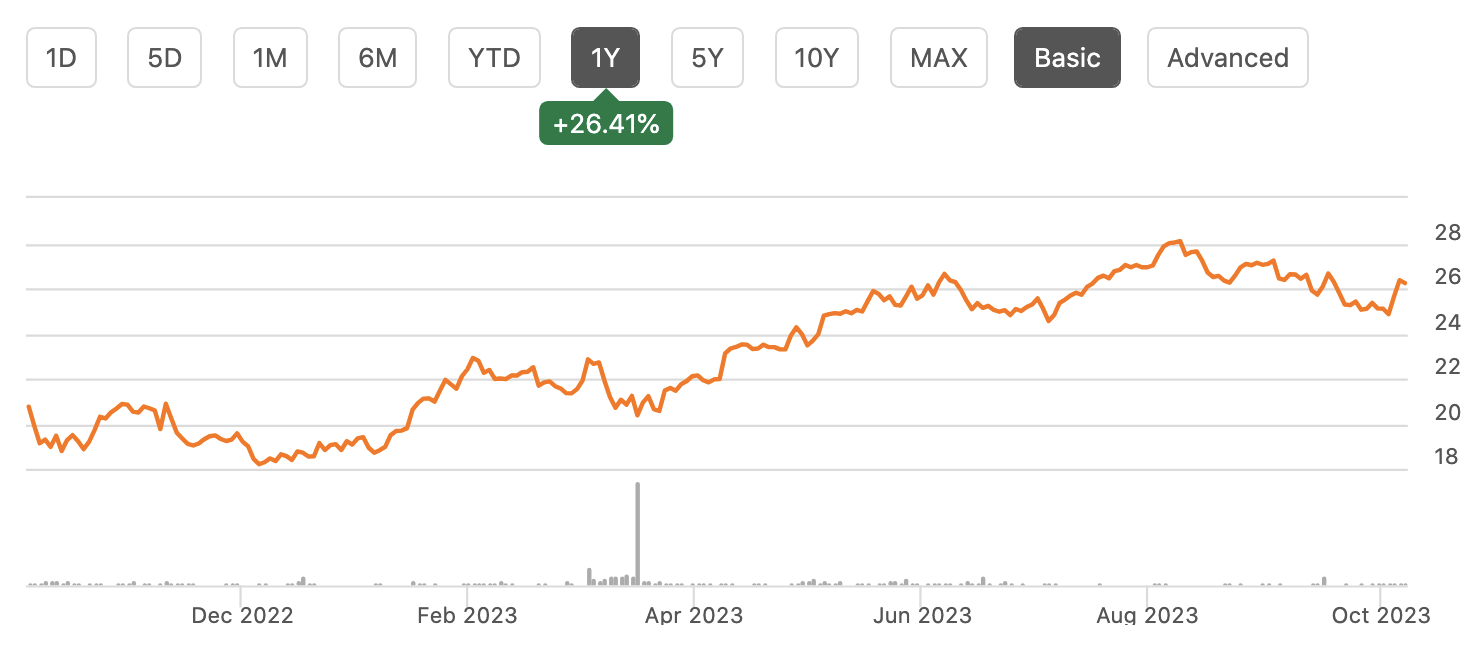

- Radian Group's shares have performed well, rising 26% in the past year, thanks to a firm housing market and reduced risk of losses on its insurance portfolio.

- Radian provides private mortgage insurance, allowing borrowers to obtain conforming mortgages with less than a 20% down payment.

- The company's strong performance, adequate reserves, and excess capital make it an attractive investment opportunity, with potential for a 15% return.

Shares of Radian Group (RDN) have been a strong performer over the past year, rising about 26%. While there have been concerns about housing, the market has remained firm, and the rise in prices have greatly reduced the risk of losses on RDN’s insurance portfolio. With shares trading around book value, I view them as attractive.

{kind=link}

Radian is a private mortgage insurer. The vast majority of mortgages in this country are insured by a government agency, primarily Fannie Mae or Freddie Mac. As a general rule in order to be a conforming mortgage to be insured by them, borrowers must meet several criteria, including putting 20% down. This is to provide Fannie and Freddie with protection from taking a loss in the event of a default—as the house would have to lose 20+% of its value for the mortgage to be underwater.

This is where companies like Radian step in. As a way to still get a conforming mortgage, a borrower can put less than 20% by purchasing private mortgage insurance (PMI). For example, a borrower could put 5% down. Radian, for a fee (either one-time or a monthly premium) will insure 15% of the home value, with Fannie/Freddie able to insure the rest. This enables buyers who lack the funds to make the down payment to buy a home though they have the added cost of the PMI premiums.

Eventually as principal is paid monthly and the mortgage falls below the 80% original loan to value level, the private mortgage insurance is closed, and the homeowner is left with just the regular mortgage payment. The potential losses PMI providers face are more sensitive to home prices than government insurance.

While home prices need to fall 20+% (in the event of default), for Fannie to face a loss, declines of just 3-5% could spark losses for Radian. Of course, if prices fall but the borrowers keep making payments, no loss is realized. A foreclosure/default needs to occur in addition to the price decline.

With this in mind, as we turn to the results, it is clear the company is performing strongly. In Radian’s second quarter , it earned $0.91 a share, which was down from $1.15 last year. This decline was because last year it released over $114 million from its reserves for insured losses. In the past quarter, reserve releases were $22 million. Smaller reserve releases are to be expected, simply because its reserves have fallen. They are now $379 million from $600 million last year. While I believe reserves are adequate and losses are likely to be quite low, further releases are likely to be small.

Beyond its reserves, Radian has $1.7 billion in excess capital supporting its private mortgage insurance, providing a roughly 40% cushion over its regulatory minimum.

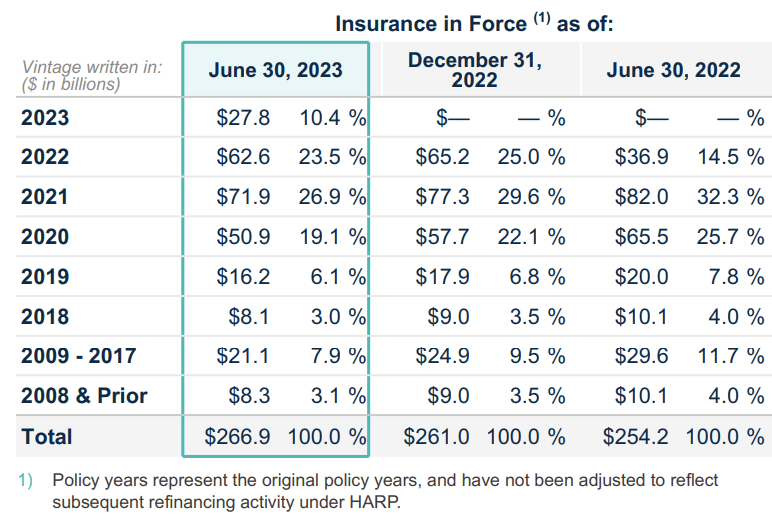

During the quarter, Radian wrote $17 billion in new policies, down from $19 billion last year. Housing transaction activity has slowed, so this decline in new business makes sense. Overall, Radian has $267 billion of insurance in force, up 5% from last year.

Radian’s reserves cover just 0.15% of its insured value, which may seem uncomfortably low. While I understand this reaction, given how the housing market has performed, Radian’s losses are likely to be consistent with this reserve level. Remember for Radian to face a loss, a homeowner a) must default and b) the house needs to be worth less than the remaining mortgage value. Below is a list of when Radian insured the home.

{kind=link}

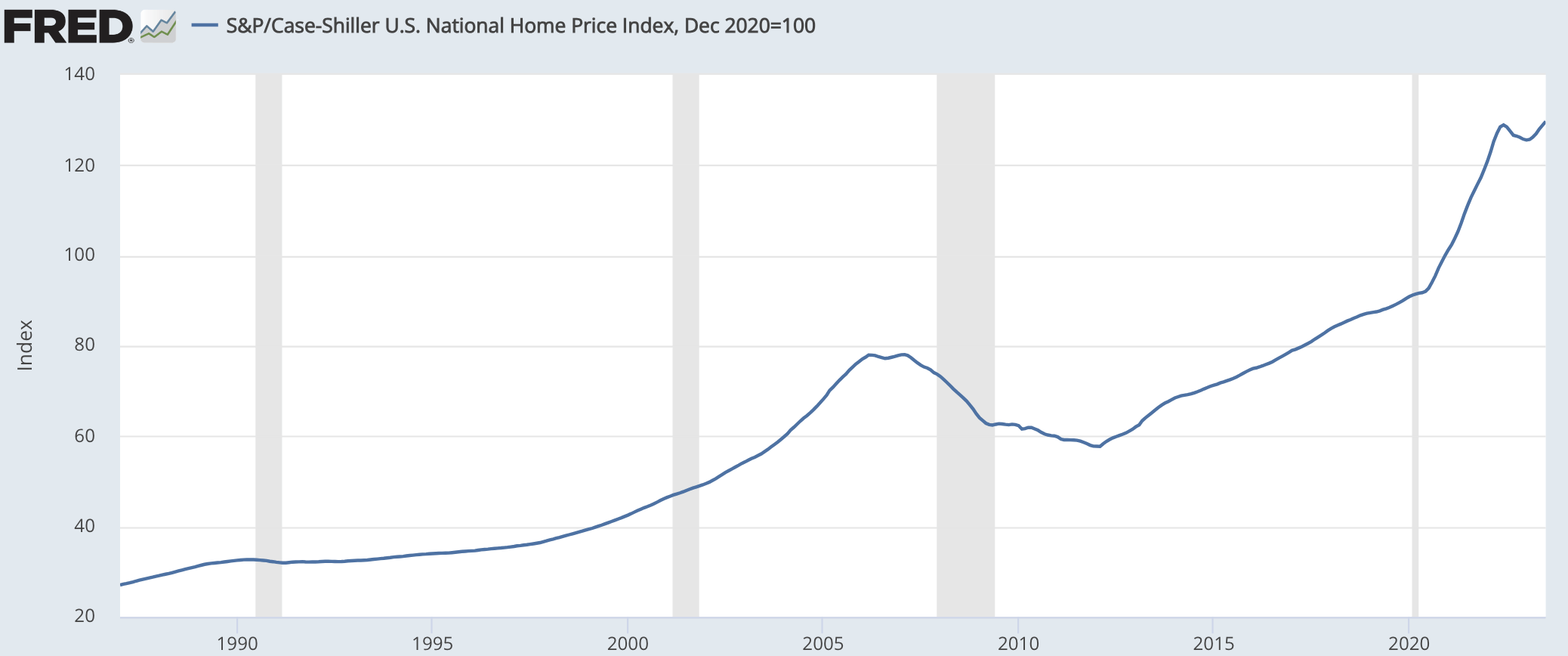

39% of Radian’s insured value comes from mortgages issued in 2020 or earlier. As you can see below, home prices are 30% higher today than at the end of 2020. We would need to a ~25% drop in home prices for prices to return to 2020 levels. Moreover, with each mortgage payment, the owner is paying down some mortgage principal.

Of course, not every home and every local market has performed as well as the nation, but we would need to see a dramatic collapse in home prices in order to create the potential for losses for Radian. With every month that passes without a crash, a little more principal is paid down, further reducing this risk on its legacy book. Peak to trough during the 2008 housing crisis, home prices fell 26%. It would take a repeat of the worst housing collapse in history to bring this 40% block of Radian’s business just to the precipice of facing any losses in my view. That is how much the rise in home prices has insulated the company, supporting low reserve levels.

{kind=link}

Home prices are also nearly 10% higher than the end of 2021, so even that 27% block of business has a health equity floor underneath it, though it is not impenetrable in the same way 2020 and earlier policies nearly are. Now, this still does leave about 34% of policies that have been issued since 2022, around current home prices. Of course with each month, the share of recent policies rises as Radian continues to write new business and older policies run-off, having paid down enough principal to no longer need PMI.

This is why I expect Radian’s reserve releases to slow. Reserves account for about 0.45% of 2022-2023 policies. Radian does not, and has never said, it runs a zero-loss business. Rather, the strong rise in home prices has created a legacy book of business that is nearly zero-loss, under all but the most severe scenarios, which has provided a nice tailwind and permitted reserve releases.

Importantly, I view Radian’s ongoing business activity as solid. As noted earlier, for PMI to face a loss: a) the borrowers need to default and b) the house needs to be sold for less than the remaining mortgage value. Credit defaults tend to rise during recessions and stay lower during economic expansions. As such, a recession is a risk for Radian, but the odds of one appears to be falling. The jobs market also remains strong with unemployment below 4%.

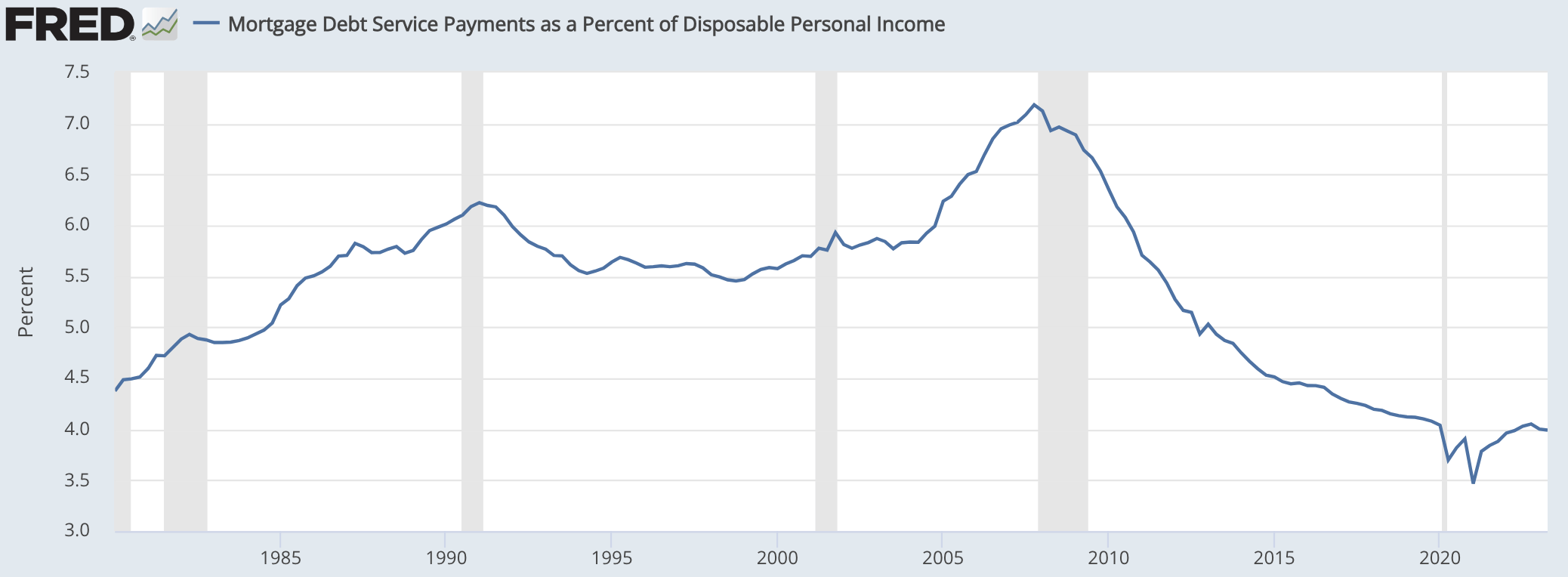

Moreover, it is important to note that mortgage payments as a share of income remain quite low by historical standards. Whereas homeowners were significantly stretching to buy homes into the lead-up of the housing crash, that has not occurred on an aggregate basis this cycle. As more people buy homes at today’s higher mortgage rates, I do expect this measure to rise. Still given how low it is, we are a significant way from worrying about over-levered borrowers, meaning even in an economic downturn, the rise in foreclosures should be less than average.

{kind=link}

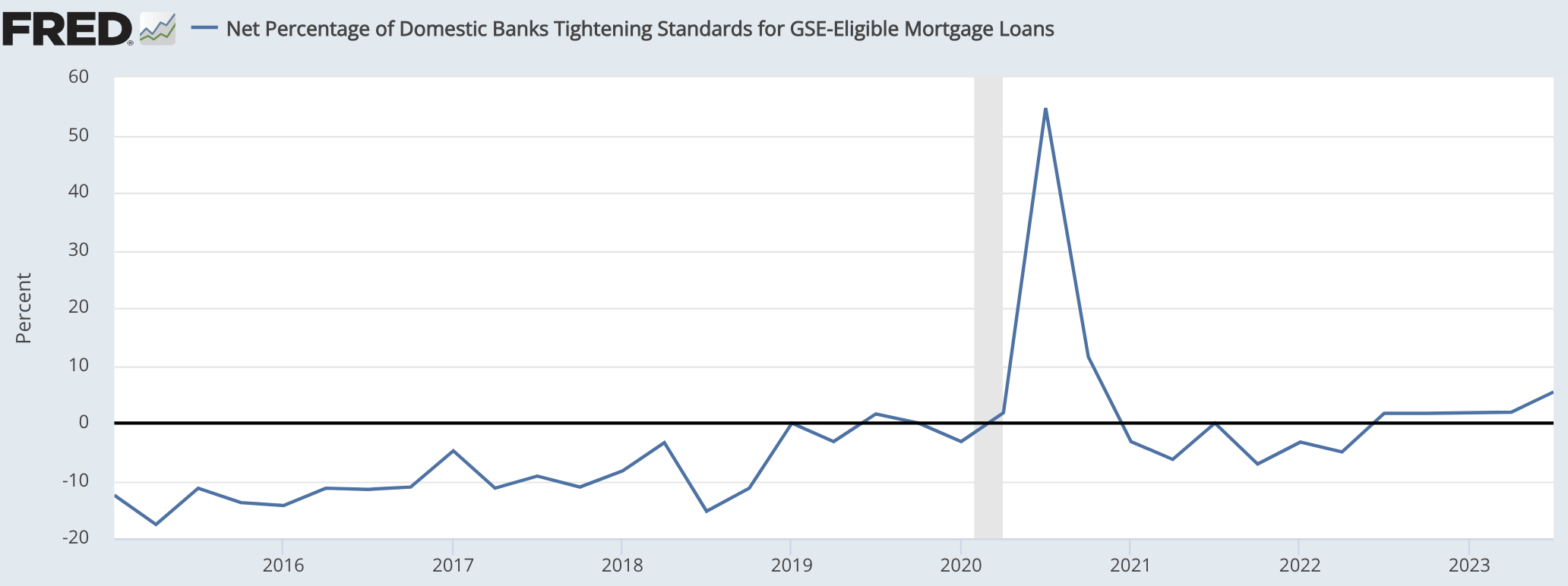

Further to this point, it is much more difficult to get a mortgage today than 15-years ago, and the fact the buyer mix has higher quality credit should also reduce default and delinquencies during the cycle. Banks tightened standards significantly during COVID and then eased them in 2021. However, since mid-2022, standards have begun tightening. These tighter standards create a favorable buyer mix for Radian’s insurance, reducing the risk of foreclosure.

{kind=link}

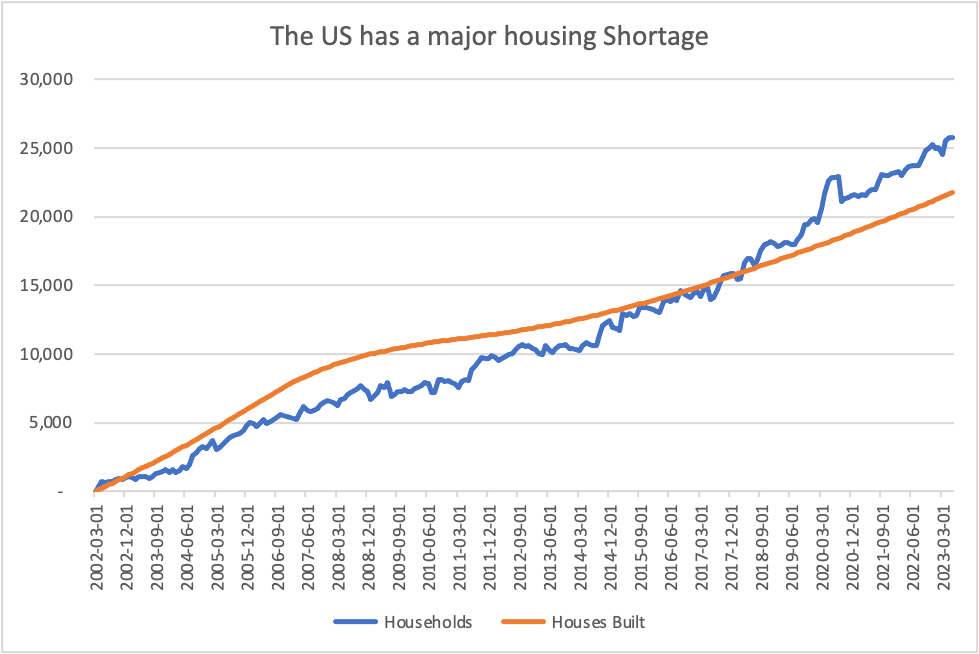

For these reasons, I would expect foreclosure activity to remain relatively muted. Now, if home prices stay strong, even if you are struggling to make payments, you can sell your house and move rather than face down foreclosure. As you can see from the earlier chart, while prices did fall a little in H2 2022 when higher rates caused buyers to step back from the market, they have since recovered toward an all-time high. I am structurally bullish on the housing market, for the simple but powerful reason we do not have enough homes.

As you can see below, we have created 4 million more households than new homes over the past twenty years. 2008 was fundamentally different—due to the surge in construction, we had overbuilt housing relative to the population. However because of how little building happened after the rise, population growth has caught up and exceeded home construction.

{kind=link}

Markets that have tight supply have more buoyant pricing as there is a backlog of buyers waiting in the wings to get in. This is a reason why housing has held up better than most expected over the past year in my view. Some buyers could only wait out higher rates for so long before life events (moving jobs, having a child, etc) led them to buy a house. This lack of housing is why so many homes sell so fast or have seen multiple bids.

This pent-up demand for housing in my view should keep prices at least around current levels, even with the rise in rates. The ability to sell your house reduces foreclosure risk, and it should also reduce the severity of any losses Radian does face. Moreover, the fact home prices have risen may make it harder for some households that previously could put the 20% down to still do so. As such, homebuyers who previously had too strong of a credit profile to need PMI, may now only put 10-15% down and buy a policy from Radian, creating a positive mix shift in the customers it insures. For these reasons, I expect the policies it is writing now to be strongly profitable.

Like other insurers, Radian maintains an investment portfolio with the premiums it receives, which totals $5.9 billion. Net investment income rose $17 million to $64 million in the quarter as book yield was 4% from 3.8%. This is because the company invests in fixed income securities, and as rates have risen, it is able to reinvest the portfolio into higher-yielding bonds, given the Fed’s rate increase.

This tailwind should continue over the next few years as short-term investments and debt due within the next year mature. Moreover, 40% of its portfolio is in asset-backed and mortgage securities. These securities are amortizing, meaning some principal is paid down every month in addition to interest. So while they do not mature at one time, these periodic partial principal payments can be reinvested at higher yields, gradually bringing book yield higher.

Radian

I would also emphasize this is an extremely high-quality portfolio. 38% of the portfolio is AAA-rated or government debt. Only 1.2% of the portfolio is below investment grade. This portfolio is unlikely to face material credit losses. This is a prudent allocation. By the nature of its business, Radian has exposure to economic downturns, as insurance claims could rise during recessions as foreclosures occur. The company would not want to face stress in its investment portfolio at the same time it faces potentially higher payouts.

Radian

In addition to the excess capital held at the operating company, Radian has $1 billion of liquidity at the holding company. With these resources, RDN can continue to return capital to shareholders. It has a 3.4% dividend yield. There is also a remaining $280 million repurchase authority. RDN bought back $5 million in the quarter. The share count is down about 23% since the end of 2019, and I would expect to see opportunistic repurchases.

Over the past year, book value rose 12% to $26.51. That growth in equity has also reduced financial leverage, with debt to capitalization falling to 25.3% from 26.4% last year. Its book value includes unrealized losses of $424 million on its investment portfolio from the rise in rates. Given strong operating cash flows, I believe it does not need to sell these and can wait for them to gradually pull back to par. Excluding this, book value is about $29.20.

Given my view we will see reserves hold about flat, due to resilience in the housing market, and see investment income continue to gradually rise as bonds mature, the company should be able to earn about $3.40-3.50 over the next year for a 7.6x earnings multiple.

That is an attractive entry point in my view, given the sustainability of earnings. I believe shares should at least be able to trade to book value, ex unrealized losses, providing ~11.5% upside, creating a 15% return opportunity with the dividend. Radian shares should be bought.

For further details see:

A Resilient Housing Market Makes Radian Attractive