FXY - A Seismic Shift For Global Financial Markets - The BOJ Starts Monetary Tightening

2023-07-28 12:58:25 ET

Summary

- The Bank of Japan has taken steps to tighten its monetary policy, marking the beginning of the end of extreme easing.

- This shift could lead to an increase in global interest rates as Japanese investors sell foreign bonds and buy domestic bonds.

- The Yen carry trade could unravel, causing a selloff in risk assets as the Japanese Yen strengthens.

The Bank of Japan surprised the markets on July 28 and made an initial step to tighten the monetary policy. This marks the beginning of the end of the most extreme monetary policy easing in the developed world, and as I will explain, this is a seismic shift for global financial markets.

First of all, what actions did BOJ take?

The BOJ governor Ueda Kazuo said after the BOJ meeting:

"Taking account of extremely high uncertainties for economic activity and prices, we agreed that it is appropriate to enhance the sustainability of monetary easing under the current framework by conducting YCC with greater flexibility and nimbly responding to both upside and downside risks to Japan's economic activity and prices."

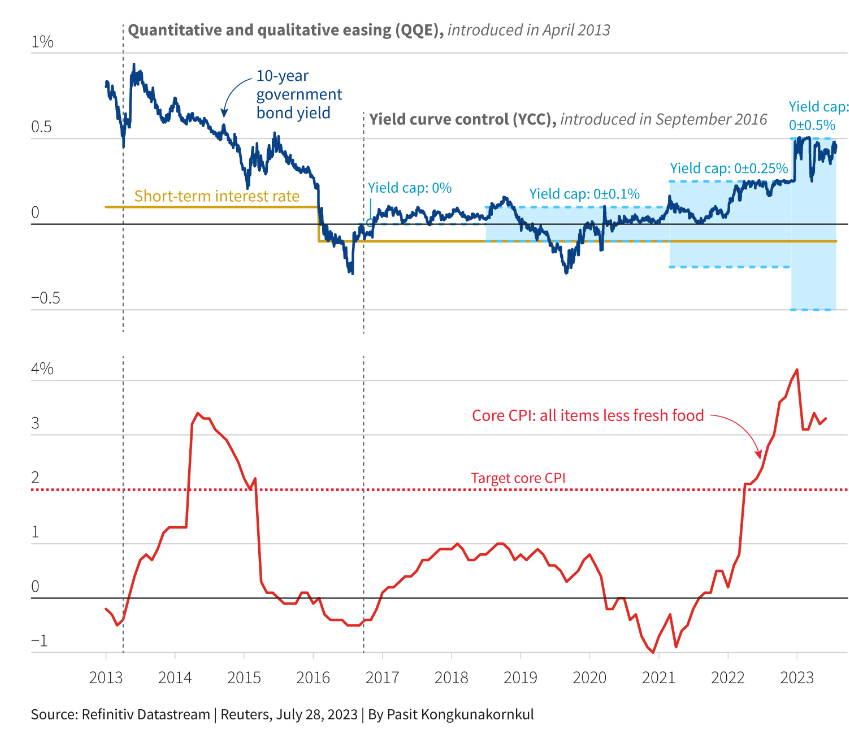

The chart below illustrates the BOJ action.

- First, the BOJ has the short-term interest rate at 0.1% from 2012 to 2016, while the 10Y JGB (Japanese Government Bond) rate was more or less flexible, with the yield ranging between 0.5% and 1%.

- In 2016, while facing deflation, the BOJ lowered the short-term interest rate to -0.1% and fixed the 10Y JGB yield at 0% - this was the introduction of the policy called the Yield Curve Control, or YCC.

- As core inflation increased towards the 1% level, the BOJ widened the range for 10Y JGB up to 0.1%, while keeping the short-term rate at -0.1%. Note, the BOJ's target for core inflation is 2%, so given that core inflation was still well below the target, the BOJ kept the monetary policy easing via the YCC.

- In 2021, the BOJ widened the range for 10Y JGB up to 0.25%, leaving the short-term rate at -0.1%.

- Just recently, the BOJ again widened the range for 10Y JGB up to 0.50%, as inflation spiked well above the 2% target to above 4%. The speculation was that this would not be sufficient to lower inflation, and that the BOJ would have to more aggressively tighten monetary policy by abandoning YCC.

- Just yesterday, the BOJ widened the range to allow the 10Y JGB interest rate to rise up to 1%, with core inflation still well above the 2% target at 3.2%.

- The short-term interest rate remains at -0.1%.

- Thus, this BOJ action could be interpreted as the beginning of the end of the most extreme monetary policy stimulus, during the period when other global central banks have already significantly tightened their policy actions.

{kind=link}

Why is this a seismic shift for global financial markets?

There are two major reasons why the actions taken by the BOJ could be a major problem for the global financial markets:

- Increase in global interest rates

First, there is a fear that Japanese investors would start to sell their global investments in bonds to invest in domestic bonds. Specifically, given that interest rates in Japan have been at 0%, Japanese investors were searching for higher yields internationally. They are the biggest holders of Treasuries outside the US, with the 15% share of all US Treasuries held by foreigners. They also own of 10% of Australian bonds and Dutch bonds, 8% of New Zealand’s bonds and Brazil's bonds.

Thus, the fear is as Japanese investors sell their foreign bonds, and buy domestic bonds, the global interest rates would increase, providing a major headwind for global economic growth.

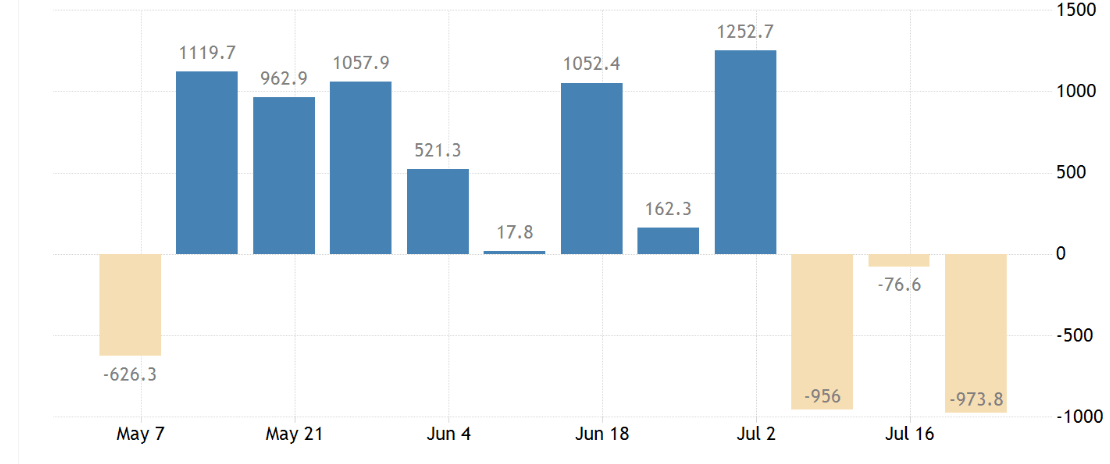

In fact, Japanese investors have already started selling foreign bonds over the last three months, with JGB's yielding 0.5%. As the JGB yield rises towards the 1%, the selling could intensify.

{kind=link}

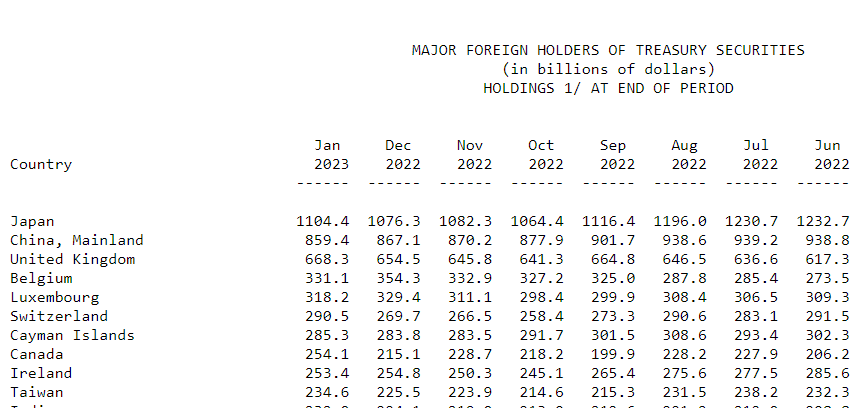

The US is particularly vulnerable due to the fact that Japanese investors hold over $1 trillion of US Treasuries, or nearly 15% of total share. This is particularly important given that China is in second place with $860 billion, and China could also be selling US Treasuries due to the geopolitical situation. Thus, the selling pressure on US Treasuries could be very high, during the period when the Fed is implementing QT, while the US government is increasing the supply of Treasuries.

{kind=link}

- The Yen carry trade

The second risk related to the BOJ action is the blow up in the Yen carry trade. Specifically, given that interest rates were so low in Japan, international investors had the opportunity to borrow in Yen with near 0% interest rate, and invest in higher yielding assets globally. This benefited emerging markets ( EEM ), emerging market currencies, and all risk assets globally, including speculative US stocks.

The unhedged (or naked) Yen carry trade works as long as the Japanese Yen ( FXY ) does not appreciate, as the Yen appreciation could cancel the yield differential and more.

The BOJ action, and related selling of foreign bonds by Japanese investors, could significantly boost the Japanese Yen, and cause the selloff in all risk assets ( SPY ) ( QQQ ) as the Yen carry trade unwinds.

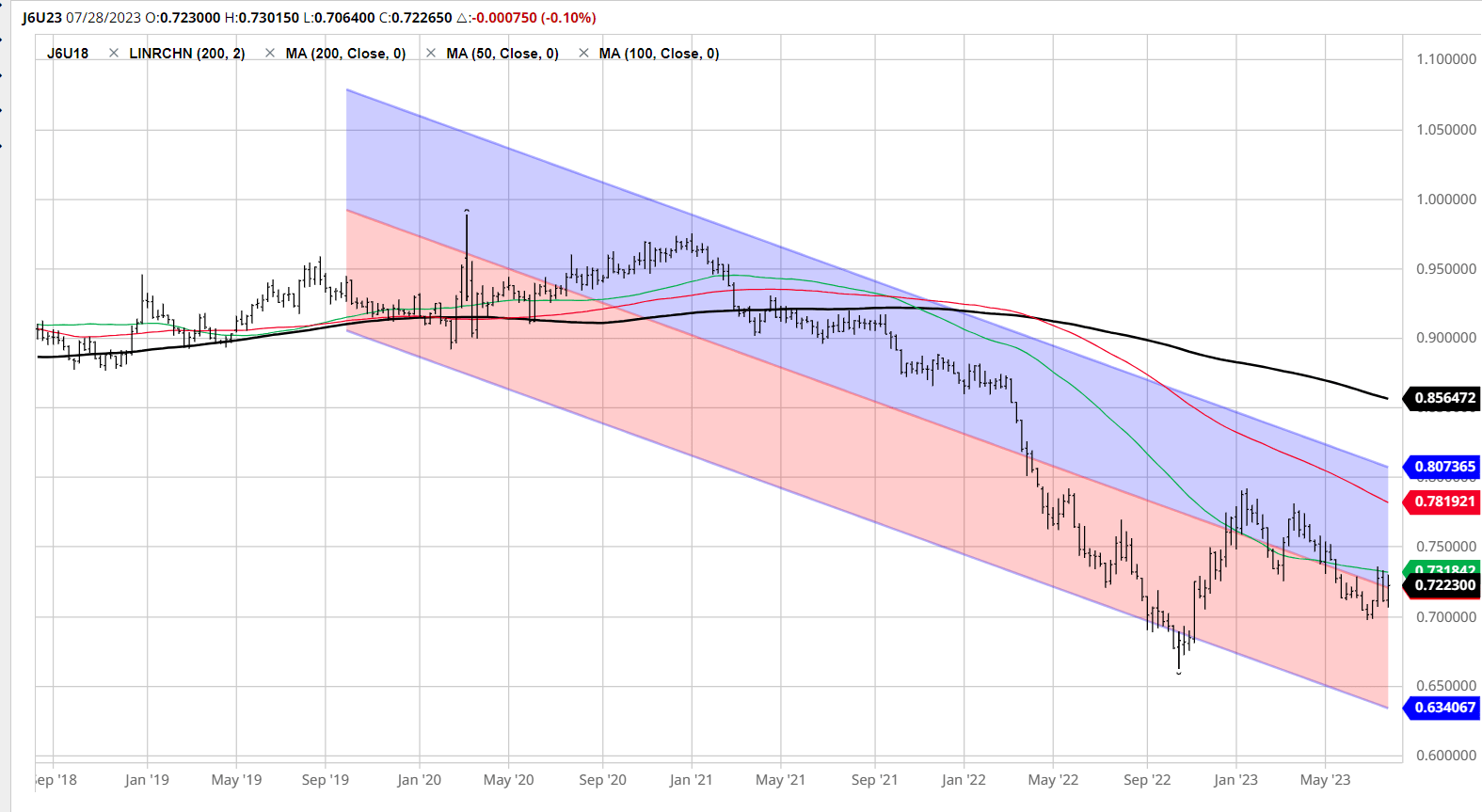

The Japanese Yen has been weakening since 2021 as the Fed has been tightening monetary policy, while the BOJ was still in the monetary easing mode. This provided a boost to the US assets via the Yen carry trade. The Japanese Yen bottomed in 2022 as the BOJ initially widened the JGB range to 0.5%. The further widening of the JGB yield to 1% could push the Yen towards 1.00000, and this could be a major headwind to US risk assets as the Yen carry trade unwinds.

{kind=link}

Implications

For the initial stage, the BOJ action could negatively impact US Treasuries ( TLT ). The sustained spike over the 4% yield on 10Y Treasury Bond could intensify the selling and push the yield towards the 5% level. Thus, at this point I would not be buying US long term bonds, and I prefer short duration ( SHY ) such as 3-month Bills yielding 5.44% annualized. However, given the high risk of a global recession, I would not be short long-term bonds either.

For further details see:

A Seismic Shift For Global Financial Markets - The BOJ Starts Monetary Tightening