PTY - A Safer Way To Retire At 55 With $2 Million

2023-11-22 07:35:00 ET

Summary

- $1 million isn’t what it used to be, but will $2 million be enough to retire at age 55?

- You could use just long-term Treasuries to generate the income for a comfortable retirement.

- There's a way to generate more income and more cushion with that same $2 million.

Co-authored with PendragonY

For Americans reaching or beyond retirement age, their income in retirement will be structured to take advantage of using the interest and returns from the money they have saved for retirement. The idea is that by the time you near retirement, you have enough saved up so that you can coast indefinitely. For younger Americans, the goal is to save enough to reach that point before they get to their targeted retirement age.

When I first joined the workforce, saving a million dollars was thought to be enough to provide income independence. After all the inflation in the past 40 years, a million dollars just isn't what it used to be.

Today, rather than a million dollars, it looks like the goal should be somewhere around $2 million.

What will $2 million get you?

A retirement fund of $2 million put entirely in fairly safe long-term Treasury bonds can provide $80,000 in annual income. A 50/50 mix of 10 and 20-year Treasury bonds yields ~5% at current prices, and without even touching the principal it would start with 20% more income than you need (so you can allow for inflation). While this amount may sound sufficient, you’ll contend with taxes, medical expenses, and inflation during retirement.

So, is $2 million enough to retire at 55-years-old? That depends on how long you might live and how much income you need to pay for your lifestyle. The Bureau of Labor Statistics estimates the average 65-year-old spends about $52,000 annually in retirement. While this number very much depends on where you choose to live (both location and home size), one would think that 1.5 times the average spending can provide a comfortable retirement in much of the country. Plus, even with the very safe option of Treasuries only, you start with a $20,000 cushion.

The 4% Withdrawal Rule or The Income Method

In investing, as in many things, being too aggressive by taking too many risks can often lead to poor outcomes. What many people don't realize is that being too passive by not taking enough risks also can lead to poor outcomes.

In selecting a mix of 20-year and 10-year Treasuries for the safe option, I did so to limit some of the risks in using Treasuries. Some people think investing in Treasuries is risk free – it isn't. While investing in Treasuries carries a minuscule credit risk, there are still other risks. Recently, with the Fed increasing interest rates we saw one of the biggest risks with Treasuries – interest rate risk. As interest rates rise, the price of existing Treasuries drops so that the old and new bonds have similar yields. The longer until the bond matures, the bigger this price drop is (the price drop has to make up more cash until maturity as the number of years to maturity increases).

This is why we've seen ETFs filled with Treasuries fall dramatically over the past three years.

Guaranteed interest and guaranteed repayment of principal is not a guarantee that the price won't drop. A retiree might "feel" better if their investment is in something that doesn't change in price, like say a CD. But the only reason a CD doesn't change in price is because it isn't publicly traded. You can't sell it if you decide there's a better opportunity. With Treasuries, you at least have the option to sell, but that also means that the price can fall, and as we've seen over the past three years, the price can fall a lot. Then when holdings mature, you are forced to reinvest at whatever the going interest rate is. That might be higher, but it also could be lower. Your income is only protected until maturity.

The other big risk that Treasury investments face is inflation risk. The interest and principal are all paid in nominal dollars, which can drop a lot if inflation is high. It's just like we have seen over the last few years. If you have a portfolio of 20-year bonds, your income isn't going to be growing very quickly. Bond investors will often "ladder" their maturities to ensure that they have maturities every single year, allowing them to reinvest at current rates. This requires striking a balance between too many maturities in one year creating the risk that rates are low that year and reinvesting at a lower rate results in a decline of income. Or not having enough maturities, and when rates are high, being unable to grow your income as much as you need to fight inflation because only 5%-10% of your portfolio is maturing.

These risks are why you shouldn't put the whole portfolio into 20-year bonds (and get 5.2% yield) and why you need to plan to have excess income as a cushion (both in case expenses ran higher than expected and to buy new assets). With $2 million, you could create a reasonable portfolio of Treasury bonds, mixing various maturities and laddering properly, you can ensure that you have a reasonable income and insulate yourself from rate and inflation risks. But is this being too cautious?

We use The Income Method for our retirement portfolio. This method focuses on buying shares of companies and funds that have a generous well-covered distribution and trade at attractive prices. We aim for a yield of 9%-10%. Our Model Portfolio does that. This is certainly a more aggressive strategy than investing in long-term Treasuries but it has the potential to generate $135,000 for living expenses with a cushion of $45,000 to protect and grow that income stream.

Which strategy is better? The Treasury Portfolio has more exposure to interest rates, inflation risks, and related price risks. For example, when interest rates go up, Treasuries take a big hit. Our "model portfolio" also has exposure to price risk in case of a market dip. Both portfolios can be managed to mitigate the risks to which it is most exposed, but the reality is that risk cannot be avoided.

An investment in equities will have more price volatility, it will have more dividend risk because dividends can be cut for a variety of reasons, some of which have nothing to do with macroeconomic conditions.

However, our retirement portfolio provides more income and much more cushion than the same amount invested in a Treasury-only portfolio. Our retirement portfolio is also very well diversified with 45-plus high dividend stocks in order to mitigate for any individual stock risk.

A Case Study

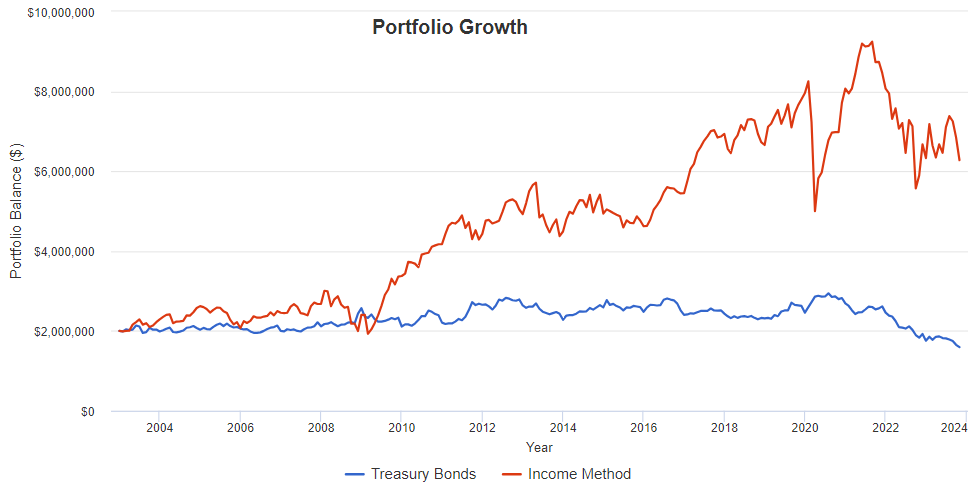

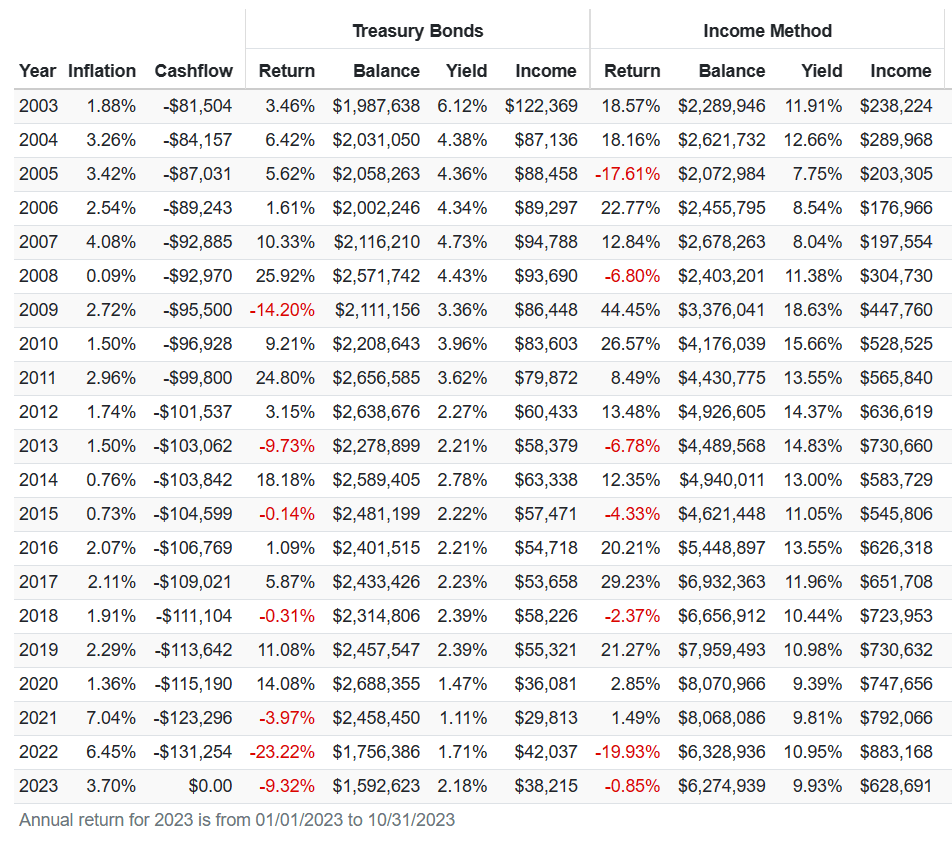

Let's look at a comparison using Portfolio Visualizer for a simplified Treasury portfolio vs. a simplified Income Method portfolio. We will use iShares 7-10 Year Treasury Bond ETF ( IEF ) and iShares 20+ Year Treasury Bond ETF ( TLT ) to simulate a portfolio that holds both mid-term and long-term Treasuries. On the Income Method side, we will use two of our picks that aren't performing at their best right now. In fact, both are trading near COVID panic prices, both have experienced multiple dividend cuts. We will use PIMCO Corporate & Income Opportunity Fund ( PTY ) and Annaly Capital Management ( NLY ). We will look at a period starting January 2003, assume an initial investment of $2 million, and a withdrawal of $80,000 year one and adjusting withdrawals for annual inflation (following the "4% rule"). Any excess income is reinvested.

Which do you think did better through the GFC, COVID, high inflation, and now the fastest interest rate hiking cycle in decade s?

{kind=link}

Portfolio Visualizer

By portfolio value, it isn't even close and hasn't been for decades. Note that both NLY and PTY are trading at lower share prices than they were in January 2003:

Yet according to Portfolio Visualizer, a $2 million investment in these two stocks and withdrawing $80,000/year would end with a portfolio value of around $6.3 million, while an investment in Treasury Bonds would have a value of approximately $1.6 million. How is that possible? From the massive amount of excess income that NLY and PTY produced which could be reinvested.

{kind=link}

Portfolio Visualizer

Every year, the income investor was able to buy more shares with the excess income. This created an even larger cushion, even more available for reinvestment, and allowed for growing the overall size of the portfolio despite declining prices. The investor that chose the "safe" route of Treasuries found themselves using most of the income to fund their lifestyle and didn't have a lot to reinvest. As a result, income declined as interest rates declined, and only recently started climbing again.

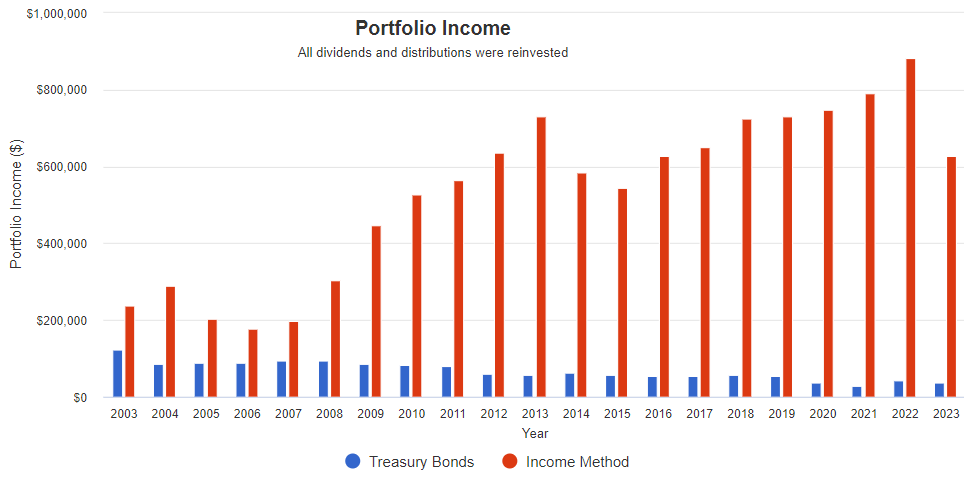

Here's a look at the numbers. Note that initially, Treasury Bonds were able to cover the cash flow needs, but as rates declined it was inevitable that the yield was unable to keep pace with inflation.

{kind=link}

Portfolio Visualizer

Meanwhile, the Income Method grew its income, and despite some dividend cuts and setbacks, the excess income was enough to reinvest. By 2022, $883k in income was 6.7x the cashflow needs. In reality, the Income Method investor could have very comfortably increased their personal spending.

While it's great if you built enough wealth to generate a large enough income from Treasuries to support your spending needs, too many retirees are living unnecessarily on shoestring budgets. You worked hard for your money - you deserve to enjoy it.

Other Considerations

According to the Social Security Administration, a 65-year-old man can expect to live for another 19 years, while a 63-year-old woman can expect to live to age 86 (23 years). This is partly why I put half of the Treasury portfolio into 20-year bonds. Even if one retired at 55, buying 20-year bonds would cover much of their retirement. This also will give the retiree plenty of time to sell the 10-year bonds early and use that cash to buy bonds that will produce more income. With the Income Method portfolio producing extra cash at the start of retirement, this likely retirement of 20-plus years gives these extra assets plenty of time to boost income to cover the full retirement period.

While this isn't an issue if one retires at 50 or at any time before 65, once the retiree begins to take Medicare, the extra income our portfolio generates will result in higher premium costs. The extra cash will more than cover the extra costs, but that's something that should be planned for.

The final consideration is that while I have presented each option separately, there's no reason why an investor can't do some of both. In fact, since each of the portfolios, Treasury-Only and our Income Method, are more exposed to different types of risks, one can combine them and have lower exposure to each type of risk than the portfolio most exposed to that risk. I like to call this embracing the power of further diversification, which results in significantly higher income. This also could lower the risk for a Treasury portfolio when interest rates go up.

Conclusion

The answer to the question posed at the start of the article, can you retire on $2 million, is yes. Even with taking very few risks, this will generate enough cash to pay for a comfortable retirement. But, taking just a bit more risk (and managing the investments more actively), you can have an even more comfortable retirement, even if you didn't save $2 million. You can start that retirement even before you reach full (or even early) retirement age.

When it comes to retirement, you don't want to simply survive financially, you want to thrive. By taking on slightly more risk, you can unlock profoundly more income. This additional income can help you have a great cushion against unexpected expenses, allow you to grow your income more rapidly, and enjoy life without having to stress over every dollar.

The Model Portfolio provides more than 80 picks with yields in excess of 9% on average. This portfolio built using our unique Income Method provides income for countless retirees. One can build an income portfolio using the Income Method to supercharge retirement finances and planning.

That's the beauty of my Income Method. That's the beauty of income investing

For further details see:

A Safer Way To Retire At 55 With $2 Million